FINANCIAL REPORTING PROBLEM

(a) According to Note 1—Accounting Policies, “Revenue comprises sales of

goods to customers outside the Group less an appropriate deduction for

actual and expected returns, discounts and loyalty scheme vouchers,

and is stated net of value added tax and other sales taxes. Revenue is

recognized when goods are delivered to our franchise partners or

customers and the significant risks and rewards of ownership have been

transferred to the buyer.”

market value of pension assets are disclosed.

(c) Examination of the auditor’s report. Also, M&S discusses a number of

new accounting pronouncements issued or effective during the fiscal

year (e.g., IFRS 7, IFRIC 11, IFRIC 14). M&S indicates that they have had

or are expected to have a material impact on the financial statements.

(d) According to the discussion of “Critical accounting estimates and

judgements”:

Refunds, gift cards and loyalty scheme accruals

Accruals for sales returns, deferred income in relation to loyalty scheme

redemption and gift card and credit voucher redemptions are estimated

on the basis of historical returns and redemptions. These are recorded so

COMPARATIVE ANALYSIS CASE

(a) Both companies use the Euro as their currency. Since both companies use the

same currency, comparability is enhanced.

(c) Both companies value inventory at lower of cost or net realizable value, using

the average cost method. Therefore, comparability is enhanced.

(d) adidas reported the following with respect to new accounting standards:

FINANCIAL STATEMENT ANALYSIS CASE—NOKIA

(a) The IASB’s framework indicates that revenue is to be recognized

when it is probable that future economic benefits will flow to the

1. For revenue related to sales, Nokia indicates that the criteria are

met when it is probable that economic benefits associated with

2. Revenue from contracts is recognized on the percentage of com–

pletion basis, when the outcome of the contract can be estimated

(b) A number of estimates are required in applying these revenue recogni-

tion policies. For example, sales may materially change if manage–

ment’s assessment of such criteria was determined to be inaccurate.

FINANCIAL STATEMENT ANALYSIS CASE—NOKIA (Continued)

With respect to revenue from contracts, recognized revenues and

profits are subject to revisions during the project in the event that the

assumptions regarding the overall project outcome are revised.

(c) Even if all phone-makers use the same policy, it still might be difficult

to compare their revenue numbers. As indicated in (b), management

makes a number of judgments and estimates in determining whether

ACCOUNTING, ANALYSIS AND PRINCIPLES

ACCOUNTING

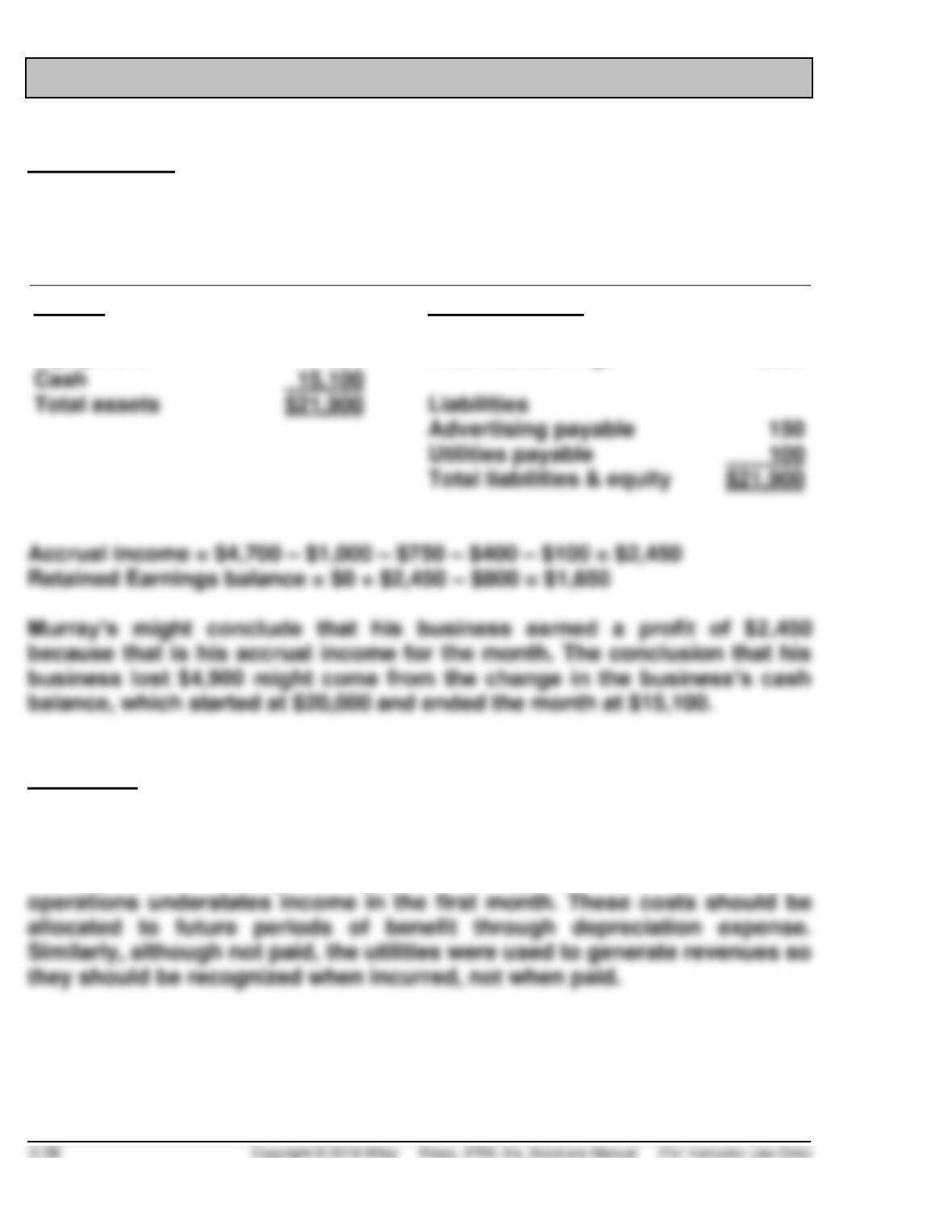

CADDIE SHACK DRIVING RANGE

Statement of Financial Position

May 31, 2019

Assets

Owners’ equity

Building

$ 6,000

Contributed capital

$20,000

Equipment

800

Retained earnings

1,650

Cash

Total assets

$21,900

Liabilities

Advertising payable

Utilities payable

100

Total liabilities & equity

$21,900

ANALYSIS

The income measure of $2,450 is most relevant for assessing the future

profitability and hence the payoffs to the owners. For example, charging

the cost of the building and equipment to expense in the first month of

ACCOUNTING, ANALYSIS AND PRINCIPLES (Continued)

PRINCIPLES

IFRS income is the accrual income computed above as $2,450. The key

concept illustrated in the difference between the loss of $4,900 and profit of

RESEARCH CASH

Search Strings: “materiality”, “completeness”

the financial statements.

(b) According to the Conceptual Framework, (chapter 3, paras. QC12–

QC13):

To be a perfectly faithful representation, a depiction would have

three characteristics. It would be complete, neutral and free from

error. Of course, perfection is seldom, if ever, achievable. The

RESEARCH CASE (Continued)

(c) According to the Conceptual Framework (chapter 1, par. OB17):

Financial performance reflected by accrual accounting

Accrual accounting depicts the effects of transactions and other events

GAAP CONCEPTS and APPLICATION

2.1. Both the IASB and FASB have similar measurement principles, based

on historical cost and fair value. The boards issued converged fair

2.2. The IASB framework identifies 5 elements: ASSETS, LIABILITIES,

EQUITY, INCOME, and EXPENSES. The U.S. GAAP framework has the

following additional elements – which expand on equity-related items.

INVESTMENTS BY OWNERS.

Increases in net assets of a particular enterprise resulting from

transfers to it from other entities of something of value to obtain or

REVENUES.

Inflows or other enhancements of assets of an entity or settlement of

its liabilities (or a combination of both) during a period from delivering

or producing goods, rendering services, or other activities that

constitute the entity’s ongoing major or central operations.

COMPREHENSIVE INCOME.

GAAP CONCEPTS and APPLICATIONS (Continued)

GAINS.

Increases in equity (net assets) from peripheral or incidental

transactions of an entity and from all other transactions and other

events and circumstances affecting the entity during a period except

those that result from revenues or investments by owners.

2.3. The IASB and the FASB face a difficult task in attempting to update,

modify, and complete a conceptual framework. There are many

challenging issues to overcome. For example, how do we trade off

characteristics such as highly relevant information that is difficult to

verify? How do we define control when we are developing a definition

of an asset? Is a liability the future sacrifice itself or the obligation to