CHAPTER 15

Equity

ASSIGNMENT CLASSIFICATION TABLE (BY TOPIC)

Topics

Questions

Brief

Exercises

Exercises

Problems

Concepts

for Analysis

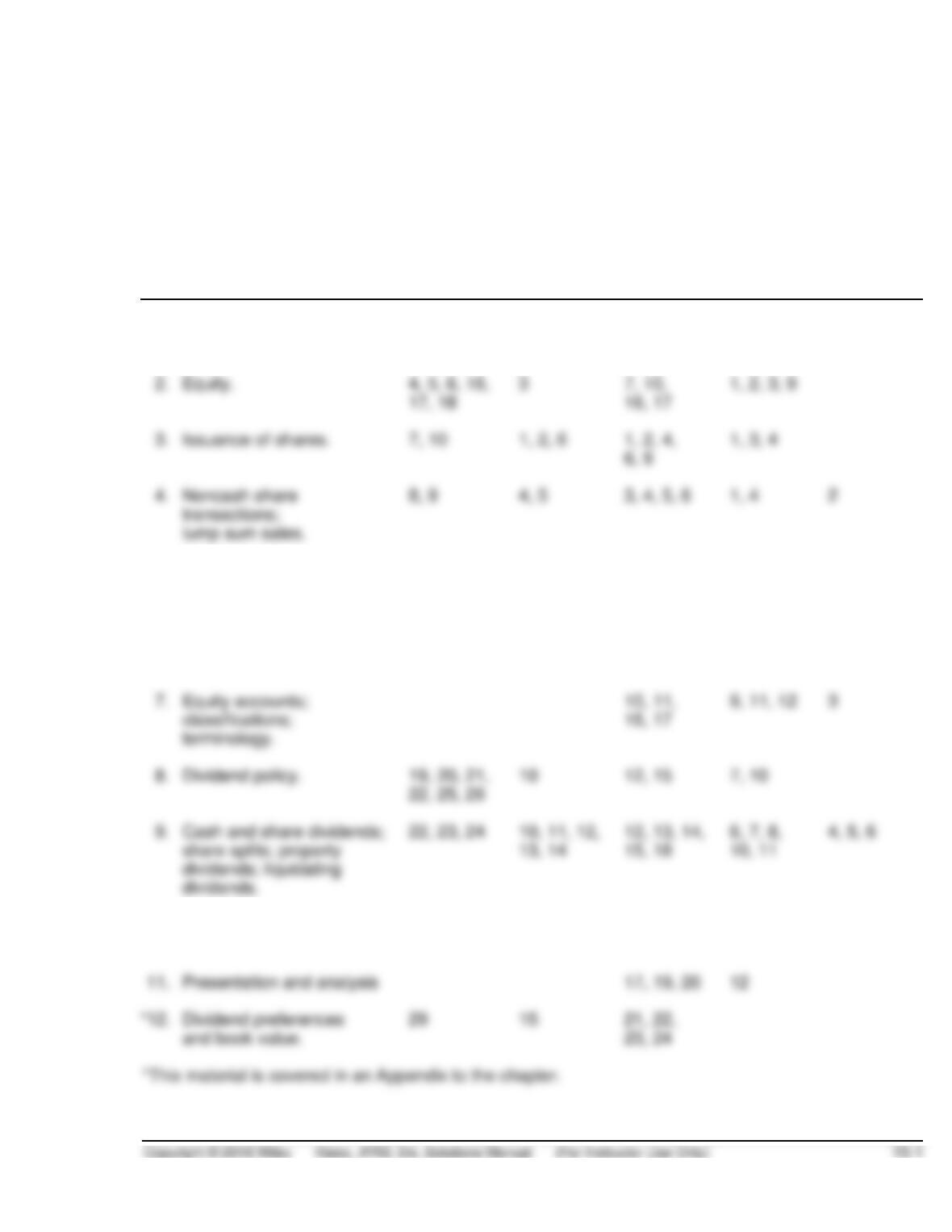

1. Shareholders’ rights;

corporate form.

1, 2, 3

1

2. Equity.

4, 5, 6, 16,

17, 18

3

7, 10,

16, 17

1, 2, 3, 9

3. Issuance of shares.

7, 10

1, 2, 6

1, 2, 4,

6, 9

1, 3, 4

4. Noncash share

transactions;

lump sum sales.

8, 9

4, 5

3, 4, 5, 6

1, 4

2

5. Treasury share

transactions,

cost method.

11, 12, 17

7, 8

3, 6, 7, 9,

10, 18

1, 2, 3,

5, 6, 7

7

6. Preference stock.

3, 13,

14, 15

9

2, 8

1, 3

7. Equity accounts;

classifications;

terminology.

10, 11,

16, 17

9, 11, 12

3

8. Dividend policy.

19, 20, 21,

22, 25, 26

12, 15

7, 10

dividends; liquidating

dividends.

13, 14

15, 18

10, 11

10. Restrictions of retained

earnings.

27, 28

9

17, 19, 20

and book value.

21, 22,

23, 24

ASSIGNMENT CLASSIFICATION TABLE (BY LEARNING OBJECTIVE)

Learning Objectives

Brief

Exercises

Exercises

Problems

Concepts

for Analysis

1. Describe the corporate form and

the issuance of shares.

1, 2, 4, 5, 6,

9

1, 2, 3, 4, 5,

6, 8, 9, 10

1, 3, 4, 9, 12

1, 2, 3

2. Describe the accounting and

reporting for treasury shares.

3, 7, 8

6, 7, 9, 10, 18

1, 2, 3, 5,

6, 7, 9, 12

3, 7

4. Indicate how to present and

analyze equity.

3

17, 19, 20

1, 2, 6, 9, 11,

12

*5. Explain the different types of

15

8, 21, 22,

ASSIGNMENT CHARACTERISTICS TABLE

Item

Description

Level of

Difficulty

Time

(minutes)

E15.1

Recording the issuances of ordinary shares.

Simple

15–20

E15.2

Recording the issuance of ordinary and preference shares.

Simple

15–20

E15.3

Shares issued for land.

Simple

10–15

E15.4

Lump-sum sale of shares with bonds.

Moderate

20–25

E15.5

Lump-sum sales of ordinary and preference shares.

Simple

10–15

E15.6

Share issuances and repurchase.

Moderate

25–30

E15.7

Effect of treasury share transactions on financials.

Moderate

15–20

E15.8

Preference share entries and dividends.

Moderate

15–20

E15.9

Correcting entries for equity transactions.

Moderate

15–20

E15.10

Analysis of equity data and equity section preparation.

Moderate

20–25

E15.11

Equity items on the statement of financial position.

Simple

15–20

E15.12

Cash dividend and liquidating dividend.

Simple

10–15

E15.13

Share split and share dividend.

Simple

10–15

E15.14

Entries for share dividends and share splits.

Simple

10–12

E15.15

Dividend entries.

Simple

10–15

E15.16

Computation of retained earnings.

Simple

05–10

E15.17

Equity section.

Moderate

20–25

E15.18

Dividends and equity section.

Moderate

30–35

E15.19

Comparison of alternative forms of financing.

20–25

E15.20

Trading on the equity analysis.

Moderate

15–20

Preference dividends.

Simple

10–15

Preference dividends.

Moderate

15–20

Preference share dividends.

15–20

Computation of book value per share.

Moderate

10–20

P15.1

Equity transactions and statement preparation.

Moderate

50–60

P15.2

Treasury share transactions and presentation.

Simple

25–35

P15.3

Equity transactions and statement preparation.

Moderate

25–30

P15.4

Share transactions—lump sum.

Moderate

20–30

P15.5

Treasury shares—cost method.

Moderate

30–40

P15.6

Treasury shares—cost method—equity section preparation.

Moderate

30–40

P15.7

Cash dividend entries.

Moderate

15–20

P15.8

Dividends and splits.

Moderate

20–25

P15.9

Equity section of statement of financial position.

Simple

20–25

P15.10

Share dividends and share split.

Moderate

35–45

P15.11

Share and cash dividends.

Simple

25–35

P15.12

Analysis and classification of equity transactions.

35–45

CA15.1

Preemptive rights and dilution of ownership.

Moderate

10–20

CA15.2

Issuance of shares for land.

Moderate

15–20

CA15.3

Conceptual issues—equity.

Moderate

25–30

CA15.4

Share dividends and splits.

Simple

25–30

CA15.5

Share dividends.

Simple

15–20

CA15.6

Share dividend, cash dividend, and treasury shares.

Moderate

20–25

CA15.7

Treasury shares.

Moderate

10–15

*This material is presented in an appendix to the chapter.

ANSWERS TO QUESTIONS

1. The basic rights of each shareholder (unless otherwise restricted) are to share proportionately:

2. The preemptive right protects existing shareholders from dilution of their ownership share in the

event the corporation issues new shares.

LO: 1, Bloom: K, Difficulty: Simple, Time: 3-5, AACSB: None, AICPA BB: None, AICPA FC: Reporting, AICPA PC: Communication

3. Preference shares commonly have preference to dividends in the form of a fixed dividend rate

and a preference over ordinary shares to remaining corporate assets in the event of liquidation.

4. The distinction between contributed (paid-in) capital and retained earnings is important for both

legal and economic points of view. Legally, dividends can be declared out of retained earnings in

5. Authorized ordinary shares—the total number of shares authorized for issuance by the country of

incorporation.

6. Par value is an arbitrary, fixed per share amount assigned to a share by the incorporators. It is

7. The issuance for cash of no-par value ordinary shares at a price in excess of the stated value of

the ordinary shares is accounted for as follows:

(1) Cash is debited for the proceeds from the issuance of the ordinary shares.

Questions Chapter 15 (Continued)

8. The proportional method is used to allocate the lump sum received on sales of two or more

classes of securities when the fair value or other sound basis for determining relative value is

9. The general rule to be applied when shares are issued for services or property other than cash is

that companies should record the shares issued at the fair value of the goods or services

received, unless that fair value cannot be measured reliably. If the fair value of the goods or

10. The direct costs of issuing shares, such as underwriting costs, accounting and legal fees, printing

11. The major reasons for purchasing its own shares are: (1) to provide tax-efficient distributions of

excess cash to shareholders, (2) to increase earnings per share and return on equity, (3) to provide

12. (a) Treasury shares should not be classified as an asset since a corporation cannot own itself.

(b) The “gain” or “loss” on sale of treasury shares should not be treated as additions to or

deductions from income. If treasury shares are carried in the accounts at cost, these so–

called gains or losses arise when the treasury shares are sold. These “gains” or “losses”

13. The character of preference shares can be altered by being cumulative or non-cumulative, partici-

pating (fully or partially) or non-participating, convertible or non-convertible, and/or callable or

Questions Chapter 15 (Continued)

14. Nonparticipating means the security holder is entitled to no more than the specified fixed dividend.

If the security is partially participating, it means that in addition to the specified fixed dividend the

security may participate with the ordinary shares in dividends up to a certain stated rate or

15. Preference shares are generally reported at par value as the first item in the equity section of a

16. Elements of equity include (1) share capital, (2) share premium, (3) retained earnings,

17. When treasury shares are purchased, the Treasury Shares account is debited and Cash is

credited at cost (€290,000 in this case). Treasury Shares is a contra equity account and Cash is

18. The answers are summarized in the table below:

Account Classification

(a) Share Capital—Ordinary Share capital

19. The dividend policy of a company is influenced by (1) the availability of cash, (2) the stability of

Questions Chapter 15 (Continued)

20. In declaring a dividend, the board of directors must consider the condition of the corporation such

that a dividend is (1) legally permissible and (2) economically sound.

In general, directors should give consideration to the following factors in determining the legality

of a dividend declaration:

(1) Retained earnings, unless legally encumbered in some manner, is usually the correct basis

for dividend distribution.

21. Cash dividends are paid out of cash. A balance must exist in retained earnings to permit a legal

22. A cash dividend is a distribution in cash while a property dividend is a distribution in assets

other than cash. Any dividend not based on retained earnings is a liquidating dividend. A

23. A share dividend results in the transfer from retained earnings to share capital equal to the par

24. (a) A share split differs from a share dividend in the amount of retained earnings to be

capitalized. A share dividend involves capitalizing (charging) retained earnings equal to the

par value of the shares distributed.

Another distinction between a share dividend and a share split is that a share dividend

Questions Chapter 15 (Continued)

(b) A declared but unissued share dividend should be classified as part of equity rather than as a

liability in a statement of financial position. A share dividend affects only equity accounts; that is,

25. A partially liquidating dividend will be debited both to Retained Earnings and Share Premium.

The portion of dividends that is a return of capital should be debited to Share Premium.

LO: 3, Bloom: C, Difficulty: Simple, Time: 3-5, AACSB: None, AICPA BB: None, AICPA FC: Reporting, AICPA PC: Communication

26. A property dividend is a nonreciprocal transfer of nonmonetary assets between an enterprise and

its owners. A transfer of a nonmonetary asset to a shareholder or to another entity in a

27. Retained earnings are restricted because of legal or contractual restrictions, or the necessity to

protect the working capital position.

LO: 4, Bloom: C, Difficulty: Simple, Time: 3-5, AACSB: None, AICPA BB: None, AICPA FC: Reporting, AICPA PC: Communication

28. Restrictions of retained earnings are best disclosed in a note to the financial statements. This

Questions Chapter 15 (Continued)

*29.

Preference

Ordinary

Total

(a)

Current year’s dividend, 7%

$ 7,000

$21,000a

$28,000

Participating dividend of 9%

9,000

36,000

Totals

$16,000

$64,000

The participating dividend was determined as follows:

Current year’s dividend:

(b)

Preference

Ordinary

Total

Dividends in arrears, 7% of $100,000

$ 7,000

$ 7,000

Current year’s dividend, 7%

7,000

$21,000

28,000

7,250

Totals

$21,250

$42,750

$64,000

(c)

Preference

Ordinary

Total

Dividends in arrears ($100,000 X 7%) – $5,000

$2,000

$ 2,000

7,000

Remainder to common

$21,000

Totals

$9,000

$21,000

$30,000

SOLUTIONS TO BRIEF EXERCISES

BRIEF EXERCISE 15.1

Cash ………………………………………………………………………. 4,500

BRIEF EXERCISE 15.2

(a) Cash ………………………………………………………………… 8,200

Share Capital—Ordinary …………………………….. 8,200

BRIEF EXERCISE 15.3

WILCO SE

Equity

December 31, 2019

Share capital—ordinary, €5 par value ……………………….. € 510,000

Share premium—ordinary ………………………………………… 1,320,000

BRIEF EXERCISE 15.4

Cash ………………………………………………………………………. 13,500

Share Capital—Preference (100 X $50)……………….. 5,000

BRIEF EXERCISE 15.4 (Continued)

Allocated to ordinary

$6,000

$15,000

X $13,500 = $ 5,400

$9,000

$15,000

BRIEF EXERCISE 15.5

Land ………………………………………………………………………. 31,000

BRIEF EXERCISE 15.6

Cash ($60,000 – $1,500) ……………………………………………. 58,500

BRIEF EXERCISE 15.7

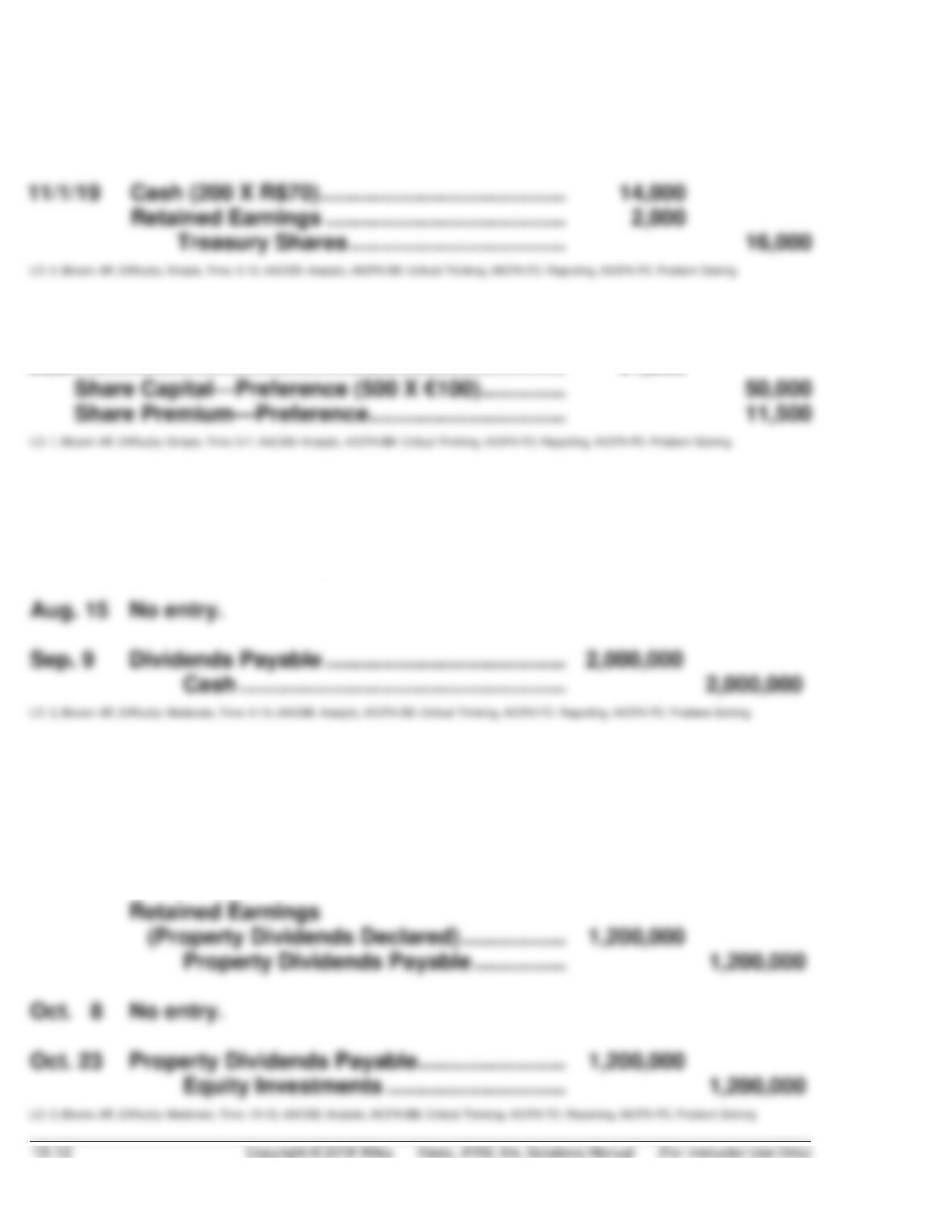

7/1/19 Treasury Shares (100 X €87) ………………………. 8,700

Cash ………………………………………………….. 8,700

BRIEF EXERCISE 15.8

8/1/19 Treasury Shares (200 X R$80) ………………… 16,000

Cash ……………………………………………… 16,000

BRIEF EXERCISE 15.9

Cash …………………………………………………………………… 61,500

BRIEF EXERCISE 15.10

Aug. 1

Retained Earnings (2,000,000 X $1) ………………………….

2,000,000

Dividends Payable…………………………..

2,000,000

Aug. 15

No entry.

Sep. 9

Dividends Payable ………………………………………………….

Cash ……………………………………………………….

2,000,000

BRIEF EXERCISE 15.11

Sep. 21

Equity Investments …………………………………………………

325,000

Unrealized Holding Gain or Loss—

Income (R$1,200,000 – R$875,000)…………………..

325,000

Property Dividends Payable …………………………..

Oct. 8

No entry.

Oct. 23

Property Dividends Payable …………………………..

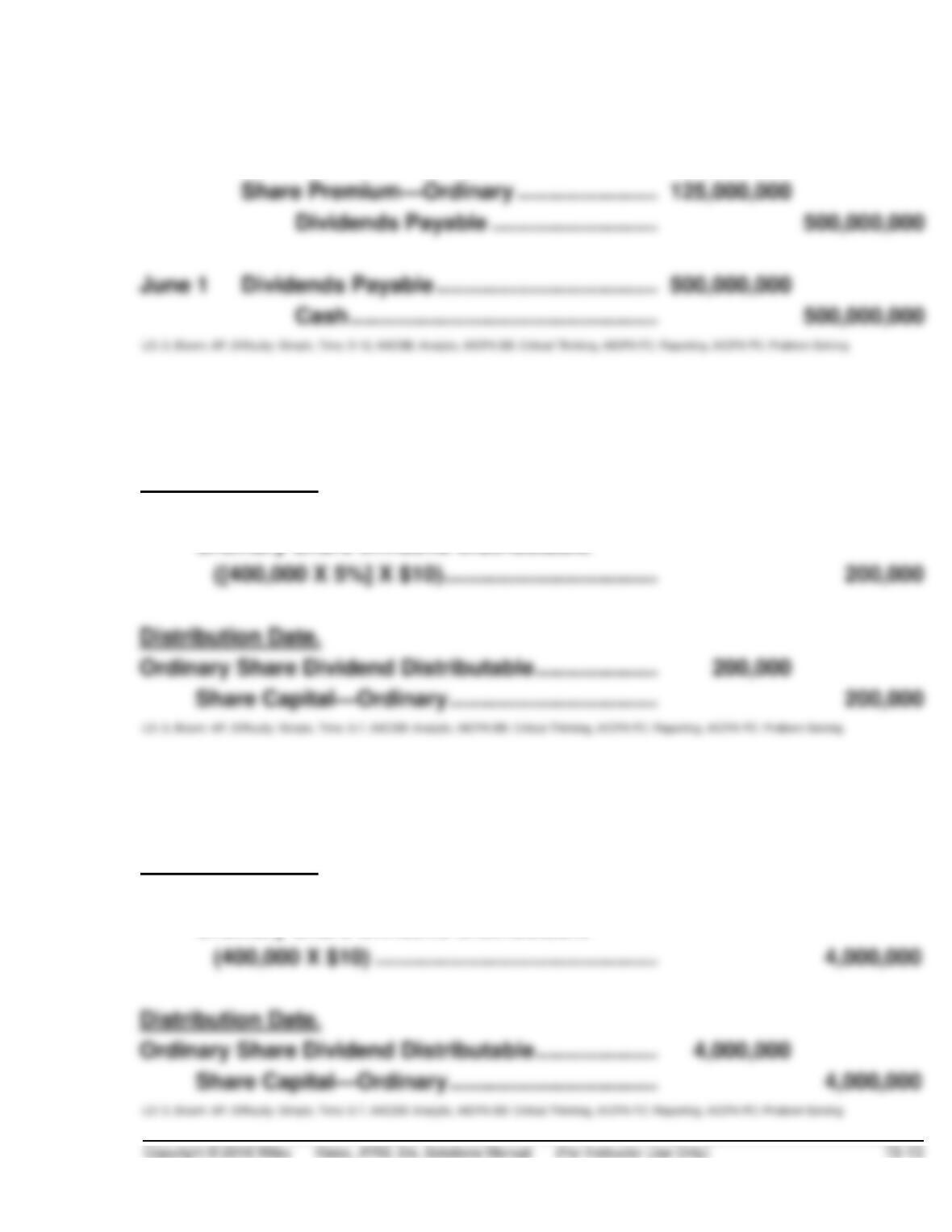

BRIEF EXERCISE 15.12

Apr. 20

Retained Earnings

(¥500,000,000 – ¥125,000,000) …………………………..

375,000,000

June 1

BRIEF EXERCISE 15.13

Declaration Date.

Retained Earnings …………………………………………………..

200,000

Ordinary Share Dividend Distributable

([400,000 X 5%] X $10) …………………………………..

Distribution Date.

Ordinary Share Dividend Distributable ……………………..

Share Capital—Ordinary ………………………………….

BRIEF EXERCISE 15.14

Declaration Date.

Retained Earnings …………………………………………………..

4,000,000

Ordinary Share Dividend Distributable

(400,000 X $10) …………………………………………….

Distribution Date.

Ordinary Share Dividend Distributable ……………………..

*BRIEF EXERCISE 15.15

(a) Preference shareholders would receive €60,000 (6% X €1,000,000) and

the remainder of €240,000 (€300,000 – €60,000) would be distributed to

SOLUTIONS TO EXERCISES

EXERCISE 15.1 (15–20 minutes)

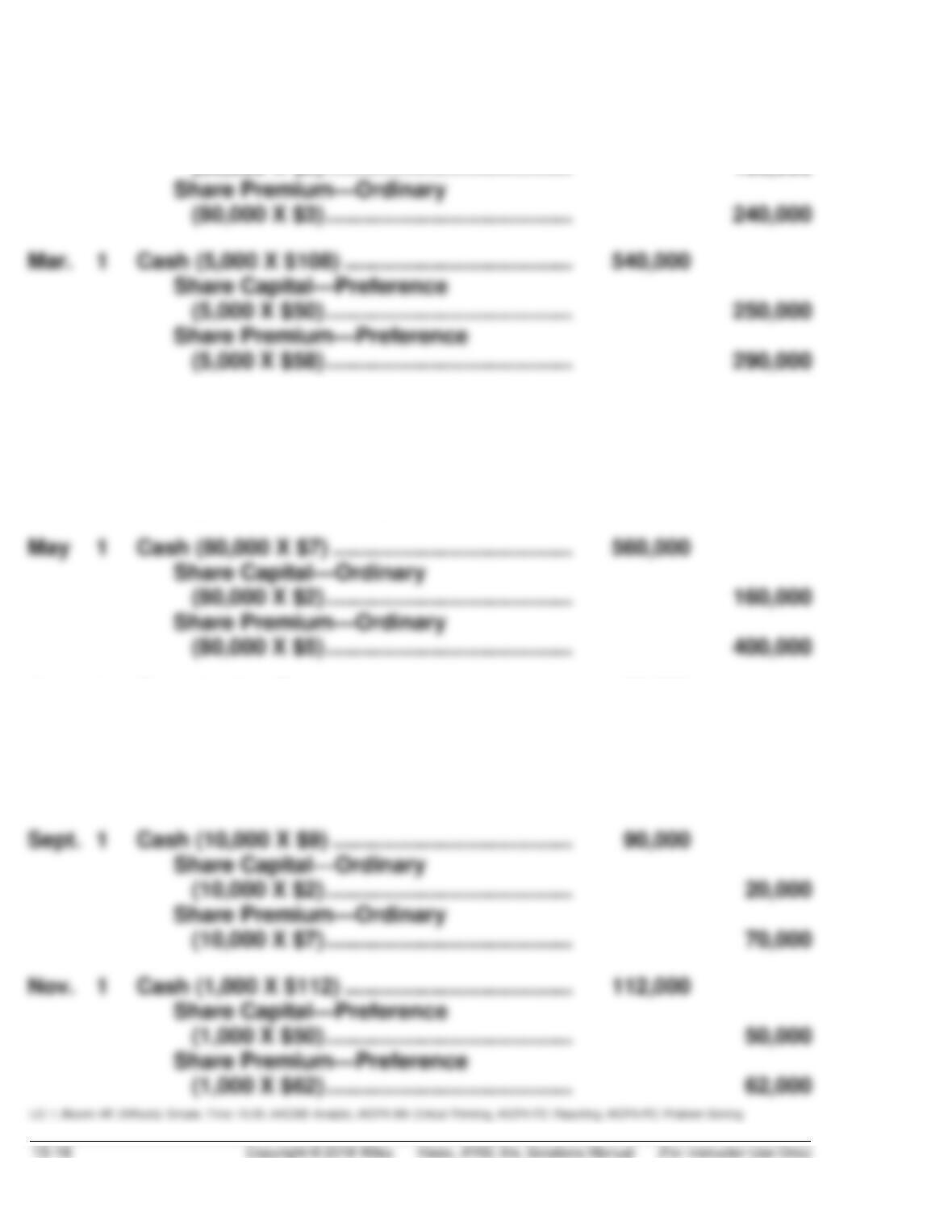

(a) Jan. 10 Cash (80,000 X €6) ………………………….. 480,000

Share Capital—Ordinary

July 1 Cash (30,000 X €8) ………………………….. 240,000

Share Capital—Ordinary

(30,000 X €3) …………………………... 90,000

Share Premium—Ordinary

(30,000 X €5) ………………………….. 150,000

(b) If the shares have a stated value of €2 per share, the entries in (a) would

be the same except for the euro amounts. For example, the Jan. 10

EXERCISE 15.2 (15–20 minutes)

Jan. 10 Cash (80,000 X $5) ………………………………… 400,000

Share Capital—Ordinary

(80,000 X $2) …………………………………. 160,000

April 1 Land …………………………………………………….. 80,000

Share Capital—Ordinary

(24,000 X $2) …………………………………. 48,000

Share Premium—Ordinary

($80,000 – $48,000) ……………………….. 32,000

Aug. 1 Organization Expense …………………………... 50,000

Share Capital—Ordinary

(10,000 X $2) …………………………………. 20,000

Share Premium—Ordinary

($50,000 – $20,000) ……………………….. 30,000

EXERCISE 15.3 (10–15 minutes)

(a) Land (£60 X 25,000) ………………………………………… 1,500,000

(b) One might use the cost of treasury shares. However, this is not a

relevant measure of this economic event. Rather, it is a measure of a

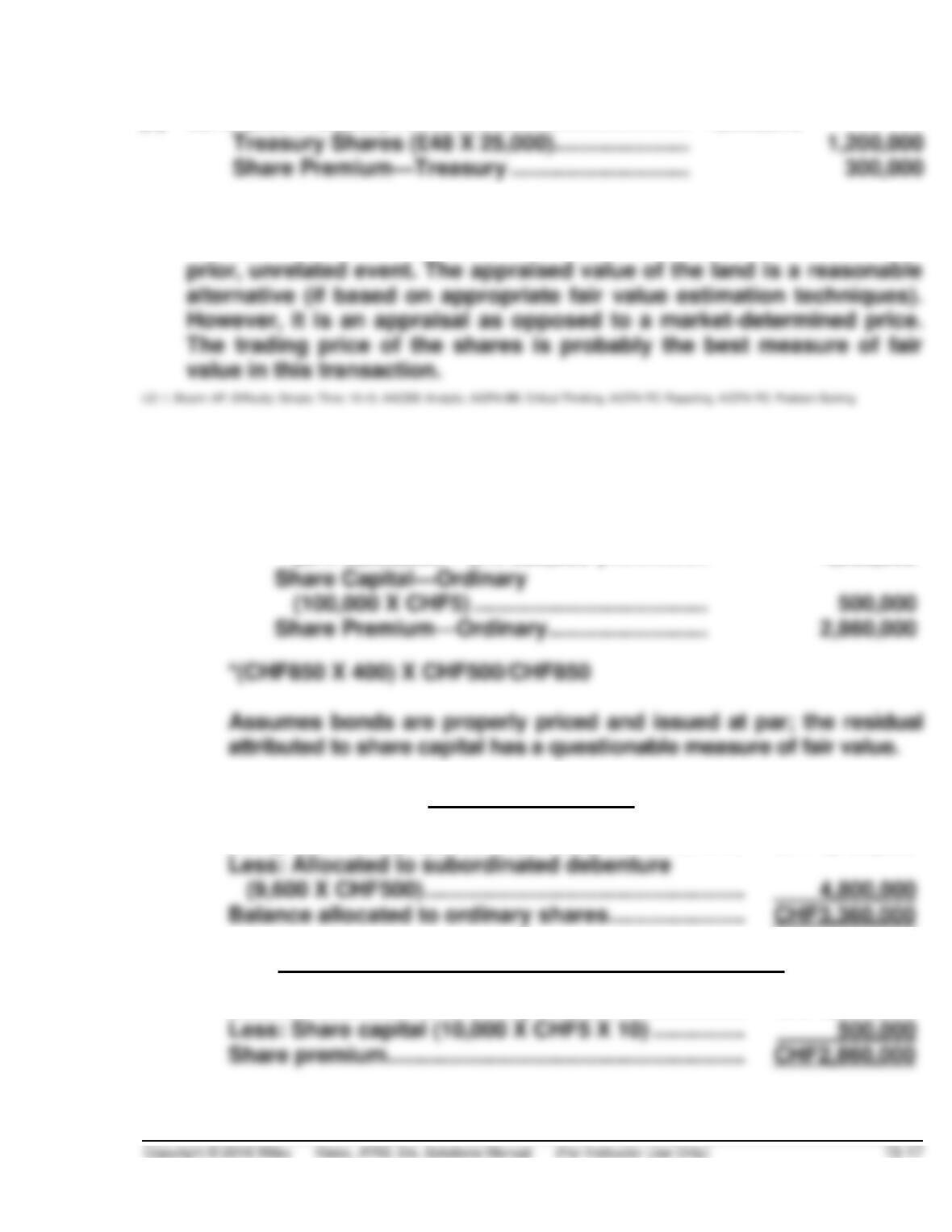

EXERCISE 15.4 (20–25 minutes)

(a) (1) Cash (CHF850 X 9,600) ………………………………… 8,160,000

Bonds Payable

(CHF5,000,000 – CHF200,000*) ……………. 4,800,000

Incremental method

Lump-sum receipt (9,600 X CHF850) ………………….. CHF8,160,000

Computation of share capital and share premium

Balance allocated to ordinary shares …………………. CHF3,360,000

EXERCISE 15.4 (Continued)

Bond issue cost allocation

Total issue cost (400 X CHF850) ………………… CHF 340,000

Less: Amount allocated to bonds ………………. 200,000

(2) Cash ………………………………………………………… 8,160,000

Bonds Payable …………………………………… 4,533,333

Share Capital—Ordinary

(100,000 X CHF5) …………………………….. 500,000

Share Premium—Ordinary ………………….. 3,126,667

(b) One is not better than the other, but would depend on the relative

reliability of the valuations for the shares and bonds. This question is

presented to stimulate some thought and class discussion.

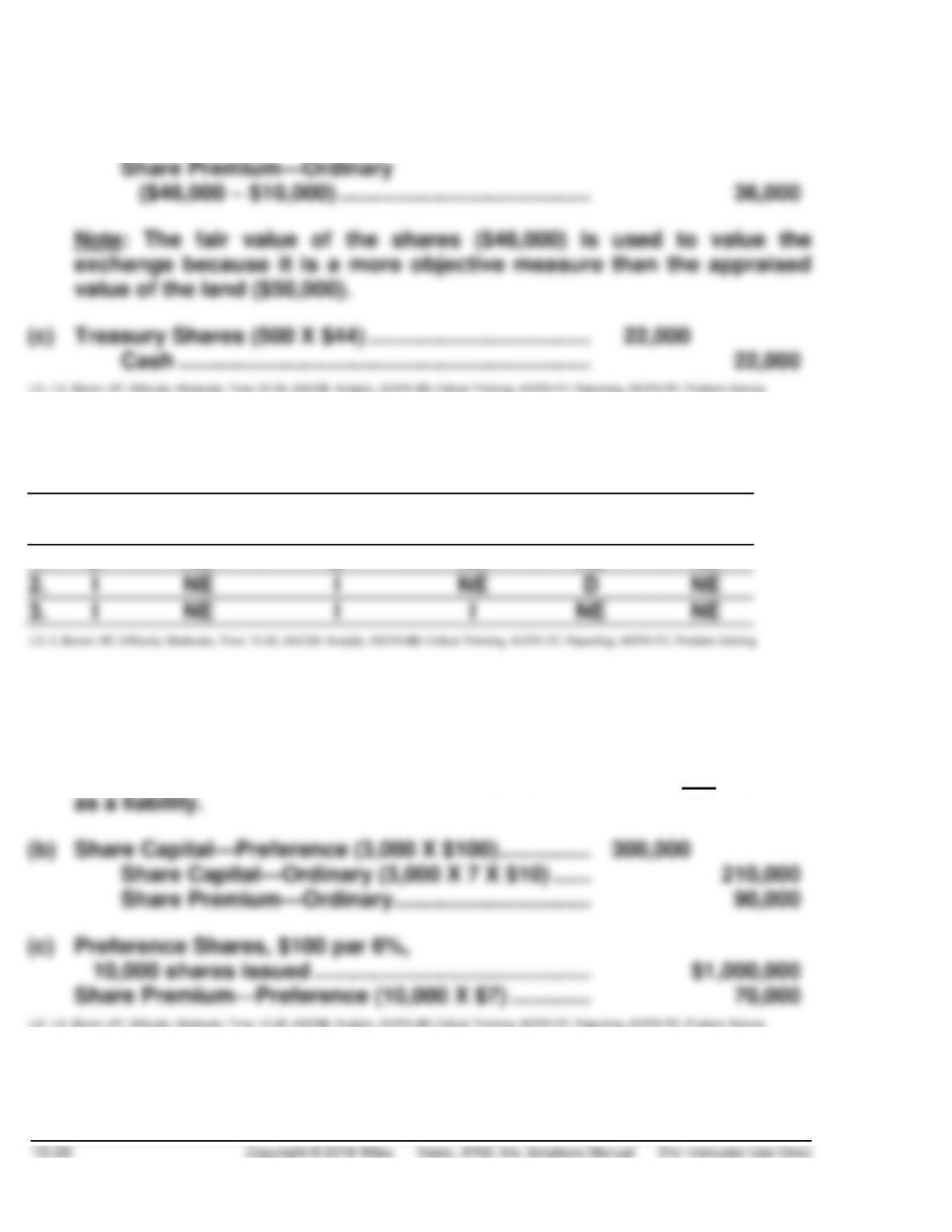

EXERCISE 15.5 (10–15 minutes)

(a) Fair value of Ordinary Shares (500 X €168) ………. € 84,000

Fair value of Preference Shares (100 X €210) ……. 21,000

€105,000

Allocated to Ordinary Shares:

(b) Lump-sum receipt €100,000

Allocated to ordinary (500 X €170) (85,000)

Balance allocated to preference € 15,000

Cash ………………………………………………………………. 100,000

EXERCISE 15.6 (25–30 minutes)

(a) Cash [(5,000 X $45) – $7,000] ……………………………… 218,000

EXERCISE 15.6 (Continued)

(b) Land (1,000 X $46) …………………………………………….. 46,000

Share Capital—Ordinary (1,000 X $10)…………. 10,000

EXERCISE 15.7 (15–20 minutes)

#

Assets

Liabilities

Equity

Share

Premium

Retained

Earnings

Net

Income

1.

D

NE

D

NE

NE

NE

EXERCISE 15.8 (15–20 minutes)

(a) $1,000,000 X 6% = $60,000; $60,000 X 3 = $180,000. The cumulative

dividend is disclosed in a note to the equity section; it is not reported