20-61 Copyright © 2018 Wiley Kieso, IFRS, 3/e, Solutions Manual (For Instructor Use Only)

CHEN Group.

Pension Worksheet—2019

General Journal Entries

Memo Record

PROBLEM 20.12 (Continued)

(b) 2019

Pension Expense …………………………………………….. 49,900

(c) Financial Statements—2019

Income Statement

Pension expense ……………………………………….. ¥49,900

Comprehensive Income Statement

20–63 Copyright © 2018 Wiley Kieso, IFRS, 3/e, Solutions Manual (For Instructor Use Only)

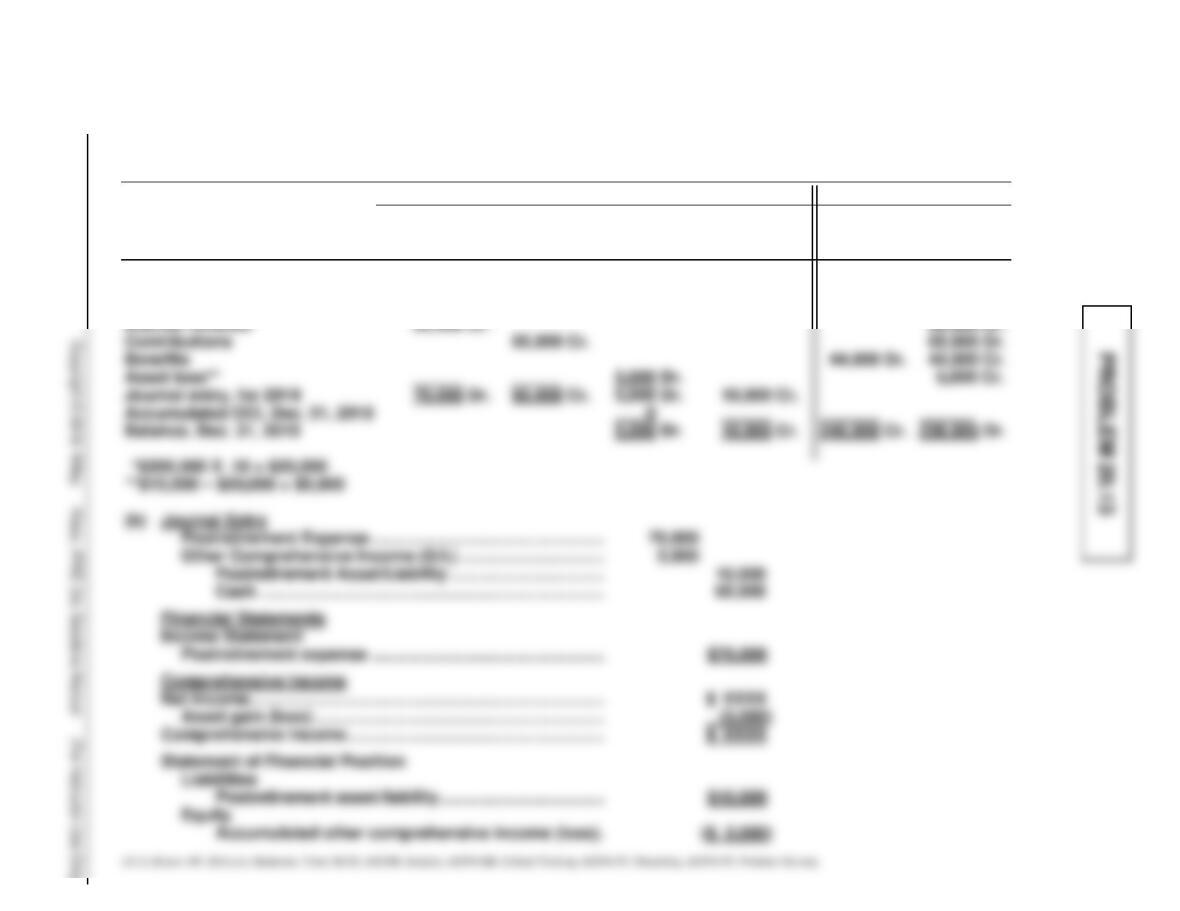

(a) HOLLENBECK FOODS INC.

Postretirement Benefit Worksheet—2019

General Journal Entries

Memo Record

Items

Annual

Postretirement

Expense

Cash

OCI—Gain/

Loss

Postretirement

Asset/Liability

DPBO

Plan Assets

Balance, Jan. 1, 2019

200,000 Cr.

200,000 Dr.

Service cost

70,000 Dr.

70,000 Cr.

Interest expense*

20,000 Dr.

20,000 Cr.

Interest revenue*

20,000 Cr.

20,000 Dr.

Contributions

65,000 Dr.

Benefits

44,000 Dr.

44,000 Cr.

Asset loss**

Journal entry, for 2019

70,000 Dr.

Accumulated OCI, Dec. 31, 2018

Balance, Dec. 31, 2019

246,000 Cr.

236,000 Dr.

PROBLEM 20.14

(a) See worksheet on next page.

(b) December 31, 2019

Postretirement Expense ………………………………. 75,000

(c) See worksheet on next page. The entry is below.

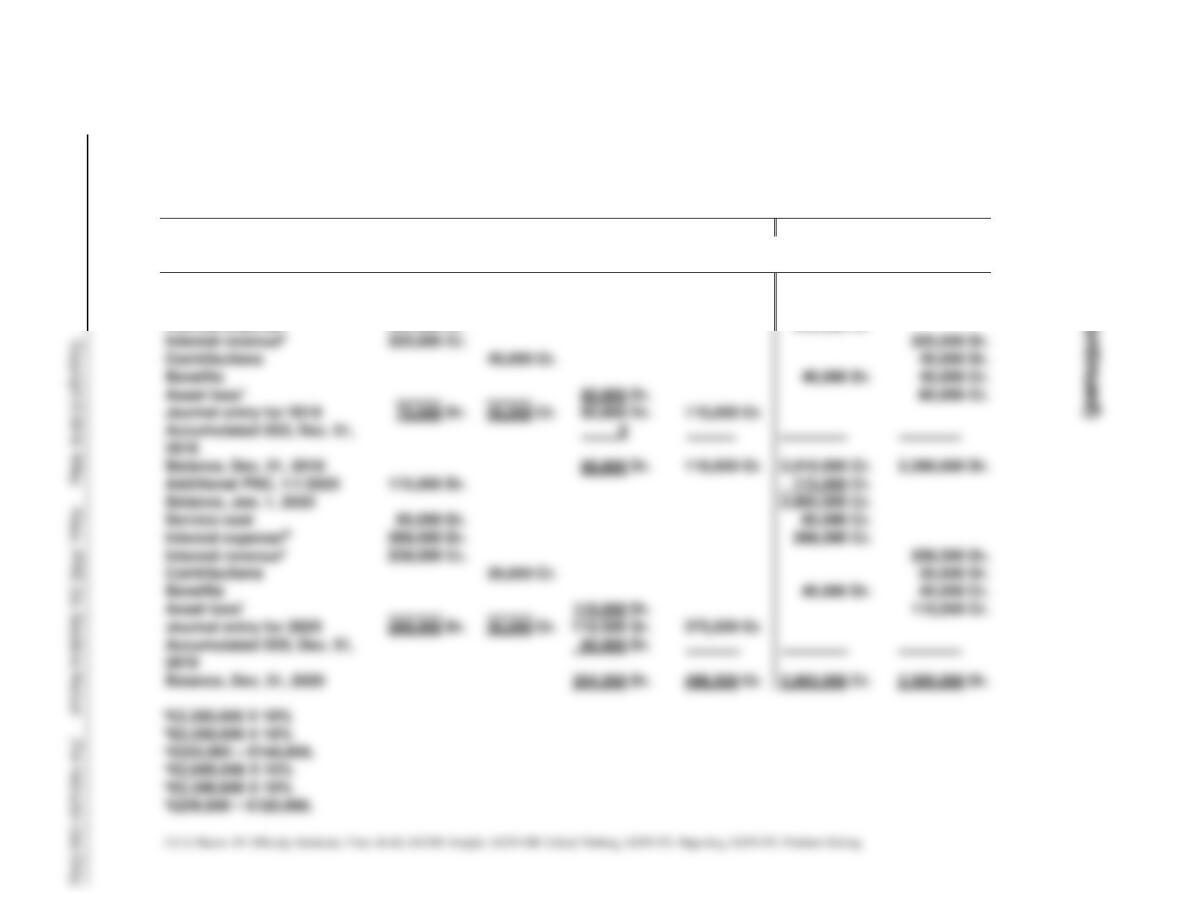

December 31, 2020

Other Comprehensive Income (G/L) ……………… 119,500

Postretirement Expense ………………………………. 289,000

Cash …………………………………………………….. 35,000

Postretirement Asset/Liability………………… 373,500

20–65 Copyright © 2018 Wiley Kieso, IFRS, 3/e, Solutions Manual (For Instructor Use Only)

General Journal Entries

Memo Record

Annual

Expense

Cash

OCI—

Gain/Loss

Postretirement

Asset/Liability

DPBO

Plan

Assets

Balance, Jan. 1, 2019

2,250,000 Cr.

2,250,000 Dr.

Service cost

75,000 Dr.

75,000 Cr.

Interest expensea

225,000 Dr.

225,000 Cr.

PROBLEM 20.14 (Continued)

Interest revenueb

225,000 Cr.

Contributions

45,000 Cr.

Benefits

Asset lossc

Journal entry for 2019

75,000 Dr.

45,000 Cr.

Balance, Dec. 31, 2019

2,510,000 Cr.

2,395,000 Dr.

Additional PSC, 1/1/2020

Balance, Jan. 1, 2020

2,685,000 Cr.

Service cost

85,000 Dr.

268,500 Dr.

268,500 Cr.

Interest revenuee

239,500 Cr.

Contributions

35,000 Cr.

Benefits

Asset lossf

Journal entry for 2020

289,000 Dr.

35,000 Cr.

Balance, Dec. 31, 2020

2,993,500 Cr.

2,505,000 Dr.

TIME AND PURPOSE OF CONCEPTS FOR ANALYSIS

CA 20.1 (Time 30–35 minutes)

Purpose—to provide the student with the opportunity to discuss some of the more traditional issues

CA 20.2 (Time 25–30 minutes)

Purpose—to provide the student with the opportunity to discuss the terminology employed in IAS No.

CA 20.3 (Time 20–25 minutes)

Purpose—to provide the student with the opportunity to discuss the reasons why accrual accounting is

CA 20.4 (Time 30–35 minutes)

Purpose—to provide the student with the opportunity to study some of the implications of IAS No. 19.

The student is required to identify the components of pension expense and how to report gains and

losses.

CA 20.5 (Time 50–60 minutes)

Purpose—to provide the student with the opportunity to discuss the implications of IAS No. 19, given a

CA 20.6 (Time 20–30 minutes)

SOLUTIONS TO CONCEPTS FOR ANALYSIS

CA 20.1

(a) A private pension plan is an arrangement whereby a company undertakes to provide its retired

employees with benefits that can be determined or estimated in advance from the provisions of a

document or from the company’s practices.

(c) 1. Relative to the pension fund the term “funded” refers to the relationship between pension

fund assets and the present value of expected future pension benefit payments; thus, the

pension fund may be fully funded or underfunded. Relative to the employer, the term

“funded” refers to the relationship of the contributions made by the employer to the pension

(d) 1. The theoretical justification for accrual recognition of pension costs is based on the expense

recognition principle. Pension costs are incurred during the period over which an employee

renders services to the enterprise; these costs may be paid upon the employee’s

CA 20.1 (Continued)

(e) Terms and their definitions as they apply to accounting for pension plans follow:

1. Service cost is the actuarial present value of benefits attributed by the pension benefit formula

2. Past service costs are the retroactive benefits granted in a plan amendment (or initiation).

3. Vested benefits are benefits that are not contingent on the employee continuing in the service

of the employer. In some plans, the payment of the benefits will begin only when the

employee reaches the normal retirement date; in other plans the payment of the benefits

CA 20.2

1. Pension asset/liability is the cumulative contributions in excess of accrued net pension expense.

This item is reported in the asset section of the statement of financial position and is reduced

when pension expense is greater than the contribution made to the fund during a period.

2. Pension asset/liability is the cumulative net pension expense accrued in excess of the employer’s

contributions. This item is reported in the liability section of the statement of financial position and

is increased when pension expense is greater than the contribution made to the fund.

CA 20.3

(a) 1. The theoretical justification for accrual recognition of pension costs is based on the expense

recognition principle. Pension costs are incurred during the period over which an employee

renders services to the enterprise; these costs may be paid upon the employee’s

(b) Terms and their definitions as they apply to accounting for pensions follow:

1. Fair value of pension assets, when based on a calculated value of pension plan asset

values over a period of time. Considerable flexibility is permitted in computing this amount.

(c) The following disclosures about a company’s pension plans should be made in financial

statements or their notes (see Illustration 20.25)

Amounts reported in the financial statements

Companies should provide reconciliation from the beginning balance to the ending balance for

each of the following:

1. Plan assets.

This reconciliation should report the following, where appropriate.

• Current service cost.

CA 20.3 (Continued)

Information on how the defined benefit plan may affect the amount, timing, and

uncertainty of future cash flows

(1) Sensitivity analysis for each significant actuarial assumption, showing how the defined

benefit obligation would have been affected by changes in the relevant actuarial assumption

that were reasonably possible at the reporting date.

(2) Methods and assumptions used in preparing the sensitivity analyses required by (1) and the

limitations of those methods.

CA 20.4

(a) Pension benefits are part of the compensation received by employees for their services. The

actual payment of these benefits is deferred until after retirement. The pension expense

measures this compensation and consists of the following two elements:

1. The service cost component is the present value of the benefits earned by the employees

(b) The major similarity between the vested benefit obligation and the defined benefit obligation is

(c) (1) Pension gains and losses, sometimes called remeasurements, result from changes in the

value of the defined benefit obligation or the fair value of the plan assets. These changes

arise from the deviations between the estimated conditions and the actual experience, and

from changes in assumptions. The volatility of these gains and losses may reflect an

CA 20.5

1. This situation can exist because companies vary as to whether they are using an implicit or ex–

plicit set of assumptions when interest rates are disclosed. In the implicit approach, two or more

assumptions do not individually represent the best estimate of the plan’s future experience with

2. This situation will occur because of the pension liability required to be reported. That is, companies

are required to report as a liability the excess of their defined benefit obligation over the fair value

of plan assets. In the past, the basic liability companies reported was the excess of the amount

expensed over the amount funded.

3. This statement is questionable. If a financial measure purports to represent a phenomenon that is

volatile, the measure should show that volatility or it will not be representationally faithful. Never-

theless, many argue that volatility is inappropriate when dealing with such long-term measures as

4. These gross pension plan assets are not reported on the employer’s books. However, the fair

value of plan assets are required to be reported in the footnote, so that a reader of the financial

statements can determine the funded status of the plan.

5. (a) In a defined contribution plan, the amount contributed is the amount expensed. No significant

reporting problems exist here. On the other hand, defined benefit plans involve many difficult

reporting issues which may lead to additional expense and liability recognition.

Significant amendments will generally increase past service cost which are included in