PROBLEM 14.2 (Continued)

Entry for accrued interest

Interest Expense ($204,868 X 1/2 X 1/2) …………………….

51,217

Bonds Payable ……………………………………………………….

Cash ($210,000 X 1/2 X 1/2) …………………………..

Entry for reacquisition

Bonds Payable ……………………………………………………….

1,023,055*

Loss on Extinguishment of Debt …………………………..

Cash ……………………………………………………….

*Premium as of 7/1/21 to be written off

($2,046,110 – $2,000,000) X 1/2 = $23,055

PROBLEM 14.3

(a)

Date

(1)

Cash

Paid

(2)

Interest

Expense

@2%

(2) – (1)

Change in

Carrying

Amount

Carrying

Amount of

Note

1/1/19

—

—

—

€32,000

4/1/19

€400

€640

€240

32,240

7/1/19

32,485

10/1/19

32,735

1/1/20

32,990

than at the beginning of the year.

(c) To earn 8% over the next two years the quarterly payments must be

€4,503 computed as follows:

(d)

Date

Cash

Paid

Interest

Expense

Change in

Carrying

Amount

Carrying

Amount of

Note

1/1/20

—

—

—

€32,990

4/1/20

€4,503

€660

€3,843

29,147

7/1/20

25,227

10/1/20

21,229

1/1/21

17,151

4/1/21

12,991

7/1/21

10/1/21

1/1/22

(e) The new sales gimmick may bring people into the showroom the first

time but will drive them away once they learn of the amount of their

PROBLEM 14.4

Dear Samantha,

When a bond is issued at face value, the annual interest expense and the

interest payout equals the face value of the bond times the interest rate

stated on its face. However, if the bond is issued to yield a higher or lower

Assume a premium: the theory behind the effective-interest method is that,

as time passes, the difference between the face value of the bond and its

carrying amount becomes smaller, resulting in a lower interest expense

To amortize the premium applying this method to the data provided, you

must know the bond’s face amount, its stated rate of interest, its effective

rate of interest, and its carrying value.

1. Multiply the stated rate times the face amount. This is the interest

payout.

PROBLEM 14.4 (Continued)

3. Subtract the amount calculated in #2 above from that found in #1. This

is the amount to be amortized for the period.

The schedule below illustrates this calculation. The face value

(R$2,000,000) is multiplied by the stated rate of 11 percent, while the

Follow these steps and you should have no trouble amortizing premiums

and discounts over the life of a bond.

Sincerely,

Attachment to letter

HOBART SA

Interest and Discount Amortization Schedule

11% Bond Issued to Yield 10%

Date

(1)

Cash Paid

(@11%)

(2)

Interest

Expense

(@10%)

(1) – (2)

Premium

Amortized

Carrying

Amount of

Bond

6/30/19

—

—

—

R$2,171,600

12/31/19

R$110,000

R$108,580

R$1,420

2,170,180

108,509

2,168,689

108,434

110,000

108,356

PROBLEM 14.5

(a)

December 31, 2019

Equipment ……………………………………………………….

Notes Payable ………………………………………………..

(Computer capitalized at the present

value of the note—£600,000 X .68301[pv4,10%])

(b)

December 31, 2020

Depreciation Expense ……………………………………………..

67,961.20

Accumulated Depreciation—Equipment

[(£409,806 – £70,000) ÷ 5] …………………………..

Interest Expense …………………………………………………….

40,980.60

Notes Payable ………………………………………………..

Schedule of Note Discount Amortization

Date

Debit, Interest Expense @10%

Credit, Notes Payable

Carrying Amount

of Note

12/31/19

—

£409,806.00

12/31/22

(c)

December 31, 2021

[(£409,806 – £70,000) ÷ 5] …………………………..

Accumulated Depreciation—Equipment …………..

Interest Expense …………………………………………………….

Notes Payable ………………………………………………..

Depreciation Expense

PROBLEM 14.6

(a)

December 31, 2018

Machinery ……………………………………………………….

182,485.20*

Cash ……………………………………………………….

50,000.00

Notes Payable…………………………..

132,485.20

*To record machinery at the

present value of the note plus

the immediate cash payment:

PV of $40,000 annuity @ 8%

for 4 years ($40,000 X 3.31213) …………………………..

$132,485.20

Down payment ……………………………………………………….

50,000.00

Capitalized value of machinery …………………………..

$182,485.20

(b)

December 31, 2019

Notes Payable ……………………………………………………….

40,000.00

Cash ……………………………………………………….

40,000.00

Interest Expense …………………………..

10,598.82

Notes Payable…………………………..

10,598.82

Schedule of Note Discount Amortization

Date

(1)

Cash Paid

(2)

Interest

Expense

@8%

(1) – (2)

Amortization

Carrying

Amount of Note

12/31/18

—

—

—

$132,485.20

12/31/19

$40,000.00

$10,598.82

$29,401.18

103,084.02*

71,330.74

37,037.20

2,962.80**

PROBLEM 14.6 (Continued)

(c)

December 31, 2020

Notes Payable ……………………………………………………….

40,000.00

Cash ……………………………………………………….

40,000.00

Interest Expense …………………………..

Notes Payable …………………………..

(d)

December 31, 2021

Notes Payable ……………………………………………………….

40,000.00

Cash ……………………………………………………….

40,000.00

Interest Expense …………………………..

Notes Payable …………………………..

(e)

December 31, 2022

Notes Payable ……………………………………………………….

40,000.00

Cash ……………………………………………………….

40,000.00

Interest Expense …………………………..

Notes Payable …………………………..

PROBLEM 14.7

(a)

Entry to record the issuance of the 11% bonds on December 18, 2019:

Cash (¥40,000,000 X 102%) ………………………………………

40,800,000

Bonds Payable ……………………………………………….

40,800,000

Entry to record the retirement of the 9% bonds on January 2, 2020:

Bonds Payable (¥30,000,000 – ¥1,842,888) ………………..

Loss on Extinguishment of Debt …………………………..

[The loss represents the excess of the

cash paid (¥31,200,000) over the

(¥28,157,112).]

(b) The loss is reported as an other income and expense item.

Note 1. Loss on Bond Extinguishment

The loss represents a loss of ¥3,042,888 from the extinguishment and

PROBLEM 14.8

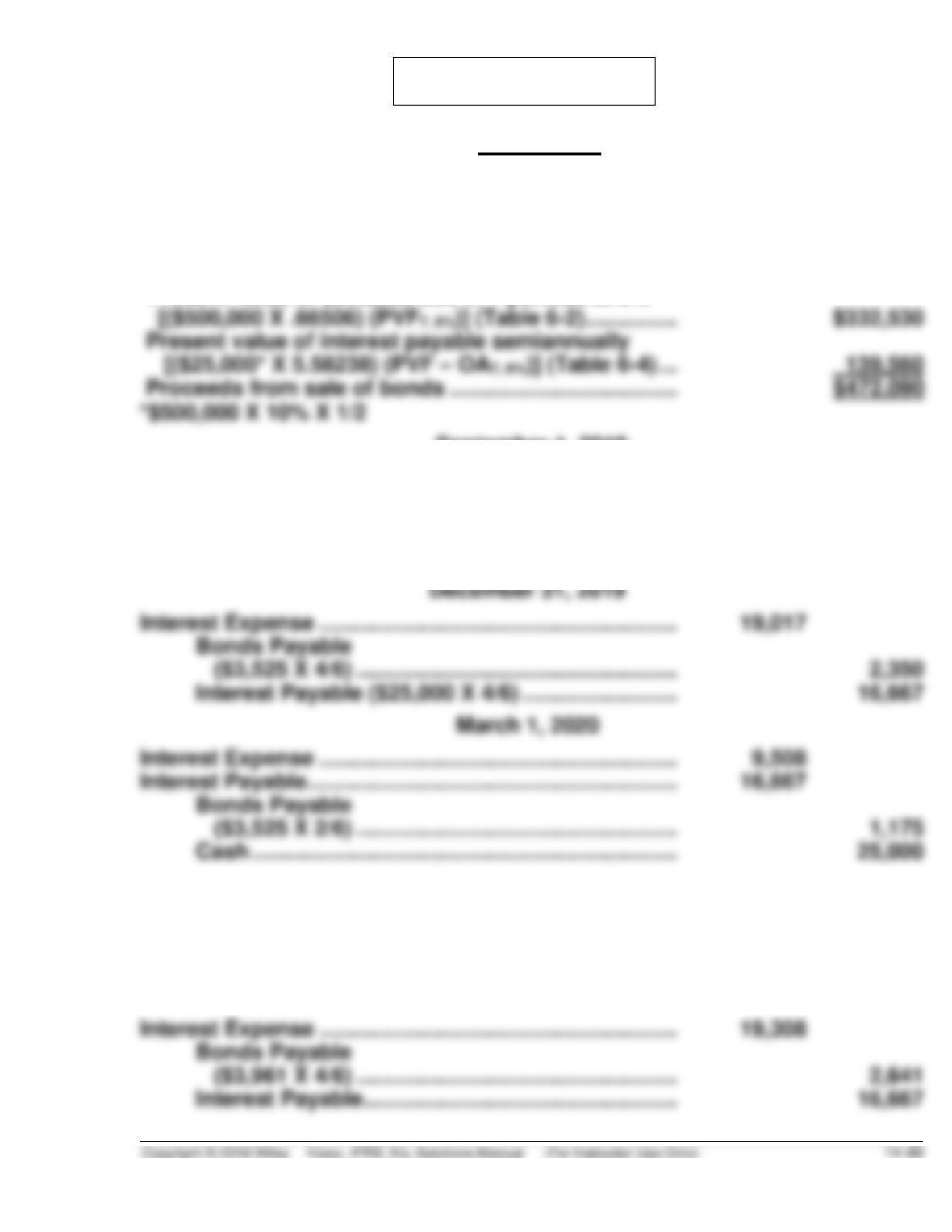

1. Sanford Co.

March 1, 2019

Cash ………………………………………………………………………

472,090*

Bonds Payable ……………………………………………….

472,090

*Present value of $500,000 due in 7 periods at 6%

[($500,000 X .66506) (PVF7, 6%)] (Table 6-2) ………………

Present value of interest payable semiannually

[($25,000* X 5.58238) (PVF – OA7, 6%)] (Table 6-4) ……

Proceeds from sale of bonds ………………………………….

September 1, 2019

Interest Expense …………………………………………………….

28,325*

Bonds Payable ……………………………………………….

3,325

Cash …………………………..………………………………….

25,000

(See amortization table on next page)

December 31, 2019

Interest Expense …………………………………………………….

19,017

Bonds Payable

($3,525 X 4/6) ……………………………………………….

2,350

Interest Payable ($25,000 X 4/6) ……………………….

16,667

Interest Expense …………………………………………………….

Interest Payable ………………………………………………………

16,667

Bonds Payable

($3,525 X 2/6) ……………………………………………….

1,175

Cash …………………………..………………………………….

25,000

September 1, 2020

Interest Expense …………………………………………………….

28,736

Bonds Payable ……………………………………………….

3,736

Cash …………………………..………………………………….

25,000

December 31, 2020

Interest Expense …………………………………………………….

19,308

Bonds Payable

($3,961 X 4/6) ……………………………………………….

2,641

Interest Payable ………………………………………………

16,667

PROBLEM 14.8 (Continued)

Schedule of Bond Discount Amortization

Effective-Interest Method

10% Bonds Sold to Yield 12%

Date

(1)

Cash

Paid

(2)

Interest

Expense

(2) – (1)

Discount

Amortized

Carrying

Amount of

Bonds

3/1/19

—

—

—

$472,090

9/1/19

$25,000

$28,325

$3,325

475,415

3/1/20

25,000

28,525

3,525

478,940

9/1/20

25,000

28,736

3,736

482,676

486,637

9/1/21

25,000

29,198

4,198

490,835

3/1/22

25,000

29,450

4,450

495,285

500,000

2. Titania Co.

June 1, 2019

Cash ………………………………………………………………………

425,853

Bonds Payable ………………………………………………..

425,853

Present value of $400,000 due in 8 periods at 5%

($400,000 X .67684) ……………………………………………….

Present value of interest payable semiannually

($24,000* X 6.46321) ……………………………………………..

Proceeds from sale of bonds …………………………………..

December 1, 2019

Interest Expense ……………………………………………………..

21,293*

Bonds Payable ……………………………………………………….

2,707

Cash ($400,000 X .12 X 6/12) …………………………..

24,000

(See amortization table on Page 14–51)

December 31, 2019

Interest Expense ($21,157 X 1/6) ………………………………

Bonds Payable

PROBLEM 14.8 (Continued)

June 1, 2020

Interest Expense ($21,157 X 5/6) ………………………………

17,631

Interest Payable ………………………………………………………

Bonds Payable ($2,843 X 5/6) …………………………………..

Cash …………………………..………………………………….

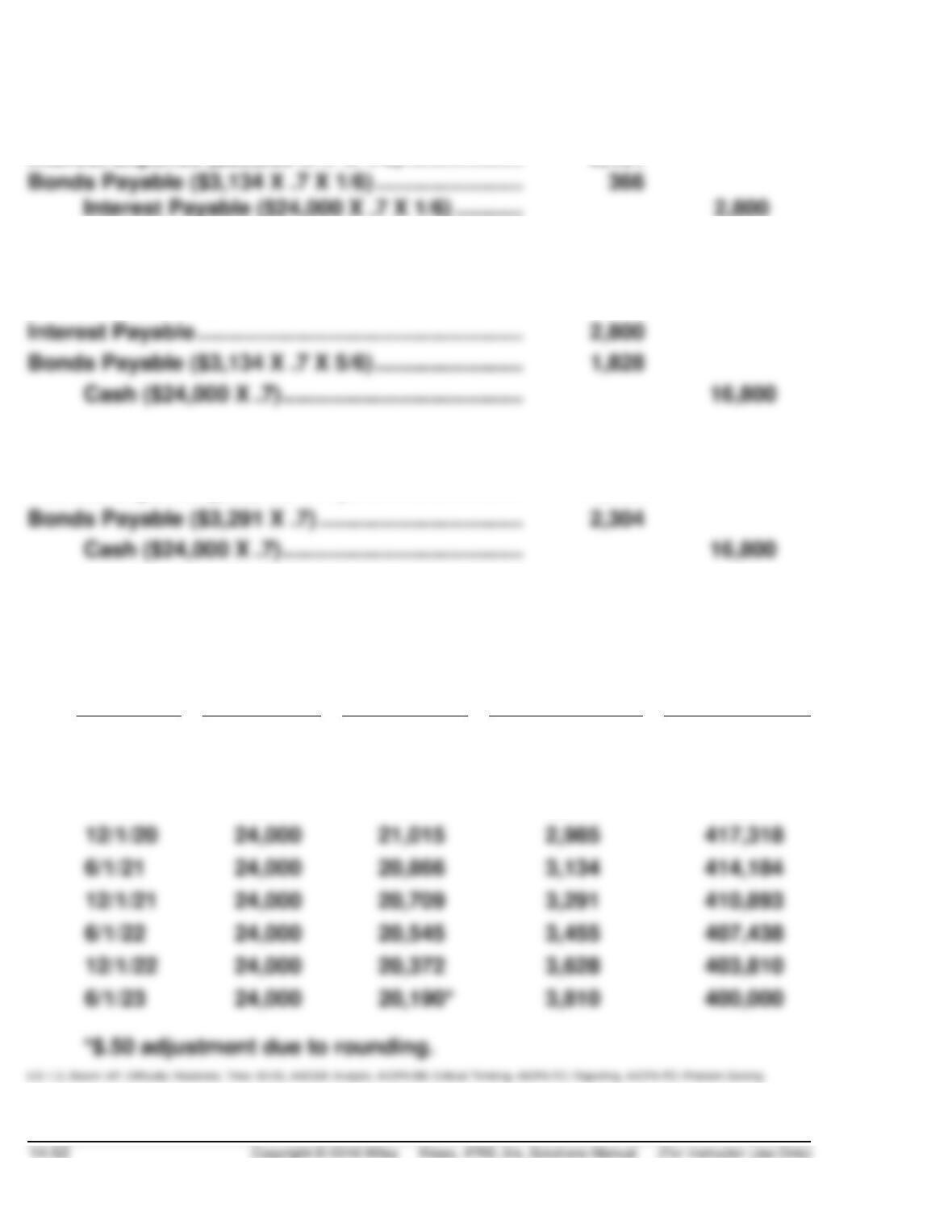

October 1, 2020

Interest Expense

($21,015 X .3* X 4/6) ………………………………………………

Bonds Payable ($2,985 X .3 X 4/6) …………………………..

Cash …………………………..………………………………….

*$120,000 ÷ $400,000 = .3

October 1, 2020

Bonds Payable ……………………………………………………….

125,494

Gain on Extinguishment of Bonds ……………………

4,294*

Cash …………………………..………………………………….

121,200

*Reacquisition price

$126,000 – ($120,000 X 12% X 4/12)

($420,303* X .30) – $597 ………………………………..

Gain on extinguishment ………………………………….

December 1, 2020

Interest Expense ($21,015 X .7*) ……………………………….

14,711

Bonds Payable ($2,985 X .7) …………………………………….

Cash ($24,000 X .7) ………………………………………….

*($400,000 – $120,000) ÷ $400,000 = .7

PROBLEM 14.8 (Continued)

December 31, 2020

Interest Expense ($20,866 X .7 X 1/6) ………………………..

2,434

Bonds Payable ($3,134 X .7 X 1/6) …………………………..

Interest Payable ($24,000 X .7 X 1/6) …………………

June 1, 2021

Interest Expense ($20,866 X .7 X 5/6) ………………………..

12,172

Interest Payable …………………………..………………………….

Bonds Payable ($3,134 X .7 X 5/6) …………………………..

Cash ($24,000 X .7) ………………………………………….

December 1, 2021

Interest Expense ($20,709 X .7) …………………………..

14,496

Bonds Payable ($3,291 X .7) …………………………………….

Cash ($24,000 X .7) ………………………………………….

Date

(1)

Cash

Paid

(2)

Interest

Expense

@5%

(1) – (2)

Premium

Amortized

Carrying

Amount of

Bonds

6/1/19

—

—

—

$425,853

12/1/19

$24,000

$21,293

$2,707

423,146

6/1/20

24,000

21,157

2,843

420,303

12/1/20

24,000

21,015

2,985

417,318

6/1/21

24,000

20,866

3,134

414,184

12/1/21

24,000

20,709

3,291

410,893

6/1/22

24,000

20,545

3,455

407,438

12/1/22

24,000

20,372

3,628

403,810

6/1/23

24,000

3,810

400,000

PROBLEM 14.9

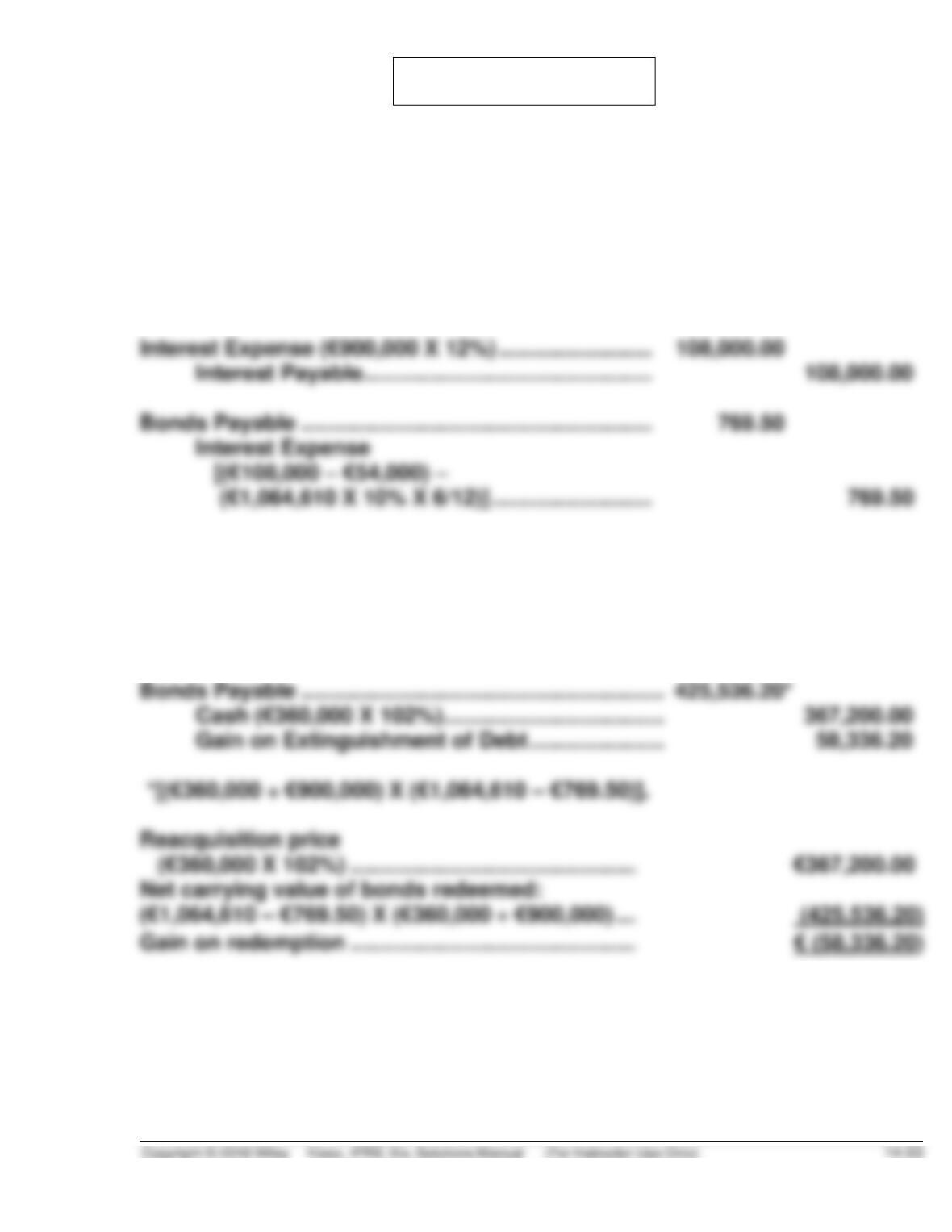

July 1, 2019

Cash

(€900,000 X 1.12290) + (€900,000 X 12% X 6/12) ………

1,064,610.00

Bonds Payable ……………………………………………….

1,010,610.00

Interest Expense (€900,000 X 12% X 6/12) …………

54,000.00

December 31, 2019

Interest Expense (€900,000 X 12%) …………………………..

108,000.00

Bonds Payable ……………………………………………………….

Interest Expense

January 1, 2020

Interest Payable ………………………………………………………

108,000.00

Cash …………………………..………………………………….

108,000.00

January 2, 2020

Bonds Payable ……………………………………………………….

Cash (€360,000 X 102%) …………………………………..

Gain on Extinguishment of Debt ………………………

Reacquisition price

(€360,000 X 102%) ………………………………………………..

Net carrying value of bonds redeemed:

PROBLEM 14.9 (Continued)

December 31, 2020

Interest Expense (€540,000* X 12%) ………………………….

64,800.00

Interest Payable ………………………………………………

*$900,000 – $360,000

Bonds Payable ……………………………………………………….

Interest Expense

€402,856.20) X .10] – €64,800 ……………………….

PROBLEM 14.10

(a)

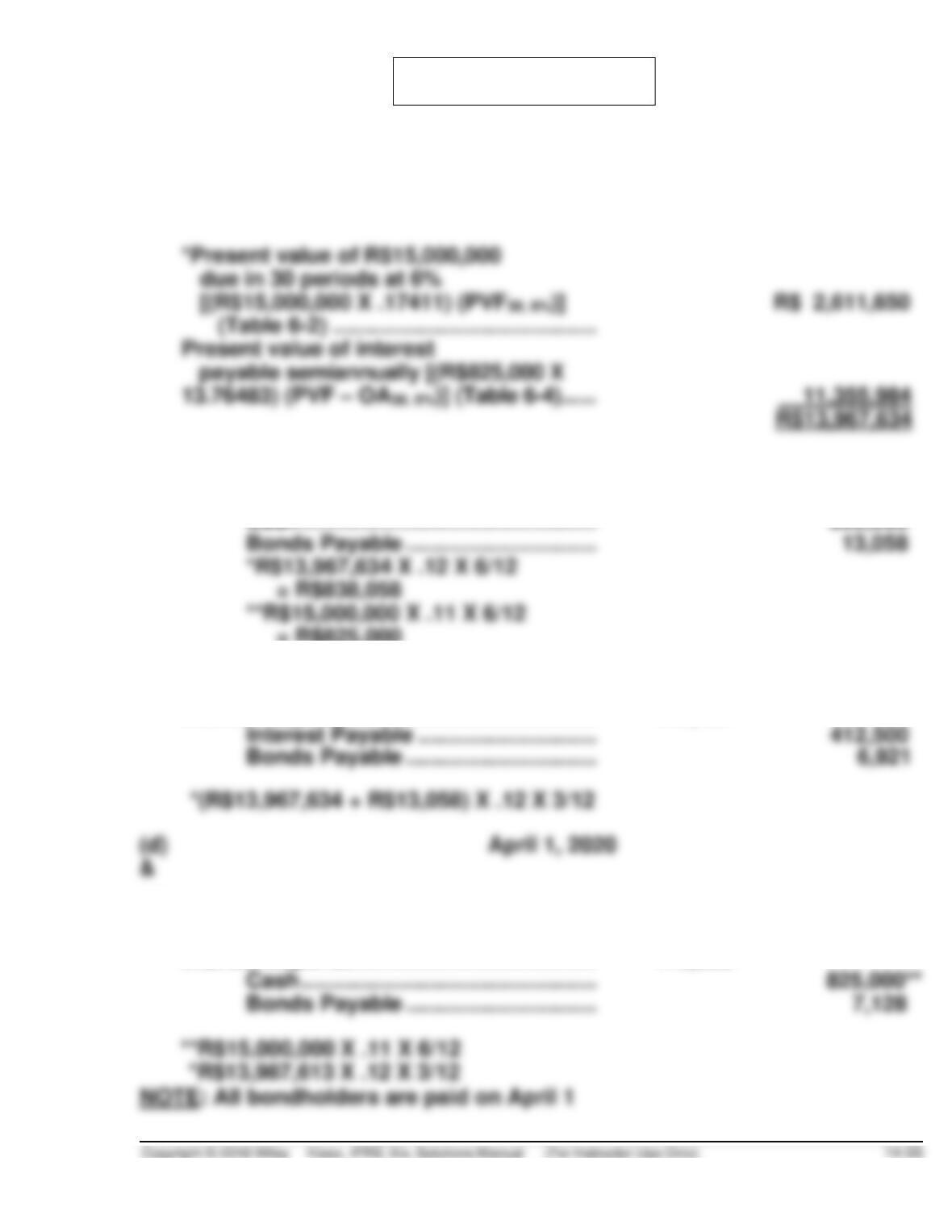

April 1, 2019

Cash ……………………………………………………….

13,967,634*

Bonds Payable …………………………..

13,967,634

*Present value of R$15,000,000

due in 30 periods at 6%

(Table 6-2) ……………………………………………………….

Present value of interest

(b)

October 1, 2019

Interest Expense ………………………………………………………

838,058*

Cash ……………………………………………………….

Bonds Payable …………………………..

*R$13,967,634 X .12 X 6/12

= R$838,058

**R$15,000,000 X .11 X 6/12

= R$825,000

(c)

December 31, 2019

Interest Expense ………………………………………………………

419,421*

Interest Payable …………………………..

Bonds Payable …………………………..

(e)

Interest Payable ……………………………………………………….

412,500

Interest Expense ………………………………………………………

419,628*

Cash ……………………………………………………….

Bonds Payable …………………………..

PROBLEM 14.10 (Continued)

The reacquisition price: 200,000 shares X R$31 = R$6,200,000.

The loss on extinguishment of the bonds is:

Reacquisition price ……………………………………………….

Less: Carrying amount

(R$13,987,613 + R$7,128) X 40% …………………………..

The entry to record extinguishment of the bonds is:

April 2, 2020

Bonds Payable ……………………………………………….

5,597,896

Loss on Extinguishment of Debt ……………………..

Share Capital—Ordinary …………………………..

Share Premium—Ordinary ………………………..

PROBLEM 14.11

(a) It is an extinguishment of debt with modification of terms.

(b)

Notes Payable (Old) ………………………………………………..

600,000

Gain on Extinguishment of Debt ………………………

Notes Payable (New) ……………………………………….

*Calculation of gain.

Pre-restructure carrying amount …………………………..

$600,000

Present value of restructured cash flows:

PROBLEM 14.12

(a)

Notes Payable ……………………………………………………….

5,000,000

Share Capital—Ordinary …………………………..

1,700,000

Share Premium—Ordinary …………………………..

2,000,000

Gain on Extinguishment of Debt ………………………

1,300,000

Carrying amount of debt …………………………..

Fair value of equity …………………………..

(3,700,000)

Gain on extinguishment

(b)

Notes Payable ……………………………………………………….

5,000,000

Land ……………………………………………………….

3,250,000

Gain on Disposition of Land …………………………..

750,000

Gain on Extinguishment of Debt ………………………

1,000,000

Fair value of land …………………………..

$4,000,000

Book value of land …………………………..

Gain on disposition of

Note payable (carrying

amount) ……………………………………………………….

$5,000,000

Fair value of land …………………………..

Gain on extinguishment

PROBLEM 14.12 (Continued)

(c)

Notes Payable (Old) ………………………………………………..

5,000,000

Gain on Extinguishment of Debt ………………………

Notes Payable (New) ……………………………………….

*Calculation of gain.

Pre-restructure carrying amount …………………………..

$ 5,000,000

Less: Present value of restructured cash flows:

Present value of $5,000,000 due in

3 years at 12% (Table 6-2);

($5,000,000 X .71178) ………………………………..

3,558,900

PROBLEM 14.13

(a)

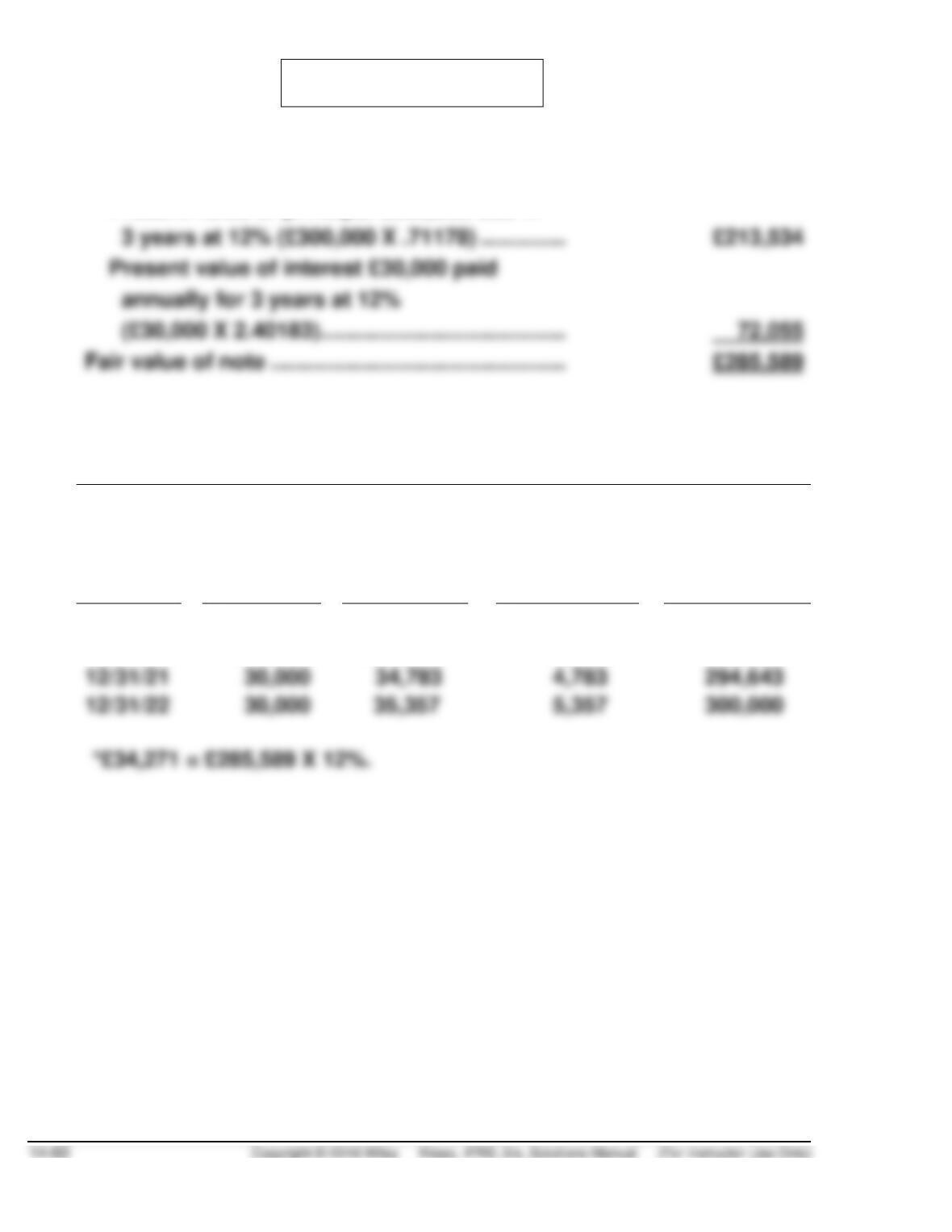

Present value of restructured cash flows:

(£30,000 X 2.40183) …………………………………………….

Present value of principal £300,000 due in

AMORTIZATION SCHEDULE AFTER DEBT MODIFICATION

MARKET INTEREST RATE 12%

Date

(1)

Cash

Paid

(2)

Interest

Expense

@12%

(2) – (1)

Amortization

Carrying

Value

12/31/19

—

—

—

£285,589

12/31/20

£30,000

£34,271*

£4,271

289,860

12/31/21

30,000

294,643

12/31/22

30,000

300,000