EXERCISE 19.11 (10–15 minutes)

Resulting Deferred Tax

Temporary Difference

(Asset)

Liability

Depreciation

€200,000

Lawsuit obligation

Installment sale

Totals

€500,000

EXERCISE 19.12 (20–25 minutes)

(a) To complete a reconciliation of pretax financial income and taxable

income, solving for the amount of pretax financial income, we must first

determine the amount of temporary differences arising or reversing

during the year. To accomplish that, we must determine the amount of

EXERCISE 19.12 (Continued)

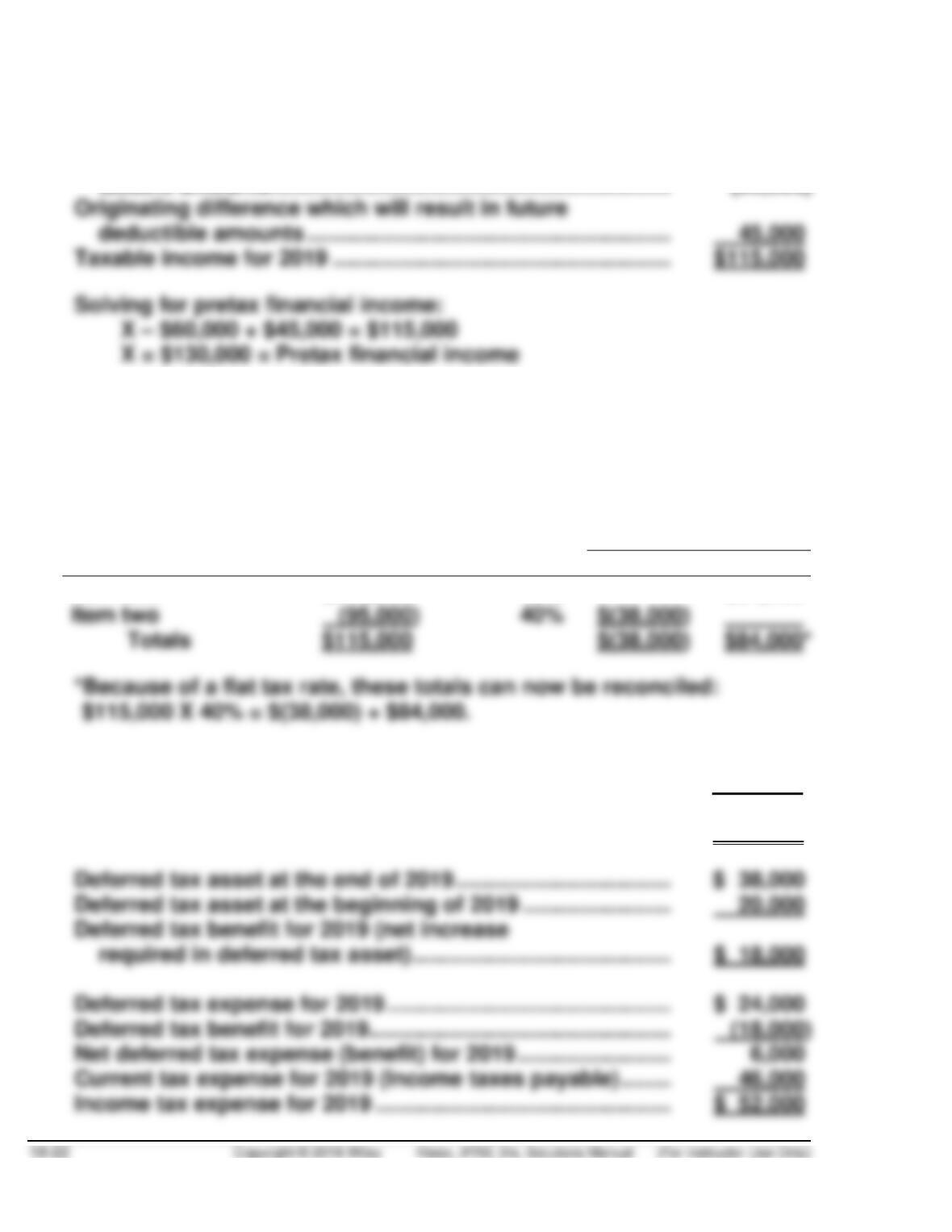

Pretax financial income ………………………………………………… $ X

Originating difference which will result in future

taxable amounts ……………………………………………………….. (60,000)

(b) Income Tax Expense ………………………………………… 52,000

Deferred Tax Asset …………………………………………… 18,000

Income Taxes Payable ($115,000 X 40%) ……… 46,000

Deferred Tax Liability …………………………..…….. 24,000

Temporary

Difference

Future Taxable

(Deductible) Amounts

Tax

Rate

Deferred Tax

(Asset)

Liability

Item one

($210,000

40%

$84,000

Totals

$84,000*

Deferred tax liability at the end of 2019 ………………………….. $ 84,000

Deferred tax liability at the beginning of 2019 ………………… (60,000)

Deferred tax expense for 2019 (net increase

required in deferred tax liability) ………………………………… $ 24,000

EXERCISE 19.12 (Continued)

(c) Income before income taxes ………………………….. $130,000

Income tax expense

Current ………………………………………………….. $46,000

EXERCISE 19.13 (20–25 minutes)

(a) Income Tax Expense ………………………………………. 187,000

Income Taxes Payable ……………………………… 136,000

Deferred Tax Liability ……………………………….. 51,000

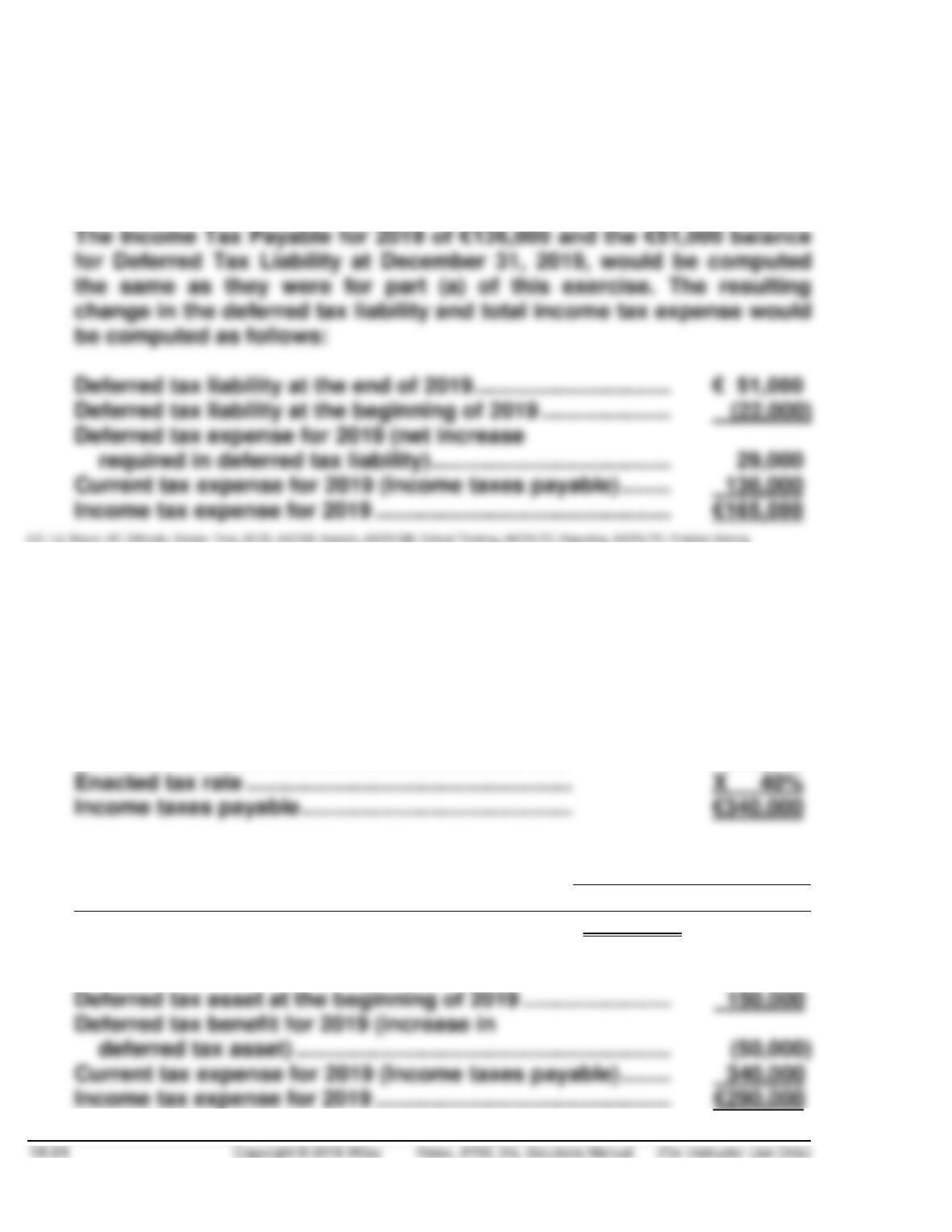

Taxable income for 2019 …………………………………. €340,000

Deferred tax liability at the end of 2019 ……………… € 51,000

Deferred tax liability at the beginning of 2019 ……. 0

Deferred tax expense for 2019 (net increase

EXERCISE 19.13 (Continued)

(b) Income Tax Expense ……………………………………….. 165,000

Income Taxes Payable ………………………………. 136,000

Deferred Tax Liability …………………………..……. 29,000

EXERCISE 19.14 (20–25 minutes)

(a) Income Tax Expense ……………………………………… 290,000

Deferred Tax Asset ………………………………………… 50,000

Income Taxes Payable …………………………….. 340,000

Taxable income ……………………………………………… €850,000

Date

Cumulative Future Taxable

(Deductible) Amounts

Tax Rate

Deferred Tax

(Asset)

Liability

12/31/19

€(500,000)

40%

€(200,000)

Deferred tax asset at the end of 2019 …………………………….. €200,000

EXERCISE 19.14 (Continued)

(b) The journal entry at the end of 2019:

Income Tax Expense ………………………………………. 30,000

Deferred Tax Asset ………………………………….. 30,000

Note to instructor: Although not requested by the instructions, the

pretax financial income can be computed by completing the following

reconciliation:

EXERCISE 19.15 (20–25 minutes)

(a) Income Tax Expense ………………………………………. 290,000

Deferred Tax Asset …………………………………………. 50,000

Income Taxes Payable ……………………………… 340,000

EXERCISE 19.16 (15–20 minutes)

(a)

Future Years

2020

2021

Total

Future taxable (deductible)

amounts

$1,000,000

$1,000,000

$2,000,000

(b) Deferred Tax Liability …………………………………. 60,000

Income Tax Expense ……………………………. 60,000

There are no changes during 2019 in the cumulative temporary

difference. The entire change in the deferred tax liability account is due

to the change in the enacted tax rate. That change is computed as

follows:

(c) Income before income taxes ……………………….. $5,000,000*

Income tax expense

Current ……………………………………………….. $2,000,000**

EXERCISE 19.16 (Continued)

**Taxable income for 2019 ………………………….. $5,000,000

Tax rate for 2019 (computed in (a)) ……………. X 40%

EXERCISE 19.17 (30–35 minutes)

Journal entry at December 31, 2018:

Income Tax Expense …………………………………………. 75,750

Deferred Tax Asset ……………………………………………. 4,000

The deferred tax account balances at December 31, 2018, are determined

as follows:

Temporary

Difference

Future Taxable

(Deductible) Amounts

Rate

Deferred Tax

(Asset)

Liability

*Because all deferred taxes were computed at the same rate, these totals

can be reconciled as follows: ¥6,000 X 40% = ¥(4,000) + ¥6,400.

EXERCISE 19.17 (Continued)

Deferred tax asset at the end of 2018 …………………………….. ¥( 4,000

Deferred tax expense for 2018 …………………………..………….. ¥ 6,400

Journal entry at December 31, 2019:

Income Tax Expense ………………………………………… 84,000

The deferred tax account balances at December 31, 2019, are determined

as follows:

Temporary

Difference

Future Taxable

(Deductible) Amounts

Rate

Deferred Tax

(Asset)

Liability

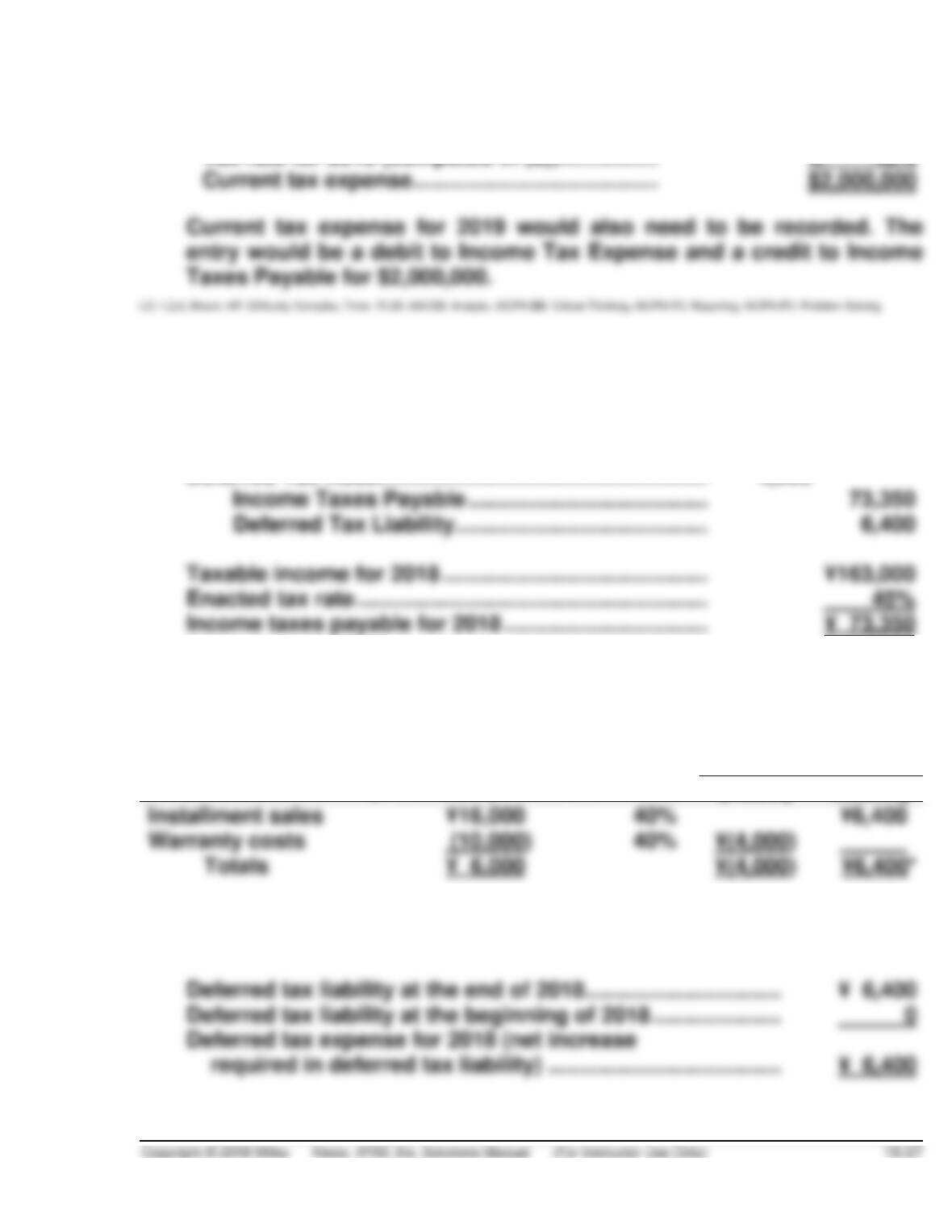

Installment sales

(¥8,000

40%

¥3,200

Totals

¥(2,000)

¥3,200*

*Because all deferred taxes were computed at the same rate, these totals

can be reconciled as follows: ¥3,000 X 40% = ¥(2,000) + ¥3,200.

Deferred tax liability at the end of 2019 ………………………….. ¥( 3,200

EXERCISE 19.17 (Continued)

Deferred tax asset at the end of 2019 …………………………..… ¥ 2,000

Deferred tax asset at the beginning of 2019 …………………… (4,000)

Deferred tax expense for 2019 (decrease

required in deferred tax asset) …………………………………… ¥ 2,000

Journal entry at December 31, 2020:

Income Tax Expense ………………………………………… 36,000

Deferred Tax Liability ……………………………………….. 3,200

Income Taxes Payable ……………………………….. 37,200

Deferred Tax Asset ……………………………………. 2,000

Deferred tax asset at the end of 2020 …………………. ¥ 0

Deferred tax asset at the beginning of 2020 ……….. 2,000

Deferred tax expense for 2020 (decrease

required in deferred tax asset) ……………………….. ¥ 2,000

EXERCISE 19.18 (20–25 minutes)

(a)

Temporary

Difference

Future Taxable

(Deductible) Amounts

Tax

Rate

December 31, 2019

Deferred Tax

(Asset)

Liability

Installment sales

(£ 96,000

35%

£33,600

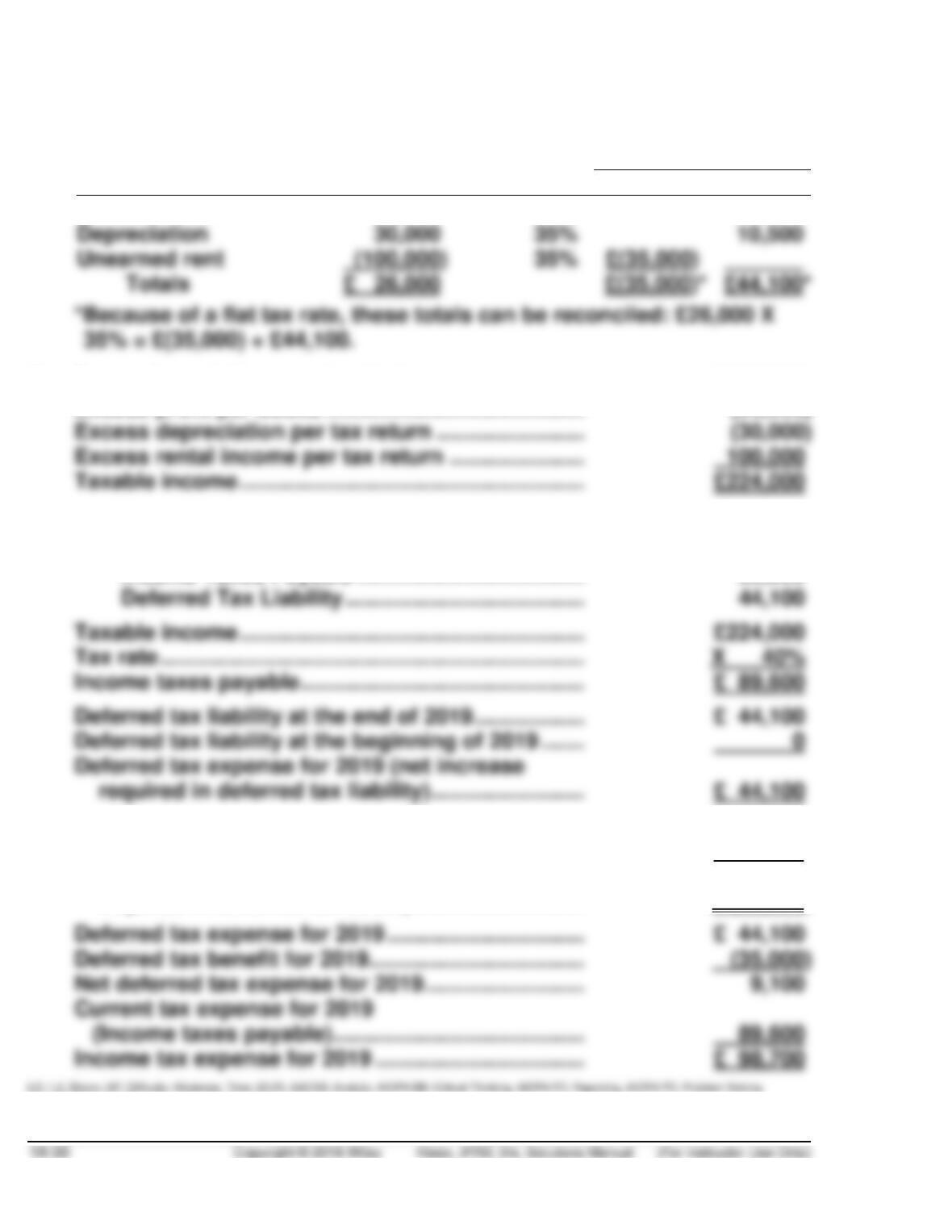

Depreciation

35%

Unearned rent

( (100,000)

35%

Totals

(£ 26,000

£44,100*

(b) Pretax financial income for 2019 ………………………. £250,000

Excess profit per books …………………………………… (96,000)

(c) Income Tax Expense ……………………………………….. 98,700

Deferred Tax Asset ………………………………………….. 35,000

Income Taxes Payable ………………………………. 89,600

Deferred tax asset at the end of 2019 ………………… £ 35,000

Deferred tax asset at the beginning of 2019 ………. 0

Deferred tax benefit for 2019 (net increase

required in deferred tax asset) ………………………. £ (35,000)

EXERCISE 19.19 (25–30 minutes)

(a) (All figures are in ¥ millions.)

Temporary Difference

Rate

Resulting Deferred Tax

(Asset)

Liability

(b) Non-current assets

Deferred tax asset

(¥36,000,000 – ¥20,000,000) ……….. ¥ 16,000,000

(c) Income before income taxes ……………….. ¥ 95,000,0002

Income tax expense

1Taxable income for 2019 ……………………. ¥160,000,000

Enacted tax rate ………………………….. X 40%

Income taxes payable for 2019 ……… ¥ 64,000,000

Cumulative deductible temporary difference

at the end of 2019 ……………………………………………….. ¥ 90,000,000

Cumulative deductible temporary difference

at the beginning of 2019 ………………………………………. 0

EXERCISE 19.19 (Continued)

Pretax financial income for 2019 ……………………………. ¥ X

Taxable temporary difference originating ……………….. (25,000,000)

Deductible temporary difference originating …………… 90,000,000

Taxable income for 2019 ……………………………………….. ¥160,000,000

Solving for X:

Deferred tax asset at the end of 2019 ……………………… ¥ 36,000,000

Deferred tax asset at the beginning of 2019 ……………. 0

Deferred tax benefit for 2019 (increase in

deferred tax asset) …………………………………………….. (36,000,000)

Deferred tax expense for 2019 …………………………..…… 10,000,000

Net deferred tax benefit for 2019 ……………………………. ¥ (26,000,000)

EXERCISE 19.20 (15–20 minutes)

(a) Income Tax Expense ……………………………………… 156,000

Deferred Tax Asset ………………………………………… 51,000

Income Taxes Payable …………………………….. 187,000

Deferred Tax Liability …………………………..….. 20,000

Future Years

2020

2021

2022

Total

Future taxable (deductible) amounts

Depreciation

Warranty costs

EXERCISE 19.20 (Continued)

Taxable income for 2019 ………………………………………….. $550,000

Tax rate …………………………………………………………………… X 34%

Income taxes payable for 2019 …………………………………. $187,000

Deferred tax asset at the end of 2019 ………………………… $ 51,000

Deferred tax asset at the beginning of 2019 ………………. 0

Deferred tax benefit for 2019 (increase in

deferred tax asset) ……………………………………………….. $ (51,000)

Deferred tax benefit for 2019 ……………………………………. $ (51,000)

Deferred tax expense for 2019 ………………………………….. 20,000

EXERCISE 19.21 (20–25 minutes)

(a) Income Tax Expense ………………………………………….. 212,680

Deferred Tax Asset …………………………………………….. 12,920

Income Taxes Payable …………………………………. 136,000

Deferred Tax Liability …………………………..………. 89,600

Taxable income ………………………………………………….. $400,000

Temporary

Difference

Future Taxable

(Deductible)

Amounts

Tax

Rate

Deferred Tax

(Asset)

Liability

Installment sale

*$ 40,000*

34%1

$13,600

$89,600

Deferred tax liability at the end of 2019 ……………………. $ 89,600

Deferred tax liability at the beginning of 2019 ………….. 0

Deferred tax expense for 2019 …………………………..……. $ 89,600

Deferred tax benefit for 2019 …………………………………… (12,920)

(b) Non-current liabilities

Deferred tax liability ($89,600 – $12,920) ………………….. $ 76,680

EXERCISE 19.22 (15–20 minutes)

(a) Income Tax Expense ………………………………………. 112,200

Deferred Tax Asset …………………………………………. 6,800

Temporary

Difference

Future Taxable

(Deductible) Amounts

Tax

Rate

Deferred Tax

(Asset)

Liability

*Because of a flat tax rate for all periods, these totals can be reconciled

as follows: $30,000 X 34% = $(6,800) + $17,000.

Deferred tax liability at the end of 2019 ……………………… $ 17,000

Deferred tax asset at the end of 2019 ………………………… $ 6,800

Deferred tax asset at the beginning of 2019 ………………. 0

Deferred tax benefit for 2019 (increase

required in deferred tax asset) ………………………………. $ (6,800)

Deferred tax expense for 2019 ………………………………….. $ 17,000

Deferred tax benefit for 2019 ……………………………………. (6,800)

EXERCISE 19.23 (30–35 minutes)

(a) 2017

Income Tax Expense ………………………………………. 37,400

Income Taxes Payable (£110,000 X 34%) ……. 37,400

2018

2020

Income Tax Expense ……………………………………… 83,600

Income Taxes Payable …………………………….. 60,800*

Deferred Tax Asset ………………………………….. 22,800

*[(£220,000 – £60,000) X 38%]

(b) Operating loss before income taxes ………………… £(260,000)

(c) 2019

Income Tax Refund Receivable ………………………. 68,000

Deferred Tax Asset ………………………………………… 17,100

EXERCISE 19.23 (Continued)

2020

Income Tax Expense …………………………………………. 83,600

Deferred Tax Asset …………………………………….. 17,100

(d) Operating loss before income taxes …………………… £(260,000)

Income tax benefit

Benefit due to loss carryback ……………………… £68,000

Benefit due to loss carryforward …………………….. 17,100 85,100

Net loss ……………………………………………………………. £(174,900)

Note: Using the assumption in part (a), the income tax section of the

2020 income statement would appear as follows:

EXERCISE 19.24 (30–35 minutes)

(a) 2017

Income Tax Expense ……………………………………… 40,000

Income Taxes Payable (€100,000 X 40%) ……. 40,000

2018

Income Tax Expense ……………………………………… 54,000

Deferred Tax Asset …………………………..………. 11,250

Benefit Due to Loss Carryforward ……………… 11,250

Income Taxes Payable

[(€120,000 – €50,000) X 45%] ………………….. 31,500

EXERCISE 19.25 (15–20 minutes)

(a) 2019

Income Tax Expense ($90,000 X .40) ………………. 36,000

Income Taxes Payable ……………………………. 36,000

2020

2021

Income Tax Expense ($180,000 X .40) …………….. 72,000

Income Taxes Payable

[($180,000 – $110,000) X .40] ……………….. 28,000

Deferred Tax Asset ………………………………… 35,200

Benefit Due to Loss Carryforward …………… 8,800

TIME AND PURPOSE OF PROBLEMS

Problem 19.1 (Time 40–45 minutes)

Purpose—to provide the student with an understanding of how to compute and properly classify

Problem 19.2 (Time 50–60 minutes)

Purpose—to provide the student with a situation where: (1) a temporary difference originates over a

three-year period and begins to reverse in the fourth period, (2) a change in an enacted tax rate occurs

Problem 19.3 (Time 40–45 minutes)

Purpose—to provide the student with an understanding of how future temporary differences for existing

depreciable assets are considered in determining the future years in which existing temporary

Problem 19.4 (Time 20–25 minutes)

Purpose—to provide the student with an understanding of permanent and temporary differences when

there are multiple differences and a single rate.

Problem 19.5 (Time 20–25 minutes)

Purpose—to provide the student with a situation involving a net operating loss which can be partially

Problem 19.6 (Time 20–25 minutes)

Purpose—to provide the student with an understanding of how the computation and classification of

Problem 19.7 (Time 45–50 minutes)

Purpose—to provide the student with a situation where: (1) a temporary difference originates in one