CHAPTER 16

Dilutive Securities and Earnings Per Share

ASSIGNMENT CLASSIFICATION TABLE (BY TOPIC)

Topics

Questions

Brief

Exercises

Exercises

Problems

Concepts

for Analysis

1.

Convertible debt

and preference

shares.

1, 2, 3, 4,

5, 6, 7

1, 2, 3

1, 2, 3, 4, 5,

6, 7, 25, 26

1

2.

Warrants and debt.

3, 8, 9

4, 5

7, 8, 9,

10, 29

1

1, 3

3.

Share options,

restricted share.

1, 10, 11,

12, 13,

14, 15

6, 7, 8

11, 12, 13,

14, 15

1, 2, 3

2, 4

4.

Earnings Per Share

(EPS)—terminology.

17, 18, 24

15

6

5.

EPS—Determining

potentially dilutive

securities.

19, 20, 21

12, 13, 14

23, 24, 25,

26, 27, 28

5, 7

6.

share method.

22, 23

27, 29

1, 5, 7

7.

EPS—Weighted-

average computation.

16, 17

10, 11

16, 17, 18,

19, 20, 21,

4, 5, 68

8.

objectives.

24, 25

9, 15

5, 6, 7

9.

EPS—

Comprehensive

calculations.

26

20, 21, 22,

23, 24, 25,

27, 28, 29

4, 6, 7, 8

4, 5

10.

shares.

28

Share appreciation

rights.

16

30, 31

ASSIGNMENT CLASSIFICATION TABLE (BY LEARNING OBJECTIVE)

Learning Objectives

Brief

Exercises

Exercises

Problems

Concepts

for

Analysis

1. Describe the accounting for the

issuance, conversion, and retirement

of convertible securities.

1, 2, 3

1, 2, 3, 4,

5, 6, 7, 25, 26

1

1

warrants and for share warrants issued

with other securities.

4, 5

7, 8, 9, 10

1

3

3. Describe the accounting and reporting

for share compensation plans.

6, 7, 8

11, 12,13,

1, 2, 3

1, 2, 3, 4

4. Compute basic earnings per share.

9, 10,

16, 17, 18,

5, 8

5, 6

5. Compute diluted earnings per share.

12, 13, 14

23, 24, 25,

26, 27, 28, 29

4, 6, 7

1, 5, 6, 7

appreciation rights plans.

30, 31

complex situation.

ASSIGNMENT CHARACTERISTICS TABLE

Item

Description

Level of

Difficulty

Time

(minutes)

E16.1

Issuance and repurchase of convertible bonds.

Moderate

10–15

E16.2

Issuance and repurchase of convertible bonds.

Moderate

15–20

E16.3

Issuance and repurchase of convertible bonds.

Moderate

15–20

E16.4

Issuance, conversion, repurchase of convertible bonds.

Moderate

15–20

E16.5

Conversion of bonds.

Simple

15–20

E16.6

Conversion of bonds.

Simple

10–15

E16.7

Issuance and conversion of bonds.

Simple

15–20

E16.8

Issuance of bonds with share warrants.

Simple

10–15

E16.9

Issuance of bonds with share warrants.

Simple

10–15

E16.10

Issuance of bonds with share warrants.

Moderate

15–20

E16.11

Issuance and exercise of share options.

Moderate

15–25

E16.12

Issuance, exercise, and forfeiture of share options.

Moderate

15–25

E16.13

Issuance, exercise, and expiration of share options.

Moderate

15–25

E16.14

Accounting for restricted shares.

Simple

10–15

E16.15

Accounting for restricted shares.

Simple

10–15

E16.16

Weighted-average ordinary shares.

Moderate

15–25

E16.17

EPS: Simple capital structure.

Simple

10–15

E16.18

EPS: Simple capital structure.

Simple

10–15

E16.19

EPS: Simple capital structure.

Simple

10–15

E16.20

EPS: Simple capital structure.

Simple

20–25

E16.21

EPS: Simple capital structure.

Simple

10–15

E16.22

EPS: Simple capital structure.

Simple

10–15

E16.23

EPS with convertible bonds, various situations.

20–25

E16.24

EPS with convertible bonds.

Moderate

15–20

E16.25

EPS with convertible bonds and preference shares.

Moderate

20–25

E16.26

EPS with convertible bonds and preference shares.

Moderate

10–15

E16.27

EPS with options, various situations.

Moderate

20–25

E16.28

EPS with contingent issuance agreement.

Simple

10–15

E16.29

EPS with warrants.

Moderate

15–20

Share-appreciation rights.

Moderate

15–25

Share-appreciation rights.

Moderate

15–25

P16.1

Entries for various dilutive securities.

Moderate

35–40

P16.2

Share-option plan.

Moderate

30–35

P16.3

Share-based compensation.

Moderate

25–30

P16.4

EPS with complex capital structure.

Moderate

30–35

P16.5

Basic EPS: Two-year presentation.

Moderate

30–35

P16.6

Computation of basic and diluted EPS.

Moderate

35–45

P16.7

Computation of basic and diluted EPS.

Moderate

25–35

P16.8

EPS with share dividend and discontinued operations.

30–40

CA16.1

Dilutive securities, EPS.

Moderate

15–20

CA16.2

Ethical issues—compensation plan.

Simple

15–20

Share warrants—various types.

Moderate

15–20

CA16.4

Share compensation plans.

Moderate

25–35

CA16.5

EPS: Preferred dividends, options, and convertible debt.

Moderate

25–35

ANSWERS TO QUESTIONS

1. Securities such as convertible debt or share options are dilutive because their features indicate

2. Corporations issue convertible securities for two reasons. One is to raise equity capital without

giving up more ownership control than necessary. A second reason is to obtain financing at

3. Convertible debt and debt issued with share warrants are similar in that: (1) both allow the issuer

to issue debt at a lower interest cost than would generally be available for straight debt; (2) both

4. The accounting treatment of the €160,000 “sweetener” to induce conversion of the bonds into

ordinary shares represents a departure from IFRS because the IASB views the transaction as the

5. (a) From the point of view of the issuer, the conversion feature of convertible debt results in a

lower cash interest cost than in the case of nonconvertible debt. In addition, the issuer in

planning its long-range financing may view the convertible debt as a means of raising equity

capital over the long term. Thus, if the market value of the underlying shares increases

(b) The purchaser obtains an option to receive either the face amount of the debt upon maturity

or the specified number of shares upon conversion. If the market value of the underlying

shares increases above the conversion price, the purchaser (either through conversion or

Questions Chapter 16 (Continued)

6. The view that separate accounting recognition should be accorded the conversion feature of

convertible debt is based on the premise that there is an economic value inherent in the

conversion feature or call on the ordinary shares and that the value of this feature should be

recognized for accounting purposes by the issuer. It may be argued that the call is not

7. The method used by the company to record the exchange of convertible debentures for ordinary

shares can be supported on the grounds that when the company issued the convertible

debentures, the proceeds could represent consideration received for the shares. Therefore, when

conversion occurs, the book value of the obligation is simply transferred to the shares exchanged

8. Cash ………………………………………………………………………………….. 3,000,000

Bonds Payable ……………………………………………………………… 2,900,000

9. If a corporation decides to issue new shares, the old shareholders generally have the right, referred

to as a share right, to purchase newly issued shares in proportion to their holdings. No entry is

10. Companies are required to use the fair value method to recognize compensation cost. For most

share option plans compensation cost is measured at the grant date and allocated to expense

Questions Chapter 16 (Continued)

11. Cordero would account for the discount as a reduction of the cash proceeds and an increase in

12. The profession recommends that the fair value of a share option be determined on the date on

which the option is granted to a specific individual.

13. IFRS requires that compensation expense be recognized over the service period. Unless

14. Using the fair value approach, total compensation expense is computed based on the fair value

15. The advantages of using restricted shares to compensate employees are: (1) The restricted

16. Weighted-average shares outstanding

Outstanding shares (all year) = ……………………………………….. 400,000

October 1 to December 31 (200,000 X 1/4) = …………………….. 50,000

17. The computation of the weighted-average number of shares requires restatement of the shares

outstanding before the share dividend or split. The additional shares outstanding as a result of a

Questions Chapter 16 (Continued)

18. (a) Basic earnings per share is the amount of earnings for the period available to each

ordinary share outstanding during the reporting period.

(b) A potentially dilutive security is a security which can be exchanged for or converted into

(d) A complex capital structure exists whenever a company’s capital structure includes

dilutive securities.

19. Convertible securities are potentially dilutive securities and part of diluted earnings per share if

20. The concept that a security may be the equivalent of common stock has evolved to meet the

reporting needs of investors in corporations that have issued certain types of convertible securities,

options, and warrants. A potentially dilutive security is a security which is not, in form, common

stock but which enables its holder to obtain common stock upon exercise or conversion. The

21. Convertible securities are considered to be potentially dilutive securities whenever their conversion

22. Under the treasury-share method, diluted earnings per share should be determined as if

outstanding options and warrants were exercised at the beginning of year (or date of issue if

later) and the funds obtained thereby were used to purchase ordinary shares at the average

market price for the period. For example, if a corporation has 10,000 warrants outstanding

Questions Chapter 16 (Continued)

23. Yes, if warrants or options are present, an increase in the market price of the ordinary shares can

increase the number of potentially dilutive ordinary shares by decreasing the number of shares

24. Antidilution is an increase in earnings per share resulting from the assumption that convertible

securities have been converted or that options and warrants have been exercised, or other

shares have been issued upon the fulfillment of certain conditions. For example, an antidilutive

condition would exist when the dividend or interest requirement (net of tax) of a convertible

security exceeds the current EPS multiplied by the number of ordinary shares issuable upon

25. Both basic earnings per share and diluted earnings per share must be presented in a complex

*26. Antidilution when multiple securities are involved is determined by ranking the securities for

maximum possible dilution in terms of per share effect. Starting with the most dilutive, earnings

SOLUTIONS TO BRIEF EXERCISES

BRIEF EXERCISE 16.1

Cash (£4,000,000 X .99) ……………………………………….. 3,960,000

BRIEF EXERCISE 16.2

Share Premium—Conversion Equity …………………… 20,000

BRIEF EXERCISE 16.3

Share Capital—Preference (1,000 X $50) ………………. 50,000

Share Premium—Conversion Equity

BRIEF EXERCISE 16.4

Cash [2,000 X ($1,000 X 1.01)] ……………………………… 2,020,000

BRIEF EXERCISE 16.5

Cash (3,000 X €1,000 X .98) ………………………………….. 2,940,000

BRIEF EXERCISE 16.6

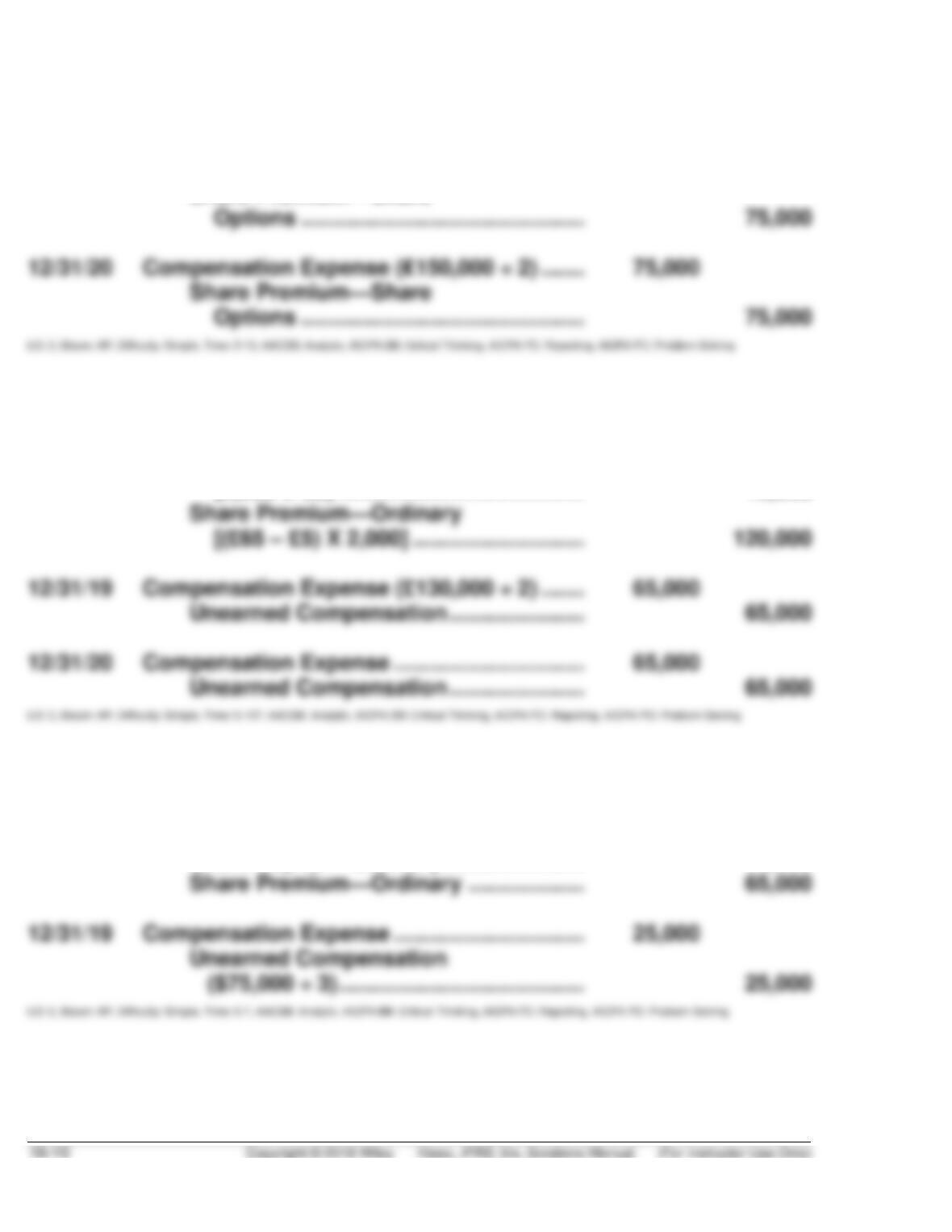

1/1/19 No entry

12/31/19 Compensation Expense (₤150,000 ÷ 2) ……. 75,000

Share Premium—Share

BRIEF EXERCISE 16.7

1/1/19 Unearned Compensation ……………………….. 130,000

Share Capital—Ordinary

(2,000 X £5) …………………………………. 10,000

BRIEF EXERCISE 16.8

1/1/19 Unearned Compensation ……………………….. 75,000

Share Capital—Ordinary ………………….. 10,000

BRIEF EXERCISE 16.9

€1,000,000 – (100,000 X €2)

= €3.20 per share

250,000 shares

LO: 4, Bloom: AP, Difficulty: Simple, Time: 5-7, AACSB: Analytic, AICPA BB: Critical Thinking, AICPA FC: Reporting, AICPA PC: Problem Solving

BRIEF EXERCISE 16.10

Dates

Outstanding

Shares

Outstanding

Fraction

of Year

Weighted

Shares

BRIEF EXERCISE 16.11

(a) (300,000 X 4/12) + (330,000 X 8/12) = 320,000

BRIEF EXERCISE 16.12

Net income ………………………………………………………………………. R$300,000

Adjustment for interest, net of tax [R$64,000 X (1 – .40)] …….. 38,400

BRIEF EXERCISE 16.13

Net income ……………………………………………………………………… €270,000

BRIEF EXERCISE 16.14

Proceeds from assumed exercise of 45,000

options (45,000 X ₺10) ………………………………………………….. ₺450,000

BRIEF EXERCISE 16.15

Earnings per share

Income from continuing operations (€600,000/100,000) ……. € 6.00

*BRIEF EXERCISE 16.16

2019: (5,000 X $4) X 50% = $10,000

SOLUTIONS TO EXERCISES

EXERCISE 16.1 (10–15 minutes)

(a) Present Value of Principal:

(€2,000,000 X .79383) ……………………………………………….. €1,587,660

Present Value of Interest Payments:

(€120,000 X 2.57710) ………………………………………………… 309,252

Present Value of the Liability Component ……………………. €1,896,912

EXERCISE 16.2 (15–20 minutes)

(a) Carrying Value of Bonds, 1-1-19

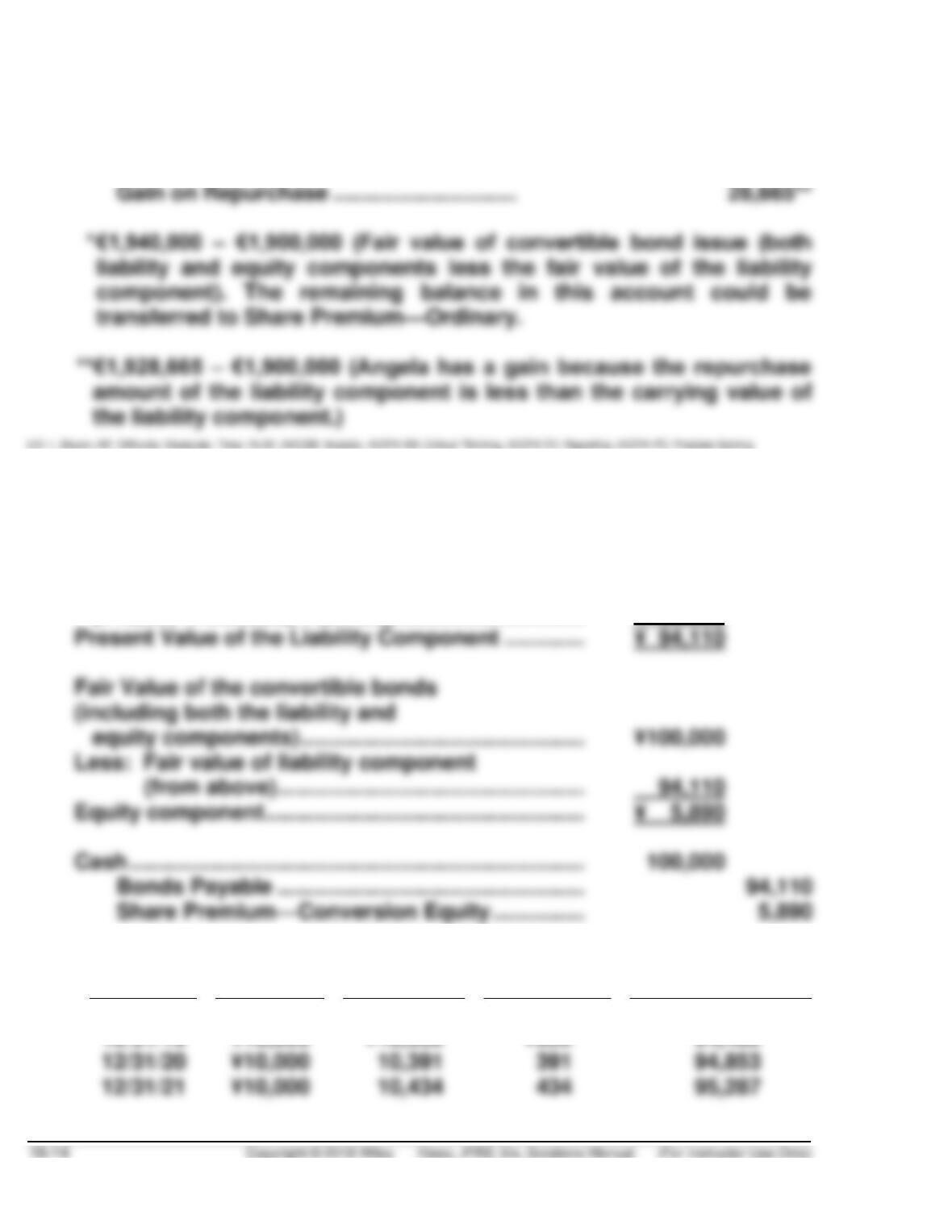

Carrying Value of Bonds, 1-1-20 ………………………………….. €1,928,665

(b) Share Premium—Conversion Equity …………… 103,088

EXERCISE 16.2 (Continued)

(c) Share Premium—Conversion Equity ……….. 40,000*

Bonds Payable ………………………………………. 1,928,665

Cash …………………………..…………………… 1,940,000

EXERCISE 16.3 (15–20 minutes)

(a) Present Value of Principal:

(¥100,000 X .35218(n = 10, i = 11%)) ………………………… ¥ 35,218

Present Value of Interest Payments:

(¥10,000 X 5.88923(n = 10, i = 11%)) ………………………… 58,892

(b)

Date

Cash

Paid

Interest

Expense

Discount

Amortized

Carrying Value

of Bonds

1/1/19

¥94,110

EXERCISE 16.3 (Continued)

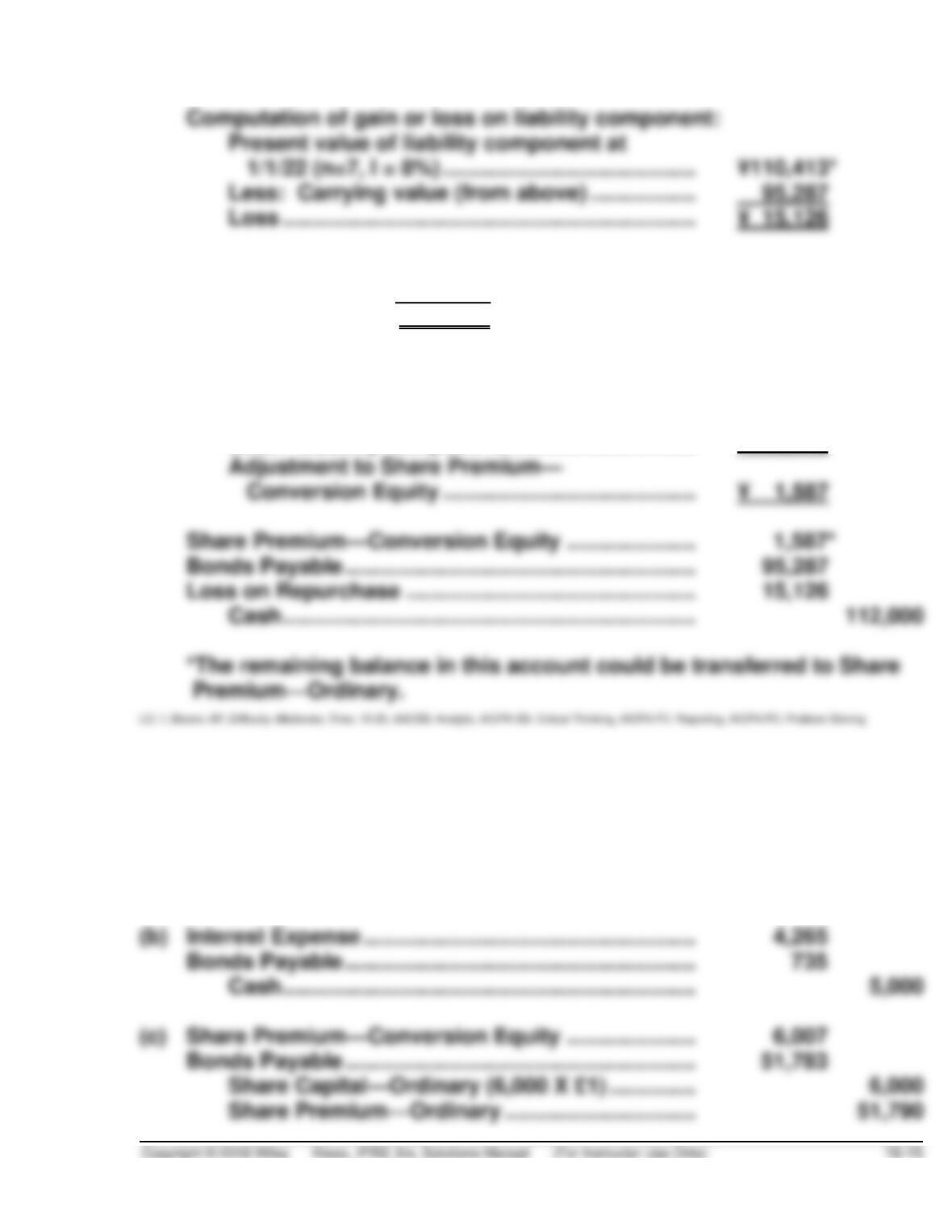

* 10,000 X 5.20637 = ¥ 52,064

100,000 X .58349 = 58,349

¥110,413

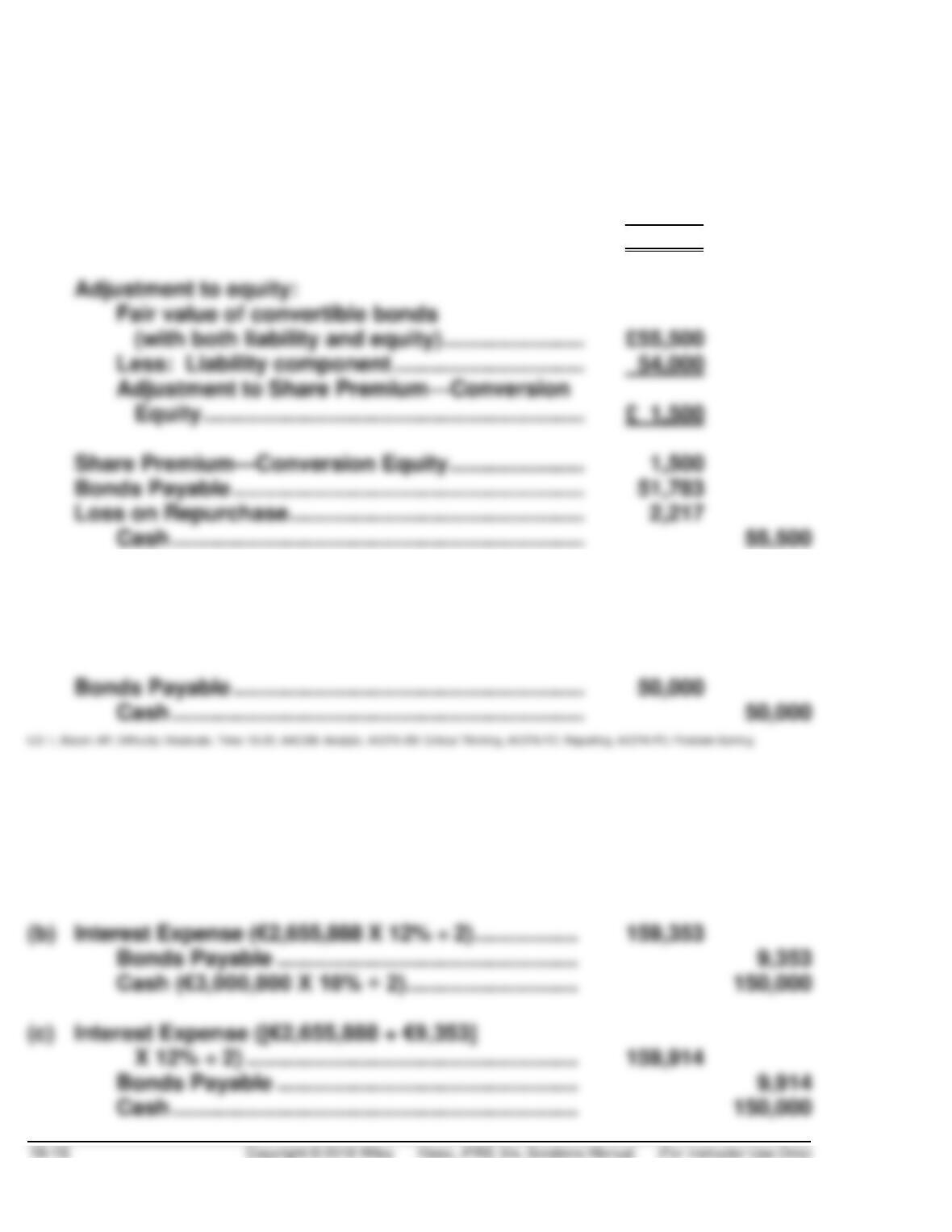

Adjustment to equity:

Fair value of convertible bonds

(with both liability and equity) ………………….. ¥112,000

Less: Liability component …………………………. 110,413

EXERCISE 16.4 (15–20 minutes)

(a) Cash ……………………………………………………………….. 60,000

Bonds Payable ………………………………………….. 53,993

Share Premium—Conversion Equity …………… 6,007

EXERCISE 16.4 (Continued)

(d) Computation of gain or loss:

Present value of liability component

at 12/31/21 ………………………………………………. £54,000

Less: Carrying value (from above) …………….. 51,783

Loss …………………………………………………………. £ 2,217

(e) Interest Expense ……………………………………………… 4,074

Bonds Payable ………………………………………………… 926

Cash …………………………..…………………………….. 5,000

EXERCISE 16.5 (15–20 minutes)

(a) Cash (€3,000,000 X .98) …………………………………… 2,940,000

Bonds Payable …………………………………………. 2,655,888

Share Premium—Conversion Equity ………….. 284,112

EXERCISE 16.5 (Continued)

Share Premium—Conversion Equity

EXERCISE 16.6 (10–15 minutes)

Conversion recorded at book value of the bonds:

EXERCISE 16.7 (15–20 minutes)

1. Cash (€10,000,000 X .99) ……………………………….. 9,900,000

2. Cash (€10,000,000 X .98) ……………………………….. 9,800,000

3. Share Premium—Conversion Equity ……………… 200,000

Conversion Expense …………………………………….. 75,000

EXERCISE 16.8 (10–15 minutes)

(a) Cash …………………………………………………………….. 150,000

EXERCISE 16.9 (10–15 minutes)

TOKACHI GROUP

Journal Entry

September 1, 2019

Cash (¥312,000,000 + ¥6,000,000) ………………………… 318,000,000

Bonds Payable …………………………..…………… 290,000,000

Schedule 1

Value of Share Warrants

Sales price (30,000 X ¥10,400) ………………………………………. ¥312,000,000

Schedule 2

Accrued Bond Interest to Date of Sale

Face value of bonds …………………………………………………….. ¥300,000,000

EXERCISE 16.10 (15–20 minutes)

(a) Cash (€3,000,000 X 1.02) ………………………………. 3,060,000

(b) Cash ……………………………………………………………. 3,060,000

Bonds Payable ………………………………………… 2,940,000

EXERCISE 16.11 (15–25 minutes)

1/2/19 No entry (total compensation cost is $600,000)

12/31/19 Compensation Expense …………………………... 300,000

12/31/20 Compensation Expense ……………………………. 300,000

Share Premium—Share Options …………. 300,000

1/3/21 Cash (30,000 X £40) ………………………………….. 1,200,000

Share Premium—Share Options

EXERCISE 16.11 (Continued)

(Note to instructor: The market price of the shares has no relevance in the

prior entry and the following one.)

5/1/21 Cash (10,000 X £40) ………………………………….. 400,000

EXERCISE 16.12 (15–25 minutes)

1/1/19 No entry (total compensation cost is €400,000)

12/31/19 Compensation Expense ……………………………… 200,000

Share Premium—Share Options ………… 200,000

(€400,000 X 1/2) (To recognize

compensation expense for 2019)

12/31/20 Compensation Expense ……………………………… 170,000

Share Premium—Share Options ………… 170,000

(€400,000 X 1/2 X 17/20) (To recognize

compensation expense for 2020)