Unlock document.

This document is partially blurred.

Unlock all pages and 1 million more documents.

Get Access

TIME AND PURPOSE OF CONCEPTS FOR ANALYSIS

CA 5.1 (Time 20–25 minutes)

Purpose—to provide a varied number of financial transactions and then determine how each of these

CA 5.2 (Time 25–30 minutes)

Purpose—to present the student with the opportunity to determine whether certain accounts should be

CA 5.3 (Time 30–35 minutes)

CA 5.4 (Time 20–25 minutes)

Purpose—to present a statement of financial position that must be analyzed to assess its deficiencies.

Items such as improper classification, terminology, and disclosure must be considered.

CA 5.5 (Time 20–25 minutes)

CA 5.6 (Time 40–50 minutes)

Purpose—to present a cash flow statement that must be analyzed to explain differences in cash flow

and net income, and sources and uses of cash flow and ways to improve cash flow.

SOLUTIONS TO CONCEPTS FOR ANALYSIS

CA 5.1

1. The new estimate would be used in computing depreciation expense for 2019. No adjustment of

the balance in accumulated depreciation at the beginning of the year would be made. Instead, the

2. The effect of the error at December 31, 2018, should be shown as an adjustment of the beginning

3. Generally, an entry is made for a cash dividend on the date of declaration. The appropriate

CA 5.2

Current Assets

Current Liabilities

Interest accrued on government securities.

Preference dividend, payable Nov. 1, 2019.

Notes receivable.

Income taxes payable.

Petty cash fund.

Customers’ advances (on contracts to be

Government securities.

completed next year).

CA 5.2 (Continued)

Borderline cases that have been classified on the basis of assumptions are:

1. Notes receivable are assumed to be collectible within the longer of one year or the operating cycle.

2. Government securities are assumed to be a temporary investment of current funds.

CA 5.3

Deficiencies in the presentation of Fonzarellis’s assets are as follows:

1. Non-controlling interest should be shown under equity as an addition to total equity.

2. Trading securities should be reported at fair value, not cost.

3. Bad Debt Reserve is generally viewed an improper terminology; Allowance for Doubtful Accounts

is considered more appropriate. The amount of estimated uncollectibles should be disclosed.

CA 5.4

Criticisms of the statement of financial position of the Rasheed Brothers Corporation are as follows:

1. The basis for the valuation of short-term investments should be shown. Short-term investments

2. An allowance for doubtful accounts receivable is not indicated.

CA 5.4 (Continued)

3. The basis for the valuation and the method of pricing for Inventory are not indicated.

7. Buildings and land should be segregated. Accumulated depreciation-buildings should be shown as

a subtraction from the Buildings account only.

8. Cash restricted for plant expansion would be more appropriately shown under the heading of

“Investments.”

9. Equity should be reported before liabilities and current liabilities should be reported after the non-

current liabilities.

10. Unrealized gains on non-trading equity investments should be appropriately reported as

accumulated other comprehensive income in the equity section. The use of the term deferred

credits is inappropriate.

CA 5.5

(a). The ethical issues involved are integrity and honesty in financial reporting, full disclosure, and the

accountant’s professionalism.

CA 5.5 (Continued)

Because of the significant impact on the financial statements of the depreciation method(s) used,

the following disclosures should be made.

CA 5.6

Date

President Kappeler, CEO

Kappeler Corporation

125 Wall Street

Middleton, Kansas 67458

Dear Mr. Kappeler:

I have good news and bad news about the financial statements for the year ended December 31, 2019.

The good news is that net income of $100,000 is close to what you predicted in the strategic plan last

year, indicating strong performance this year. The bad news is that the cash balance is seriously low.

Enclosed is the Statement of Cash Flows, which best illustrates how both of these situations occurred

simultaneously.

The corporation made significant investments in equipment and land. These were paid from cash

reserves. These purchases used 75% ($300,000/$400,000) of the company’s cash. In addition, the

redemption of the bonds improved the equity of the corporation and reduced interest expense.

However, it also used 25% ($100,000/$400,000) of the corporation’s cash. It is normal to use cash for

investing and financing activities. But when cash is used, it must also be replenished.

FINANCIAL REPORTING PROBLEM

(a) M&S could have adopted the account form or report form. M&S uses the

report form.

(b) On April 2, 2016, M&S had negative working capital (current assets less

(c) The following table summarizes M&S’s cash flows from operating,

investing, and financing activities in 2015 and 2016 (in millions).

2016

2015

Net cash provided by operating activities

£ 1,212.0

£1,278.0

(d) 1. Net Cash Provided by Operating Activities ÷ Average Current

Liabilities = Current Cash Debt Coverage

FINANCIAL REPORTING PROBLEM (Continued)

3. Net cash provided by operating activities less capital expenditures

and dividends

Net cash provided by operating activities .......

£1,212.0

COMPARATIVE ANALYSIS CASE

(a) Both adidas and Puma use the account form.

(b) adidas had a working capital of €2,133 million (€7,497 million – €5,364

(c) The most significant difference relates to intangible assets. adidas has

Goodwill and Other Intangible Assets of €3,208 million (24% of assets);

Puma has Intangible Assets of €403.3 million (or 15% of assets). adidas

is about four times bigger than Puma.

(d) adidas has increased net cash provided by operating activities from

(e) Puma

COMPARATIVE ANALYSIS CASE (Continued)

(€ millions)

Free cash flow

Net cash provided by operating activities .................

€ (37.1)

Puma’s free cash flow is €44.5.

adidas

Current Cash Debt

adidas has strong liquidity and financial flexibility.

Puma’s working capital position appears sound but its cash

generating ability is very tenuous with negative free cash flow.

FINANCIAL STATEMENT ANALYSIS CASE 1

(a) These accounts are shown in the order in which Cathay Pacific actually

presented the accounts. The order shown may be modified somewhat.

NON-CURRENT ASSETS AND LIABILITIES

Fixed assets

LONG-TERM LIABILITIES

Deferred taxation

Retirement benefit obligations

NET NON-CURRENT ASSETS

CURRENT ASSETS AND LIABILITIES

CAPITAL AND RESERVES

Share capital—ordinary

Reserves

Funds attributable to owners of Cathay Pacific

Non-controlling interest

(b) When Cathay passengers purchase tickets for future flights, Cash and

FINANCIAL STATEMENT ANALYSIS CASE 2

(a) Working Capital, Current Ratio

Without off-balance-sheet commitments

Working Capital Current Ratio

Without information on off-balance-sheet commitments, an analyst

would overstate Dior’s liquidity, as measured by working capital and

the current ratio.

(b) 1. Based on the analysis in Part (a), Dior has a pretty good liquidity

cushion. It would be able to pay a loan of up to €2,970 million, if

due in one year.

FINANCIAL STATEMENT ANALYSIS CASE 3

(a) (W in billions) Current Year Prior Year

Cash provided by operations ..... W10,217 W8,807

Capital expenditures ................... W8,190 W5,071

(b) Cash provided by operations increased in the current year relative to

the prior year by W1,410 billion (W10,217 – W8,807). This is due to a

ACCOUNTING, ANALYSIS, AND PRINCIPLES

ACCOUNTING

HOPKINS PLC

Statement of Financial Position

December 31, 2019

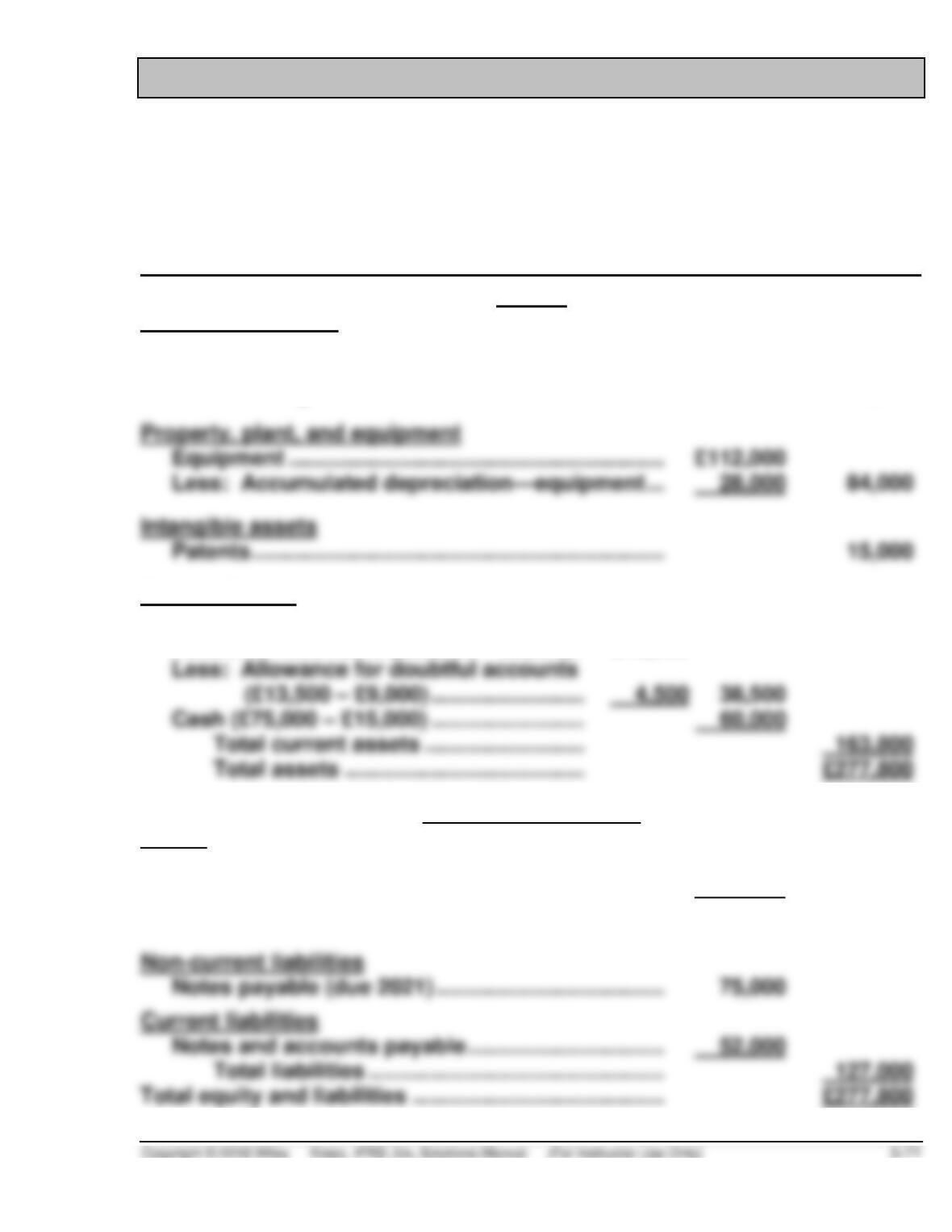

Assets

Non-current assets

Long-term investments

Bond sinking fund ................................................. £ 15,000

Current Assets

Inventory ................................................... 65,300

Accounts receivable (£52,000 – £9,000) . £43,000

Equity and Liabilities

Equity

Share capital-ordinary .......................................... £100,000

Retained earnings ................................................. 50,800

Total equity ..................................................... £150,800

ACCOUNTING, ANALYSIS, AND PRINCIPLES (Continued)

ANALYSIS

The classified statement of financial position provides subtotals for current

assets and current liabilities, which are assets expected to be converted to

cash (or liabilities expected to be paid from cash) in the next year or operating

PRINCIPLES

The primary objection that the bank is likely to raise about this supple-

mental information is the reliability of the estimates of fair values for the

RESEARCH CASE

(a) International Accounting Standard 8 covers the disclosure of account-

ing policies.

(c) An entity shall select and apply its accounting policies consistently

for similar transactions, other events and conditions, unless an IFRS

specifically requires or permits categorisation of items for which different

(d) Disclosure

When initial application of an IFRS has an effect on the current period

or any prior period, would have such an effect except that it is imprac-

ticable to determine the amount of the adjustment, or might have an

effect on future periods, an entity shall disclose:

a. the title of the IFRS;

RESEARCH CASE (Continued)

f. for the current period and each prior period presented, to the

extent practicable, the amount of the adjustment:

Financial statements of subsequent periods need not repeat these

disclosures. (para. 28)

When a voluntary change in accounting policy has an effect on the

current period or any prior period, would have an effect on that period

except that it is impracticable to determine the amount of the adjustment,

or might have an effect on future periods, an entity shall disclose:

a. the nature of the change in accounting policy;

b. the reasons why applying the new accounting policy provides reliable

GAAP PRACTICE

GAAP5.1. The similarities between IFRS and U.S. GAAP related to statement

of financial position presentation are as follows:

• IAS 1 specifies minimum note disclosures. These must include

information about (1) accounting policies followed, (2) judgments

that management has made in the process of applying the entity’s

GAAP5.2. The IASB and the FASB are working on a project to converge their

standards related to financial statement presentation. This joint project

will establish a common, high-quality standard for presentation of

information in the financial statements, including the classification and

GAAP PRACTICE (Continued)

GAAP5.3. Rainmaker would present current assets first in its statement of

financial position instead of last under IFRS. It would report cash

GAAP5.4. (a) Some of the differences are:

1. Report form and subtotals—Nordstrom uses a modified report

form but does not report “Total non-current assets.” It also

does not report “Total liabilities.” Nordstrom also uses “Total

liabilities and shareholders’ equity” instead of just “Total

liabilities and equity.”

2. Classifications—the classifications are arranged according

to decreasing liquidity. For example, “Current assets” are

listed first, then “Property, plant, and equipment”. Current