EXERCISE 22.15 (Continued)

4. Amortization Expense—Copyright …………………… 2,500(c)

Retained Earnings ………………………………………….. 5,000(d)

EXERCISE 22.16 (10–15 minutes)

1. Salaries and Wages Expense ………………………….. 3,400

Salaries and Wages Payable …………………….. 3,400

2. Salaries and Wages Expense ………………………….. 31,100

Salaries and Wages Payable …………………….. 31,100

EXERCISE 22.17 (10–15 minutes)

Retained Earnings …………………………………………………. 33,700*

Inventory ……………………………………………………….. 14,200**

Accumulated Depreciation—Equipment

($38,500(a) – $19,000(b)) …………………………………. 19,500

Computations: Effect on retained earnings

over (under) statement

Overstatement of 2019 ending inventory

($14,200**

Overstatement of 2018 depreciation

Understatement of 2019 depreciation

Total effect of errors on retained earnings

EXERCISE 22.18 (25–30 minutes)

(a) Effect of errors on 2019 net income: £21,700 overstatement

Computations:

Effect on 2019 net income

over (under) statement

Understatement of 2018 ending inventory

Effect on working capital

over (under) statement

Overstatement of 2019 ending inventory

£( 7,100

Total effect on working capital (understated)

(c) Effect of errors on retained earnings: £25,600 understatement

Computations:

Effect on retained earnings

over (under) statement

Overstatement of 2019 ending inventory

£( 7,100

EXERCISE 22.19 (20–25 minutes)

(a) 1. Supplies Expense (R2,500 – R1,100) …………….. 1,400

Supplies ………………………………………………. 1,400

5. Rental Income (R24,000 ÷ 2) …………………………. 12,000

Unearned Rent ……………………………………… 12,000

(b) 1. Retained Earnings ………………………………………. 1,400

Supplies ………………………………………………. 1,400

2. Retained Earnings ………………………………………. 2,900

Salaries and Wages Payable …………………. 2,900

6. Retained Earnings ………………………………………. 45,000

Accumulated Depreciation—Equipment … 45,000

7. Retained Earnings ………………………………………. 7,200

Accumulated Depreciation—Equipment … 7,200

[Same as in (a).]

EXERCISE 22.20 (20–25 minutes)

2018

2019

Income before tax

$101,000

$77,400

Corrections:

Sales erroneously included in 2018 income

(38,200)

38,200

Understatement of 2018 ending inventory

8,640

(8,640)

Adjustment to bond interest expense*

Corrected income before tax

*Bond interest expense for 2018 and 2019 was computed as follows:

Book Value of Bonds

Stated Interest

Effective Interest

2018

$240,000

$15,000^

$16,800**

2019

241,800

15,000^

16,926****

EXERCISE 22.21 (10–15 minutes)

2018

2019

Item

Over–

statement

Under-

statement

No

Effect

Over–

statement

Under-

statement

No

Effect

(1)

X

X

(2)

X

X

(3)

X

(4)

X

X

(5)

X

X

TIME AND PURPOSE OF PROBLEMS

Problem 22.1 (Time 30–35 minutes)

Purpose—to provide a problem that requires the student to: (1) account for two changes in estimate,

Problem 22.2 (Time 30–40 minutes)

Purpose—to develop an understanding of the way in which accounting changes and error corrections

Problem 22.3 (Time 30–40 minutes)

Purpose—to provide a problem that requires the student to: (1) prepare correcting entries for two years’

unrecorded sales commissions, (2) three years’ inventory errors, and (3) prepare entries for two different

accounting changes.

Problem 22.4 (Time 40–50 minutes)

Problem 22.5 (Time 30–35 minutes)

Purpose—to develop an understanding of the impact which a change in the method of inventory pricing

Problem 22.6 (Time 25–30 minutes)

Purpose—to develop an understanding of the journal entries and the reporting which are necessitated

Problem 22.7 (Time 25–30 minutes)

Problem 22.8 (Time 30–35 minutes)

Purpose—to help a student understand the effect of errors on income and retained earnings. The

Problem 22.9 (Time 20–25 minutes)

Purpose—to develop an understanding of the effect that errors have on the financial statements. The

Time and Purpose of Problems (Continued)

Problem 22.10 (Time 50–60 minutes)

Purpose—to develop an understanding of the correcting entries and income statement adjustments that

SOLUTIONS TO PROBLEMS

PROBLEM 22.1

(a) 1. Cost of equipment ………………………………………… $85,000(a)

Less: Residual value …………………………………….. 5,000

Depreciable cost ………………………………………….. $80,000

Depreciation to 2019

Depreciation in 2019

Cost of equipment …………………………………. $85,000(a)

Depreciation in 2019

2. Cost of Building …………………………………………… $300,000

Less: Depreciation to 2019

2017…………………………………………………… 60,000

PROBLEM 22.1 (Continued)

3. Depreciation Expense ($120,000(g) – $16,000) ÷ 8 .. 13,000(l)

Accumulated Depreciation—Machine …………. 13,000

Accumulated Depreciation—Machine ……………….. 3,000

Retained Earnings …………………………………….. 3,000(q)

Depreciation recorded in 2017:

Depreciation

taken

Depreciation that

should be taken

Differences

(b) HOLTZMAN COMPANY

Comparative Income Statements

For the Years 2019 and 2018

2019

2018

Income before depreciation expense………………..

$300,000

$310,000

Depreciation expense* …………………………………….

47,750(o)

69,000(p)

*Depreciation Expense

PROBLEM 22.2

(a) 1. Bad debt expense for 2016 should not have been reduced by

€10,000. A change in the experience rate is considered a change

in estimate, which should be handled prospectively.

(b) BOTTICELLI SpA

Comparative Income Statements

For the Years 2016 through 2019

2016

2017

2018

2019

Net income (unadjusted)

€140,000

€160,000

€205,000

€276,000

3. Inventory

Net income (adjusted)

1. Bad debt expense

PROBLEM 22.3

1. Retained Earnings …………………………………. 3,500,000

2. Cost of Goods Sold ………………………………. 25,700,000(a)

Retained Earnings …………………………... 19,000,000(b)

Inventory ………………………………………… 6,700,000(c)

Income Overstated (Understated)

2017

2018

2019

3. Accumulated Depreciation—

Equipment ………………………………………….. 4,800,000

Depreciation Expense ……………………… 4,800,000(d)

Equipment cost …………………………………….. ¥100,000,000

4. Construction in Process ………………………… 45,000,000(e)

Deferred Tax Liability ………………………. 18,000,000(f)

Retained Earnings …………………………... 27,000,000

PROBLEM 22.4

(a) ASTON PLC

Projected Income Statement

For the Year Ended December 31, 2019

Sales …………………………………………….. £29,000,000

Cost of goods sold ………………………… £14,000,000

Depreciation expense …………………….. 1,600,000(a)

Operating expenses ……………………….. 6,400,000 22,000,000

Conditions met:

1. Net income before taxes and bonus > £7,000,000.

2. Payable for income taxes does not exceed £3,000,000.

(a)Depreciation for the current year includes £600,000 for the old equip–

ment and £2,000,000 for the robotic equipment. If the robotic equipment

(b) Students’ answers will vary.

There is nothing unethical about changing the first-year election of

PROBLEM 22.4 (Continued)

immediate needs for cash of £1,000,000 for the president’s bonus and

£3,000,000 for income taxes, there may be a need to sell some of the

investments. Therefore, the transfer of £3,000,000 of held–for-collection

investments to trading investments may also be appropriate.

It is naive to believe that corporate officers do no planning for year-end

Some stakeholders and their interests are:

Stakeholder

Interests

President

Personal gain of £1,000,000 bonus.

CFO

Placed in ethical dilemma between the interests

of the president and the corporation.

for his personal gain.

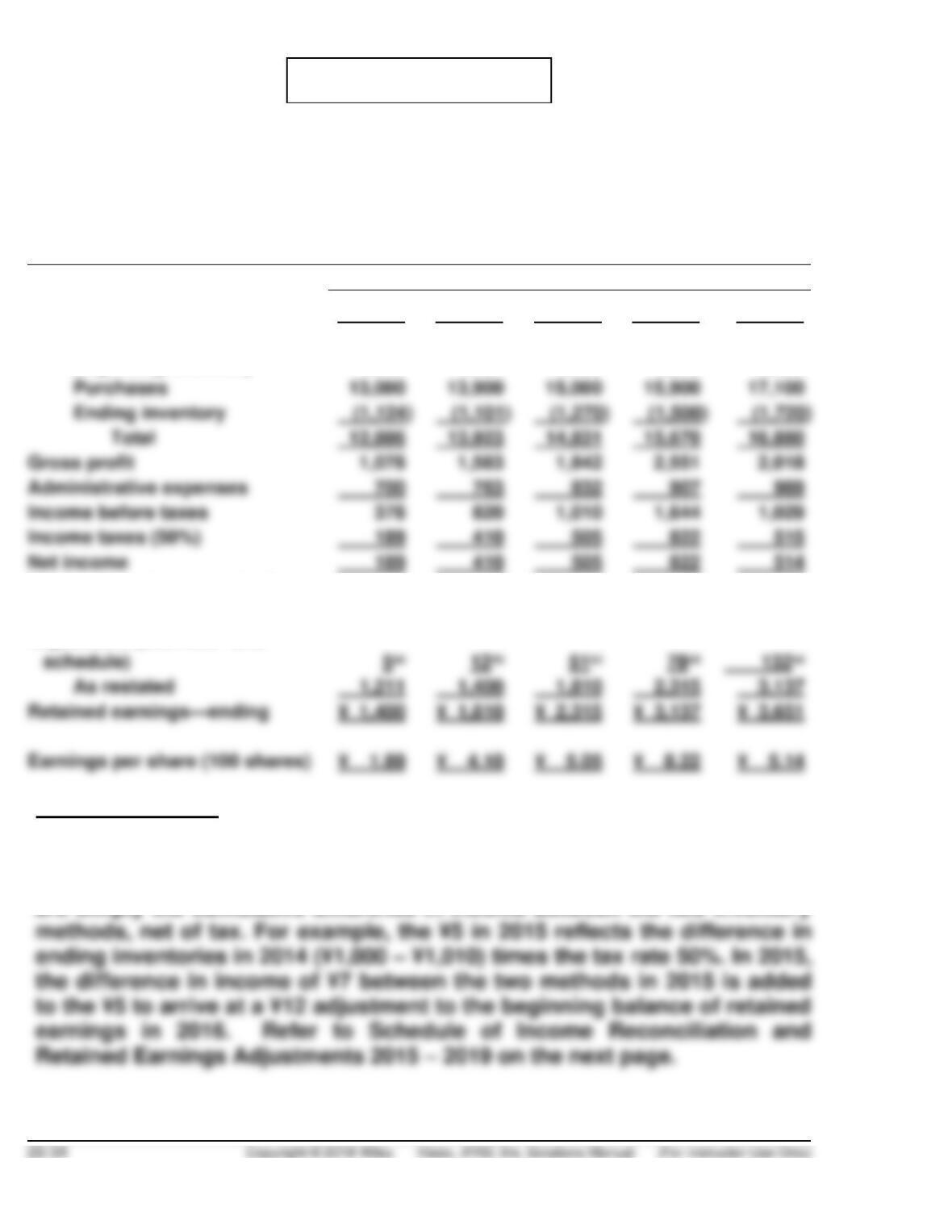

PROBLEM 22.5

UTRILLO INSTRUMENT LTD

Statement of Income and Retained Earnings

For the Years Ended May 31

(Amounts in millions)

2015

2016

2017

2018

2019

Sales—net

¥13,964

¥15,506

¥16,673

¥18,221

¥18,898

Cost of goods sold

Beginning inventory

1,010

1,124

1,101

1,270

1,500

Purchases

Ending inventory

Total

Gross profit

1,078

1,583

1,842

2,551

2,018

Administrative expenses

Income before taxes

1,010

1,644

1,029

Income taxes (50%)

Net income

Retained earnings—beginning:

As originally reported

1,206

1,388

1,759

2,237

3,005

As restated

Retained earnings—ending

Earnings per share (100 shares)

Adjustment (See note* and

*Note to instructor:

The retained earnings balances are usually reported in the above manner.

If desired, only the restated balances might be reported. The adjustments

are simply the cumulative difference in income between the two inventory

PROBLEM 22.5 (Continued)

In 2019, the Company changed its method of pricing inventory from the

first-in, first-out (FIFO) to the average cost method in order to more fairly

present the financial operations of the company. The financial statements

for prior years have been restated to retrospectively reflect this change,

resulting in the following effects on net income and related per share

amounts:

Increase in

2015

2016

2017

2018

2019

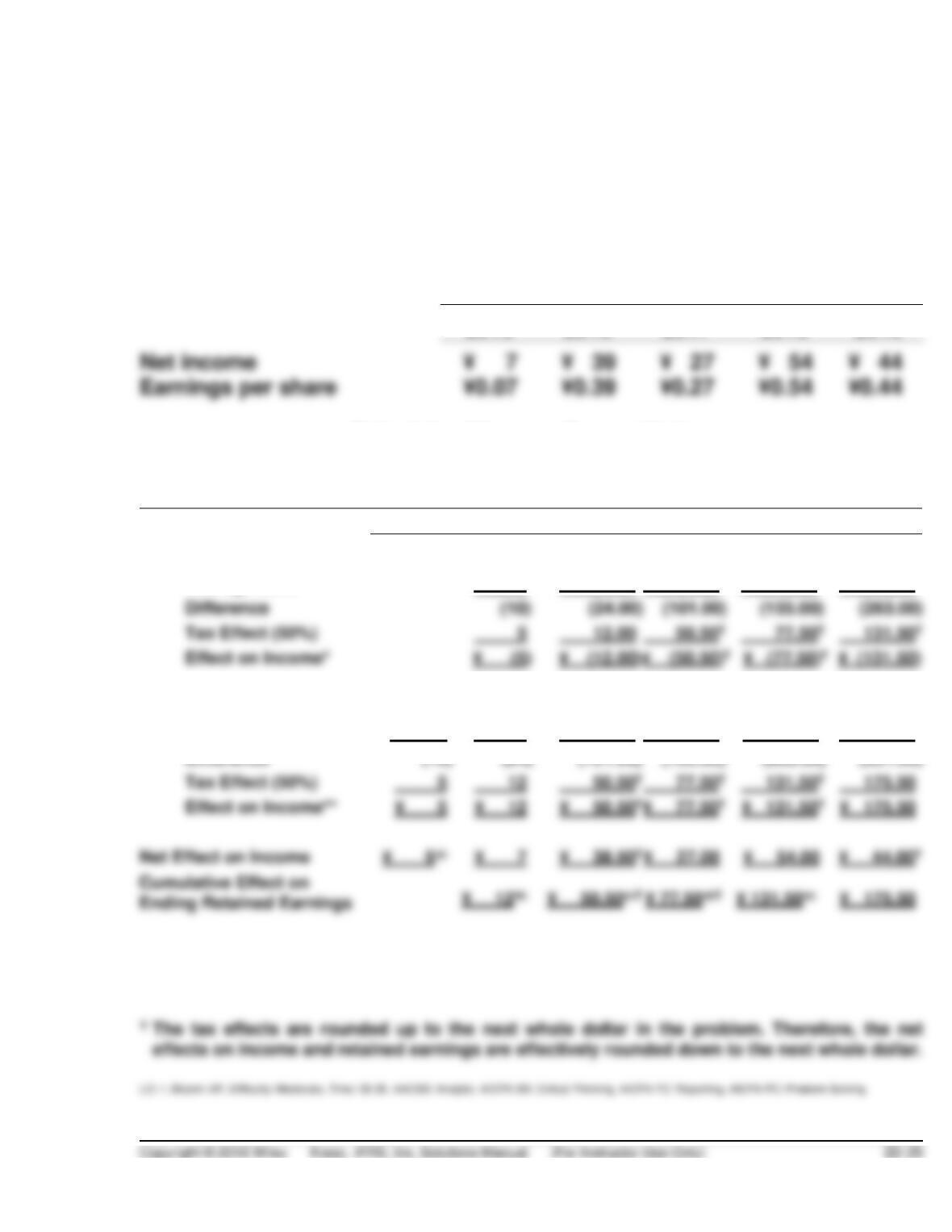

Schedule of Income Reconciliation

and Retained Earnings Adjustments

2015–2019

2014

2015

2016

2017

2018

2019

Beginning Inventory FIFO

¥1,000

¥1,100.00

¥1,000.00

¥1,115.00

¥1,237.00

Average Cost

1,010

1,124.00

1,101.00

1,270.00

1,500.00

Difference

Effect on Income*

¥ (12.00)

Ending Inventory FIFO

¥1,000

¥1,100

¥1,000.00

¥1,115.00

¥1,237.00

¥1,369.00

Average Cost

1,010

1,124

1,101.00

1,270.00

1,500.00

1,720.00

Difference

Tax Effect (50%)

5

12

175.50

Effect on Income**

¥ 5

¥ 12

¥ 175.50

Net Effect on Income

¥ 7

¥ 27.00

¥ 54.00

*Larger (smaller) beginning inventory has negative (positive) effect on net income.

**Larger (smaller) ending inventory has positive (negative) effect on net income.

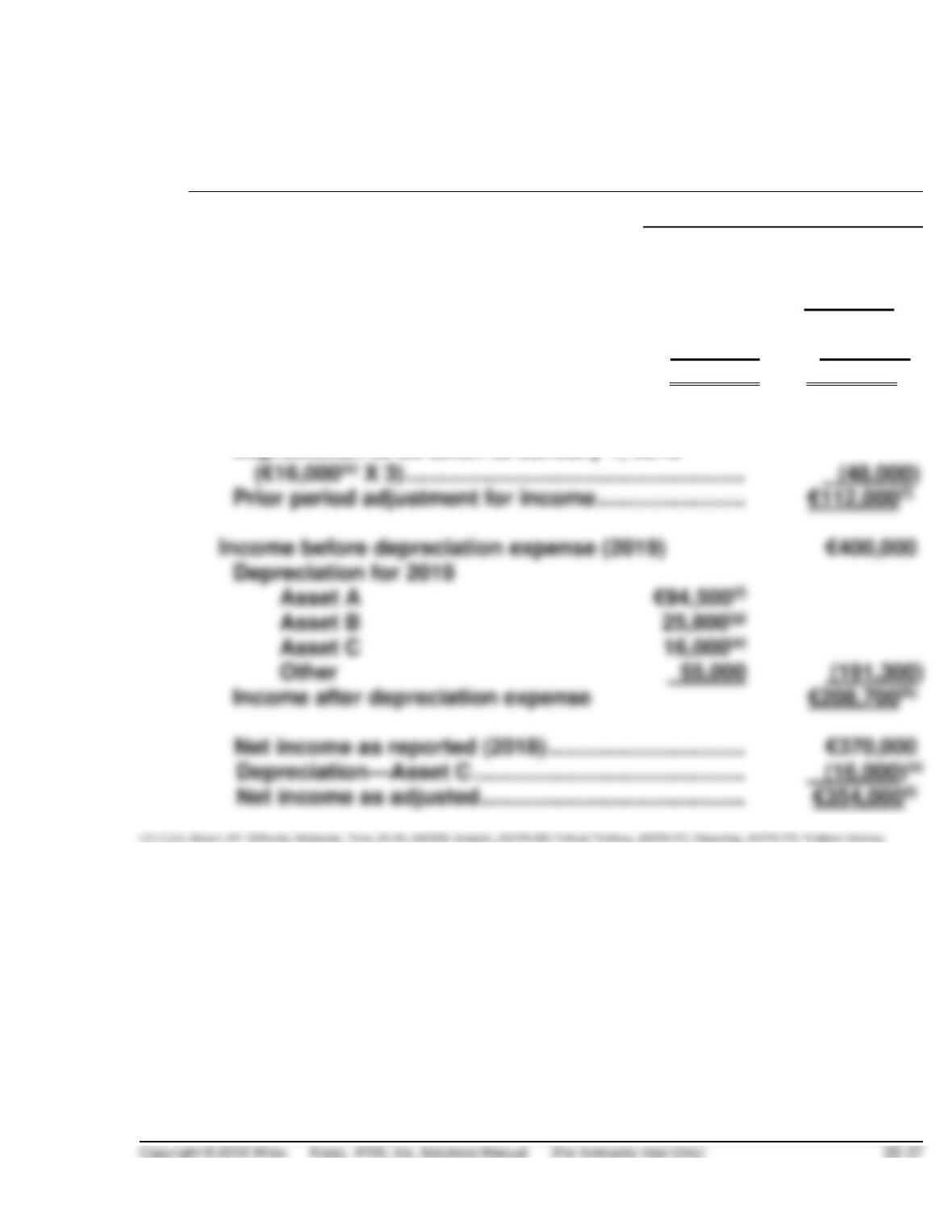

PROBLEM 22.6

(a) 1. Depreciation Expense ………………………………… 94,500(f)

Accumulated Depreciation—Asset A ……. 94,500

Computations:

Cost of Asset A ……………………………………… €540,000

2. Depreciation Expense ………………………………… 25,800(g)

Accumulated Depreciation—Asset B ……. 25,800

Computations:

Original cost ………………………………………. €180,000(c)

Accumulated depreciation (1/1/19)

3. Asset C …………………………………………………….. 160,000(d)

Accumulated Depreciation—Asset C

PROBLEM 22.6 (Continued)

(b) MADRASA SA

Comparative Retained Earnings Statements

For the Years Ended

2019

2018

Retained earnings, January 1, as previously

reported

€200,000

Add: Error in recording Asset C

112,000(f)

Retained earnings, January 1, as adjusted

€666,000

312,000

Add: Net income

208,700(h)

354,000(i)

Retained earnings, December 31

€874,700

€666,000

Amount expensed incorrectly in 2015 ……………….. €160,000(d)

Depreciation to be taken to January 1, 2018

PROBLEM 22.7

(1)

Depreciation Expense …………………………..………………. 3,200

Accumulated Depreciation—Delivery Vehicles … 3,200

(2)

(3)

Cash ……………………………………………………………………. 5,600

Accounts Receivable ……………………………………… 5,600

(4)

(5)

Litigation Loss ……………………………………………………… 125,000

Estimated Litigation Liability ………………………….. 125,000

(6)

(7)

(8)

Depreciation Expense ($40,000 ÷ ……………………….. 8) 5,000