Problem 21.9 (Time 30–40 minutes)

Purpose—to develop an understanding of the accounting treatment accorded a sales-type lease involving an

unguaranteed residual value. The student is required to discuss the nature of the lease with regard to the

Problem 21.10 (Time 30–40 minutes)

Purpose—to develop an understanding of lessee accounting for a finance lease with an unguaranteed residual

Problem 21.11 (Time 30–40 minutes)

Purpose—to develop an understanding of how residual values affect the accounting for the lessee and the

Problem 21.12 (Time 35–45 minutes)

Purpose—to develop an understanding of the accounting procedures involved in a finance (sales-type) leasing

Problem 21.13 (Time 30–40 minutes)

Purpose—to provide an understanding of how lease information is reported on the statement of financial

Problem 21.14 (Time 30–40 minutes)

Purpose— The student is required to identify the type of lease involved, explain the respective reasons for their

Problem 21.15 (Time 20–30 minutes)

Purpose— The student is required to identify the type of lease involved, explain the respective reasons for their

SOLUTIONS TO PROBLEMS

PROBLEM 21.1

The lessee determines the lease liability as follows.

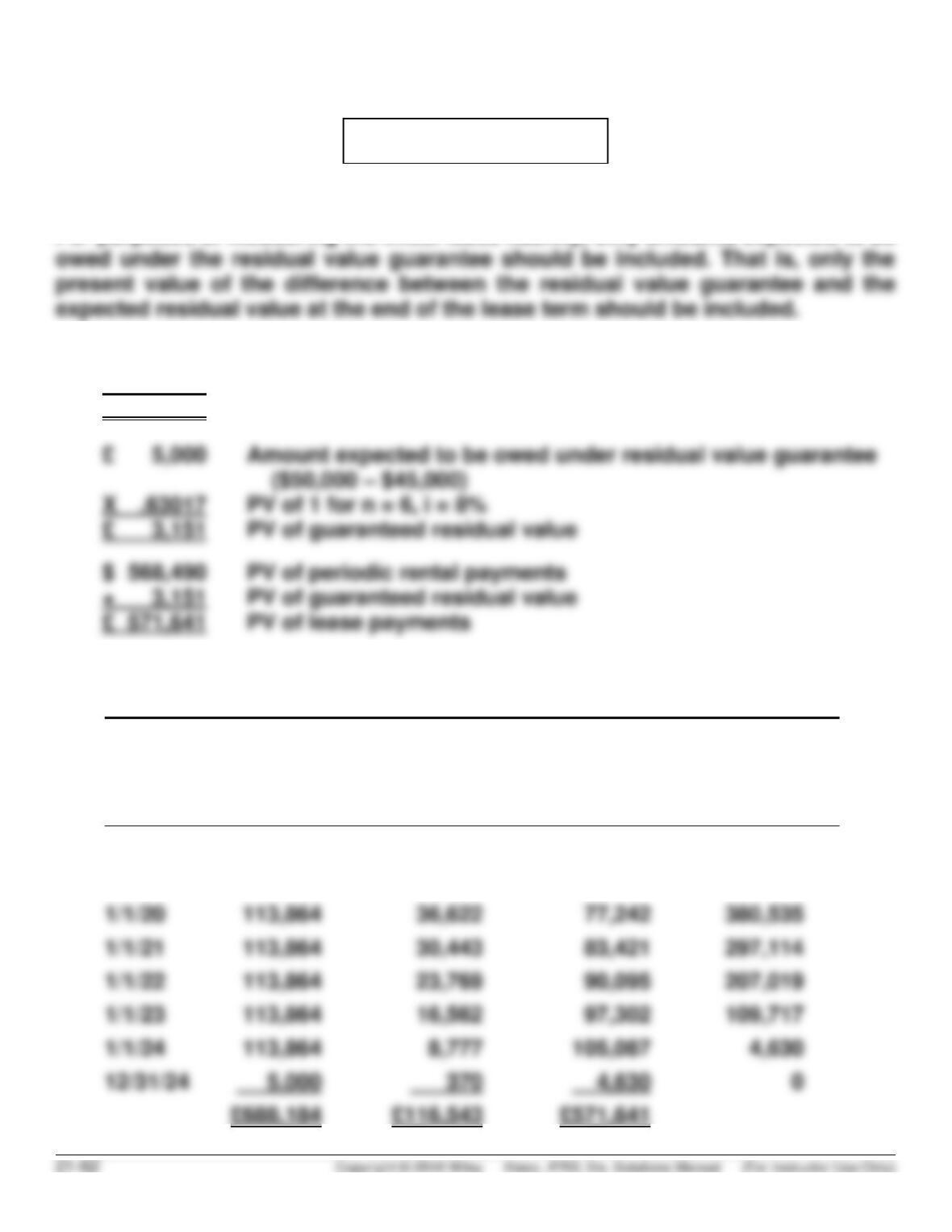

For purposes of measuring the initial lease liability, only amounts expected to be

£ 113,864 Annual rental payment

X 4.99271 PV of an annuity-due of 1 for n = 6, i = 8%

£ 568,490 PV of periodic rental payments

(a) VANCE PLC (Lessee)

Lease Amortization Schedule

Date

Annual

Lease

Payment

Plus GRV

Interest (8%)

on Liability

Reduction

of Lease

Liability

Lease

Liability

1/1/19

£571,641

1/1/19

£113,864

£ –0–

£113,864

457,777

380,535

1/1/22

1/1/23

1/1/24

PROBLEM 21.1 (Continued)

(b) January 1, 2019

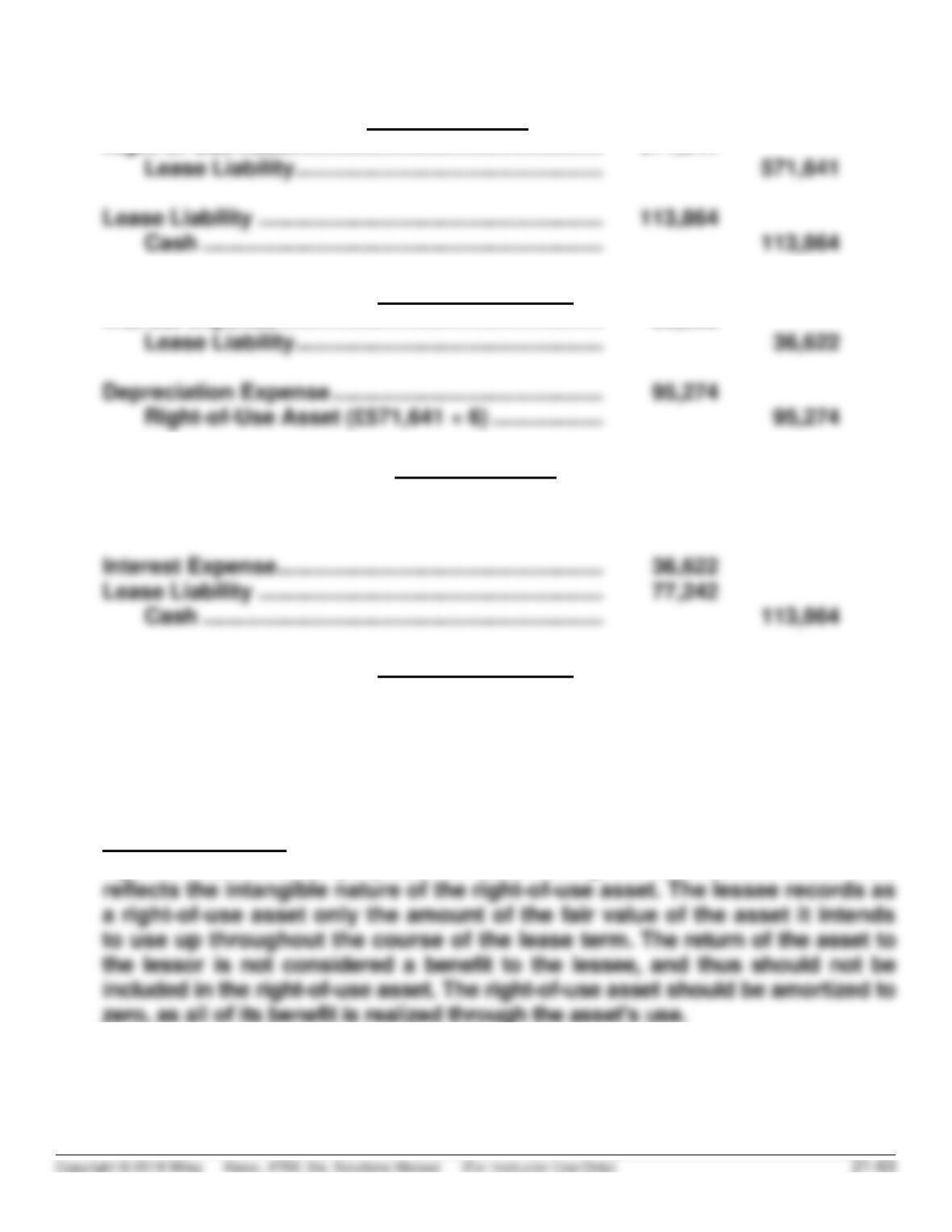

Right-of–Use Asset …………………………………………. 571,641

December 31, 2019

Interest Expense …………………………………………….. 36,622

January 1, 2020

Lease Liability ……………………………………………….. 36,622

Interest Expense ………………………………………. 36,622

December 31, 2020

Interest Expense …………………………………………….. 30,443

Lease Liability ………………………………………….. 30,443

Depreciation Expense …………………………………….. 95,274

Right-of–Use Asset …………………………………… 95,274

Note to instructor: The guaranteed residual value is not subtracted from the

right-of–use asset for purposes of determining the amortizable base. This

PROBLEM 21.1 (Continued)

(c) A lease incentive does not impact the measurement of the lease liability.

PROBLEM 21.2

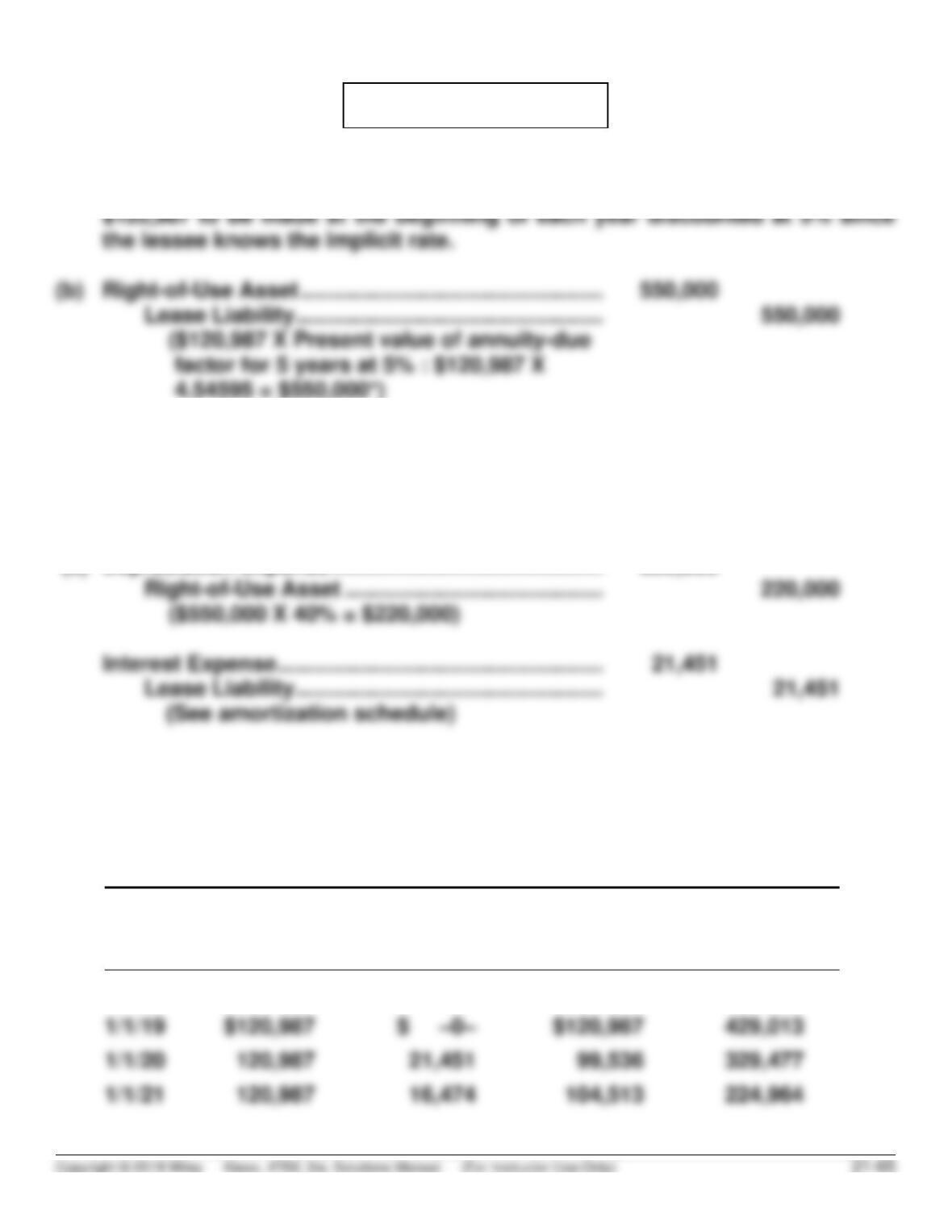

(a) The $550,000 is the present value of the five annual lease payments of

*Rounded.

Lease Liability ……………………………………………….. 120,987

Cash ……………………………………………………….. 120,987

(c) Depreciation Expense …………………………………….. 220,000

(d) Lease Liability ……………………………………………….. 120,987

Cash ……………………………………………………….. 120,987

CAGE COMPANY (Lessee)

Lease Amortization Schedule (partial)

Date

Annual

Lease

Payment

Interest (5%)

on Liability

Reduction

of Lease

Liability

Lease

Liability

1/1/19

$550,000

PROBLEM 21.2 (Continued)

(e) CAGE COMPANY

Statement of Financial Position (Partial)

December 31, 2019

*The current portion of the lease liability will contain a component for the accrued interest

(f) Insurance payments are an executory cost. Assuming a gross lease, the

insurance payments must be included in the present value of the lease payments

when initially valuing the lease liability. Therefore, the initial liability would be

measured as follows:

Present value of rental payments (see part b) ….. $550,000

Assets

Liabilities

Non-current assets:

Current:

Right-of-use Asset

$330,000

Lease liability

$120,987*

Noncurrent:

Lease liability

$329,477**

PROBLEM 21.3

(a) December 31, 2019

Right-of–Use Asset …………………………………………. 175,888

Lease Liability ………………………………………….. 175,888*

December 31, 2019

Lease Liability ……………………………………………….. 40,000

Cash ……………………………………………………….. 40,000

(To record the first rental payment)

(b) LUDWICK STEEL SA (Lessee)

Lease Amortization Schedule

(Annuity-Due Basis)

Date

Annual

Lease

Payment

Interest (8%)

on Liability

Reduction

of Lease

Liability

Lease

Liability

12/31/19

—

—

—

€175,888

12/31/23

12/31/24

PROBLEM 21.3 (Continued)

December 31, 2020

Depreciation Expense …………………………………….. 25,127

December 31, 2020

Interest Expense …………………………………………….. 10,871

(c) December 31, 2021

Depreciation Expense ……………………………………….. 25,127

Right-of–Use Asset ……………………………………… 25,127

(To record annual amortization on leased

assets)

PROBLEM 21.3 (Continued)

(d) LUDWICK STEEL SA

Statement of Financial Positon (Partial)

December 31, 2021

Non-current assets:

Current liabilities:

PROBLEM 21.4

Entries on August 1, 2019:

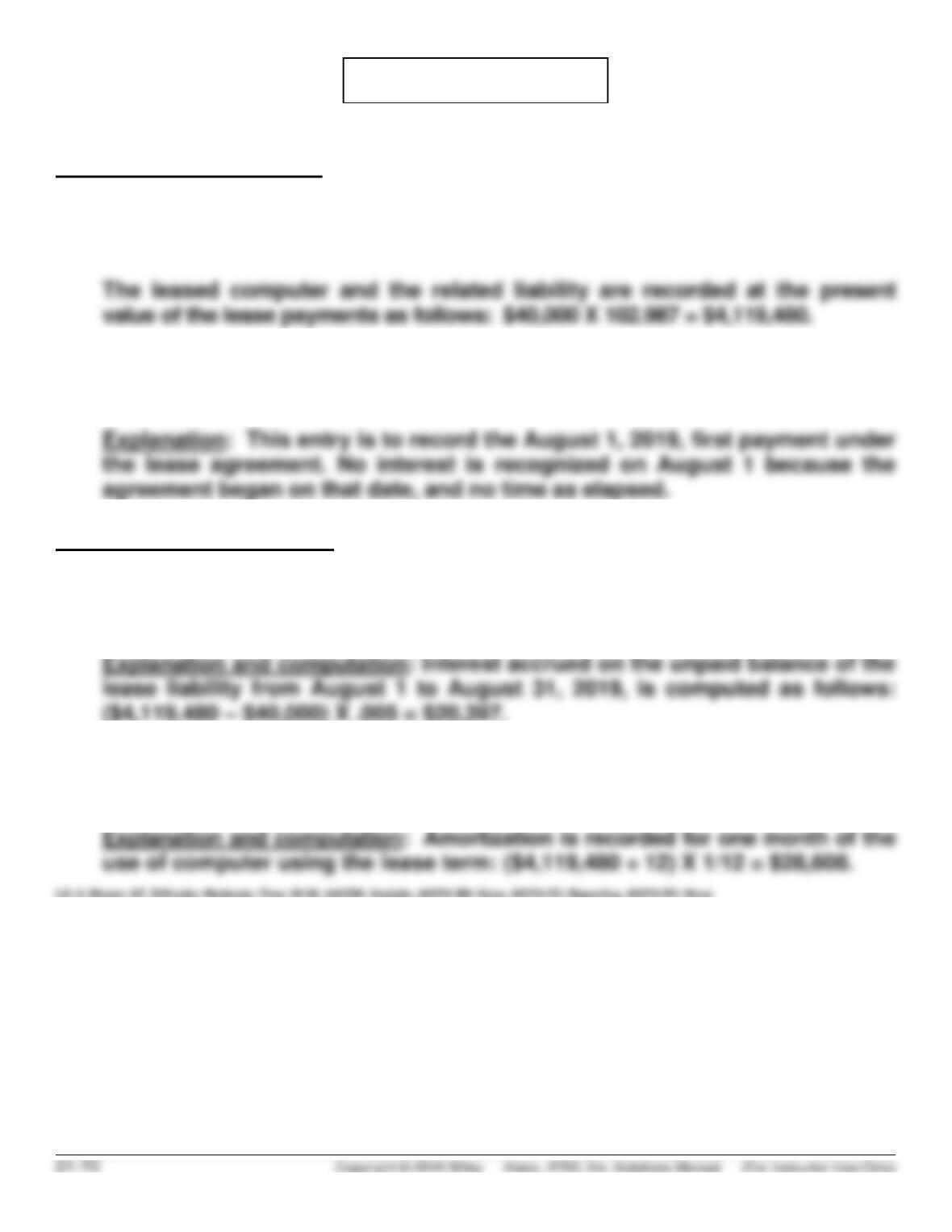

(1) Right-of–Use Asset ……………………………………… 4,119,480

Lease Liability ………………………………………. 4,119,480

(2) Lease Liability ………………………………………….. 40,000

Cash ………………………………………………….. 40,000

Entries on August 31, 2019:

(1) Interest Expense ……………………………………….. 20,397

Lease Liability …………………………………….. 20,397

(2) Depreciation Expense ……………………………….. 28,608

Right-of–Use Asset ……………………………… 28,608

PROBLEM 21.5

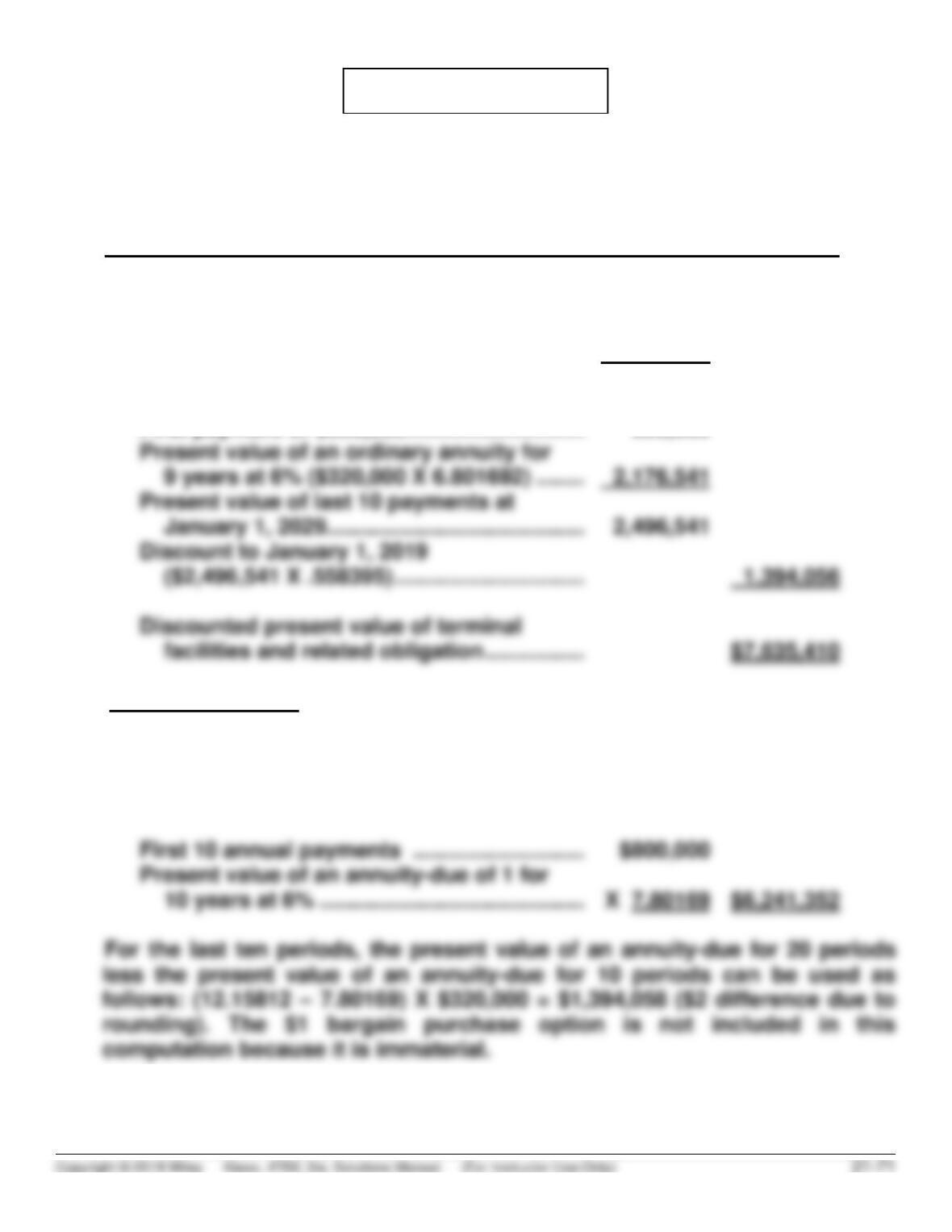

(a) GRISHELL TRUCKING

Schedule to Compute the Discounted Present Value

of Terminal Facilities and the Related Obligation

January 1, 2019

Present value of first 10 payments:

Immediate payment ………………………………… $ 800,000

Present value of an ordinary annuity for

9 years at 6% ($800,000 X 6.801692) …….. 5,441,354 $6,241,354*

Present value of last 10 payments:

First payment of $320,000 ……………………….. 320,000

(Note to instructor: The student can compute the $6,241,354 by using the

present value of an annuity-due for 10 periods at 6%.

*The calculation could also be done as a pure annuity-due of 1 for 10

periods as follows ($2 rounding difference):

PROBLEM 21.5 (Continued)

(b) GRISHELL TRUCKING

Journal Entries

(1) 1/1/21

Partial Amortization Schedule

(Annuity-Due Basis)

Date

Lease

Payment

Interest (6%)

on Lease

Liability

Reduction of

Lease

Liability

Lease

Liability

(2) 12/31/21

Depreciation Expense …………………………………….. 190,885

Right-of–Use Asset …………………………………… 190,885

purchase option is available at the end of the lease term.

(3) 12/31/21

Interest Expense …………………………………………….. 361,936

PROBLEM 21.6

(a) This is a sales-type lease for Glaus (lessor), since the lease term is greater

(b) Calculation of annual rental payment

(c) Computation of lease liability, or present value of lease payments:

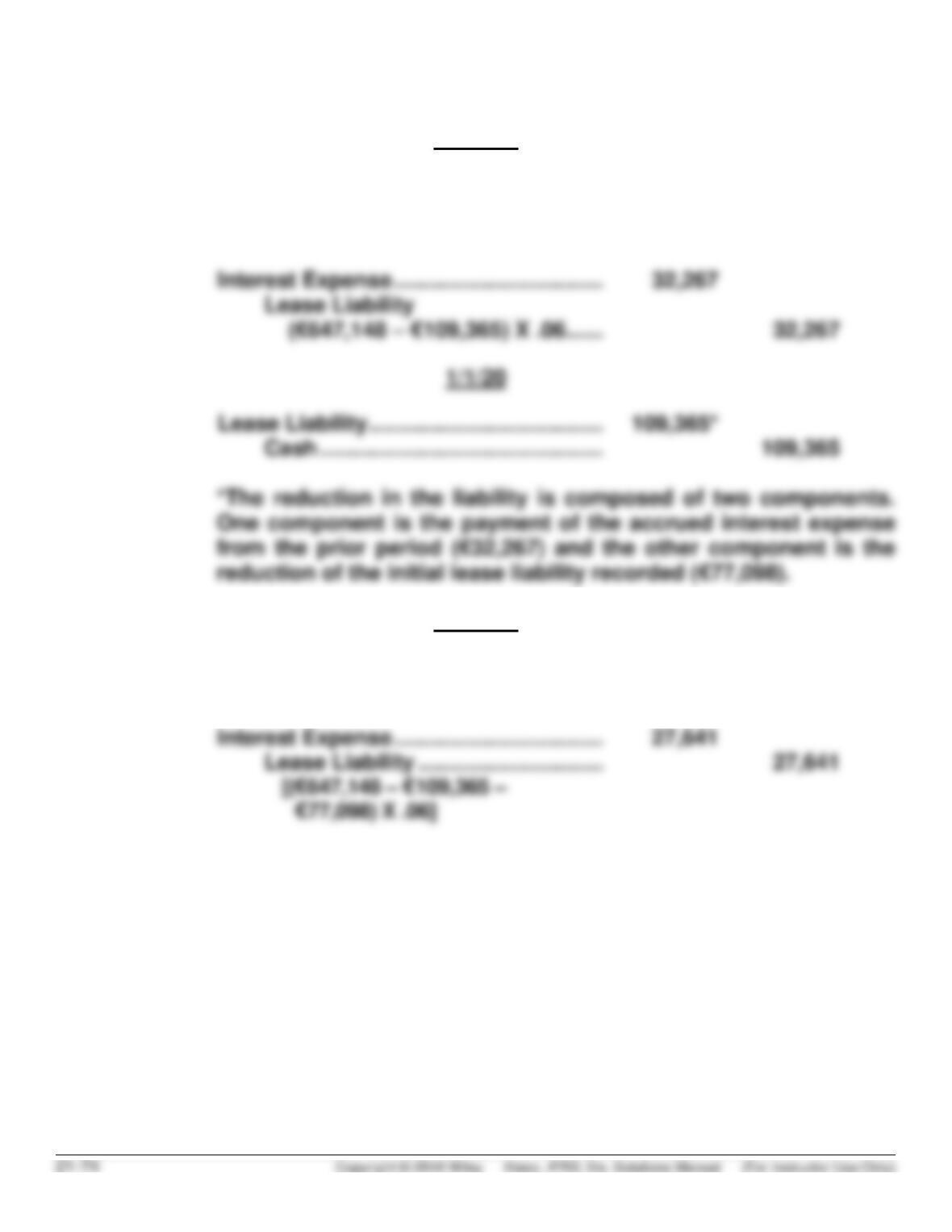

PV of annual payments: €109,365 X 5.91732* = €647,148

*Present value of an annuity-due at 6% for 7 periods.

1/1/19

(d) Right-of-Use Asset ………………………… 647,148

Lease Liability ………………………… 647,148

PROBLEM 21.6 (Continued)

12/31/19

Depreciation Expense ……………………. 92,450

Right-of–Use Asset

(€647,148 ÷ 7) ………………………. 92,450

12/31/20

Depreciation Expense ……………………. 92,450

Right-of–Use Asset ………………….. 92,450

PROBLEM 21.6 (Continued)

1/1/19

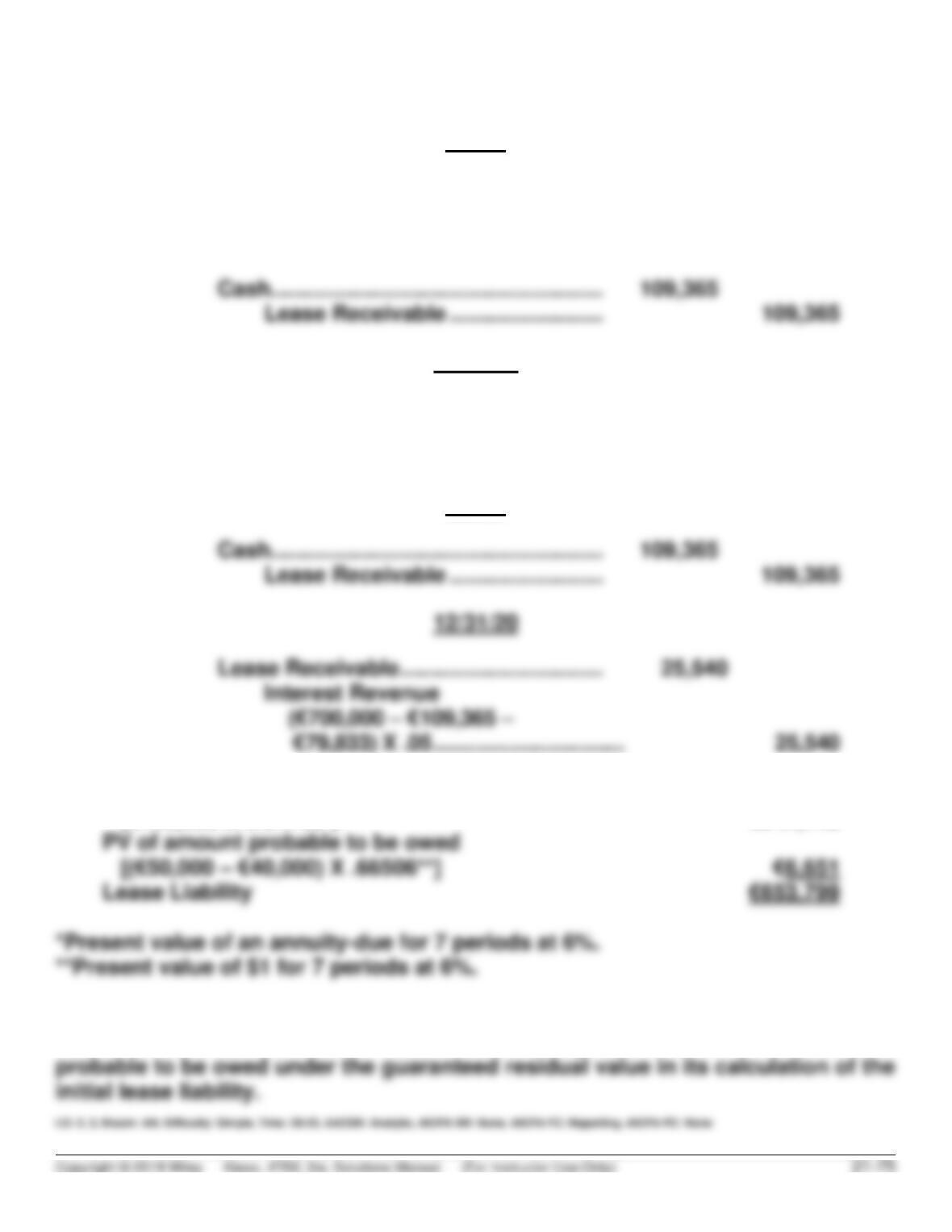

(e) Lease Receivable …………………………... 700,000

Cost of Goods Sold ……………………….. 525,000

Sales Revenue ………………………… 700,000

Inventory ………………………………… 525,000

12/31/19

Lease Receivable …………………………... 29,532

Interest Revenue

[(€700,000 – €109,365) X .05] … 29,532

1/1/20

(f) PV of annual payments

(€109,365 X 5.91732*) €647,148

In this case, the guaranteed residual value is greater than the expected residual

value. Therefore, the lessee must include the present value of the amount

PROBLEM 21.7

(a) The noncancelable lease is a sales-type lease because: (1) the lease term is

for 83% (10 ÷ 12) of the economic life of the leased asset, and

(2) the present value of the lease payments exceeds 90% of the fair value of

the leased property (see calculation below).

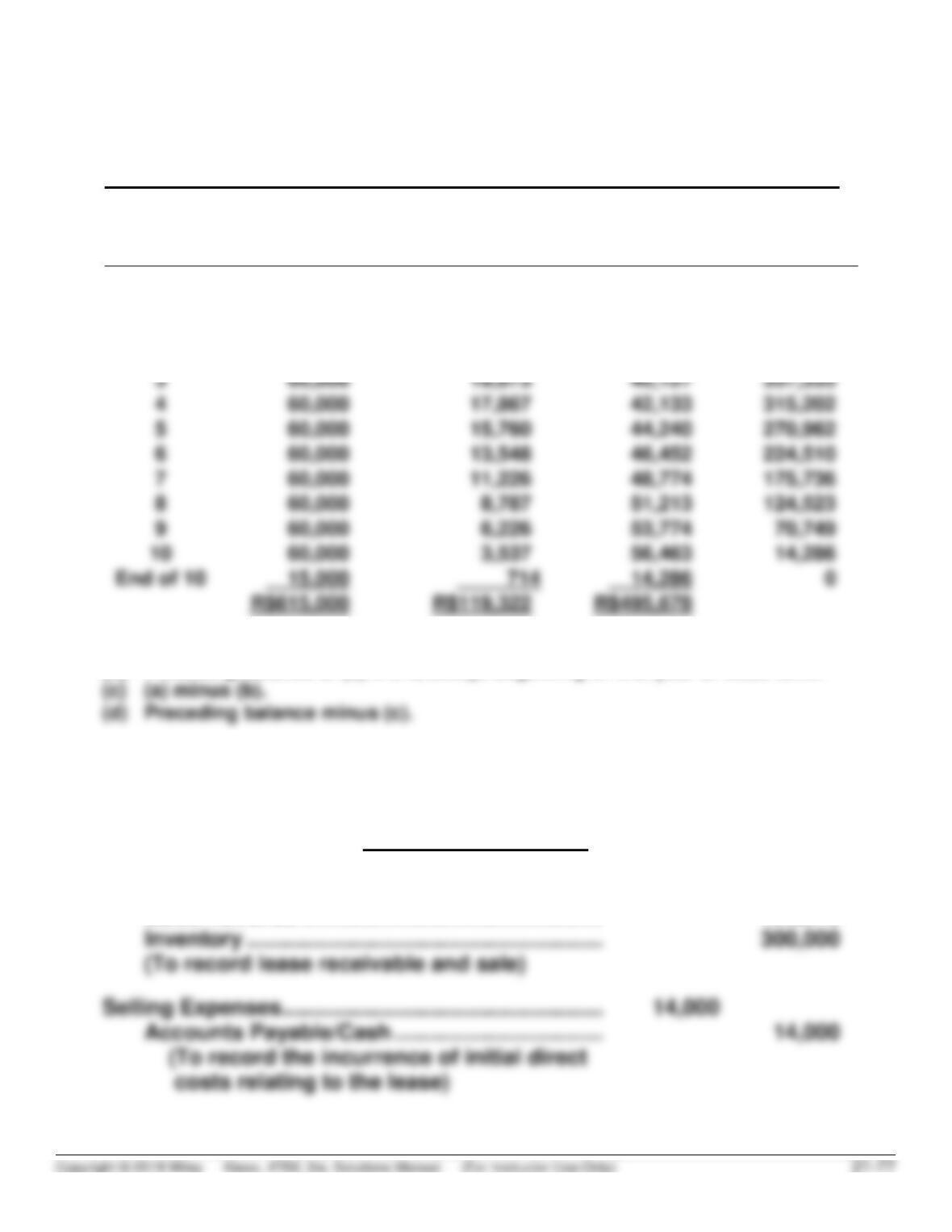

1. Lease Receivable:

Present value of annual payments of $60,000

made at the beginning of each period for 10 years,

2. Sales price is the same as the present value of

lease payments ……………………………………………………… R$495,678

PROBLEM 21.7 (Continued)

(b) AMIRANTE SA (Lessor)

Lease Amortization Schedule

(Annuity-Due basis, guaranteed residual value)

Beginning

of Year

Annual Lease

Payment Plus

Residual Value

Interest (5%)

on Lease

Receivable

Recovery

of Lease

Receivable

Lease

Receivable

(a)

(b)

(c)

(d)

Initial PV

—

—

—

R$495,678

1

R$ 60,000

—

R$ 60,000

435,678

2

60,000

R$ 21,784

38,216

397,462

3

357,335

4

315,202

5

60,000

44,240

270,962

6

224,510

7

8

60,000

51,213

9

R$615,000

R$495,678

(a) Annual lease payments and guaranteed residual value.

(b) Preceding balance of (d) X 5%, except beginning of first year of lease term.

(c) Lessor’s journal entries:

Beginning of the Year

Lease Receivable …………………………………………… 495,678

Cost of Goods Sold ………………………………………… 300,000

Sales Revenue …………………………………………. 495,678

PROBLEM 21.7 (Continued)

Cash ………………………………………………………………… 60,000

Lease Receivable ………………………………………… 60,000

(To record receipt of the first lease

payment)

End of the Year

PROBLEM 21.8

(a)

For purposes of measuring the initial lease liability, only probable amounts

expected to be owed under the residual value guarantee should be included.

That is, only the present value of the difference between

PROBLEM 21.8 (Continued)

(b) CHAMBERS MEDICAL (Lessee)

Lease Amortization Schedule

(Annuity-Due Basis, GRV)

Beginning

of Year

Annual Lease

Payment Plus

GRV

Interest (5%)

on Unpaid

Liability

Reduction

of Lease

Liability

Lease

Liability

(a)

(b)

(c)

(d)

Initial PV

R$489,539

1

R$ 60,000

R$ 0

R$ 60,000

429,539

2

60,000

21,477

38,523

391,016

3

60,000

19,551

40,449

350,567

4

60,000

42,472

308,095

5

60,000

44,595

6

60,000

13,175

46,825

216,675

7

60,000

49,166

167,509

8

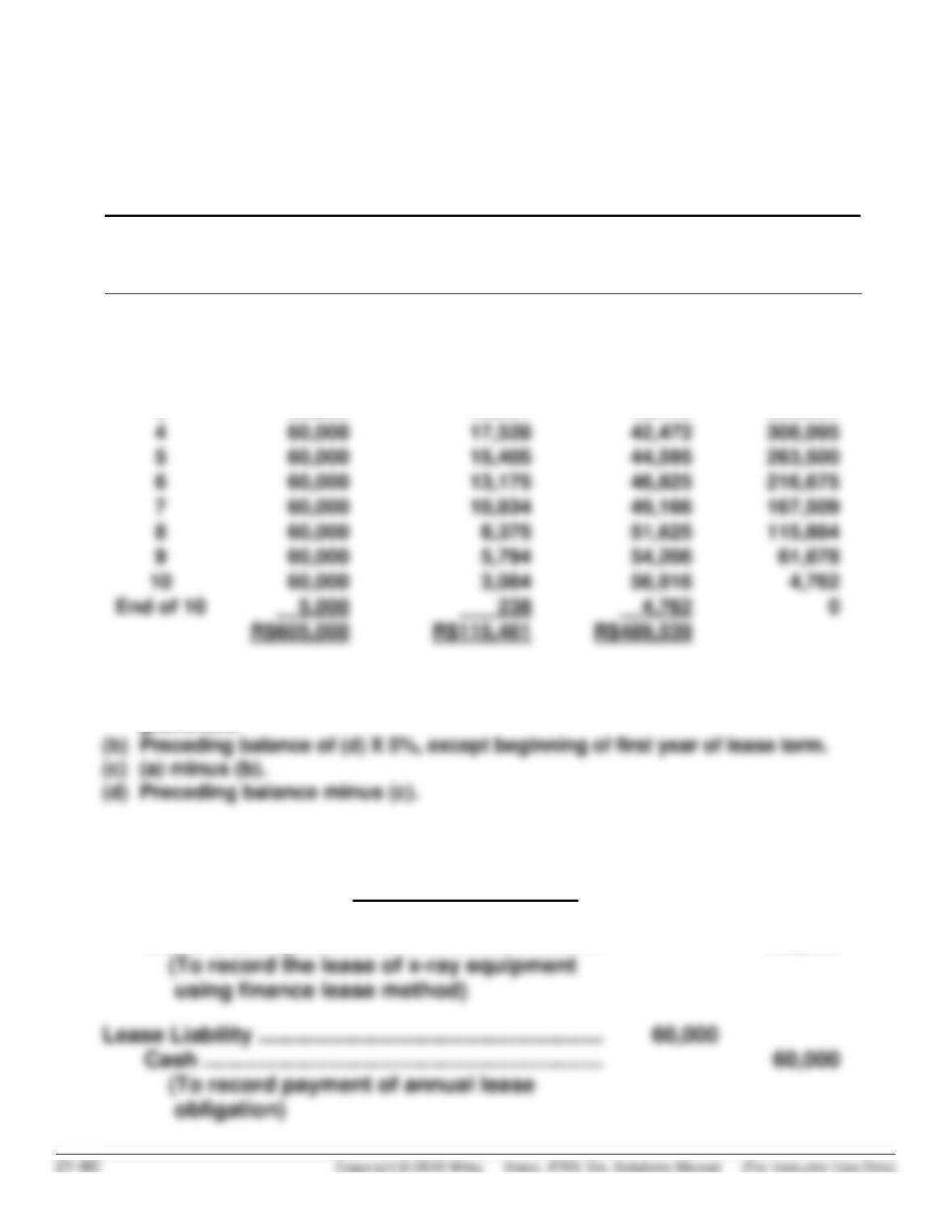

60,000

51,625

115,884

9

60,000

54,206

60,000

56,916

238

(a) Annual lease payments and amount expected to be owed under residual value

guarantee.

(c) Lessee’s journal entries:

Beginning of the Year

Right-of–Use Asset …………………………………………. 489,539

Lease Liability ………………………………………….. 489,539