EXERCISE 7.5 (Continued)

(b)

July 29

Cash ……………………………………………………….

2,000

Accounts Receivable—Arquette …………………………

1,960

Sales Discounts Forfeited …………………………..

40

EXERCISE 7.6 (5–10 minutes)

July 1

Accounts Receivable ………………………………………………

30,000

Sales Revenue ……………………………………………….

30,000

July 10

Cash ……………………………………………………….

Sales Discounts ………………………………………………………

Accounts Receivable …………………………..

30,000

Accounts Receivable ………………………………………………

Sales Revenue ……………………………………………….

Cash ……………………………………………………….

Accounts Receivable …………………………..

EXERCISE 7.7 (10–15 minutes)

(a)

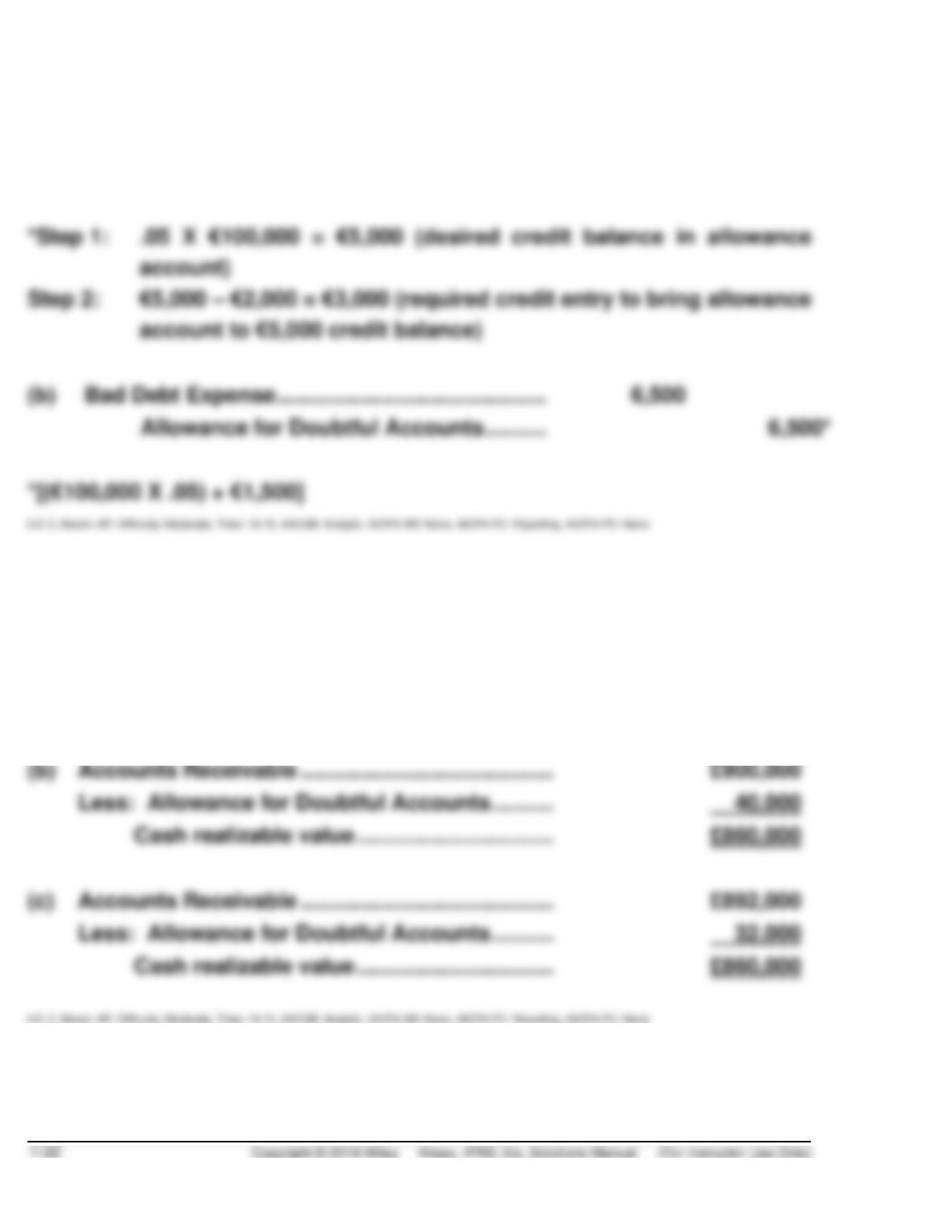

Bad Debt Expense …………………………………………………..

3,000

Allowance for Doubtful Accounts …………………….

3,000*

(b)

Bad Debt Expense …………………………………………………..

6,500

Allowance for Doubtful Accounts …………………….

6,500*

EXERCISE 7.8 (5–10 minutes)

(a)

Allowance for Doubtful Accounts …………………………..

8,000

Accounts Receivable …………………………..

8,000

(b)

Accounts Receivable ………………………………………………

Less: Allowance for Doubtful Accounts …………………..

Cash realizable value …………………………..

(c)

Accounts Receivable ………………………………………………

Less: Allowance for Doubtful Accounts …………………..

Cash realizable value …………………………..

EXERCISE 7.9 (8–10 minutes)

(a)

Bad Debt Expense …………………………………………………..

4,950

Allowance for Doubtful Accounts

($80,000 X 4%) + $1,750 = $4,950 ………………….

(b)

Bad Debt Expense …………………………………………………..

Allowance for Doubtful Accounts

[($80,000 X 5%) – $1,700] …………………………..

EXERCISE 7.10 (10–12 minutes)

(a) The direct write-off approach is not theoretically justifiable even

though required for income tax purposes. The direct write-off method

does not match expenses with revenues of the period, nor does it

EXERCISE 7.11 (8–10 minutes)

Balance 1/1 ($700 – $255)

$ 445

Over one year

4/12 (#2412) ($1,710 – $1,000 – $400*)

310

Eight months and 19 days

11/18 (#5681) ($2,000 – $1,250)

750

One month and 13 days

EXERCISE 7.12 (15–20 minutes)

7/1

Accounts Receivable—Legler Co. …………………………..

9,800

Sales Revenue (€10,000 X 98%) ……………………….

9,800

7/5

Cash [€12,000 X (1 – .09)]…………………………………………

Loss on Sale of Receivables …………………………..

1,080

Accounts Receivable (€12,000 X 98%) ………………

Sales Discounts Forfeited …………………………..

EXERCISE 7.12 (Continued)

7/9

Accounts Receivable ……………………………………………….

180

Sales Discounts Forfeited

(€9,000 X 2%) ……………………………………………….

180

Cash ……………………………………………………………………….

5,640

Finance Charge (€6,000 X 6%) …………………………..

360

Notes Payable …………………………………………………

7/11

Accounts Receivable—Legler Co. …………………………..

200

Sales Discounts Forfeited

(€10,000 X 2%) …………………………..………………….

This entry may be made at the next time financial statements are

prepared. Also, it may occur on 12/29 when Legler Company’s receiv–

able is adjusted.

12/29

Allowance for Doubtful Accounts …………………………..

9,000

Accounts Receivable—Legler Co.

[€9,800 + €200 = €10,000;

€10,000 – (10% X €10,000) = €9,000] ………………

9,000

12/31

Bad Debt Expense ………………………………………………….

Allowance for Doubtful Accounts

(€350,000 – €275,000) …………………………..

EXERCISE 7.13 (10–15 minutes)

1.

7/1/19

Notes Receivable …………………………………………………….

900,000

Land ……………………………………………………….

590,000

Gain on Sale of Land

(£900,000 – £590,000) ……………..

310,000

Computation of total interest

Face value of note

Present value of 1 for 4 periods at 12%

Present value of note

Face value of note

Total interest on notes receivable

2.

7/1/19

Notes Receivable …………………………………………………….

221,163.68

Service Revenue …………………………..

221,163.68

Computation of the present value of the note:

Maturity value ……………………………………………………

£400,000.00

Present value of £400,000 due in

8 years at 12%—£400,000 X .40388 ………………….

Present value of £12,000

payable annually for 8 years at

12% annually—£12,000 X 4.96764 …………………….

Present value of the note …………………………..

EXERCISE 7.14 (20–25 minutes)

(a)

Notes Receivable ……………………………………………………

247,935

Service Revenue …………………………………………….

247,935*

(b)

Notes Receivable ……………………………………………………

24,794

Interest Revenue …………………………………………….

24,794*

*$247,935 X 10% = $24,794

(c)

Notes Receivable ……………………………………………………

Interest Revenue …………………………………………….

* ($247,935 + $24,794) x 10% = 27,273

Notes Receivable ……………………………………………

EXERCISE 7.15 (10–15 minutes)

(a)

Cash ………………………………………………………………………

290,000

Interest Expense …………………………………………………….

Notes Payable ………………………………………………..

*2% X $500,000 = $10,000

(b)

Cash ………………………………………………………………………

350,000

Accounts Receivable …………………………..

EXERCISE 7.15 (Continued)

(c)

Notes Payable ……………………………………………………….

300,000

Interest Expense …………………………………………………….

Cash ……………………………………………………….

*10% X $300,000 X 3/12 = $7,500

EXERCISE 7.16 (15–18 minutes)

1.

Cash ……………………………………………………….

18,000

Loss on Sale of Receivables

(¥20,000 X 10%) ……………………………………………………

2,000

Accounts Receivable …………………………..

20,000

2.

Cash ……………………………………………………….

50,600

Interest Expense (¥55,000 X 8%) …………………………..

4,400

Notes Payable …………………………..…………………….

55,000

3.

Bad Debt Expense …………………………………………………..

5,850

Allowance for Doubtful Accounts

[(¥82,000 X 5%) + ¥1,750] …………………………..

4.

Bad Debt Expense …………………………………………………..

Allowance for Doubtful Accounts

(¥5,800 – ¥1,100) …………………………………………..

EXERCISE 7.17 (10–15 minutes)

Cash ………………………………………………………………………

190,000

Interest Expense …………………………..…………………………

10,000

Liability to Warren Company …………………………..

200,000

LO: 5, Bloom: AP, Difficulty: Moderate, Time: 10-15, AACSB: Analytic, AICPA BB: None, AICPA FC: Reporting, AICPA PC: None

EXERCISE 7.18 (15–20 minutes)

(a)

According to the IASB, determining whether receivables that are trans–

ferred can be accounted for as a sale is based on an evaluation of

(b)

The following journal entry would be made:

Cash ……………………………………………………….

235,000

Due from Factor (€250,000 X 4%) ……………………..

10,000

(€250,000 X 2%) ……………………………………………

Accounts Receivable …………………………..

EXERCISE 7.19 (10–15 minutes)

(a)

July 1

Cash ……………………………………………………….

378,000

Due from Factor ………………………………………………………

16,000*

Loss on Sale of Receivables …………………………..

**(1 1/2% X ¥400,000) = ¥6,000

(b)

July 1

Accounts Receivable …………………………..

400,000

Due to SEK Corp. …………………………..

Financing Revenue …………………………..

EXERCISE 7.20 (10–15 minutes)

(a)

Accounts Receivable ……………………………………………….

100,000

Sales Revenue ………………………………………………..

100,000

Accounts Receivable …………………………..

(b) Accounts Receivable Turnover =

Net Sales

Average Trade Receivables (net)

(c) Grant’s turnover ratio has declined significantly. That is, it is turning

EXERCISE 7.21 (10–15 minutes)

(a)

Cash [€10,000 X (1 – .09)] …………………………………………

9,100

Due from Factor ………………………………………………………

500

Loss on Sale of Receivables …………………………..

400

Accounts Receivable ………………………………………

Computation of cash received

Accounts receivable ……………………………………….

Less: Due from factor (5% X €10,000) ………………

Finance charge (4% X €10,000) ………………

Cash received …………………………………………..

(b) Accounts Receivable Turnover =

Net Sales

Average Trade Receivables (net)

Average Trade Receivables (net)

=

*EXERCISE 7.22 (5–10 minutes)

1.

April 1

Petty Cash ……………………………………………………….

Cash ……………………………………………………….

2.

April 10

Inventory (Transportation-in) …………………………..

60

Supplies Expense …………………………..

25

Postage Expense …………………………………………………….

40

Accounts Receivable—Employees …………………………..

17

Miscellaneous Expense …………………………..

36

Cash Over and Short …………………………..

10

Cash ($200 – $12) …………………………..

3.

April 20

Petty Cash ……………………………………………………….

Cash ……………………………………………………….

*EXERCISE 7.23 (10–15 minutes)

Accounts Receivable—Employees

($40.00 + $34.00) ……………………………………………………

74.00

Nick Teasdale, Drawings ………………………………………….

Maintenance and Repair Expense …………………………..

14.35

Postage Expense ($20.00 – $7.90) …………………………..

12.10

Supplies ………………………………………………………………….

Cash Over and Short ………………………………………………..

11.45

Cash ($300.00 – $10.20) …………………………………..

*EXERCISE 7.24 (15–20 minutes)

(a) KIPLING PLC

Bank Reconciliation

July 31

Balance per bank statement, July 31 ………………………..

£ 8,650

Add: Deposits in transit ………………………………………….

2,850a

Deduct: Outstanding checks …………………………..

1,100b

Correct cash balance, July 31 …………………………..

£10,400

Add: Collection of note ………………………………………….

Less: Bank service charge …………………………..

NSF check ……………………………………………………

Corrected cash balance, July 31 …………………………..

£10,400

Deposits per books

Deposits per bank in July

£ 4,500

Less deposits in transit (June)

1,540

Deposits mailed and received

in July

Deposits in transit, July 31

bComputation of outstanding checks

Checks written per books

£3,100

Checks cleared by bank in July

£ 4,000

Less outstanding checks

(June)*

2,000

Checks written and cleared

in July

Outstanding checks, July 31

*EXERCISE 7.24 (Continued)

(b)

Cash……………………………………………………………………….

1,150

Office Expense (Bank Charges) …………………………..

15

Accounts Receivable ……………………………………………….

Notes Receivable …………………………………………….

*EXERCISE 7.25 (15–20 minutes)

(a) ARAGON COMPANY

Bank Reconciliation, August 31, 2019

County National Bank

Balance per bank statement, August 31, 2019 ……………

$ 8,089

Add: Cash on hand ………………………………………………….

Balance per books, August 31, 2019

($10,050 + $35,000 – $35,403) …………………………..

$ 9,647

Add: Note ($1,000) and interest ($40) collected ………….

1,040

Deduct: Bank service charges …………………………..

Understated check for supplies …………………..

38

(b)

Notes Receivable …………………………………………….

Interest Revenue ……………………………………………..

(To record collection of note and interest)

*EXERCISE 7.25 (Continued)

Office Expense—Bank Charges …………………………..

20

Cash ………………………………………………………………

20

(To record August bank charges)

Supplies Expense ……………………………………………………

18

Cash ………………………………………………………………

18

TIME AND PURPOSE OF PROBLEMS

Problem 7.1 (Time 20–25 minutes)

Purpose—to provide the student with an understanding of the statement of financial position effect that

Problem 7.2 (Time 20–25 minutes)

Purpose—to provide the student with the opportunity to determine various items related to accounts

receivable and the allowance for doubtful accounts. Five independent situations are provided.

Problem 7.3 (Time 20–30 minutes)

Problem 7.4 (Time 25–35 minutes)

Problem 7.5 (Time 20–30 minutes)

Problem 7.6 (Time 25–35 minutes)

Purpose—to provide the student with a number of business transactions related to accounts receivable

that must be journalized. Recoveries of receivables, and write-offs are the types of transactions

presented. The problem provides a good cross section of a number of accounting issues related to

receivables.

Problem 7.7 (Time 30–35 minutes)

Purpose—to provide the student with a simple note receivable problem with no imputation of interest.

Problem 7.8 (Time 30–35 minutes)

Problem 7.9 (Time 40–50 minutes)

Purpose—the student calculates the current portion of long-term receivables and interest receivable,

Problem 7.10 (Time 25–30 minutes)

Problem 7.11 (Time 20–25 minutes)

Time and Purpose of Problems (Continued)

*Problem 7.12 (Time 20–25 minutes)

Purpose—to provide the student the opportunity to do the accounting for petty cash and a bank

reconciliation.

SOLUTIONS TO PROBLEMS

PROBLEM 7.1

(a)

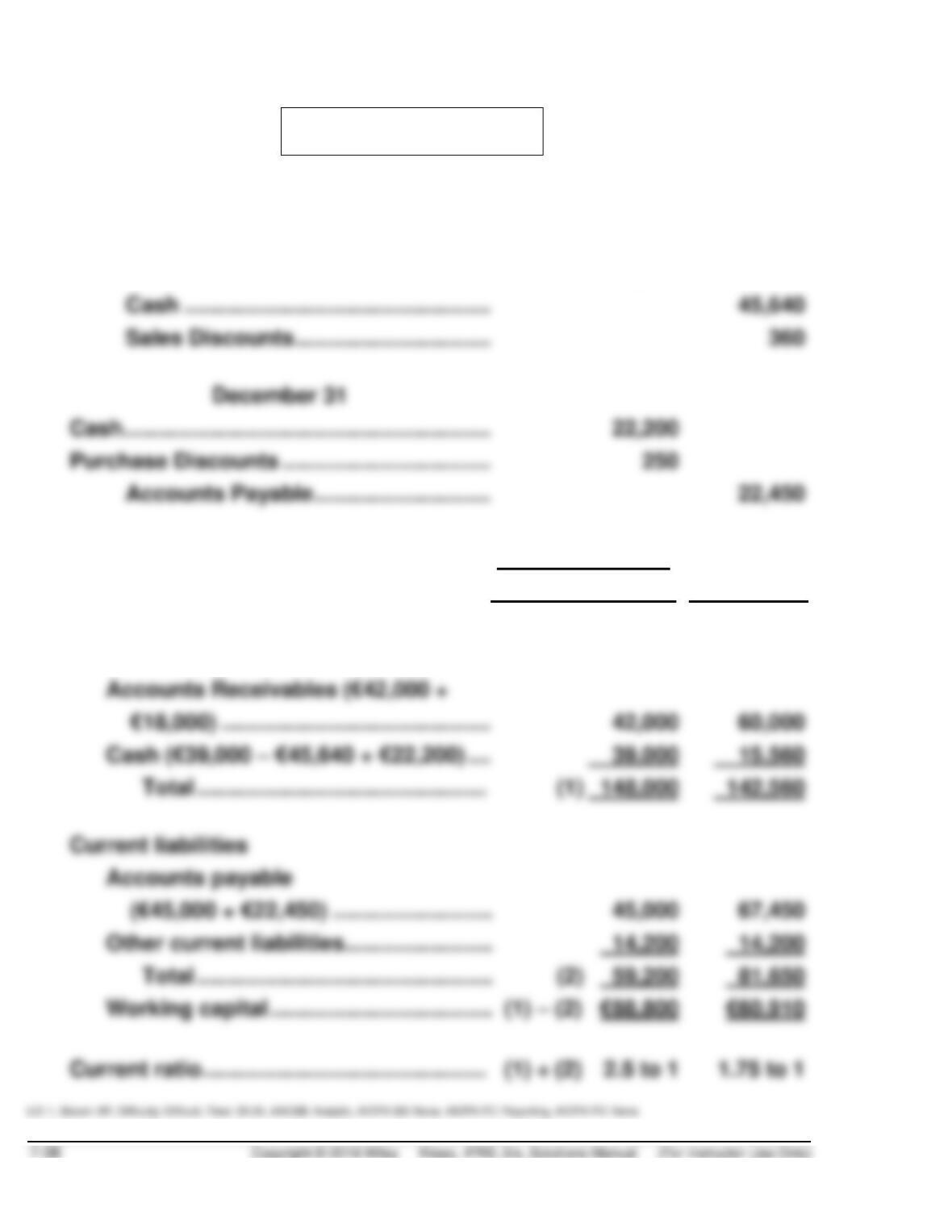

December 31

Accounts Receivable (€17,640 + €360) ………………..

18,000

Sales Revenue ………………………………………………….

28,000

Cash ……………………………………………………….

Sales Discounts …………………………..

December 31

22,200

Purchase Discounts …………………………..……………..

Accounts Payable …………………………..

(b)

Per Statement of

Financial Position

After

Adjustment

Current assets

Inventory ……………………………………………………….

€ 67,000

€ 67,000

Accounts Receivables (€42,000 +

€18,000) ……………………………………………………….

42,000

Cash (€39,000 – €45,640 + €22,200) ……………………..

Total ……………………………………….. (1)

Current liabilities

Other current liabilities ……………………

Total ………………………………………… (2)

PROBLEM 7.2

1.

Accounts receivables ……………………………………………………

$ 53,000

Percentage …………………………………………………………………..

7%

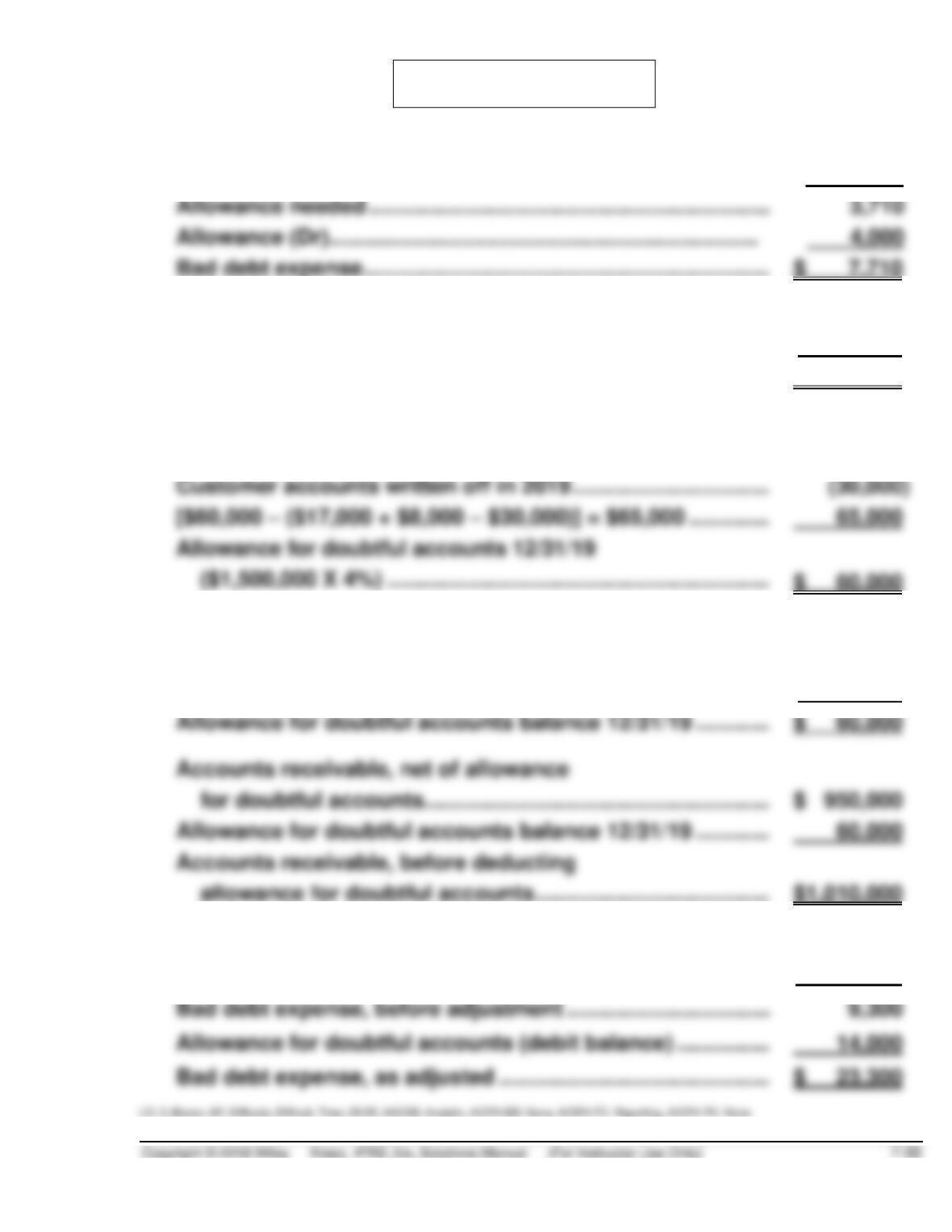

Allowance needed ………………………………………………………..

Allowance (Dr)……………..………………..…………………………….

Bad debt expense …………………………………………………………

2.

Accounts receivable …………………………………………………….

$1,750,000

Amounts estimated to be uncollectible ………………………….

(180,000)

Cash realizable value ……………………………………………………

$1,570,000

3.

Allowance for doubtful accounts 1/1/19 …………………………

$ 17,000

Collections of accounts written off in prior years ……………

8,000

Customer accounts written off in 2019 …………………………..

[$60,000 – ($17,000 + $8,000 – $30,000)] = $65,000 ………….

65,000

4.

Bad debt expense for 2019 ……………………………………………

$ 84,000

Customer accounts written off as uncollectible

during 2019 ………………………………………………………………

(24,000)

Allowance for doubtful accounts balance 12/31/19 …………

$ 60,000

Allowance for doubtful accounts balance 12/31/19 …………

60,000

5.

Accounts receivable …………………………………………………….

$ 310,000

Percentage …………………………………………………………………..

X 3%

Bad debt expense, before adjustment …………………………...

Allowance for doubtful accounts (debit balance) ……………

14,000

PROBLEM 7.3

(a) The Allowance for Doubtful Accounts should have a balance of $45,000

at year-end. The supporting calculations are shown below:

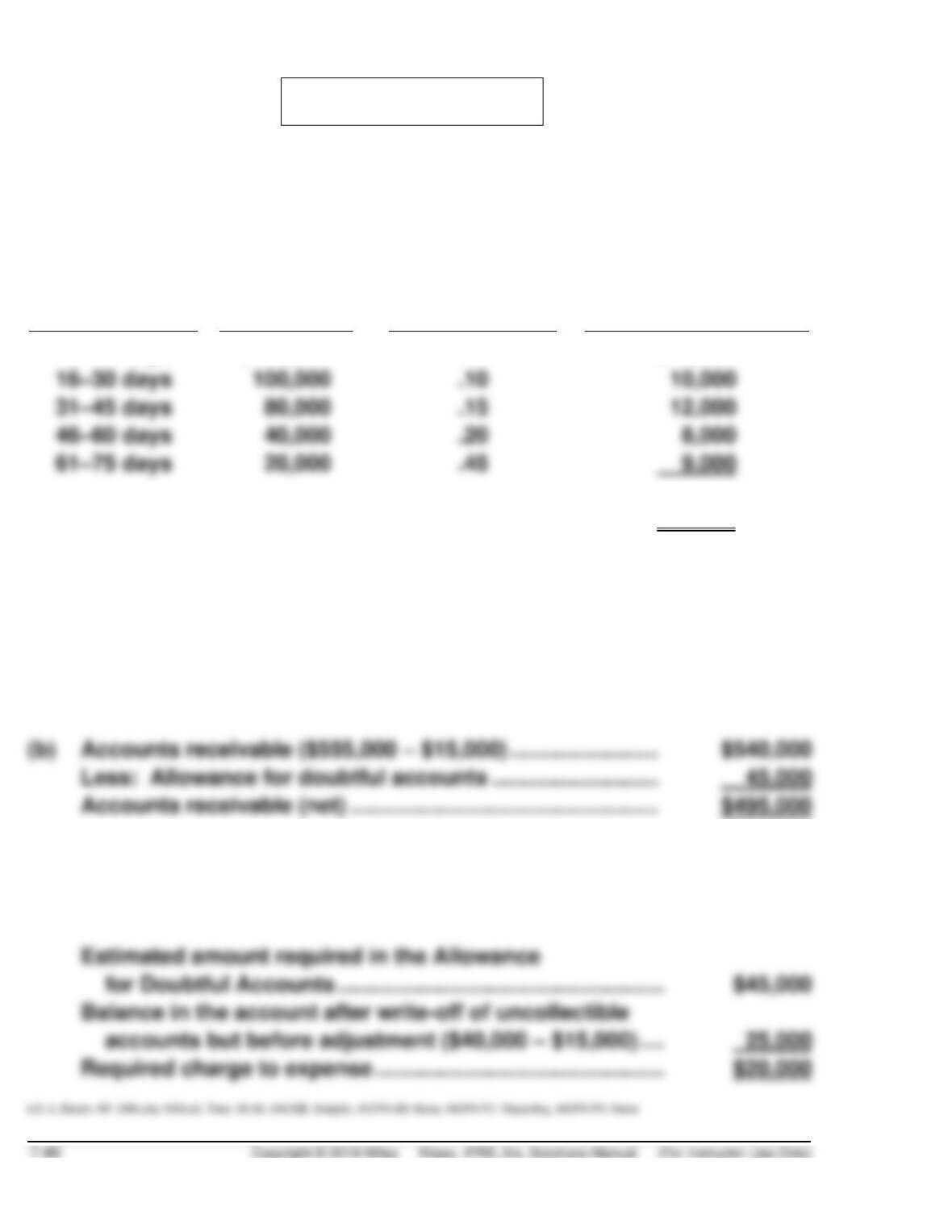

Days Account

Outstanding

Amount

Expected

Percentage

Uncollectible

Estimated

Uncollectible

0–15 days

$300,000

.02

$ 6,000

.10

80,000

.15

40,000

.20

.45

9,000

Balance for Allowance for Doubtful Accounts

$45,000

The accounts which have been outstanding over 75 days ($15,000)

and have zero probability of collection would be written off immediately

by a debit to Allowance for Doubtful Accounts for $15,000 and a credit

to Accounts Receivable for $15,000. It is not considered when deter–

mining the proper amount for the Allowance for Doubtful Accounts.

(c) The year-end bad debt adjustment would decrease before-tax income

$20,000 as computed below: