PROBLEM 7.4

(a) FORTNER PLC

Analysis of Changes in the

Allowance for Doubtful Accounts

For the Year Ended December 31, 2019

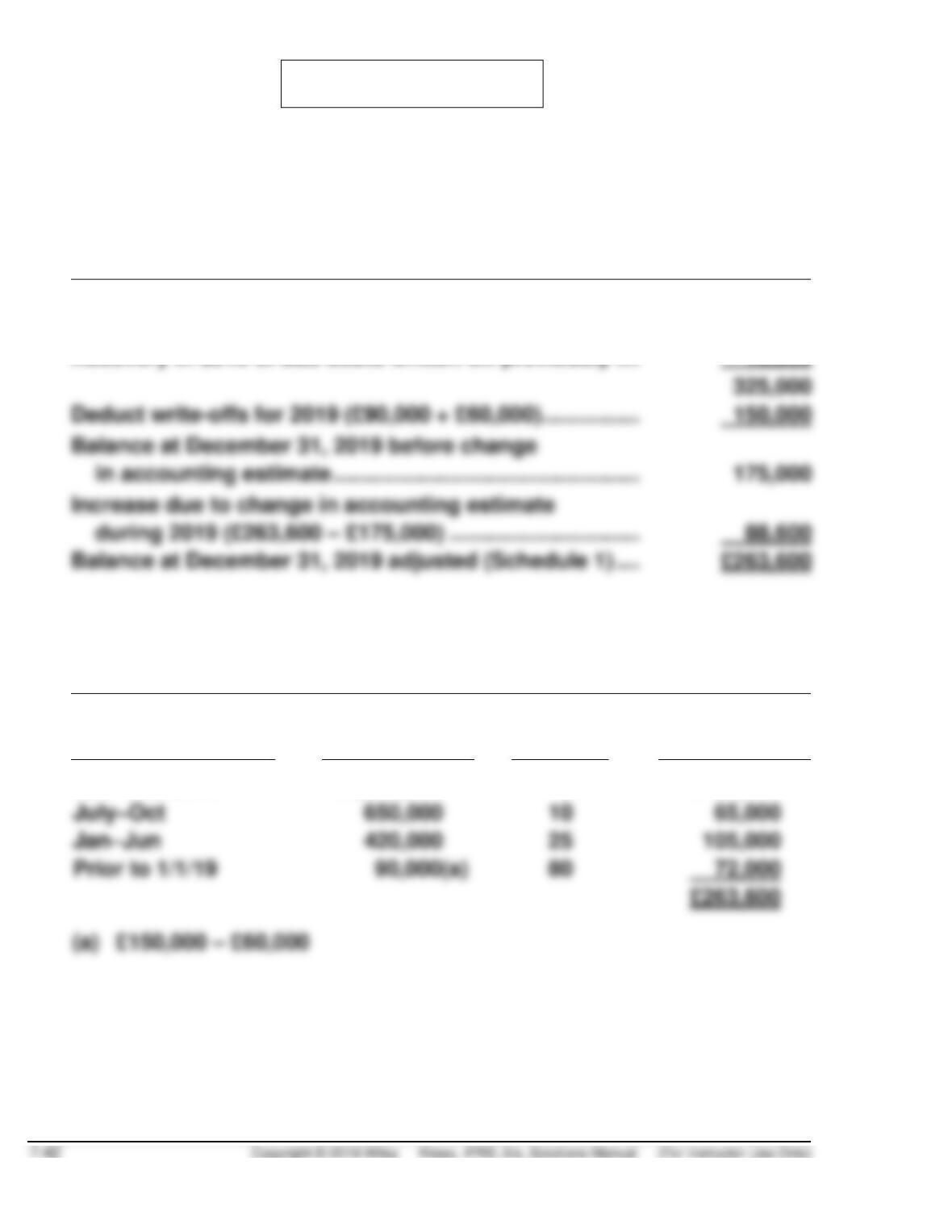

Balance at January 1, 2019 ………………………………………..

£130,000

Provision for doubtful accounts (£9,000,000 X 2%) ……..

180,000

Recovery in 2019 of bad debts written off previously ….

15,000

325,000

in accounting estimate …………………………………………..

during 2019 (£263,600 – £175,000) ………………………….

88,600

Schedule 1

Computation of Allowance for Doubtful Accounts

at December 31, 2019

Aging

Category

Balance

%

Doubtful

Accounts

Nov–Dec 2019

£1,080,000

2

£ 21,600

July–Oct

650,000

65,000

420,000

90,000(a)

72,000

PROBLEM 7.4 (Continued)

(b) The journal entry to record this transaction is as follows:

Bad Debt Expense …………………………………..

88,600

PROBLEM 7.5

Bad Debt Expense …………………………………………….

3,240

Accounts Receivable ………………………………..

3,240

(To correct bad debt expense and

write off accounts receivable)

Accounts Receivable ………………………………………..

4,840

Advance on Sales Contract ……………………….

4,840

Allowance for Doubtful Accounts ………………………

3,700

Accounts Receivable ………………………………..

3,700

(To write off €3,700 of uncollectible

accounts)

Allowance for Doubtful Accounts ………………………

7,279.64

Bad Debt Expense …………………………………….

7,279.64

(To reduce allowance for doubtful

account balance)

Balance (€8,750 + €18,620 – €3,240 – €3,700) ………

Corrected balance (see below) …………………………..

Age

Balance

Aging

Schedule

Under 60 days

€172,342

1%

€ 1,723.42

3%

36,684 (€39,924 – €3,240)

6%

Over 120 days

19,944 (€23,644 – €3,700)

PROBLEM 7.5 (Continued)

If the student did not make the entry to record the €3,700 write-off earlier,

Balance (€8,750 + €18,620 – €3,240)…………….

Corrected balance (see below) ……………………

Age

Balance

Aging

Schedule

Under 60 days

€172,342

1%

€ 1,723.42

3%

6%

Over 120 days

PROBLEM 7.6

–1–

Cash…………………………………………………………………

136,800*

Sales Discounts ………………………………………………..

1,200

Accounts Receivable ………………………………..

138,000

–2–

Accounts Receivable …………………………………………

5,300

Allowance for Doubtful Accounts ………………

Cash…………………………………………………………………

5,300

Accounts Receivable ………………………………..

–3–

Allowance for Doubtful Accounts ………………………

17,500

Accounts Receivable ………………………………..

–4–

Bad Debt Expense …………………………………………….

14,900

Allowance for Doubtful Accounts ………………

R$20,000 – R$5,100 = R$14,900)

PROBLEM 7.7

10/1/19

Notes Receivable ……………………………………………………

120,000

Sales Revenue …………………………..

120,000

12/31/19

Interest Receivable …………………………..

Interest Revenue …………………………..

2,400

*$120,000 X .08 X 3/12 = $2,400

10/1/20

Cash ……………………………………………………….

Interest Receivable …………………………..

2,400

Interest Revenue …………………………..

**$120,000 X .08 X 9/12 = $7,200

12/31/20

Interest Receivable …………………………..

2,400

Interest Revenue ………………………….

2,400

10/1/21

Cash ……………………………………………………….

9,600

Interest Receivable …………………………..

2,400

Interest Revenue …………………………

7,200

Cash ……………………………………………………….

120,000

Notes Receivable …………………………..

120,000

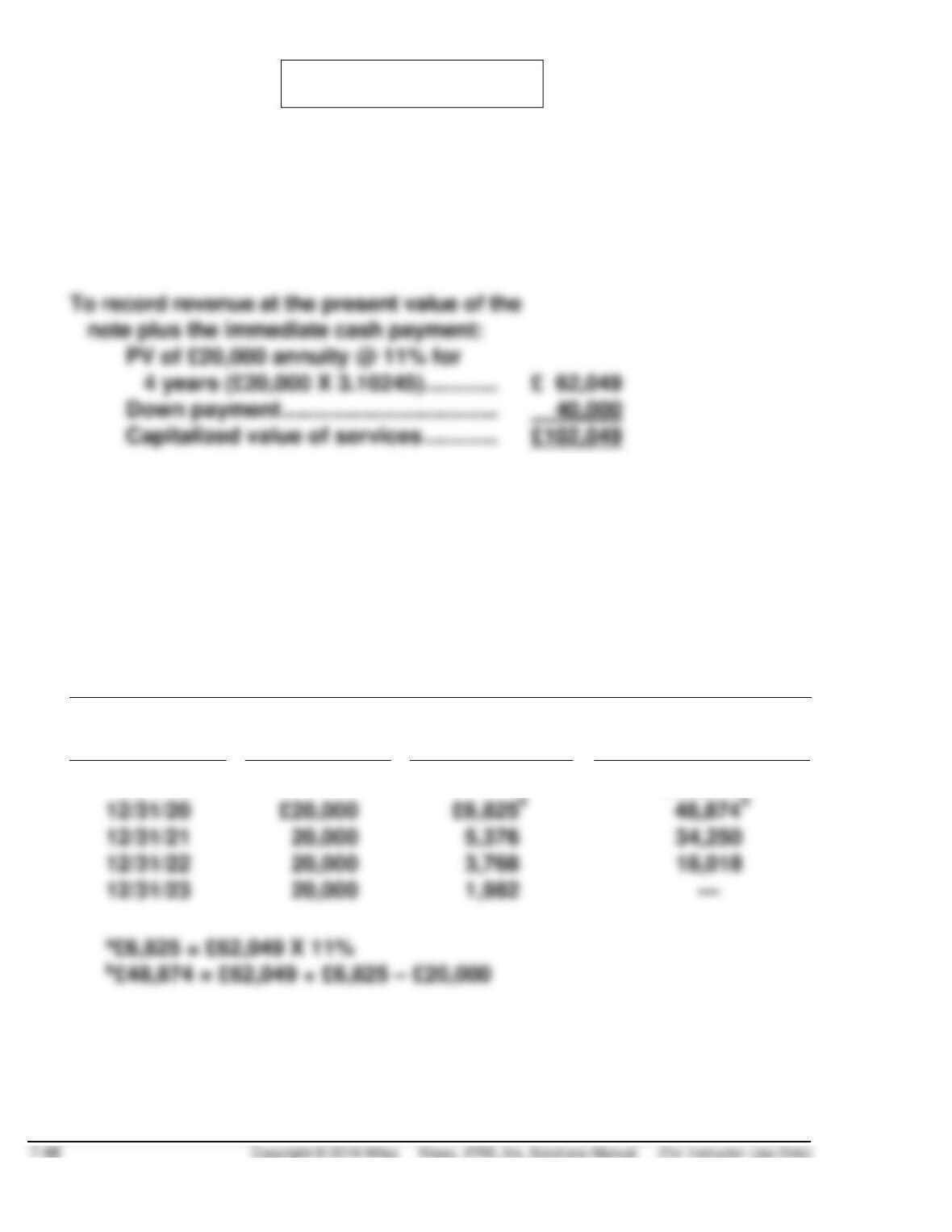

PROBLEM 7.8

(a)

December 31, 2019

Cash……………………………………………………………….

40,000

Notes Receivable …………………………………………….

62,049

Service Revenue …………………………..…………

102,049

Down payment ……………………………..

(b)

December 31, 2020

Cash………………………………………………………………….

20,000

Notes Receivable ……………………………………….

20,000

Notes Receivable ……………………………………………….

6,825

Interest Revenue ………………………………………..

6,825

Schedule of Note Discount Amortization

Date

Cash

Received

Interest

Revenue

Carrying Amount

of Note

12/31/19

—

—

£62,049

£20,000

PROBLEM 7.8 (Continued)

(c)

December 31, 2021

Cash …………………………………………………..

20,000

Notes Receivable …………………………

20,000

Notes Receivable …………………………………

Interest Revenue …………………………

(d)

December 31, 2022

Cash …………………………………………………..

20,000

Notes Receivable …………………………

20,000

Notes Receivable …………………………………

Interest Revenue …………………………

(e)

December 31, 2023

Cash …………………………………………………..

20,000

Notes Receivable …………………………

20,000

Notes Receivable …………………………………

Interest Revenue …………………………

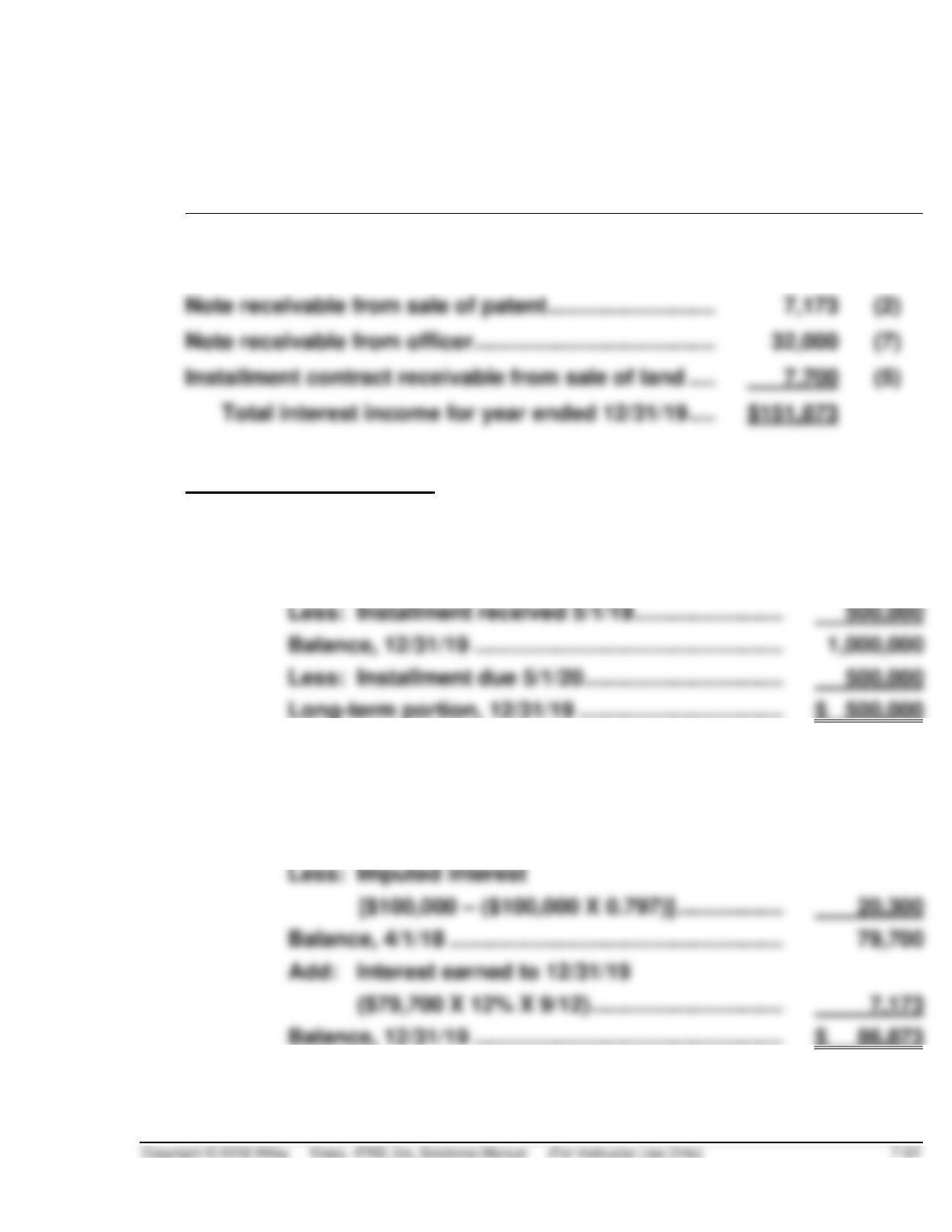

PROBLEM 7.9

(a) BRADDOCK INC.

Long-Term Receivables Section of Statement of Financial Position

December 31, 2019

9% note receivable from sale of division, due

in annual installments of $500,000 to

May 1, 2021, less current installment ……………..

$ 500,000

(1)

8% note receivable from officer, due Dec. 31,

2021, collateralized by 10,000 shares

of Braddock, Inc., common stock

with a fair value of $450,000…………………………..

Zero-interest-bearing note from sale of patent,

net of 12% imputed interest, due April 1,

2021 …………………………………………………………….

(2)

Installment contract receivable, due in annual

installments of $45,125 to July 1, 2023,

less current installment ………………………………..

110,275

(3)

Total long-term receivables ………………………..

$1,097,148

(b) BRADDOCK INC.

Partial Statement of Financial Position Balances

December 31, 2019

Current portion of long-term receivables:

Note receivable from sale of division …………………………

$500,000

(1)

receivables ……………………………………………………..

Accrued interest receivable:

Note receivable from sale of division …………………………

(4)

Installment contract receivable …………………………..

(5)

PROBLEM 7.9 (Continued)

(c) BRADDOCK INC.

Interest Revenue from Long-Term Receivables

For the Year Ended December 31, 2019

Interest income:

Note receivable from sale of division …………………………

$105,000

(6)

Note receivable from sale of patent …………………………..

(2)

Installment contract receivable from sale of land ……….

7,700

(5)

Total interest income for year ended 12/31/19 ……….

$151,873

Explanation of Amounts

(1)

Long-term Portion of 9% Note Receivable at 12/31/19

Face amount, 5/1/18 ………………………………………..

$1,500,000

Less: Installment received 5/1/19 …………………….

500,000

Balance, 12/31/19 ……………………………………………

Less: Installment due 5/1/20 …………………………...

500,000

Long-term portion, 12/31/19 …………………………….

$ 500,000

(2)

Zero-interest-bearing Note, Net of Imputed Interest

at 12/31/19

Face amount 4/1/19 …………………………………………

$ 100,000

Less: Imputed interest

[$100,000 – ($100,000 X 0.797)] ………………

20,300

Balance, 4/1/18 ……………………………………………….

Add: Interest earned to 12/31/19

($79,700 X 12% X 9/12) …………………………..

7,173

PROBLEM 7.9 (Continued)

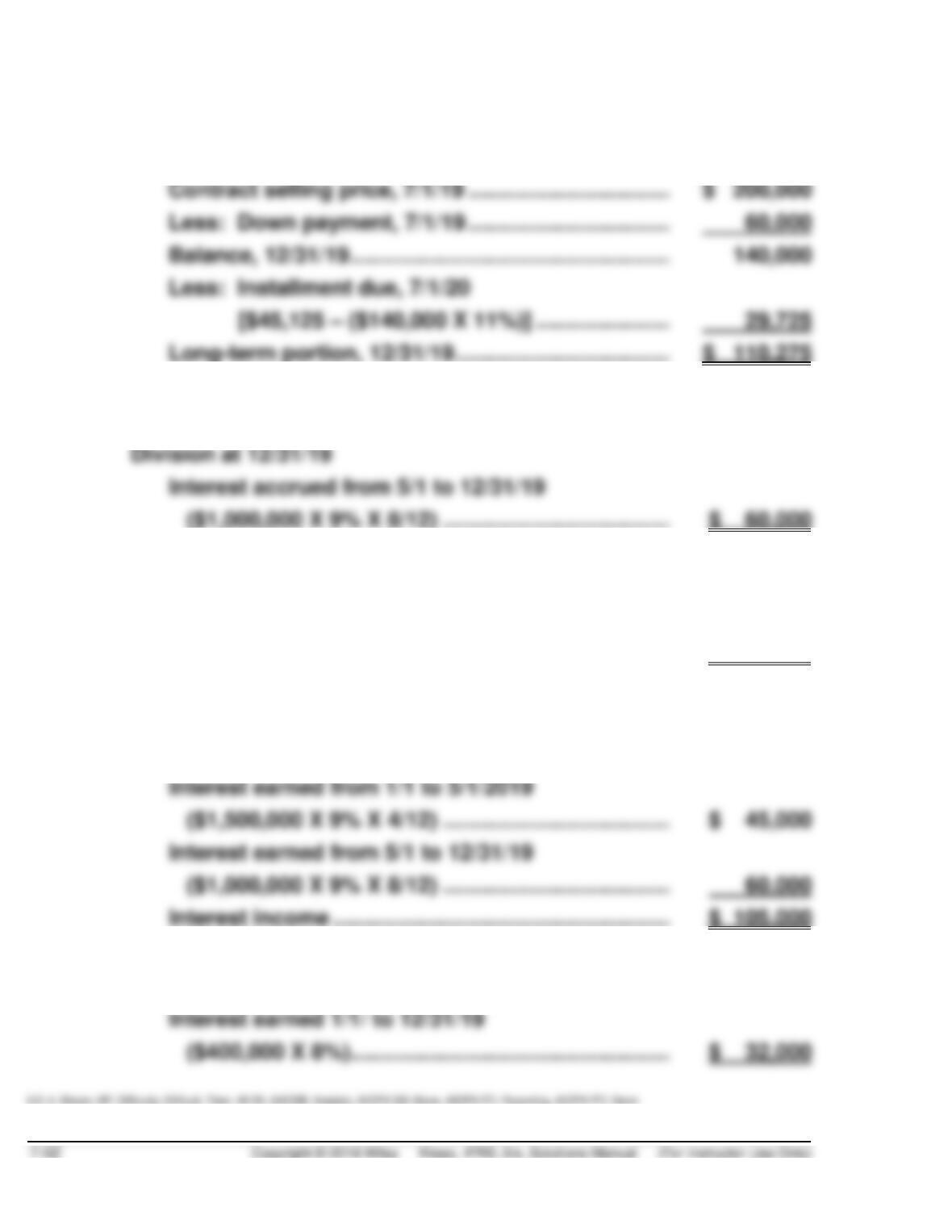

(3)

Long-term Portion of Installment Contract

Receivable at 12/31/19

Contract selling price, 7/1/19 …………………………...

Less: Down payment, 7/1/19 …………………………...

Balance, 12/31/19 …………………………..………………..

Less: Installment due, 7/1/20

[$45,125 – ($140,000 X 11%)] ………………….

(4)

Accrued Interest—Note Receivable, Sale of

Division at 12/31/19

Interest accrued from 5/1 to 12/31/19

(5)

Accrued Interest—Installment Contract at 12/31/19

Interest accrued from 7/1 to 12/31/19

($140,000 X 11% X 1/2) ………………………………….

$ 7,700

(6)

Interest Revenue—Note Receivable, Sale of

Division, for 2019

Interest earned from 1/1 to 5/1/2019

($1,500,000 X 9% X 4/12) ……………………………….

Interest earned from 5/1 to 12/31/19

($1,000,000 X 9% X 8/12) ……………………………….

(7)

Interest Revenue—Note Receivable, Officer, for 2019

Interest earned 1/1/ to 12/31/19

PROBLEM 7.10

(000’s omitted)

July 1, 2019

Cash ……………………………………………………………………….

119,250

Finance Charge (.005 X ¥150,000) ……………………………..

750

Notes Payable (80% X ¥150,000) ……………………….

120,000

Notes Payable ………………………………………………………….

Accounts Receivable ……………………………………….

80,000

Finance Charge ……………………………………………………….

350

Finance Charge Payable (.005 X ¥70,000) ………….

August 31, 2019

Notes Payable ………………………………………………………….

40,000

Cash* ………………………………………………………………………

9,550

Finance Charge (.005 X [¥150,000 –

¥80,000 – ¥50,000]) ………………………………………………..

100

Finance Charge Payable …………………………..………………

350

Accounts Receivable ……………………………………….

50,000

*Total cash collection …………………………..…………………

Less: Finance charge payable (from previous entry) …

350

Finance charge (current month) [(.005 X

(¥150,000 – ¥80,000 – ¥50,000)] ……………………..

100

Note payable (balance) (¥120,000 – ¥80,000)…….

PROBLEM 7.11

SANDBURG COMPANY

Income Statement Effects

For the Year Ended December 31, 2019

Expenses resulting from accounts receivable

assigned (Schedule 1) …………………………………………..

€22,320

Total expenses …………………………..………………………

€52,320

Schedule 1

Computation of Expense

for Accounts Receivable Assigned

Assignment expense:

Accounts receivable assigned …………………………..

€400,000

Advance by Keller Finance Company …………………..

Interest expense ………………………………………………………

Total expenses …………………………………………………..

€22,320

*PROBLEM 7.12

(a)

Petty Cash ……………………………………………………….

250.00

Cash ………………………………………………………….

250.00

Postage Expense ……………………………………………….

33.00

Supplies …………………………………………………………….

65.00

Accounts Receivable—Employees ………………………

30.00

Shipping Expense …………………………..………………….

57.45

Advertising Expense ………………………………………….

22.80

Miscellaneous Expense ………………………………………

15.35

Cash (£250.00 – £26.40) ………………………………

223.60

Petty Cash ……………………………………………………….

50.00

Cash ………………………………………………………….

(b)

Balance per bank: ………………………………………………

£6,522

Add:

Cash on hand …………………………………………….

£ 246

Deposit in transit ……………………………………….

3,000

3,246

Deduct: Checks outstanding……………………………….

850

Balance per books: …………………………………………….

Add: Note receivable (collected with interest) ……..

930

Deduct: Bank Service Charges …………………………..

27

*(£8,850 + £31,000 – £31,835)

Cash …………………………..……………………………………..

Notes Receivable ……………………………………….

Interest Revenue ………………………………………..

Office Expense (Bank Charges) …………………………..

Cash ………………………………………………………….

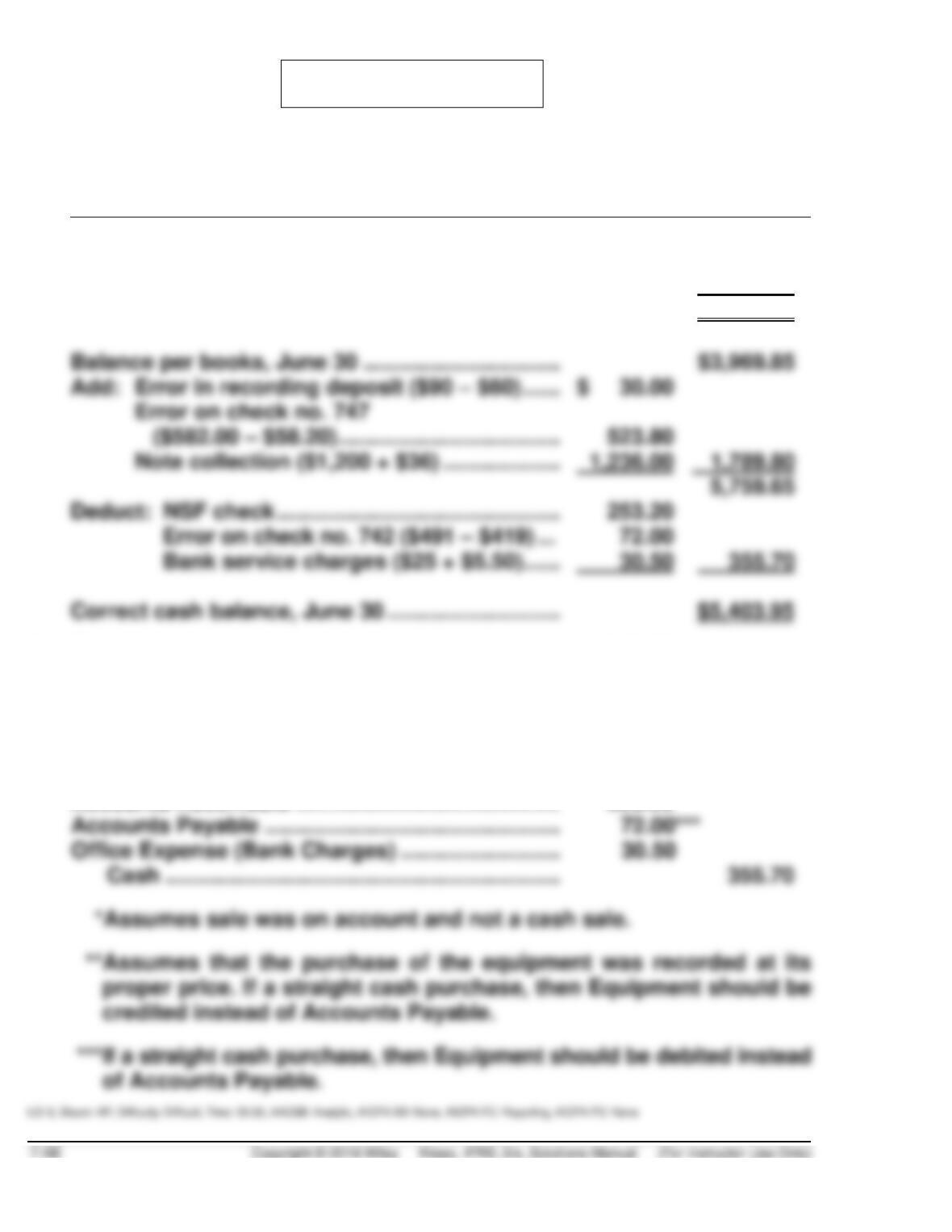

*PROBLEM 7.13

(a) AGUILAR CO.

Bank Reconciliation

June 30, 2019

Balance per bank, June 30 ………………………………………..

$4,150.00

Add: Deposits in transit …………………………………………..

3,390.00

Deduct: Outstanding checks …………………………..

2,136.05

Correct cash balance, June 30 …………………………..

$5,403.95

Balance per books, June 30 …………………………..

$3,969.85

Add: Error in recording deposit ($90 – $60) ………………

Error on check no. 747

($582.00 – $58.20) …………………………………………

523.80

Note collection ($1,200 + $36) ………………………….

Deduct: NSF check ………………………………………………….

253.20

Error on check no. 742 ($491 – $419) …

Bank service charges ($25 + $5.50) ………………

Correct cash balance, June 30 …………………………..

$5,403.95

(b) Cash ………………………………………………………………

1,789.80

Accounts Receivable ………………………………….

30.00*

Accounts Payable ………………………………………

523.80**

Notes Receivable ……………………………………….

1,200.00

Interest Revenue ………………………………………..

36.00

Accounts Receivable ………………………………………

253.20

Accounts Payable …………………………………………..

Office Expense (Bank Charges) ……………………….

Cash ……………………………………………………….

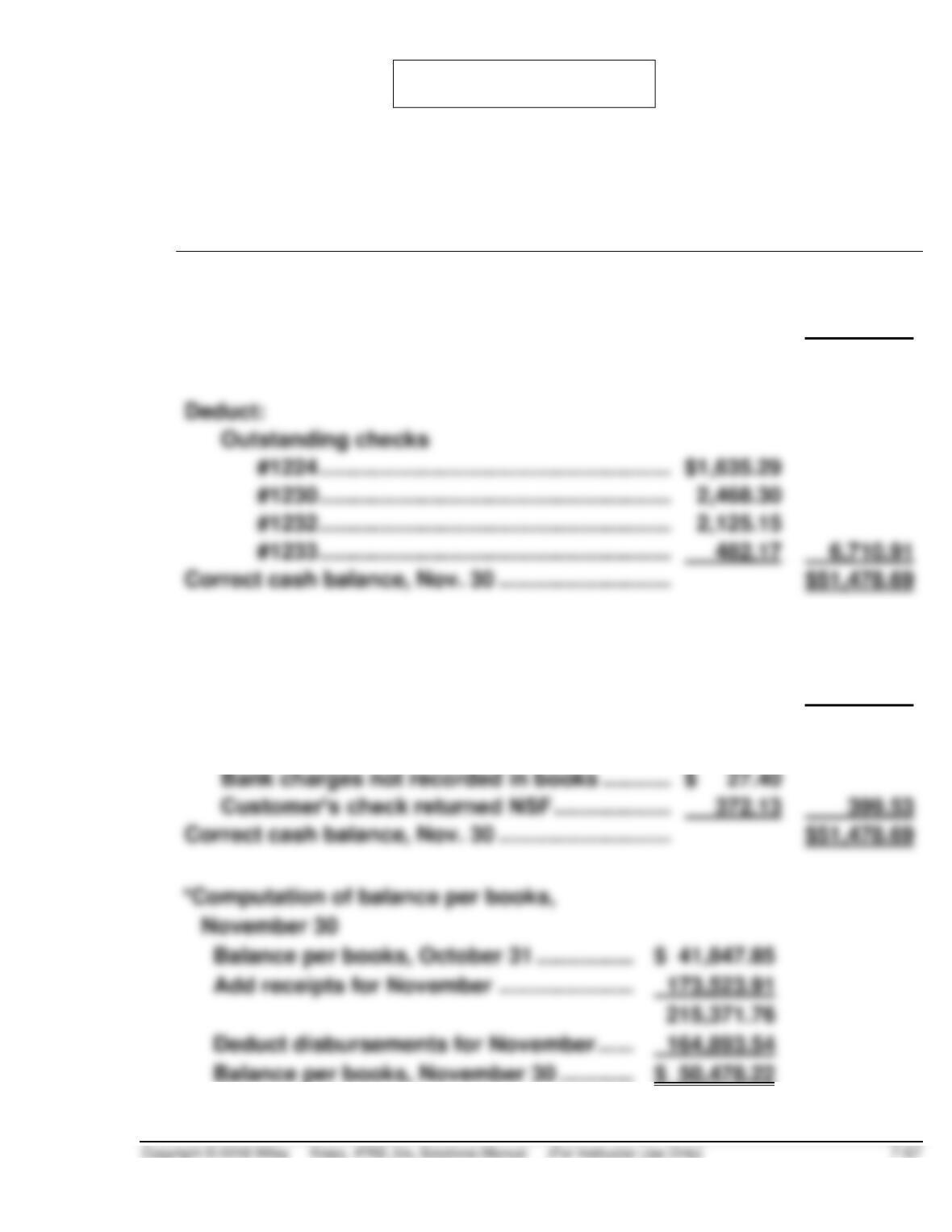

*PROBLEM 7.14

(a) HASELHOF INC.

Bank Reconciliation

November 30

Balance per bank statement, November 30 ………………

$56,274.20

Add:

Cash on hand, not deposited …………………………..

1,915.40

58,189.60

Deduct:

Outstanding checks

#1224 ……………………………………………………….

#1230 ……………………………………………………….

#1232 ……………………………………………………….

#1233 ……………………………………………………….

6,710.91

Balance per books, November 30 …………………………..

$50,478.22*

Add:

Bond interest collected by bank …………………………

1,400.00

51,878.22

Deduct:

Bank charges not recorded in books ………………….

Customer’s check returned NSF …………………………

399.53

*PROBLEM 7.14 (Continued)

(b)

November 30

Cash…………………………………………………………

1,400.00

Interest Revenue ……………………………….

1,400.00

November 30

Office Expense (Bank Charges) …………………

Cash ………………………………………………..

November 30

Accounts Receivable …………………………………

Cash ………………………………………………..

TIME AND PURPOSE OF CONCEPTS FOR ANALYSIS

CA 7.1 (Time 10–15 minutes)

CA 7.2 (Time 15–20 minutes)

Purpose—to provide the student with the opportunity to discuss the accounting for cash discounts,

trade discounts, and the factoring of accounts receivable.

CA 7.3 (Time 25–30 minutes)

Purpose—to provide the student with the opportunity to discuss the advantages and disadvantages of

CA 7.4 (Time 25–30 minutes)

Purpose—to provide the student the opportunity to discuss when interest revenue from a note receivable

CA 7.5 (Time 25–30 minutes)

CA 7.6 (Time 20–25 minutes)

Purpose—to provide the student with a discussion problem related to notes receivable sold without and

with recourse.

CA 7.7 (Time 20–30 minutes)

CA 7.8 (Time 25–30 minutes)

Purpose—to provide the student the opportunity to calculate interest revenue on an interest-bearing

CA 7.9 (Time 25–30 minutes)

Purpose—to provide the student with a case related to the imputation of interest. One company has

CA 7.10 (Time 25–30 minutes)

Purpose—to provide the student with a case to analyze receivables irregularities, including a shortage.

This is a good writing assignment.

CA 7.11 (Time 25–30 minutes)

SOLUTIONS TO CONCEPTS FOR ANALYSIS

CA 7.1

(a) The direct write-off method overstates the trade accounts receivable on the statement of financial

position by reporting them at more than their cash realizable value. Furthermore, because the

write-off often occurs in a period after the revenues were generated, the direct write-off method

does not match bad debts expense with the revenues generated by sales in the same period.

CA 7.2

(a) (1) Kimmel should account for the sales discounts at the date of sale using the net method by

recording accounts receivable and sales revenue at the amount of sales less the sales

discounts available.

(b) Trade discounts are neither recorded in the accounts nor reported in the financial statements.

Therefore, the amount recorded as sales revenues and accounts receivable is net of trade

discounts and represents the cash-equivalent price of the asset sold.

(c) To account for the accounts receivable factored on August 1, 2019, Kimmel should decrease