EXERCISE 4.7 (30–40 minutes)

(a) WEATHERSPOON SHOE

Statement of Comprehensive Income

For the Year Ended December 31, 2019

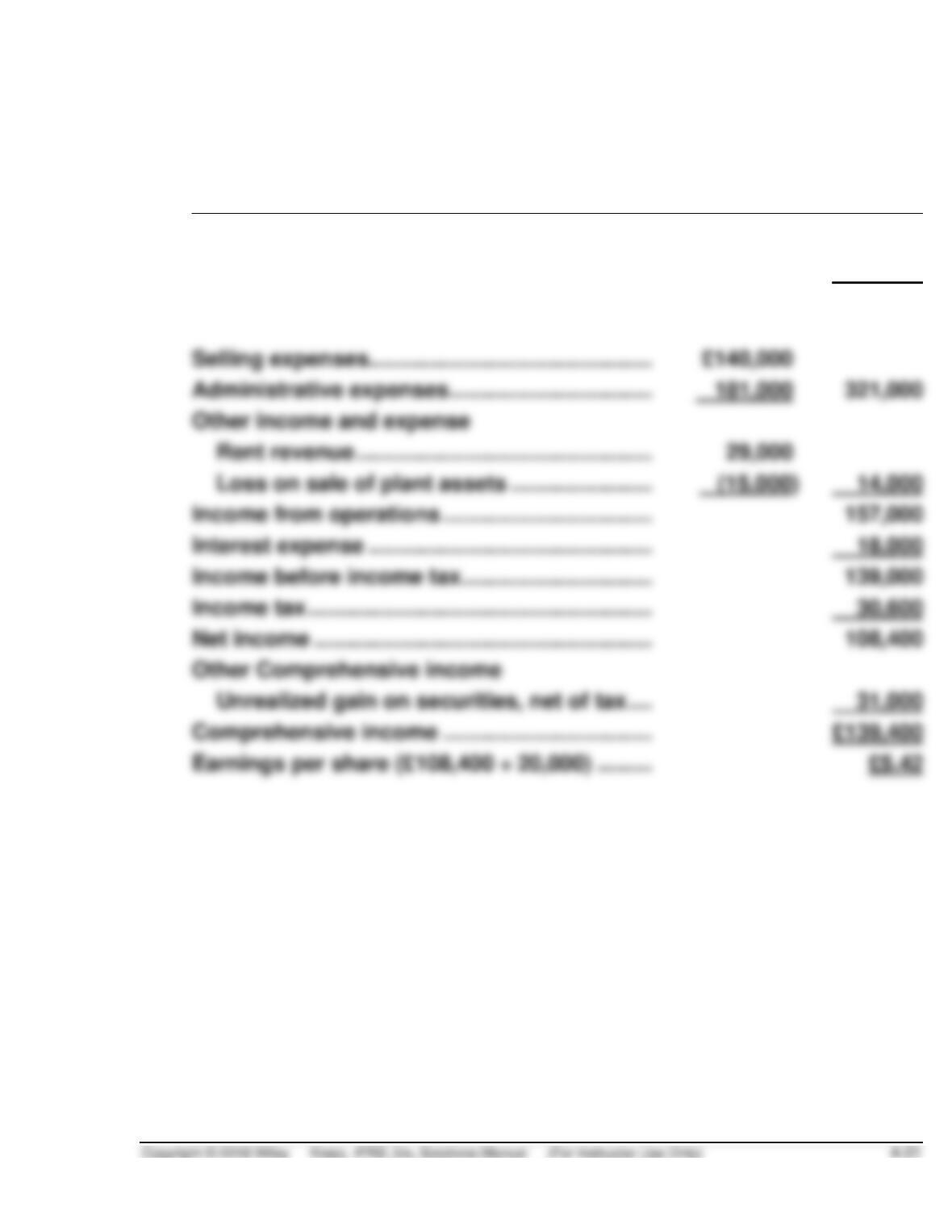

Net sales …………………………………………………..

£980,000

Cost of goods sold ……………………………………

516,000

Gross profit ………………………………………………

464,000

Selling expenses ……………………………………….

Administrative expenses …………………………...

321,000

Other income and expense

Rent revenue …………………………………………

Loss on sale of plant assets …………………..

14,000

Income from operations …………………………….

157,000

Interest expense ……………………………………….

18,000

Income before income tax ………………………….

139,000

Income tax ………………………………………………..

30,600

Net income ……………………………………………….

108,400

Other Comprehensive income

Unrealized gain on securities, net of tax ….

31,000

Comprehensive income …………………………….

£139,400

Earnings per share (£108,400 ÷ 20,000) ………

EXERCISE 4.7 (Continued)

(b) WEATHERSPOON SHOE

Income Statement

For the Year Ended December 31, 2019

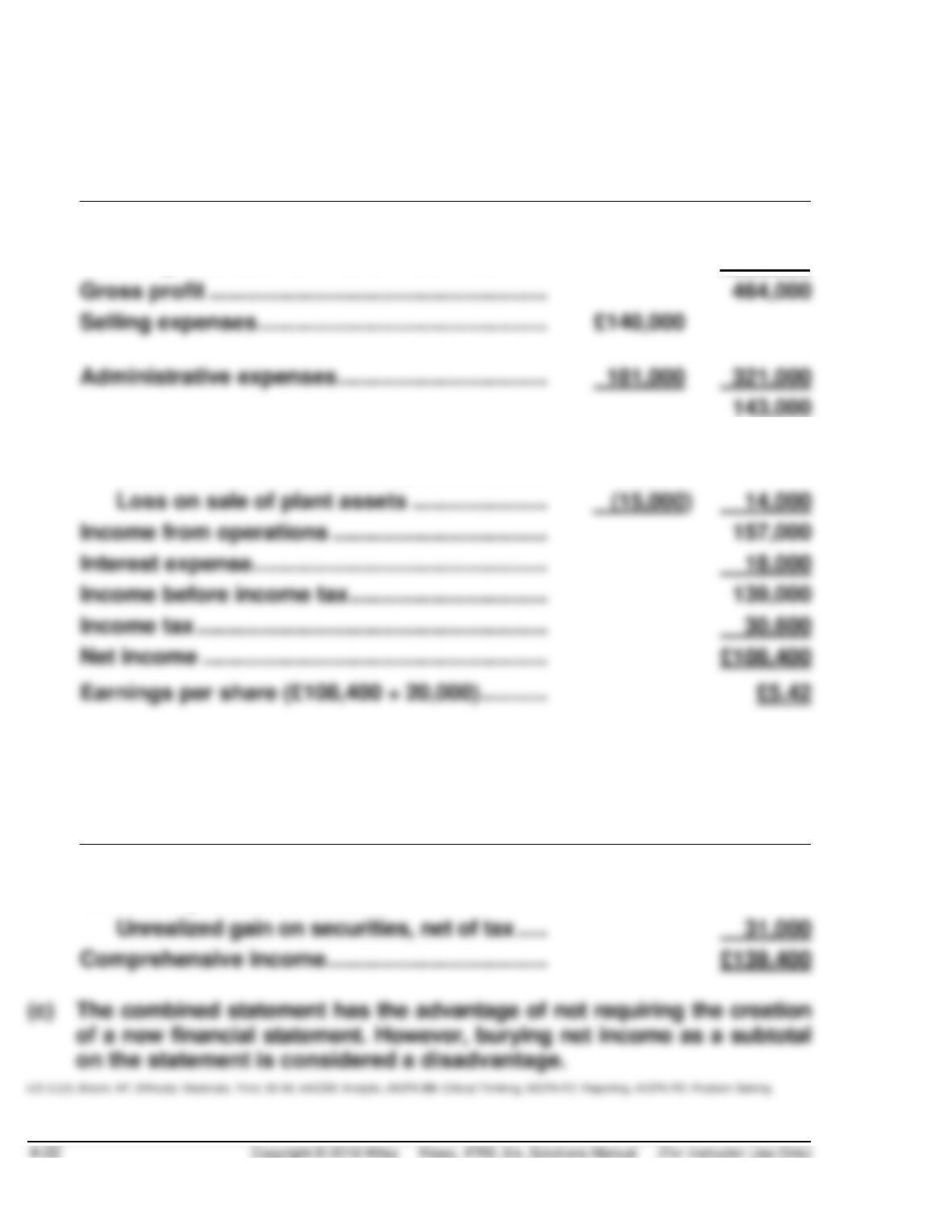

Net sales ……………………………………………………

£980,000

Cost of goods sold …………………………………….

516,000

Gross profit ……………………………………………….

Administrative expenses …………………………….

321,000

Other income and expense

Rent revenue ………………………………………..

29,000

Loss on sale of plant assets ………………….

14,000

Income from operations ……………………………..

Interest expense …………………………………………

18,000

Income before income tax …………………………..

Income tax …………………………………………………

30,600

WEATHERSPOON SHOE

Comprehensive Income Statement

For the Year Ended December 31, 2019

Net income ………………………………………………..

£108,400

Other comprehensive income

Unrealized gain on securities, net of tax …..

31,000

Comprehensive income ………………………………

£139,400

EXERCISE 4.8 (15–20 minutes)

(a) Net sales …………………………………………………………….. € 540,000

Less: Cost of goods sold …………………………………….. (260,000)

(b) Income before income tax ……………………………………. €100,000*

Income tax (€100,000 X .30) ………………………………….. 30,000

Income from continuing operations………………………. 70,000

Discontinued operations, less applicable

EXERCISE 4.9 (30–35 minutes)

(a) TAO LTD

Income Statement

For the Year Ended December 31, 2019

Sales

Net sales …………………………..…………………………..

HK$1,200,000

Cost of goods sold …………………………..……………….

780,000

Gross profit …………………………………………….

420,000

Selling expenses ……………………………………………….

HK$65,000

Administrative expenses …………………………..

48,000

113,000

Other income and expense

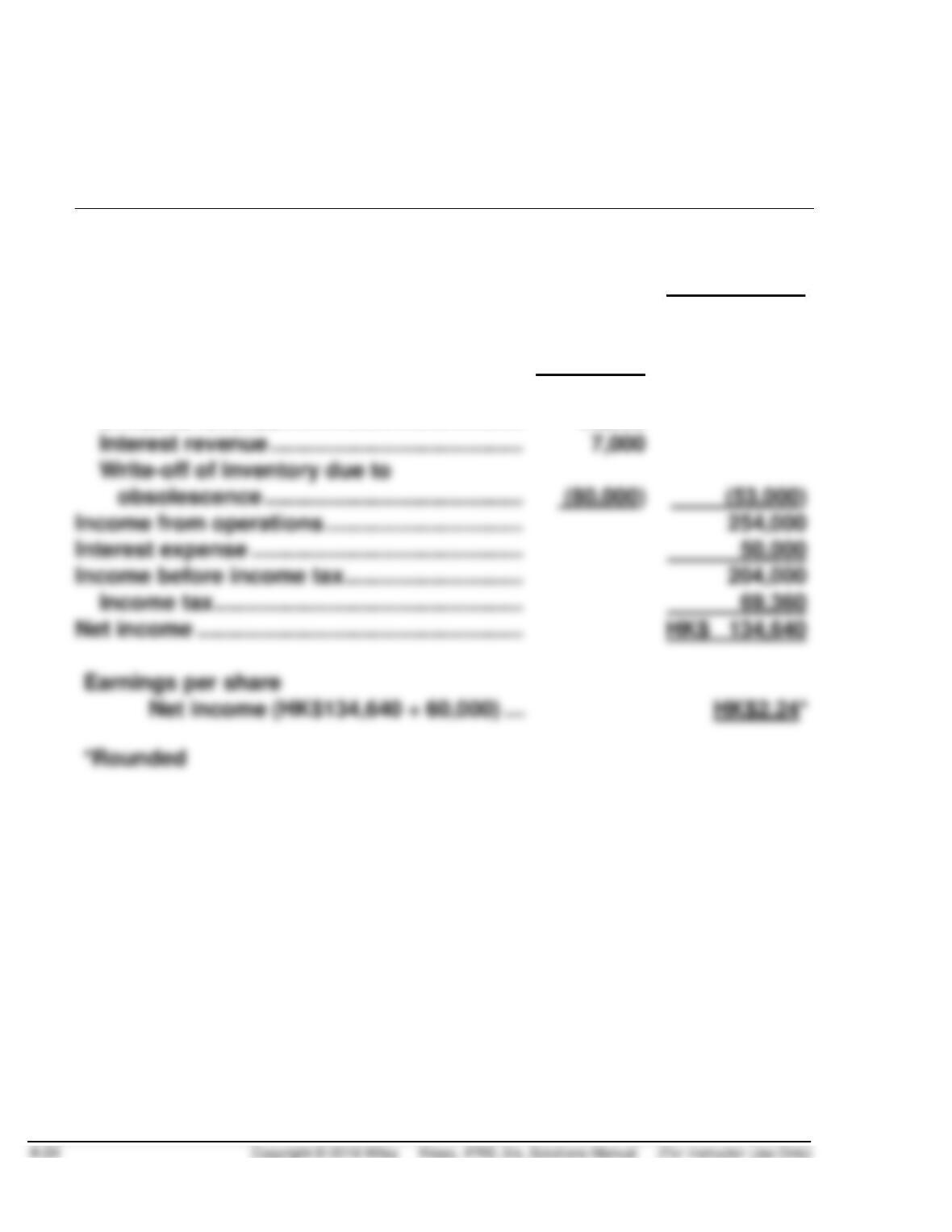

Dividend revenue ………………………………………………..

20,000

Interest revenue ………………………………………………….

Income from operations …………………………..

254,000

Interest expense …………………………………………………….

50,000

Income before income tax …………………………..

Income tax …………………………..…………………………..

69,360

Net income ……………………………………………………….

HK$ 134,640

Earnings per share

EXERCISE 4.9 (Continued)

(b) TAO LTD

Retained Earnings Statement

For the Year Ended December 31, 2019

Retained earnings, Jan. 1, as reported …………………………..

HK$ 980,000

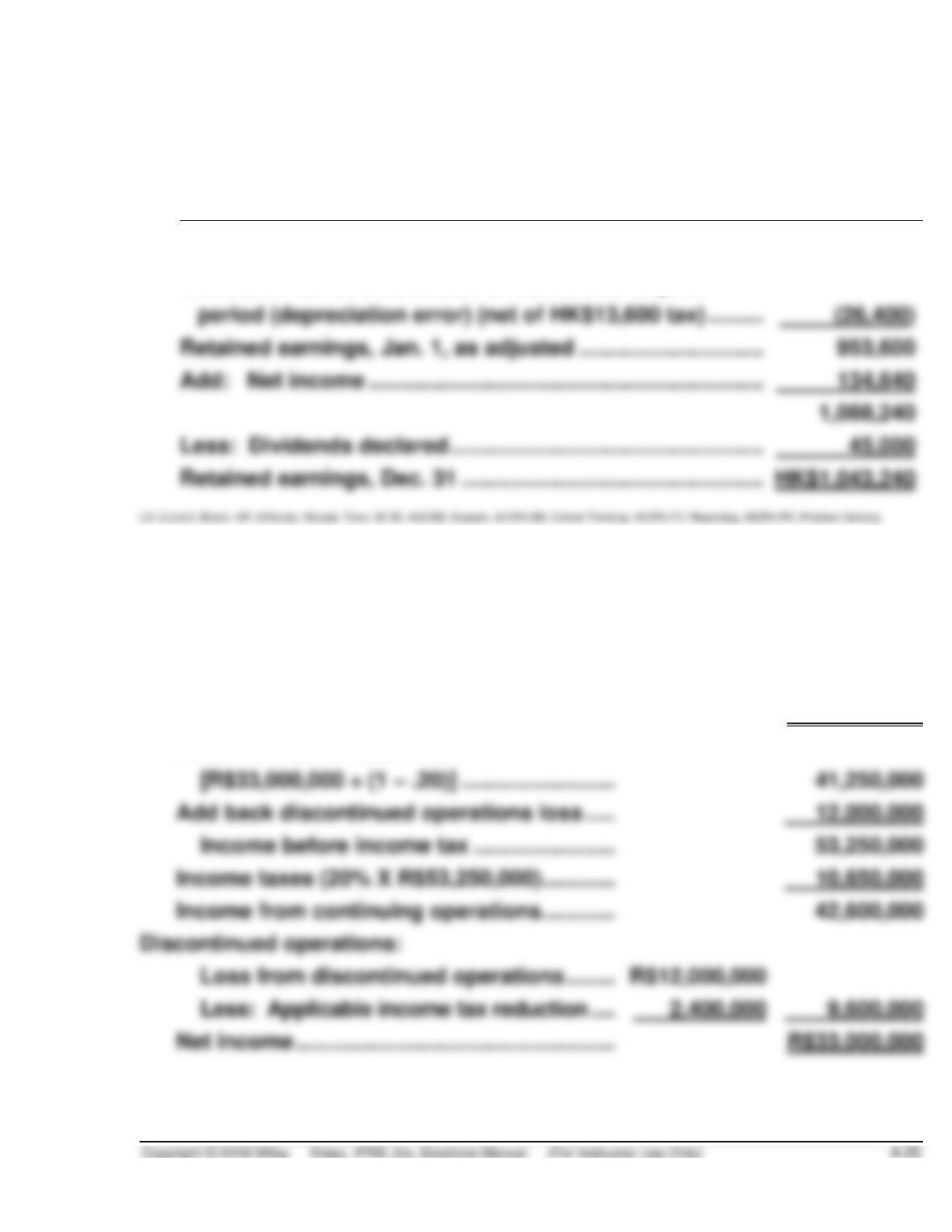

period (depreciation error) (net of HK$13,600 tax) ……………………

Retained earnings, Jan. 1, as adjusted …………………………..

Add: Net income ……………………………………………………….

Less: Dividends declared ……………………………………………………….

Correction for overstatement of net income in prior

EXERCISE 4.10 (20–25 minutes)

Computation of net income:

2019 net income after tax …………………………..

R$33,000,000

2019 net income before tax

[R$33,000,000 ÷ (1 – .20)] …………………………..

Add back discontinued operations loss …………………………..

Income before income tax …………………………..

Income taxes (20% X R$53,250,000) …………………………..

Income from continuing operations …………………………..

Discontinued operations:

Loss from discontinued operations …………………………..

Less: Applicable income tax reduction …………………………..

EXERCISE 4.10 (Continued)

Net income ………………………………………………………………………..

R$33,000,000

Less: Provision for preference dividends

Income available to ordinary shareholders ………………………….

Ordinary shares ……………………………………………………….

Income statement presentation

Earnings per share:

Income from continuing operations …………………………..

R$4.23a

Discontinued operations, net of tax …………………………..

EXERCISE 4.11 (20–25 minutes)

WOODS CORPORATION

Income Statement

For the Year Ended December 31, 2019

Net sales(a) ………………………………………………………

$4,062,000

Cost of goods sold(b) …………………………..……………

2,665,000

Gross profit ………………………………………………..

1,397,000

Selling expenses(c) …………………………………………..

$636,000

Administrative expenses(d) ……………………………….

491,000

1,127,000

Other income and expense

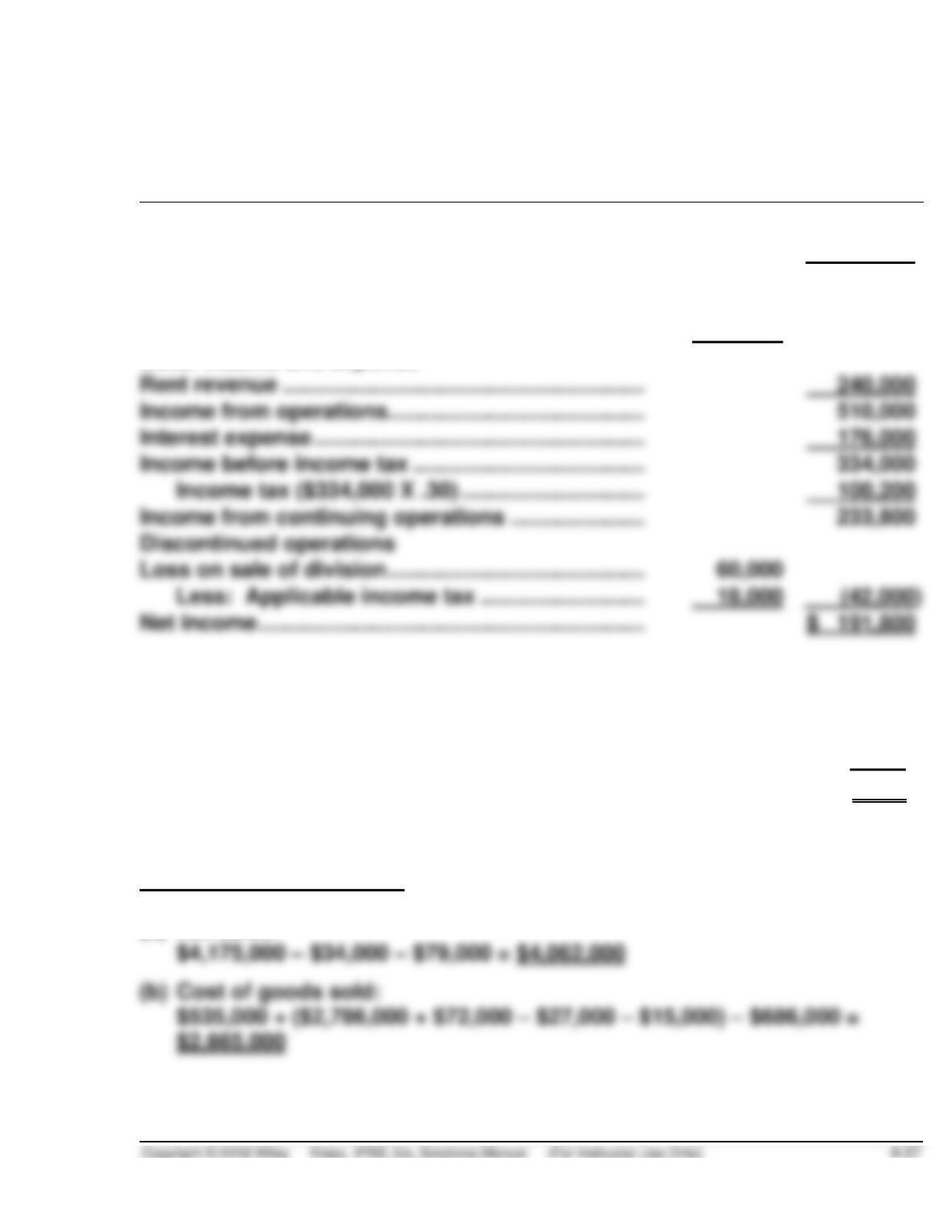

Rent revenue …………………………………………………..

240,000

Income from operations……………………………………

510,000

Interest expense ………………………………………………

176,000

Income before income tax ………………………………..

Income tax ($334,000 X .30) …………………………

100,200

Income from continuing operations ………………….

Discontinued operations

Loss on sale of division ……………………………………

Less: Applicable income tax ………………………

18,000

(42,000)

Net income ………………………………………………………

Earnings per share

($900,000 ÷ $10 par value = 90,000 shares)

Income from continuing operations ($233,800 ÷ 90,000) ……

$2.60*

Discontinued operations, net of tax …………………………………

(0.47)*

Net income …………………………………………………………………….

$2.13

*Rounded

Supporting computations

(a) Net sales:

EXERCISE 4.11 (Continued)

(c) Selling expenses:

EXERCISE 4.12 (20–25 minutes)

(a) McENTIRE CORPORATION

Retained Earnings Statement

For the Year Ended December 31, 2019

Balance, January 1, as reported ……………………………………….

$225,000*

Correction for depreciation error (net of $5,000 tax) ………….

(20,000)

inventory methods (net of $9,000 tax) …………………………

Balance, January 1, as adjusted ……………………………………….

Add: Net income ……………………………………………………….

Less: Dividends declared ……………………………………………….

(b) Total retained earnings would still be reported as $245,000. A restriction

does not affect total retained earnings; it merely labels part of the retained

earnings as being unavailable for dividend distribution. Retained earnings

would be reported as follows:

Retained earnings:

Appropriated ……………………………………………..

Unappropriated ………………………………………….

EXERCISE 4.13 (15–20 minutes)

Net income:

Income before income tax …………………………..

€21,650,000

Income tax (35% X €21,650,000) …………………………..

7,577,500

Income from continuing operations …………………………..

Discontinued operations

Loss before income tax…………………………..

Less: Applicable income tax (35%) …………………………..

Preference dividends declared: …………………………..

€ 860,000

Weighted average shares outstanding …………………………..

4,000,000

Earnings per share

Income from continuing operations …………………………..

€3.30*

Discontinued operations, net of tax …………………………..

EXERCISE 4.14 (15–20 minutes)

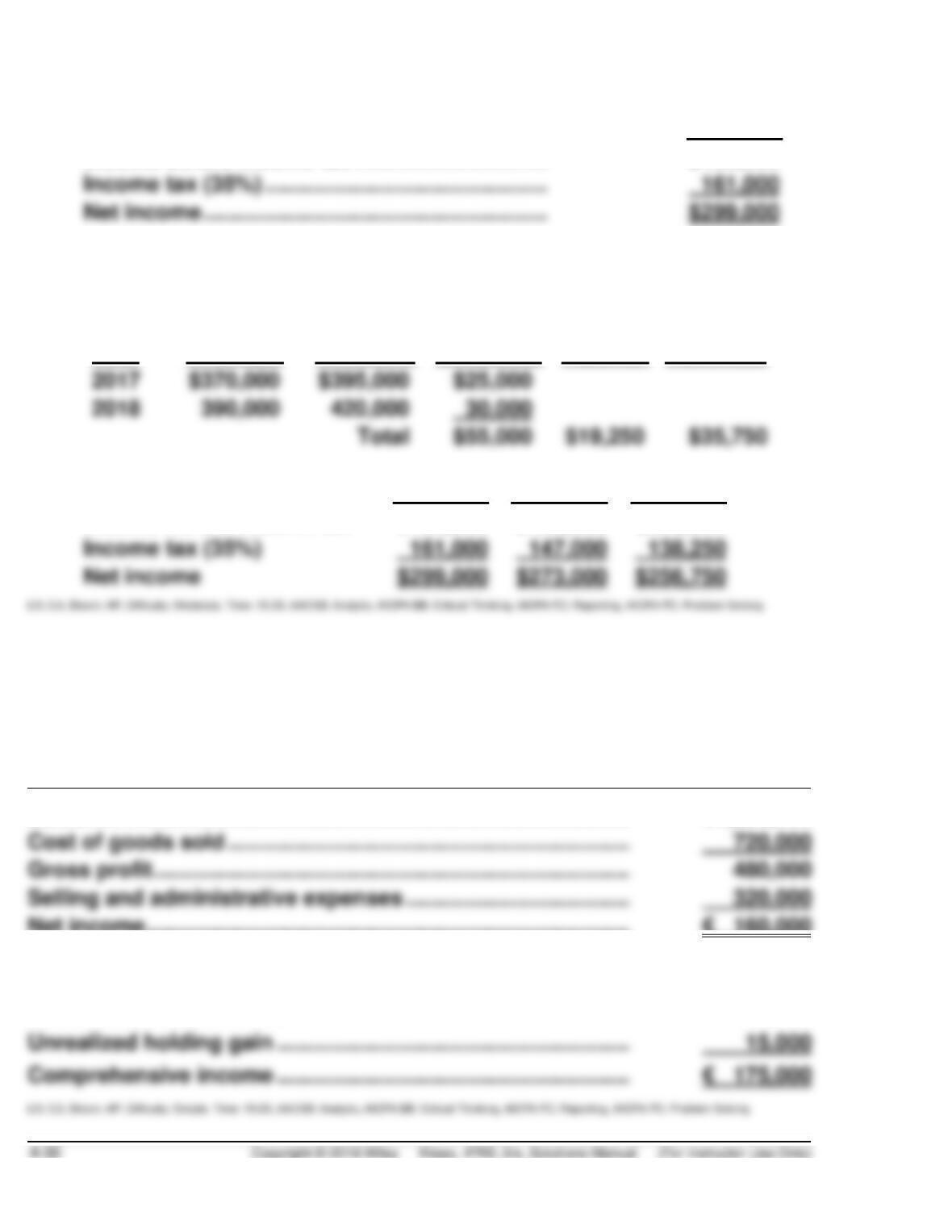

(a) 2019

Income before income tax …………………………. $460,000

(b) Cumulative effect for years prior to 2019:

Year

Weighted

Average

FIFO

Difference

Tax Rate

(35%)

Net Effect

$395,000

390,000

$19,250

(c)

2019

2018

2017

Income before income tax

$460,000

$420,000

$395,000

Income tax (35%)

Net income

$299,000

$273,000

$256,750

EXERCISE 4.15 (15–20 minutes)

GAERTNER AG

Income Statement

For the Year Ended December 31, 2019

Sales ………………………………………………………………………………

€1,200,000

Cost of goods sold ………………………………………………………….

Gross profit …………………………………………………………………….

Selling and administrative expenses ………………………………..

Net income ……………………………………………………………………..

€ 160,000

Comprehensive Income Statement

Net income ……………………………………………………………………..

€ 160,000

Unrealized holding gain …………………………………………………..

Comprehensive income …………………………………………………..

€ 175,000

EXERCISE 4.16 (15–20 minutes)

BRYANT PLC

Statement of Changes in Equity

For the Year Ended December 31, 2019

Share Capital—

Ordinary

Retained

Earnings

Accumulated

other

Comprehensive

Income

Total

Equity

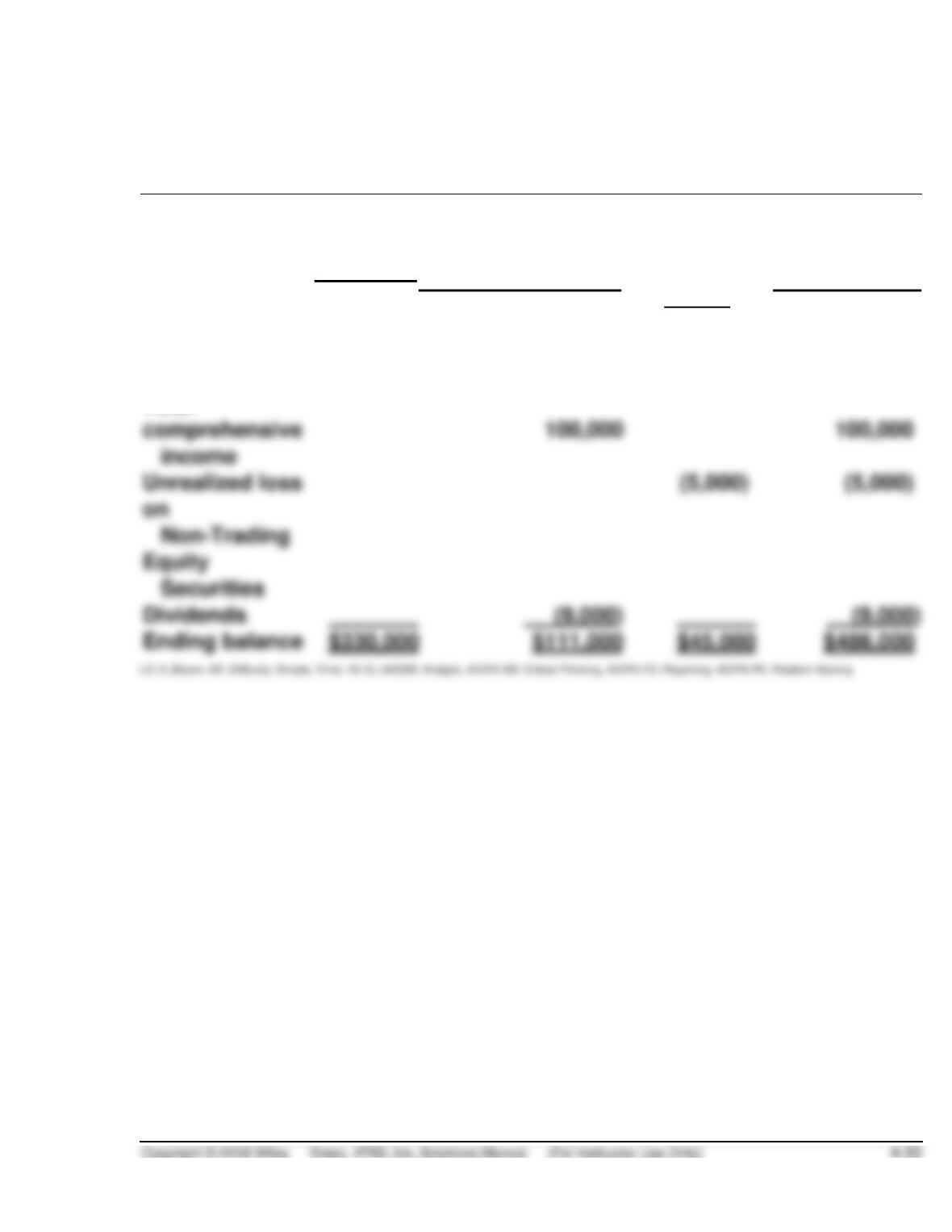

Beginning balance

£350,000

£ 90,000

£80,000

£520,000

Total comprehensive

income

170,000*

170,000

Dividends

EXERCISE 4.17 (30–35 minutes)

(a) VEGA SA

Statement of Comprehensive Income

For the Year Ended December 31, 2019

Sales ………………………………………………………………………………..

R$1,700,000

Cost of goods sold ……………………………………………………….

850,000

Gross profit ……………………………………………………….

Selling expenses ……………………………………………………….

Administrative expenses …………………………………………………..

Other income and expense

Gain on sale of plant assets …………………………..

Rent revenue …………………………………………………

Loss on impairment of land…………………………..

EXERCISE 4.17 (Continued)

Income before income tax ………………………………………

385,000

Income tax ……………………………………………………….

119,000

Income from continuing operations ………………………..

266,000

Discontinued operations

Loss on discontinued operations ……………………

R$ 75,000

Less: Applicable income tax reduction ………………

Net income ……………………………………………………….

216,500

Other comprehensive income

Unrealized holding gain …………………………..

Earnings per share:

(R$266,000 ÷ 100,000) …………………………………………………

Loss on discontinued operations, net of tax ……………………

Income from continuing operations

(b) VEGA SA

Retained Earnings Statement

For the Year Ended December 31, 2019

Retained earnings, January 1 …………………………………………………

R$600,000

Add: Net income ……………………………………………………….

216,500

816,500

Less: Dividends declared …………………………..………………………….

150,000

EXERCISE 4.18 (10–15 minutes)

HASBRO INC.

Statement of Changes in Equity

For the Year Ended December 31, 2019

Share

Capital—

Ordinary

Retained Earnings

Accumulated

other

Comprehensive

Income

Total Equity

Beginning

balance

$300,000

$20,000

$50,000

$370,000

Capital shares

30,000

30,000

100,000

Dividends

Ending balance

Total

TIME AND PURPOSE OF PROBLEMS

Problem 4.1 (Time 5–10 minutes)

Purpose––to provide the student with an opportunity to indicate where various transactions would be

reported on the Statement of Comprehensive Income or the Statement of Retained Earnings.

Problem 4.2 (Time 30–35 minutes)

Problem 4.3 (Time 25–30 minutes)

Problem 4.4 (Time 30–40 minutes)

Problem 4.5 (Time 30–40 minutes)

Purpose—to provide the student with the opportunity to prepare an income statement and a retained

earnings statement from the same underlying information. A substantial number of operating expenses

must be reported in this problem unlike Problem 4.1. As a consequence, the problem is time-consuming.

Problem 4.6 (Time 20–25 minutes)

Purpose—to provide the student with a problem on the income statement treatment of (1) an

Problem 4.7 (Time 25–35 minutes)

Purpose—to provide the student with an opportunity to prepare a retained earnings statement. A number

Problem 4.8 (Time 25–35 minutes)

SOLUTIONS TO PROBLEMS

PROBLEM 4.1

1. E

2. C

PROBLEM 4.2

DICKINSON AG

Income Statement

For the Year Ended December 31, 2019

Sales ………………………………………………………………………

€25,000,000

Cost of goods sold ………………………………………………….

16,000,000

Gross profit ……………………………………………………….

9,000,000

Selling and administrative expenses ………………………..

4,700,000

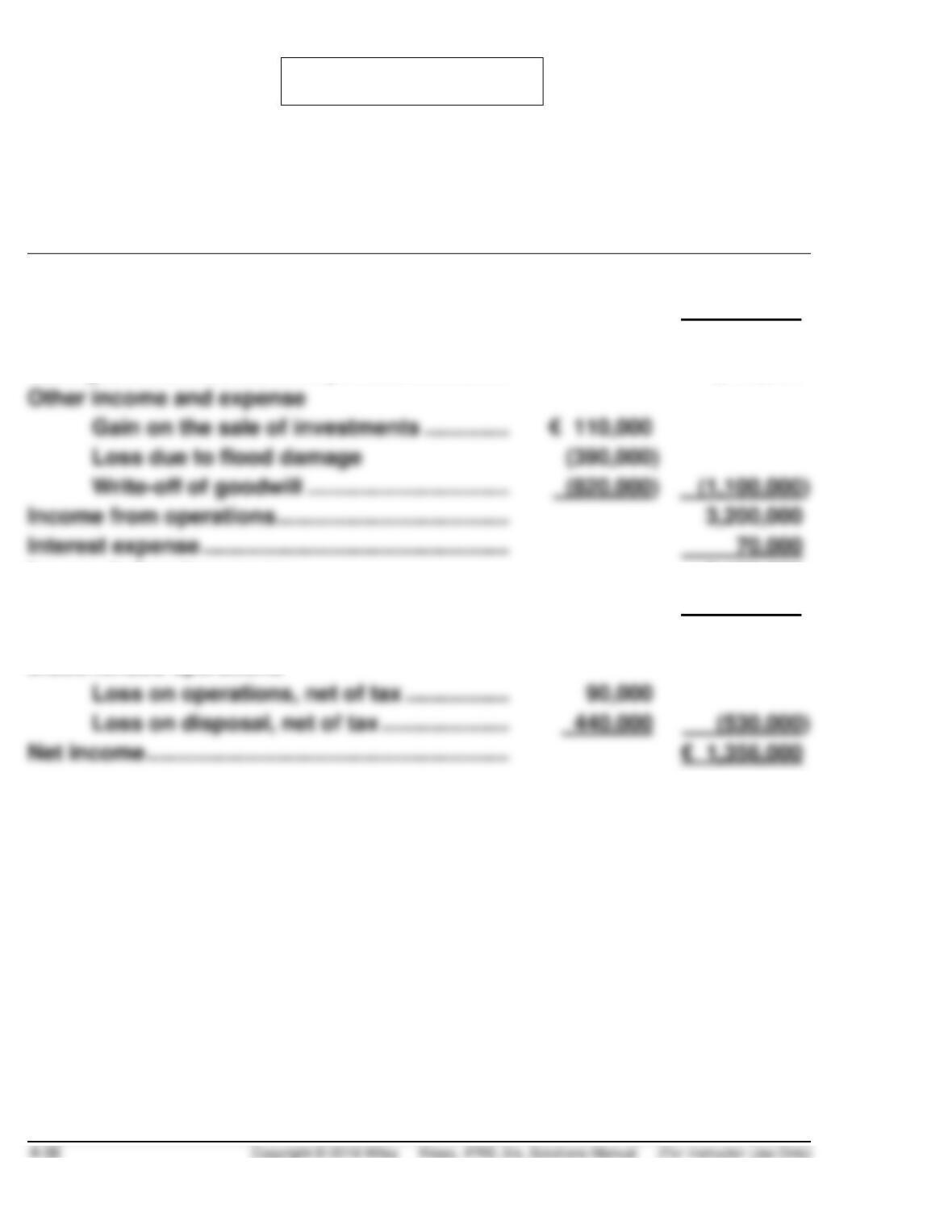

Other income and expense

Gain on the sale of investments ……………………..

Loss due to flood damage

Write-off of goodwill ………………………………………

Income from operations …………………………………………..

3,200,000

Interest expense ……………………………………………………..

70,000

Income before income tax ……………………………………….

3,130,000

Income tax ……………………………………………………….

1,244,000

Income from continuing operations ………………………….

1,886,000

Discontinued operations

Loss on operations, net of tax ………………………..

Loss on disposal, net of tax …………………………..

(530,000)

Net income ……………………………………………………….

PROBLEM 4.2 (Continued)

Earnings per share:

Income from continuing operations ………………..

€3.61a

Discontinued operations

Loss on operations, net of tax ………………..

€(0.18)

Loss on disposal, net of tax ……………………

(0.88)

Net income …………………………………………………….

€2.55b

DICKINSON AG

Retained Earnings Statement

For the Year Ended December 31, 2019

Retained earnings, January 1 …………………………..

€ 980,000

Add: Net income …………………………………………..

1,356,000

2,336,000

Less: Dividends

PROBLEM 4.3

THOMPSON LTD

Income Statement

For the Year Ended December 31, 2019

Net sales (£1,100,000 – £14,500 – £17,500) …………..

£1,068,000

Cost of goods sold* …………………………………………..

645,000

Gross profit ………………………………………………………

423,000

Selling expenses ……………………………………………….

£232,000

Administrative expenses ……………………………………

99,000

Other income and expense

Gain on sale of land …………………………………..

Rent revenue …………………………………………….

48,000

Income before income tax ………………………………….

140,000

53,900

*Cost of goods sold: Can be verified as follows:

Merchandise inventory, Jan. 1 …………………………..

£ 89,000

Purchases ……………………………………………………….

£610,000

Less: Purchase discounts ……………………………….

10,000

Net purchases ………………………………………………….

Add: Freight-in …………………………..…………………..

20,000

620,000

Merchandise available for sale ………………………….

Less: Merchandise inventory, Dec. 31 ………………

64,000

PROBLEM 4.3 (Continued)

THOMPSON LTD

Retained Earnings Statement

For the Year Ended December 31, 2019

Retained earnings, January 1 …………………………………………

£160,000

Add: Net income ……………………………………………………….

86,100

Less: Cash dividends …………………………..………………………

45,000

PROBLEM 4.4

MAHER AG

Income Statement (Partial)

For the Year Ended December 31, 2019

Income before income tax ……………………………………..

€748,500(a)

Income tax (€748,500 X .30) …………………………..

224,550

Income from continuing operations ………………………..

Discontinued operations

Loss from disposal of recreational division …..

Less: Applicable income tax reduction …………

Net income ……………………………………………………………

Earnings per share:

Income from continuing operations ………………

€4.37*

Discontinued operations, net of tax ………………