EXERCISE 15.9 (15–20 minutes)

May 2 Cash ……………………………………………………….. 192,000

Share Capital—Ordinary

(12,000 X £10) …………………………..…….. 120,000

Share Premium—Ordinary

(12,000 X £6) …………………………………… 72,000

EXERCISE 15.10 (20–25 minutes)

(a) (1) The par value is HK$2.50. This amount is obtained from either of

the following: 2020—HK$545 ÷ 218 or 2019—HK$540 ÷ 216.

(2) The cost of treasury shares was higher in 2020. The cost at

(b) Equity (in millions of HK$)

Share capital—ordinary, HK$2.50 par value, 500,000,000

EXERCISE 15.11 (15–20 minutes)

Item

Assets

Liabilities

Equity

Share

Premium

Retained

Earnings

Net

Income

1.

I

NE

I

NE

I

I

2.

NE

NE

NE

NE

NE

NE

3.

NE

I

D

NE

D

NE

4.

NE

NE

NE

NE

NE

NE

5.

NE

D

NE

D

6.

NE

NE

NE

NE

7.

NE

I

D

NE

D

8.

NE

NE

NE

NE

D

NE

EXERCISE 15.12 (10–15 minutes)

(a)

6/1

Retained Earnings …………………………..

6,000,000

Dividends Payable …………………………..

6,000,000

6/14

No entry on date of record.

6/30

Dividends Payable …………………………..

6,000,000

Cash ……………………………………………………….

6,000,000

EXERCISE 15.13 (10–15 minutes)

(a) No entry—simply a memorandum note indicating the number of shares

has increased to 10 million and par value has been reduced from

₺10 to ₺5 per share.

EXERCISE 15.13 (Continued)

(c) Share dividends and splits serve the same function with regard to the

EXERCISE 15.14 (10–12 minutes)

(a)

Retained Earnings (10,000 X €10) …………………………..

100,000

Ordinary Share Dividend Distributable …………………

100,000

Ordinary Share Dividend Distributable …………………….

Share Capital—Ordinary …………………………..

100,000

(b)

Retained Earnings (200,000 X €10) …………………………..

Ordinary Share Dividend Distributable …………………

Ordinary Share Dividend Distributable …………………….

Share Capital—Ordinary …………………………..

EXERCISE 15.15 (10–15 minutes)

(a)

Retained Earnings ………………………………………………….

30,000

Ordinary Share Dividend Distributable …………….

30,000

(60,000 shares X 5% X R$10 = R$30,000)

Share Capital—Ordinary…………………………..

30,000

EXERCISE 15.15 (Continued)

(c)

January 5, 2020

Debt Investments (R$125,000 – R$90,000) ………………..

35,000

Unrealized Holding Gain or

Loss—Income ……………………………………………..

Retained Earnings …………………………..……………………..

Property Dividends Payable …………………………..

Property Dividends Payable…………………………..

Debt Investments ……………………………………………

EXERCISE 15.16 (5–10 minutes)

Total income since incorporation ………………………..

W287,000

Less: Total cash dividends paid …………………………

W60,000

Total value of share dividends …………………..

Current balance of retained earnings …………………..

EXERCISE 15.17 (20–25 minutes)

TELLER SE

Partial Statement of Financial Position

December 31, 2019

Equity

Share capital—preference, €4 cumulative,

par value €50 per share; authorized 60,000

shares, issued and outstanding 10,000 shares

€ 500,000

Share capital—ordinary, par value €1 per share;

authorized 600,000 shares, issued 200,000

Share premium—ordinary ……………………………………

Share premium—treasury …………………………………….

Retained earnings ……………………………………………….

Treasury shares, 10,000 shares at cost …………………

EXERCISE 15.18 (30–35 minutes)

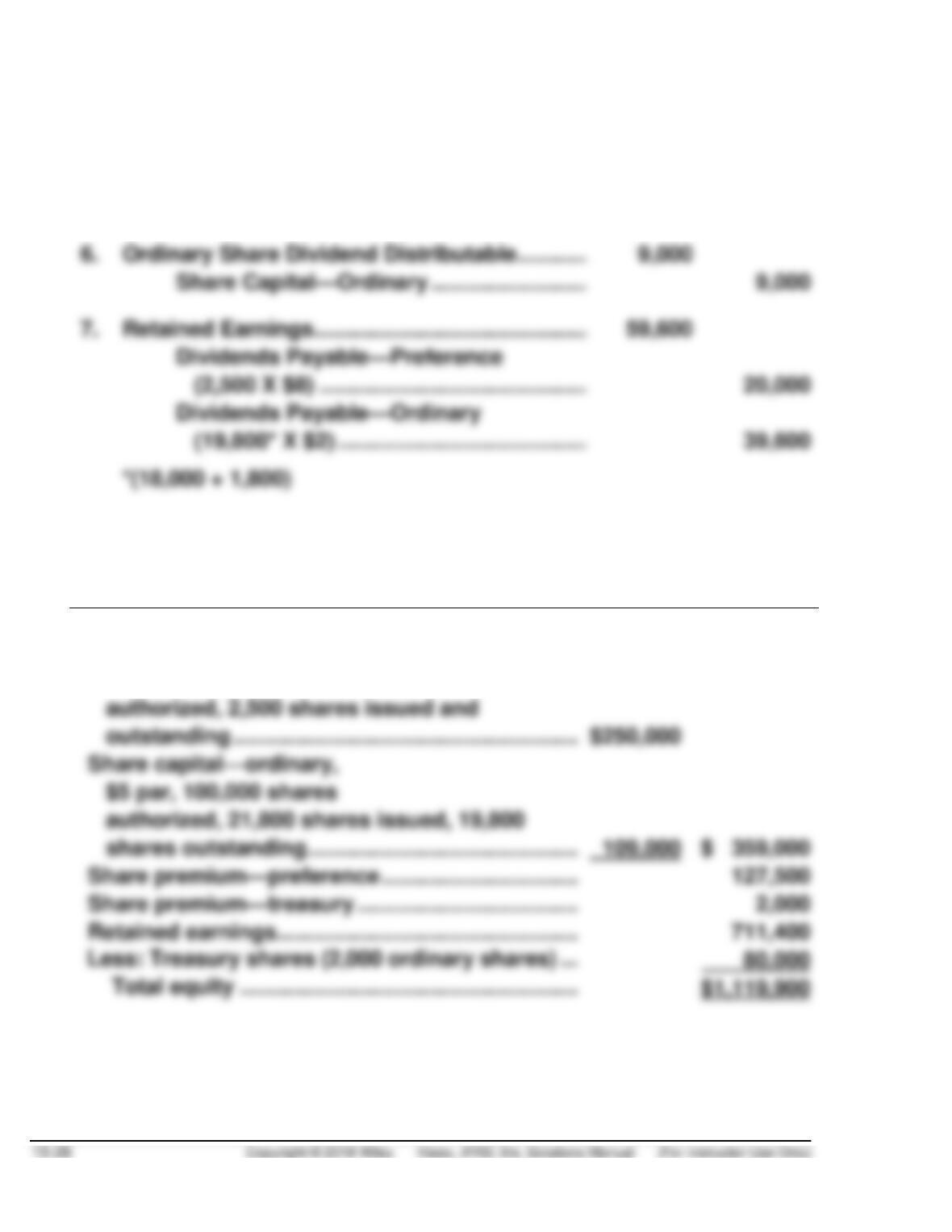

(a)

1.

Dividends Payable—Preference

(2,000 X $8) ……………………………………………………….

16,000

(20,000 X $2) ……………………………………………………….

40,000

30,000

52,500

Share Capital—Preference

Dividends Payable—Ordinary

EXERCISE 15.18 (Continued)

5.

Retained Earnings (1,800* X $5) …………………………..

9,000

Ordinary Share Dividend Distributable

(1,800 X $5) ………………………………………………….

9,000

*(20,000 – 2,700 + 700 = 18,000; 18,000 X 10%)

Ordinary Share Dividend Distributable……………………..

Share Capital—Ordinary …………………………..

9,000

Retained Earnings …………………………………………………..

Dividends Payable—Preference

(2,500 X $8) ………………………………………………….

Dividends Payable—Ordinary

(19,800* X $2) ……………………………………………….

*(18,000 + 1,800)

(b)

ELIZABETH COMPANY

Partial Statement of Financial Position

December 31, 2020

Equity

Share capital—preference,

8%, $100 par, 10,000 shares

authorized, 2,500 shares issued and

outstanding ………………………………………………….

$5 par, 100,000 shares

authorized, 21,800 shares issued, 19,800

shares outstanding ……………………………………….

Share premium—preference …………………………..

Share premium—treasury ………………………………..

Retained earnings ……………………………………………

EXERCISE 15.18 (Continued)

Computations:

Preference shares $200,000 + $50,000 = $250,000

EXERCISE 15.19 (20–25 minutes)

(a) Wilder Ltd. is the more profitable in terms of return on total assets.

This may be shown as follows:

Note to Instructor: These returns are based on net income related to

total assets, where the ending amount of total assets is considered

EXERCISE 15.19 (Continued)

(b) Ingalls plc is the more profitable in terms of return on ordinary share

equity. This may be shown as follows:

Ingalls plc

£648,000

= 24%

£2,700,000

£720,000

Ingalls plc

Funds Supplied

Funds

Supplied

Rate of Return

on Funds at

17.14%*

Cost of

Funds

Accruing to

Ordinary

Shares

Non-current

liabilities

£1,200,000

£205,680

£72,000*

£133,680

The schedule indicates that the income earned on the total assets

(before interest cost) was £719,880. The interest cost (net of tax) of

this income was £72,000, which indicates a net return to the ordinary

share equity of £647,880.

(c) The Ingalls plc earned a net income per share of £6.48 (£648,000 ÷

100,000) while Wilder Ltd. had an income per share of £4.97 (£720,000

EXERCISE 15.19 (Continued)

(d) Yes, from the point of view of net income it is advantageous for the

shareholders of Ingalls plc to have non-current liabilities outstanding.

EXERCISE 15.20 (15-20 minutes)

(a) Rate of return on ordinary share equity:

(b) DeVries Plastics is trading on the equity successfully, since its return

on ordinary share equity is greater than interest paid on bonds.

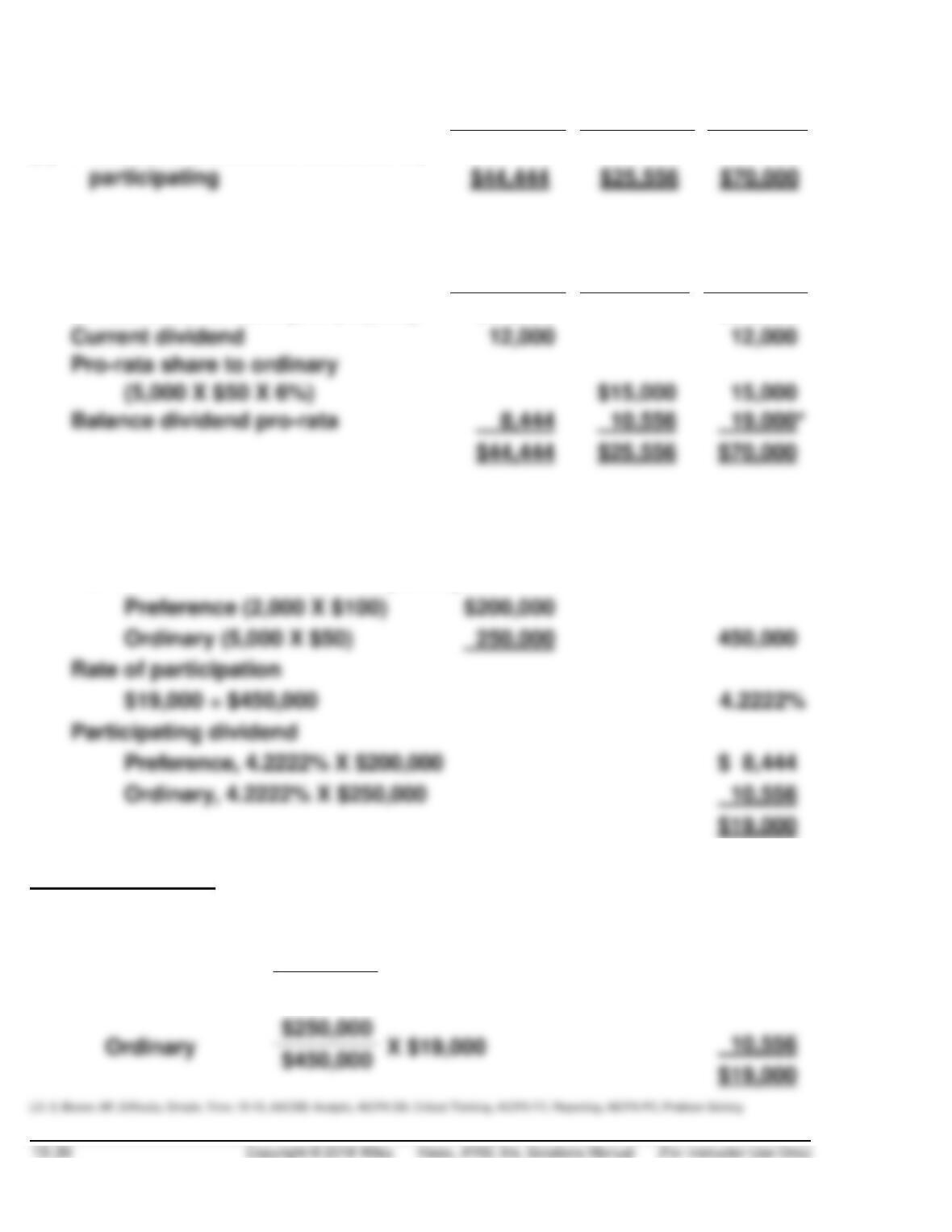

*EXERCISE 15.21 (10–15 minutes)

Preference

Ordinary

Total

(a)

Preference shares are non-cumulative,

(b)

Preference shares are cumulative,

*EXERCISE 15.21 (Continued)

Preference

Ordinary

Total

(c)

Preference shares are cumulative,

participating

The computation for these amounts is as follows:

Preference

Ordinary

Total

Dividends in arrears (2 X $12,000)

$24,000

$24,000

Current dividend

Pro-rata share to ordinary

(5,000 X $50 X 6%)

Balance dividend pro-rata

*Additional amount available for participation

($70,000 – $24,000 – $12,000 – $15,000)

19,000

Par value of shares that are to participate

Preference (2,000 X $100)

Ordinary (5,000 X $50)

Rate of participation

$19,000 ÷ $450,000

Participating dividend

Preference, 4.2222% X $200,000

Ordinary, 4.2222% X $250,000

Note to instructor: Another way to compute the participating amount is as

follows:

Preference

$200,000

X $19,000

$ 8,444

$450,000

$250,000

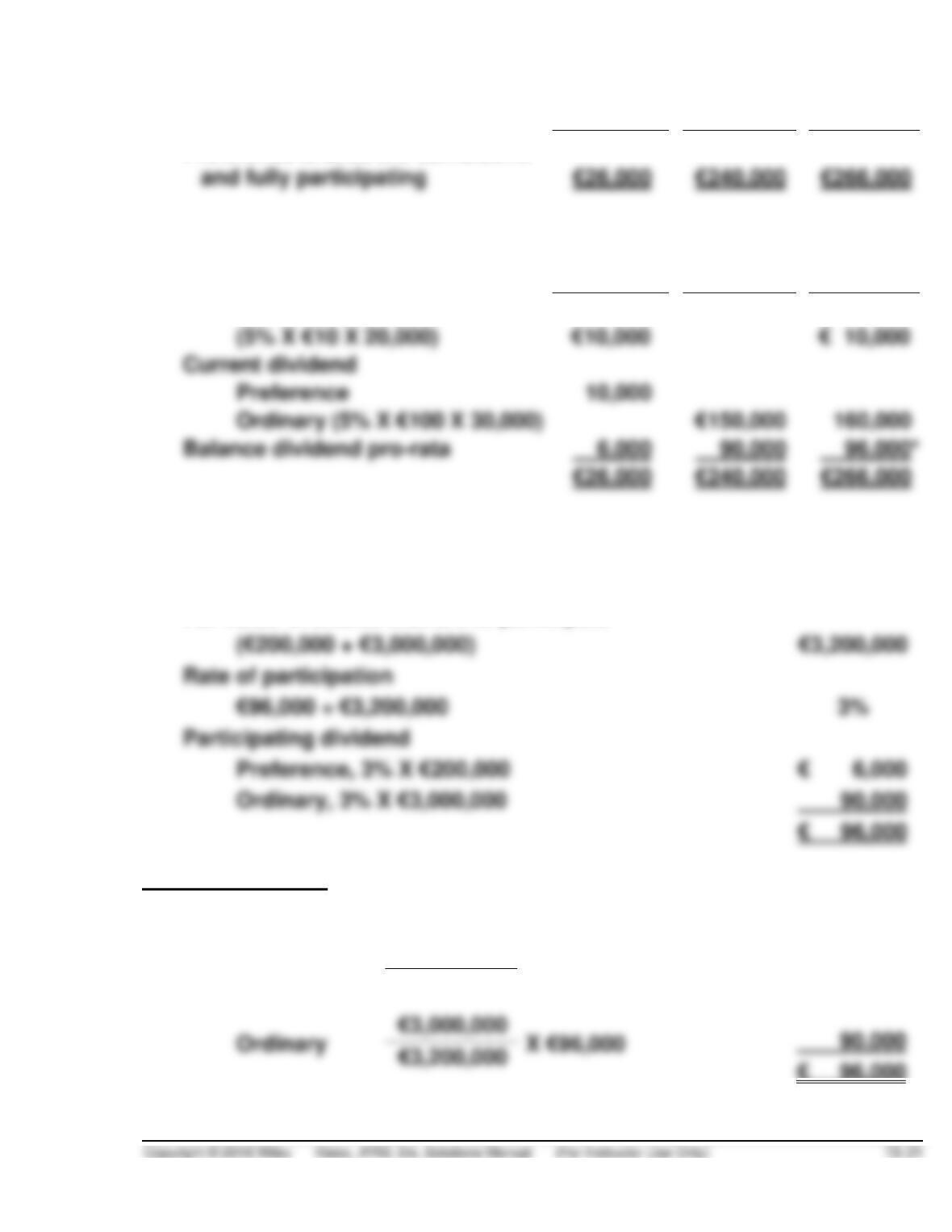

*EXERCISE 15.22 (15–20 minutes)

(a)

Preference

Ordinary

Total

Preference shares are cumulative

and fully participating

The computation for these amounts is as follows:

Preference

Ordinary

Total

(5% X €10 X 20,000)

Current dividend

Preference

Ordinary (5% X €100 X 30,000)

Balance dividend pro-rata

96,000*

Dividends in arrears

*Additional amount available for participation

(€266,000 – €10,000 – €160,000)

€ 96,000

Par value of shares that are to participate

(€200,000 + €3,000,000)

Rate of participation

Participating dividend

Preference, 3% X €200,000

€ 6,000

Ordinary, 3% X €3,000,000

Note to instructor: Another way to compute the participating amount is as

follows:

Preference

€200,000

X €96,000

€ 6,000

€3,200,000

€ 96,000

*EXERCISE 15.22 (Continued)

(b)

Preference

Ordinary

Total

Preference shares are non-cumulative

and non-participating

€10,000

€256,000

€266,000

The computation for these amounts is as follows:

Current dividend (preferred)

(5% X €10 X 20,000)

Remainder to ordinary

(€266,000 – €10,000)

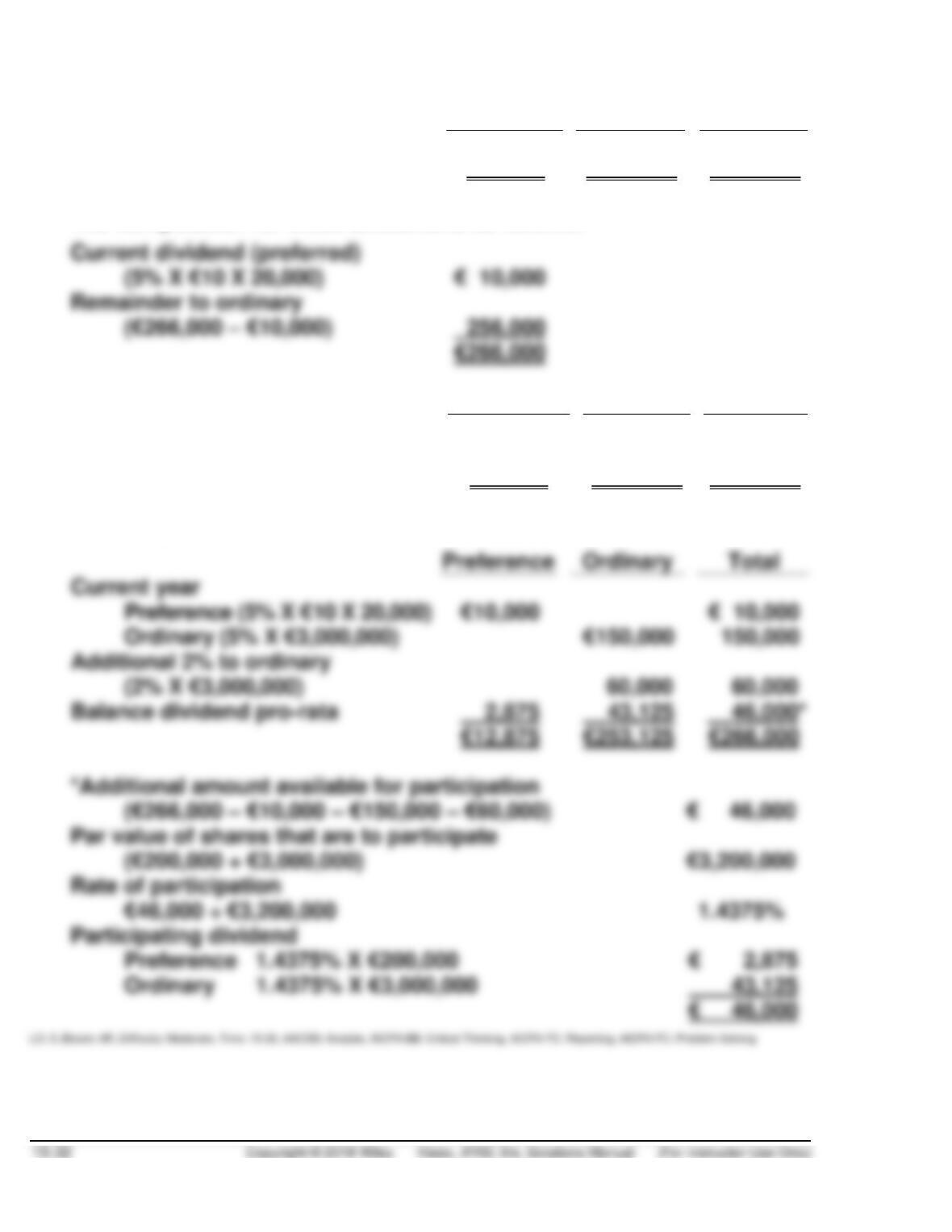

(c)

Preference

Ordinary

Total

Preference shares are non-cumulative

and participating in distributions

in excess of 7%

€12,875

€253,125

€266,000

The computation for these amounts is as follows:

Preference

Current year

Preference (5% X €10 X 20,000)

€10,000

Ordinary (5% X €3,000,000)

Additional 2% to ordinary

Balance dividend pro-rata

*Additional amount available for participation

(€266,000 – €10,000 – €150,000 – €60,000)

Par value of shares that are to participate

(€200,000 + €3,000,000)

Rate of participation

Participating dividend

Preference 1.4375% X €200,000

Ordinary 1.4375% X €3,000,000

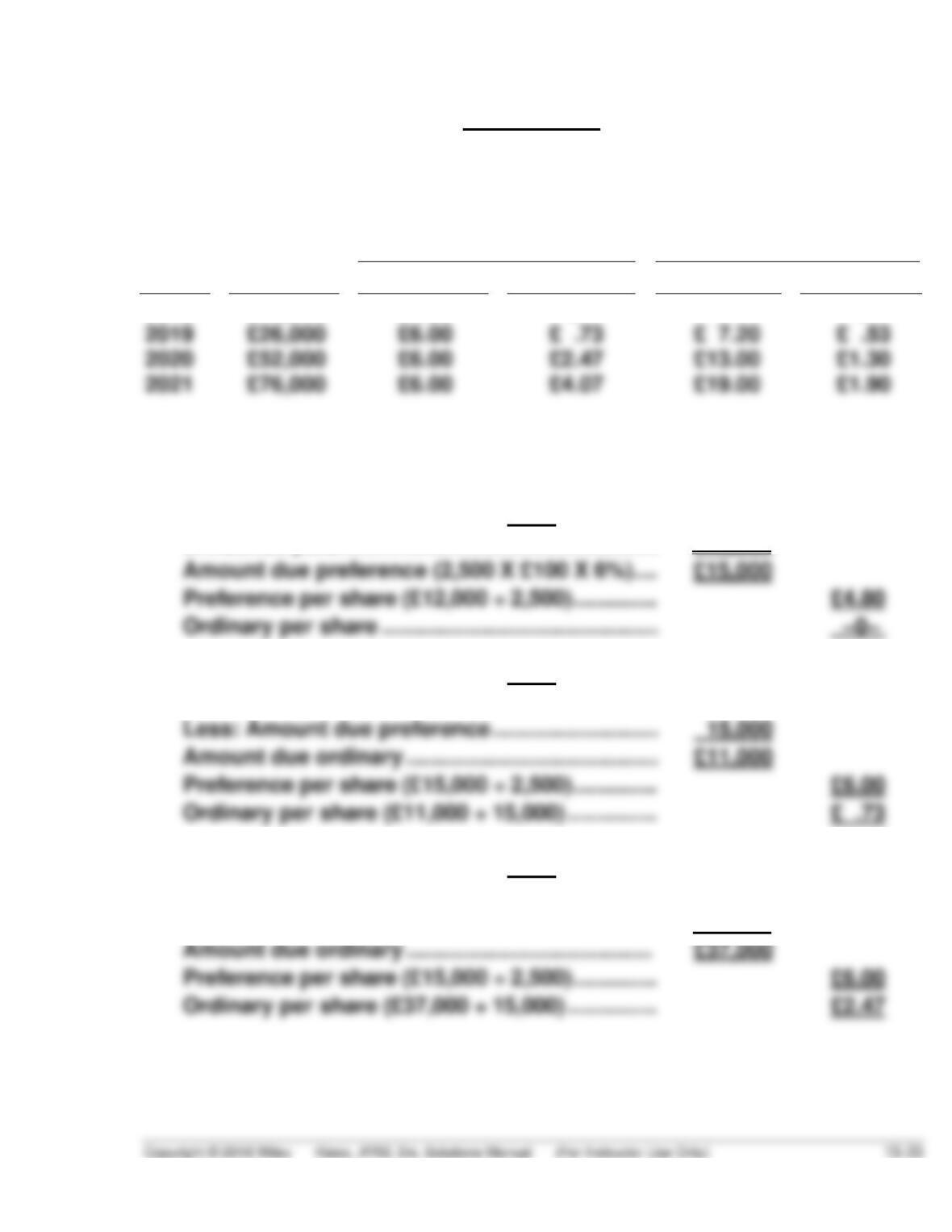

*EXERCISE 15.23 (15–20 minutes)

Assumptions

(a)

(b)

Preference,

non-cumulative, and

non-participating

Preference,

cumulative, and fully

participating

Year

Paid-out

Preference

Ordinary

Preference

Ordinary

2018

£12,000

£4.80

–0–

£ 4.80

–0–

2020

£52,000

£6.00

The computations for part (a) are as follows:

2018

Dividends paid …………………………………………….

£12,000

Amount due preference (2,500 X £100 X 6%) ….

£15,000

Preference per share (£12,000 ÷ 2,500) …………..

Ordinary per share ………………………………………

2019

Dividends paid …………………………………………….

£26,000

Less: Amount due preference ………………………

15,000

Amount due ordinary …………………………………..

£11,000

Preference per share (£15,000 ÷ 2,500) …………..

Ordinary per share (£11,000 ÷ 15,000) ……………

2020

Dividends paid ……………………………………………

£52,000

Less: Amount due preference ……………………..

15,000

Amount due ordinary ………………………………….

£37,000

Preference per share (£15,000 ÷ 2,500) …………..

Ordinary per share (£37,000 ÷ 15,000) ……………

*EXERCISE 15.23 (Continued)

2021

Dividends paid ……………………………………………..

£76,000

Less: Amount due preference ……………………….

Amount due ordinary ……………………………………

£61,000

Preference per share (£15,000 ÷ 2,500)…………….

Ordinary per share (£61,000 ÷ 15,000) ……………..

The computations for part (b) are as follows:

2018

Dividends paid ……………………………………………..

£12,000

Amount due preference (2,500 X £100 X 6%) …..

£15,000

Preference per share (£12,000 ÷ 2,500)…………….

Ordinary per share ……………………………………….

2019

Dividends paid ……………………………………………..

£26,000

Less: Amount due preference

In arrears (£15,000 – £12,000) ………………..

3,000

Current…………………………………………………

£18,000

Amount due ordinary (£26,000 – £18,000) ………

£ 8,000

Preference per share (£18,000 ÷ 2,500)…………….

Ordinary per share (£8,000 ÷ 15,000) ……………….

*EXERCISE 15.23 (Continued)

2020

Dividends paid ………………………………………..

£52,000

Amount due preference

Current (2,500 X £100 X 6%)……………..

£15,000

Amount due ordinary

Current (15,000 X £10 X 6%)……………..

£ 9,000

Amount available for participation

(£52,000 – £15,000 – £9,000)……………..

Par value of shares that are to participate

(£250,000 + £150,000) ………………………

Rate of participation

£28,000 ÷ £400,000 …………………………..

7%

Participating dividend

Preference (7% X £250,000) ……………..

£ 17,500

Ordinary (7% X £150,000) …………………

£ 10,500

Total amount per share—Preference

Current £15,000

Participation 17,500

£32,500 ÷ 2,500

Total amount per share—Ordinary

Current £ 9,000

Participation 10,500

£19,500 ÷ 15,000

*EXERCISE 15.23 (Continued)

2021

Dividends paid ………………………………………..

£76,000

Amount due preference

Current (2,500 X £100 X 6%) ……………..

£15,000

Amount due ordinary

Current (15,000 X £10 X 6%) ……………..

Amount available for participation

(£76,000 – £15,000 – £9,000) ……………..

£ 52,000

Par value that is to participate

(£250,000 + £150,000) ………………………

£400,000

Rate of participation

£52,000 ÷ £400,000 …………………………..

Participating dividend

Preference (13% X £250,000)…………….

£ 32,500

Ordinary (13% X £150,000) ……………….

Total amount per share—Preference

Current £15,000

Participation 32,500

£47,500 ÷ 2,500

Total amount per share—Ordinary

Current £ 9,000

Participation 19,500

£28,500 ÷ 15,000

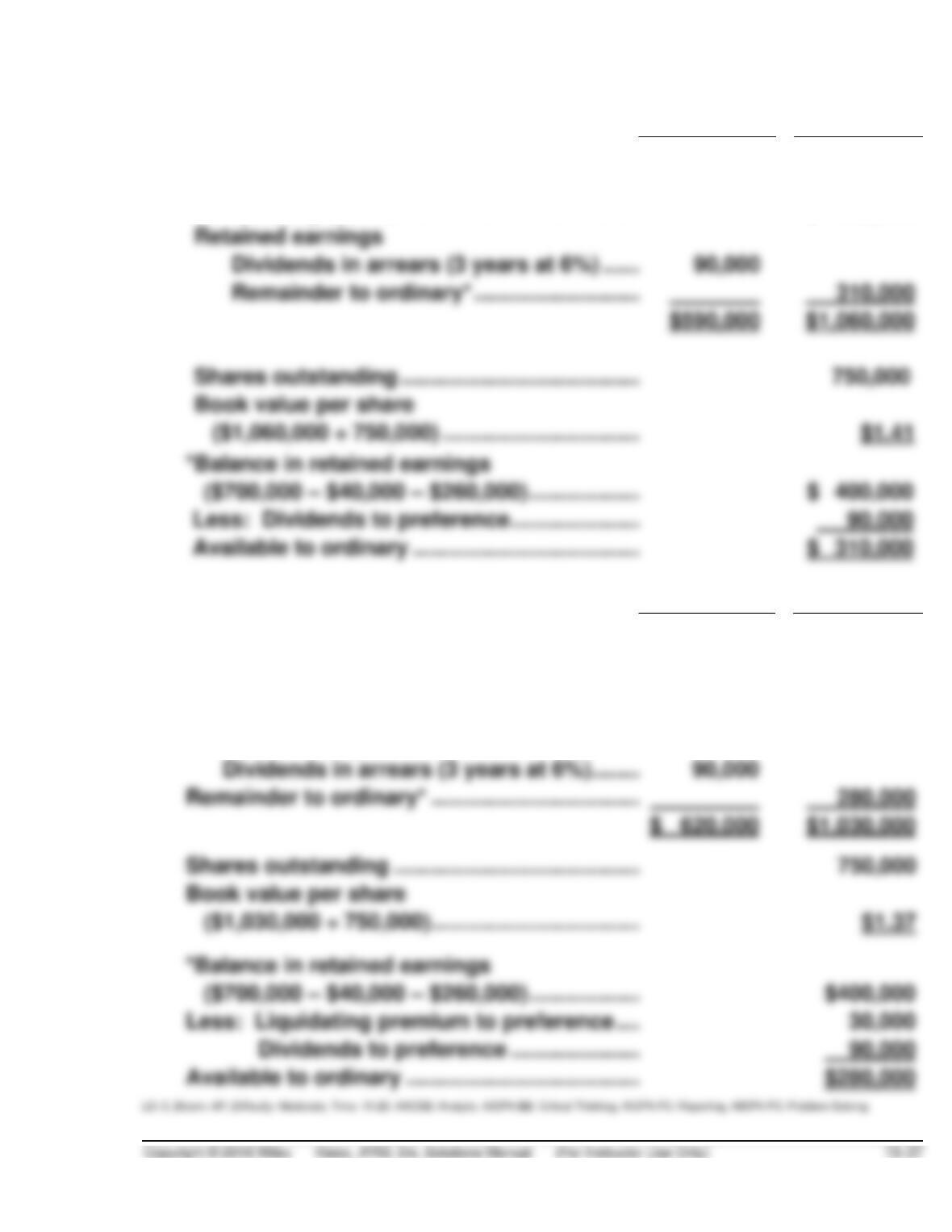

*EXERCISE 15.24 (10–20 minutes)

(a)

Preference

Ordinary

Equity

Preference shares …………………………………

$500,000

Ordinary shares …………………………………….

$ 750,000

Retained earnings

Dividends in arrears (3 years at 6%) ……….

Remainder to ordinary* ………………………….

310,000

Shares outstanding …………………………………….

*Balance in retained earnings

($700,000 – $40,000 – $260,000) ………………..

(b)

Ordinary

Preference

Equity

Preference share …………………………………..

$ 500,000

Liquidating premium …………………………..

30,000

Ordinary shares …………………………………………

$ 750,000

Retained earnings

Dividends in arrears (3 years at 6%) ………..

Remainder to ordinary* ……………………………….

280,000

Shares outstanding …………………………………….

*Balance in retained earnings

($700,000 – $40,000 – $260,000) …………………

Less: Liquidating premium to preference …….

Dividends to preference ……………………

Available to ordinary …………………………………..

TIME AND PURPOSE OF PROBLEMS

Problem 15.1 (Time 50–60 minutes)

Purpose—to provide the student with an understanding of the necessary entries to properly account for

Problem 15.2 (Time 25–35 minutes)

Purpose—to provide the student with an opportunity to record the acquisition of treasury shares and its

sale at three different prices. In addition, an equity section of the statement of financial position must be

prepared.

Problem 15.3 (Time 25–30 minutes)

Purpose—to provide the student with an opportunity to record seven different transactions involving

Problem 15.4 (Time 20–30 minutes)

Purpose—to provide the student with an understanding of the necessary entries to properly account for

Problem 15.5 (Time 30–40 minutes)

Purpose—to provide the student with an understanding of the proper entries to reflect the reacquisition,

Problem 15.6 (Time 30–40 minutes)

Purpose—to provide the student with an understanding of the necessary entries to properly account for

Problem 15.7 (Time 15–20 minutes)

Purpose—to provide the student with an understanding of the proper accounting for the declaration and

Problem 15.8 (Time 20–25 minutes)

Purpose—to provide the student with an understanding of the accounting effects related to share

Problem 15.9 (Time 20–25 minutes)

Purpose—to provide the student with an understanding of the effect which a series of transactions

Time and Purpose of Problems (Continued)

Problem 15.10 (Time 35–45 minutes)

Problem 15.11 (Time 25–35 minutes)

Purpose—to provide the student with an understanding of the proper accounting for the declaration and

Problem 15.12 (Time 35–45 minutes)

Purpose—to provide the student a comprehensive problem involving all facets of the equity section.

SOLUTIONS TO PROBLEMS

PROBLEM 15.1

(a)

January 11

Cash (20,000 X $16) …………………………………………. 320,000

Share Capital—Ordinary (20,000 X $10) ……… 200,000

Share Premium—Ordinary …………………………. 120,000

February 1

July 29

Treasury Shares (1,800 X $17) ………………………….. 30,600

Cash …………………………..……………………………. 30,600