PROBLEM 6.10

1. Purchase.

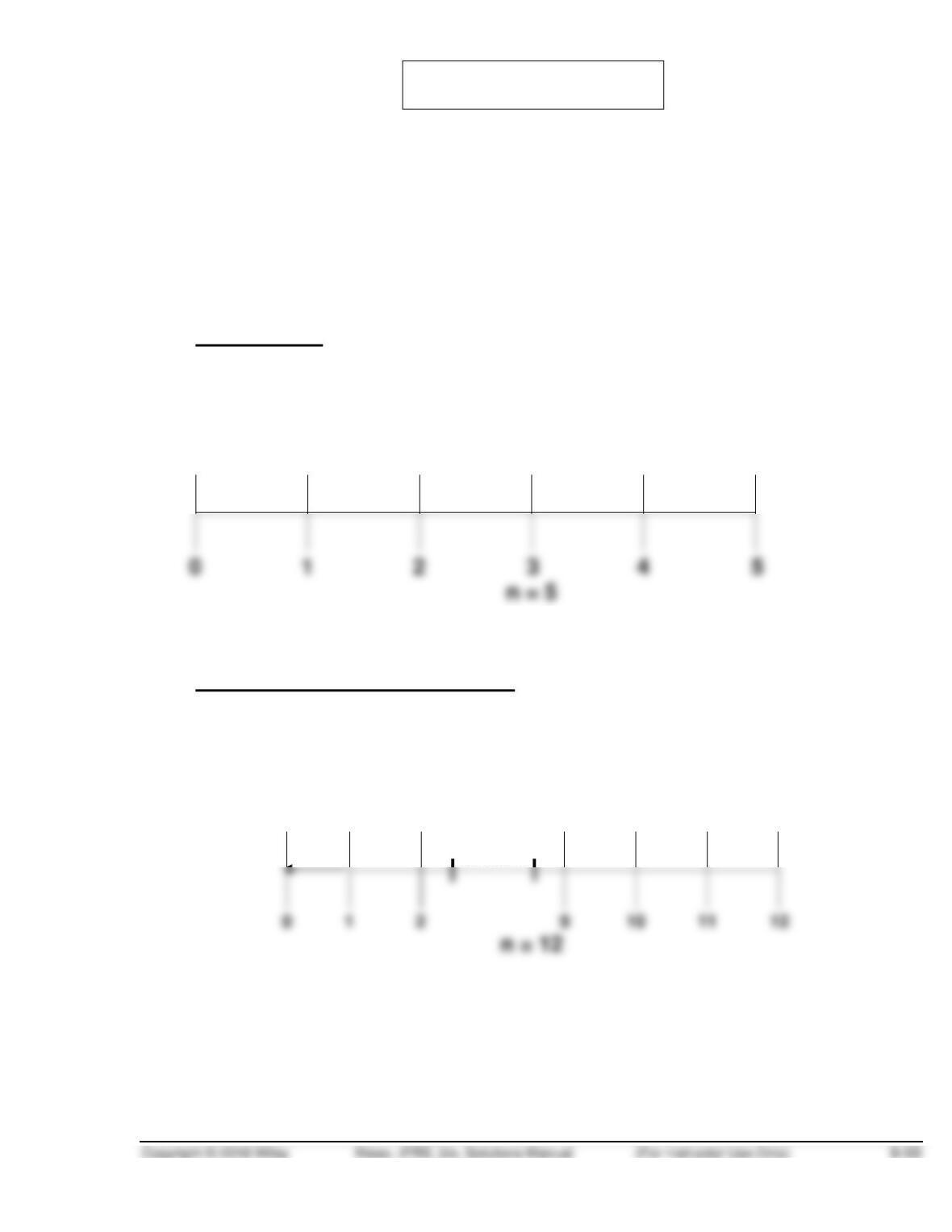

Time diagrams:

Installments

i = 10%

PV – OA = ?

R =

$350,000 $350,000 $350,000 $350,000 $350,000

Property taxes and other costs

i = 10%

PV – OA = ?

R = $40,000 + $16,000

$56,000 $56,000 $56,000 $56,000 $56,000 $56,000

PROBLEM 6.10 (Continued)

Insurance

i = 10%

PV – AD = ?

R =

$27,000 $27,000 $27,000 $27,000 $27,000 $27,000

Residual Value

i = 10%

PV = ? FV = $500,000

Formula for installments:

PV – OA = R (PVF – OAn, i)

PROBLEM 6.10 (Continued)

Formula for property taxes and other costs:

PV – OA = R (PVF – OAn, i)

Formula for insurance:

PV – AD = R (PVF – ADn, i)

Formula for residual value:

PV = FV (PVFn, i)

PROBLEM 6.10 (Continued)

Present value of net purchase costs:

Down payment………………………………………………..

$ 400,000

Installments ……………………………………………………

Property taxes and other costs ………………………..

Insurance ……………………………………………………….

202,367

Total costs ……………………………………………………..

$2,310,711

Less: Residual value ………………………………………

159,315

2. Lease.

Time diagrams:

Lease payments

i = 10%

PV – AD = ?

R =

$270,000 $270,000 $270,000 $270,000 $270,000

Interest lost on the deposit

i = 10%

PV – OA = ?

PROBLEM 6.10 (Continued)

Formula for lease payments:

PV – AD = R (PVF – ADn, i)

Interest lost on the deposit per year = $100,000 (10%) = $10,000

PV – OA = R (PVF – OAn, i)

PV – OA = $10,000 (PVF – OA12, 10%)

PV – OA = $10,000 (6.81369)

PV – OA = $68,137*

PROBLEM 6.11

(a) Annual retirement benefits.

Jean–current salary

£ 48,000

X 2.56330

(future value of 1, 24 periods, 4%)

123,038

annual salary during last year of

work

X .50

retirement benefit %

Colin–current salary

£ 36,000

X 3.11865

(future value of 1, 29 periods, 4%)

112,271

annual salary during last year of

work

X .40

retirement benefit %

£ 44,909

annual retirement benefit

Anita–current salary

£ 18,000

annual salary during last year of

work

X .40

retirement benefit %

£ 15,169

annual retirement benefit

Gavin–current salary

£ 15,000

X 1.73168

(future value of 1, 14 periods, 4%)

annual salary during last year of

work

X .40

retirement benefit %

£ 10,390

annual retirement benefit

PROBLEM 6.11 (Continued)

(b) Fund requirements after 15 years of deposits at 12%.

Jean will retire 10 years after deposits stop.

£ 61,519 annual plan benefit

[PV of an annuity due for 30 periods – PV of an

X2.69356 annuity due for 10 periods (9.02181 – 6.32825)]

£165,705

£ 44,909

annual plan benefit

due for 15 periods (9.15656 – 7.62817)]

£ 68,638

Anita will retire 5 years after deposits stop.

£ 15,169

annual plan benefit

X4.74697

[PV of an annuity due for 25 periods – PV of an annuity

due for 5 periods (8.78432 – 4.03735)]

£ 72,007

£ 10,390

annual plan benefit

(PV of an annuity due for 20 periods)

PROBLEM 6.11 (Continued)

£165,705

Jean

68,638

Colin

(c) Required annual beginning-of-the-year deposits at 12%:

Deposit X (future value of an annuity due for 15 periods at 12%) = FV

Deposit X (37.27972 X 1.12) = £393,270

PROBLEM 6.12

(a) The time value of money would suggest that NET Life’s discount rate

is substantially higher than First Security’s. The actuaries at NET Life

(b) As the controller of STL, Buhl assumes a fiduciary responsibility to

the present and future retirees of the corporation. As a result, he is

responsible for ensuring that the pension assets are adequately

(c) If STL switched to NET Life

The primary beneficiaries of Buhl’s decision would be the corporation

and its many shareholders by virtue of reducing £8 million of annual

pension costs.

The present and future retirees of STL may be negatively affected by

If STL stayed with First Security

In the short run, the primary beneficiaries of Buhl’s decision would be

the employees and retirees of STL given the lower risk pension asset

plan.

PROBLEM 6.13

Cash Flow Probability

Estimate X Assessment = Expected Cash Flow Present Value

2020 $ 2,500 20% $ 500

4,000 60% 2,400

5,000 20% 1,000 X PV

Factor,

2022 $ 4,000 30% $1,200

6,000 40% 2,400

7,000 30% 2,100 X PV

Factor,

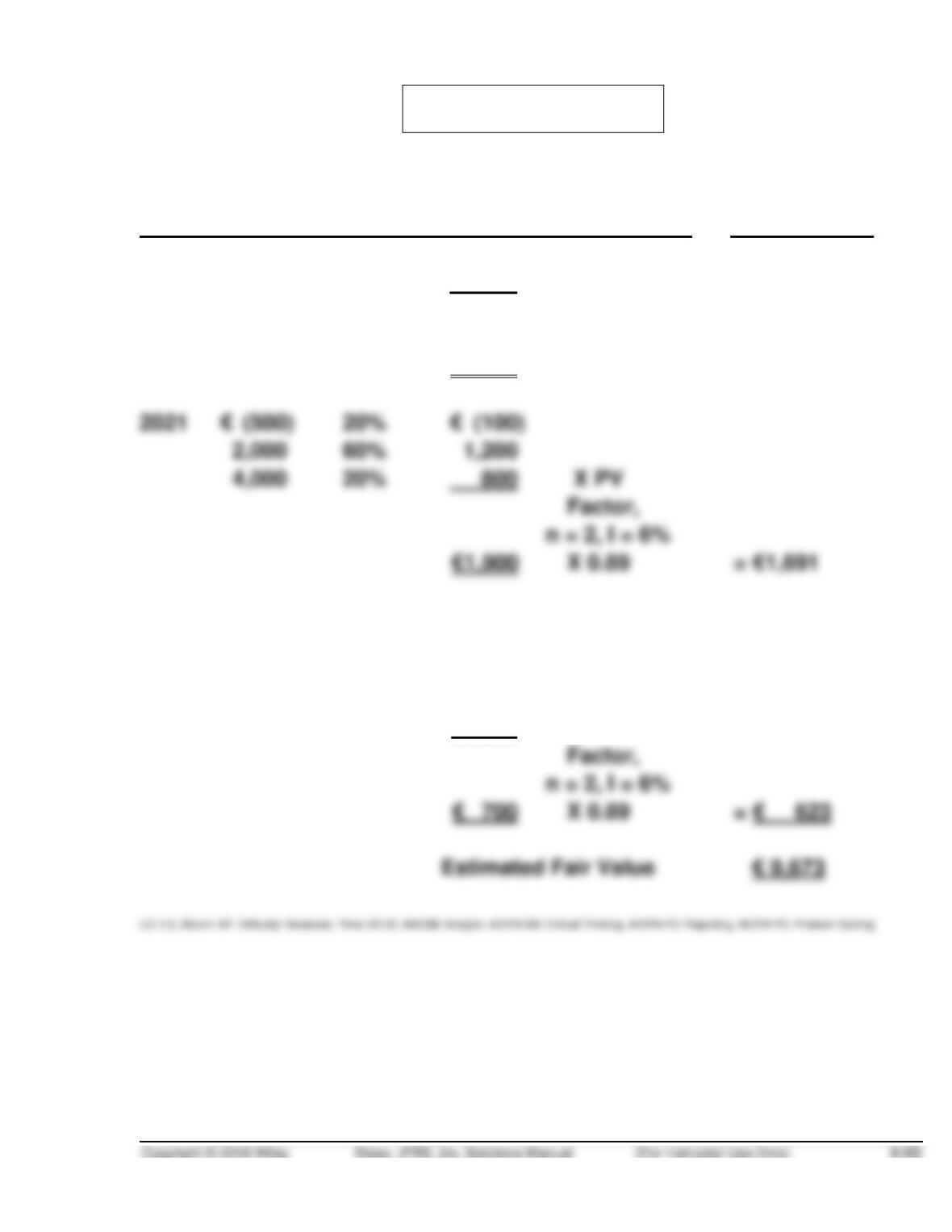

PROBLEM 6.14

Cash Flow Probability

Estimate X Assessment = Expected Cash Flow Present Value

2020 €6,000 40% €2,400

9,000 60% 5,400 X PV

Factor,

n = 1, I = 6%

€7,800 X 0.9434 = € 7,359

Residual

Value

Received

at the End

of 2021 € 500 50% € 250

900 50% 450 X PV

PROBLEM 6.15

(a) The expected cash flows to meet the environmental liability represent a

deferred annuity. Developing a fair value estimate requires determining

the present value of the annuity of expected cash flows to be paid after

10 years and then determine the present value of that amount today.

Cash Flow Probability

Estimate X Assessment = Expected Cash Flow

$15,000 10% $ 1,500

The value today of the annuity payments to commence in ten years is:

$ 64,269

Present value of annuity

Alternatively, the present value of the deferred annuity can be computed

as follows:

(b) This fair value estimate is based on unobservable inputs—Murphy’s

own data on the expected future cash flows associated with the

$ 23,600

Expected cash outflows

ordinary annuity for 10 periods at 5% (9.39357 – 7.72173)]

FINANCIAL REPORTING PROBLEM

(a) 1. Intangible assets, goodwill

For impairment of goodwill and other intangible assets, fair value is

determined using a discounted cash flow analysis.

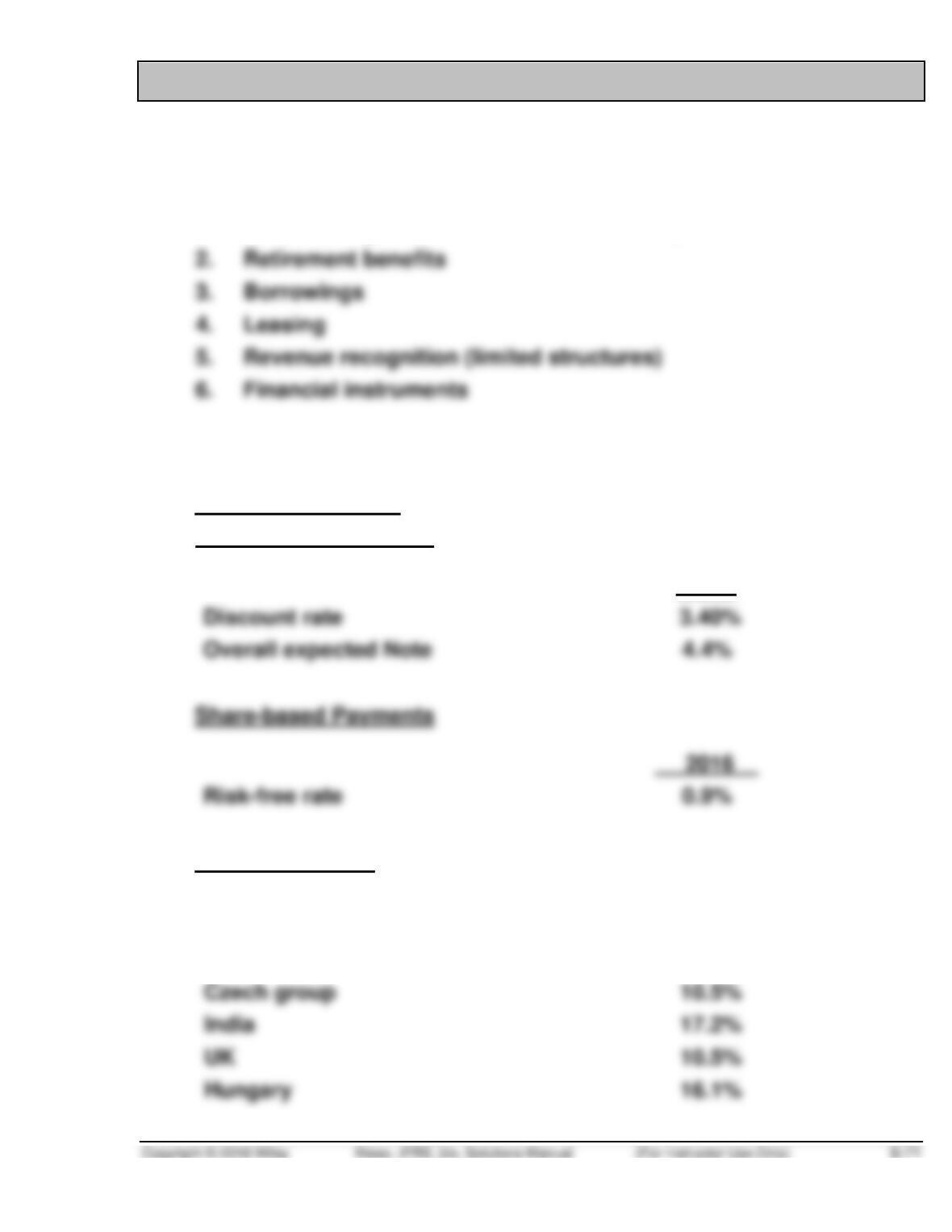

(b) 1. The following rates are disclosed in the accompanying notes:

Retirement Benefits

Financial Assumptions

2016

Discount rate

Overall expected Note

Risk-free rate

Intangible Assets

Czech group

10.5%

India

17.2%

10.5%

Hungary

16.1%

Pre-tax discount rate

Panama

8.3%

FINANCIAL REPORTING PROBLEM (Continued)

Borrowings

Interest Rate Analysis

2016

2. There are different rates for various reasons:

(1) The maturity dates—short-term vs. long-term.

(2) The security or lack of security for debts—mortgages and col-

lateral vs. unsecured loans.

FINANCIAL STATEMENT ANALYSIS CASE

(a) Cash inflows of $375,000 less cash outflows of $125,000 = Net cash

flows of $250,000.

(b) Cash inflows of $275,000 less cash outflows of $155,000 = Net cash

flows of $120,000.

(c) The new estimates, following the impairment, indicate a much lower

net cash inflow. The estimate of future cash flows is very useful. It

ACCOUNTING, ANALYSIS, AND PRINCIPLES

ACCOUNTING

(a) $50,000 X (PVF – OA10, ?%) = $320,883

(PVF – OA10, ?%) = $320,883 ÷ $50,000

(PVF – OA10, ?%) = 6.41766

ANALYSIS

The note receivable consists of a fixed set of payments to be received.

PRINCIPLES

Regulators are commonly faced with the relevance–faithful presentation trade–

off. Many believe that fair value provides more relevant information because

RESEARCH CASE

(a) The components of present value measurement include the following

elements that together capture the economic differences between

assets (IAS 36, paragraph A1):

(a) an estimate of the future cash flow, or in more complex cases, series

(b) Accounting applications of present value have traditionally used a single

set of estimated cash flows and a single discount rate, often described

as ‘the rate commensurate with the risk’. In effect, the traditional approach

The expected cash flow approach is, in some situations, a more effective

measurement tool than the traditional approach. In developing a

measurement, the expected cash flow approach uses all expectations

RESEARCH CASE (Continued)

(c) When an asset-specific rate is not directly available from the market,

an entity uses surrogates to estimate the discount rate. The purpose is

to estimate, as far as possible, a market assessment of:

(a) the time value of money for the periods until the end of the asset’s