BRIEF EXERCISE 18.13 (continued)

October 11, 2019

Sales Returns and Allowances………………………….. 78,000

Accounts Receivable …………………………………. 78,000

Returned Inventory ………………………………………….. 62,400

Cost of Goods Sold

Accounts Receivable ……………………………………….. 700,000

Allowance for Sales Returns and

Allowances (.15 X $700,000) ………………. 105,000

Sales Revenue ………………………………………….. 595,000

October 11, 2019

BRIEF EXERCISE 18.13 (continued)

October 31, 2019

Inventory ($84,000 − $62,400) …………………………... 21,600

Estimated Inventory Returns …………………….. 21,600

BRIEF EXERCISE 18.14

Kristin would recognize in its financial statements the following:

(a) Net sales of $5,800 comprised of sales, $6,000 ($20 X 300) less

sales returns and allowances of $200 ($20 X 10).

BRIEF EXERCISE 18.15

When to recognize revenue in a bill-and-hold arrangement depends on the

circumstances. Mills determines when it has satisfied its performance

obligation to transfer a product by evaluating when ShopBarb obtains

control of that product. For ShopBarb to have obtained control of a product

in a bill-and-hold arrangement, all of the following criteria should be met:

(a) The reason for the bill-and-hold arrangement must be substantive.

June 1, 2019

Accounts Receivable ……………………………………….. 200,000

Sales Revenue ………………………………………….. 200,000

Mills makes the following entry to record the cash received.

September 1, 2019

Cash ……………………………………………………………….. 200,000

Accounts Receivable …………………………………. 200,000

BRIEF EXERCISE 18.16

Accounts Payable (ShipAway Cruise Lines) ……………… 70,000

BRIEF EXERCISE 18.17

Cash ………………………………………………………………………. 18,850*

Advertising Expense ……………………………………………….. 500

BRIEF EXERCISE 18.18

Amounts Reported in Income

Sales revenue …………………………………………………. $1,000,000

Warranty expense……………………………………………. 40,000

Amounts Reported on the Statement of Financial Position

BRIEF EXERCISE 18.18 (continued)

The company recognizes revenue related to the service type warranty over

the two-year period that extends beyond the assurance warranty period

BRIEF EXERCISE 18.19

No entry is required on May 1, 2019 because neither party has performed

on the contract. On June 15, 2019, Eric agreed to pay the full price and

therefore Mount has an unconditional right to those funds on that date.

On receiving the cash on June 15, 2019, Mount records the following entry.

June 15, 2019

Cash ……………………………………………………………….. 25,000

BRIEF EXERCISE 18.20

The initiation fee may be viewed as separate performance obligation

because it provides a renewal option at a lower price than normally

BRIEF EXERCISE 18.21

In evaluating how to account for the modification, Stengel Co. concludes

that the remaining services to be provided are distinct from the services

transferred on or before the date of the contract modification. In addition,

*BRIEF EXERCISE 18.22

Construction in Process …………………………………… 1,700,000

Materials, Cash, Payables. …………………………. 1,700,000

Accounts Receivable ……………………………………….. 1,200,000

Billings on Construction in Process …………… 1,200,000

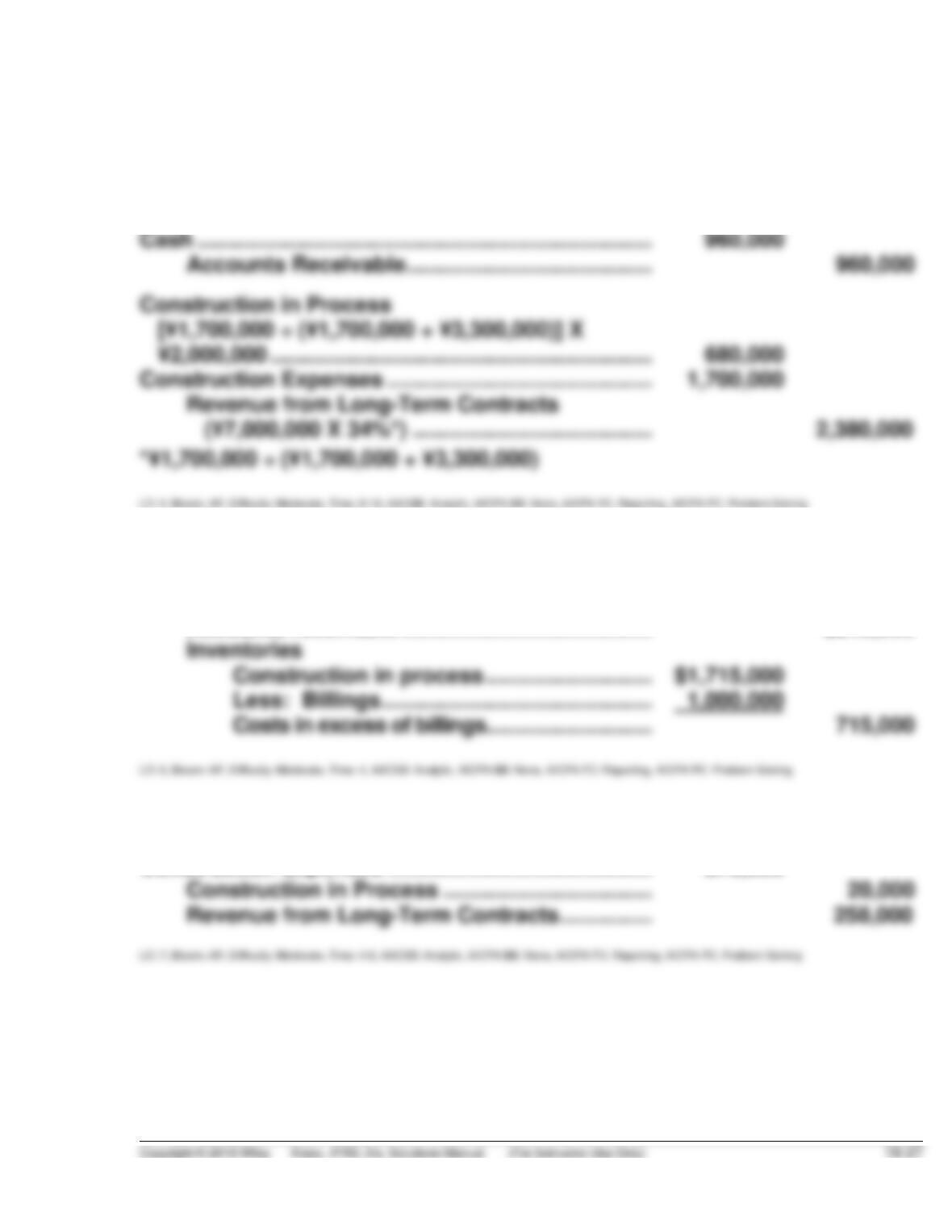

*BRIEF EXERCISE 18.23

Current Assets

Accounts receivable ………………………………….. $240,000

*BRIEF EXERCISE 18.24

Construction Expenses ……………………………………. 278,000

*BRIEF EXERCISE 18.25

April 1, 2019

Cash ………………………………………………………………. 25,000

Notes Receivable ($75,000 – $25,000 – $8,598) …… 41,402

July 1, 2019

Unearned Service Revenue (Training) ………………. 2,000

SOLUTIONS TO EXERCISES

EXERCISE 18.1 (10–15 minutes)

(1) Kawaski is in the business of buying and selling both new and used

Jeeps and this activity should be considered part of its ordinary

(2) This statement is not correct. In the new standard, indicators that

control has passed to the customer include having (1) a present

obligation to pay, (2) physical possession, (3) legal title, (4) risks and

rewards of ownership, and (5) acceptance of the asset.

(4) This statement is not correct. For a valid contract to exist, the

collection of revenue must be probable.

(5) The distinction between revenue and gains is important because it is

useful to understand how these increases in net income occurred.

EXERCISE 18.2 (10–15 minutes)

(1) A wholly unperformed contract is not recorded until one or both of the

parties have performed. The new revenue standard uses the asset

EXERCISE 18.2 (continued)

(3) Elaina should account for this additional option. Whether the option

provides for free goods or goods at a discount, the option is a

(4) Under the new standard, the collectability criterion is designed to

prevent companies from applying the revenue model to problematic

EXERCISE 18.3 (10–15 minutes)

(a) May 1, 2019

No entry – neither party has performed on May 1, 2019.

(b) May 15, 2019

(c) May 31, 2019

Unearned Sales Revenue ………………………………….. 900

EXERCISE 18.4 (20–25 minutes)

(a) The journal entry to record the sale and related cost of goods sold are

as follows:

January 2, 2019

Notes Receivable …………………………………….. 600,000

Sales Revenue ($610,000 − $10,000) … 600,000

(b) January 2, 2019

Notes Receivable …………………………………….. 610,000

Sales Revenue ……………………………….. 610,000

Note that the time value of money is not considered because the

contract is less than a year. Also, if payment occurs within 5 days,

under the net method, the entry would be:

EXERCISE 18.4 (continued)

If payment occurs within 5 days, under the gross method, the entry

would be

EXERCISE 18.5 (20–25 Minutes)

(a) The transaction price for this contract should be computed as follow:

Contract price $200,000

(b) The transaction price for this contract should be computed as follow:

Contract price $200,000

Expected value of the bonus 39,000

NOTE TO INSTRUCTOR: Given just two outcomes, the company could

determine the bonus component of the transaction price based on the most

likely outcome ($40,000). If reliable, use of probability outcomes is more

accurate.

EXERCISE 18.6 (20-25 minutes)

The transaction price that Real Estate Inc. should record is $3,000,000. At

this point, it appears that it will be difficult for Real Estate Inc. to argue that

EXERCISE 18.7 (15–20 minutes)

(a) Because the arrangement only has two possible outcomes (regulatory

approval is achieved or not), Blair determines the transaction price

(b) December 20, 2019

Accounts Receivable ……………………………….. 10,000,000

EXERCISE 18.8 (15–20 minutes)

(a) Aaron determines that the transaction price for the 100 policies is

$14,500 [($100 X 100) + ($10 X 4.5 X 100)].

(b) Aaron will recognize revenue of $3,222 ($14,500 X 12/54), because on

EXERCISE 18.9 (20–25 minutes)

(a) December 31, 2019

December 31, 2020

Unearned Rent Revenue …………………………... 240,000

Rent Revenue …………………………………… 240,000

EXERCISE 18.9 (continued)

(b) The marina operator should recognize that advance rentals generated

$190,400 ($152,000 + $38,400) of cash in exchange for the marina’s

promise to deliver future services. In effect, this has reduced future

EXERCISE 18.10 (25–30 minutes)

July 1, 2019

No entry – neither party has performed under the contract.

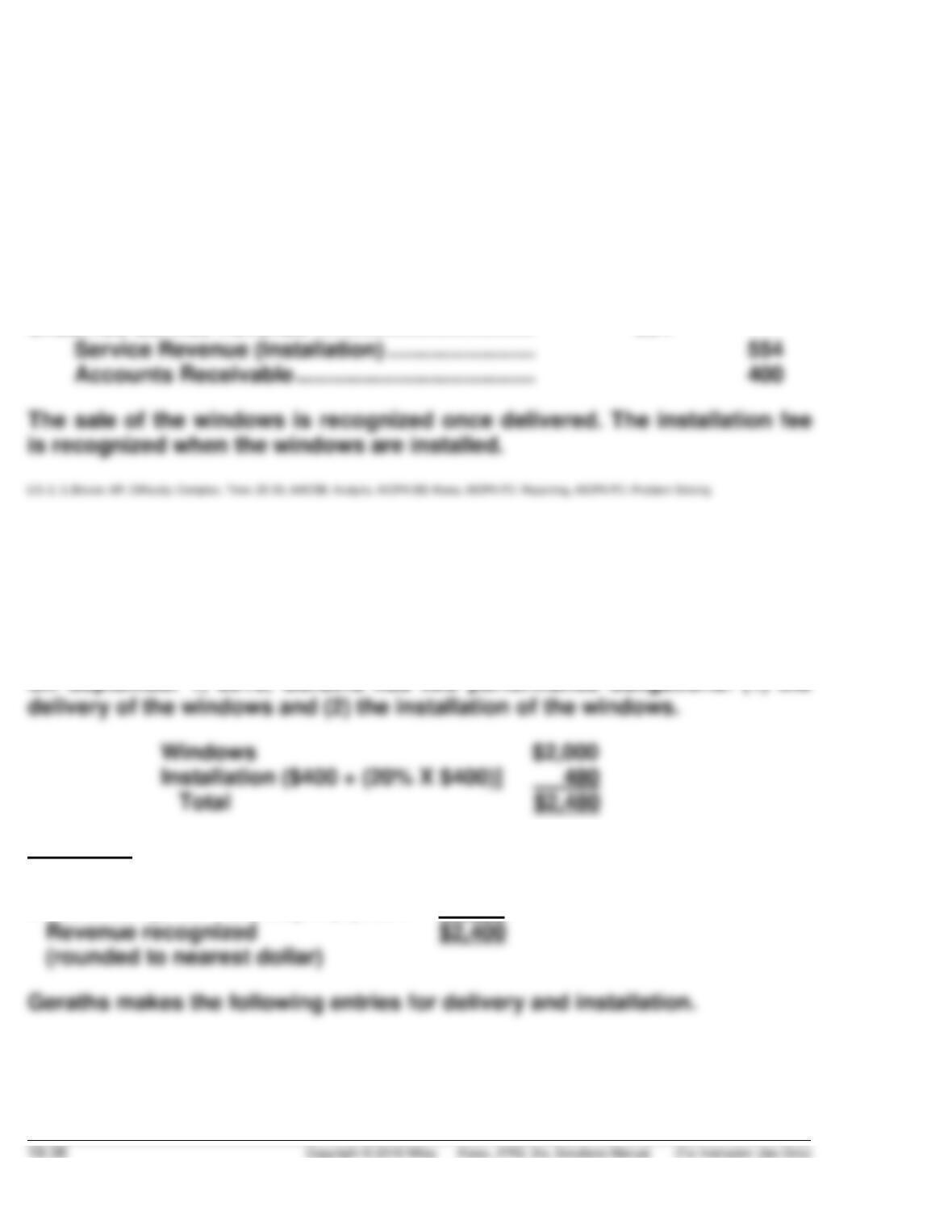

On September 1, 2019, Geraths has two performance obligations: (1) the

delivery of the windows and (2) the installation of the windows.

Windows $2,000

Installation 600

Total $2,600

Allocation

Geraths makes the following entries for delivery and installation.

September 1, 2019

EXERCISE 18.10 (continued)

Cost of Goods Sold …………………………………………. 1,100

Inventory …………………………………………………. 1,100

(Windows delivered, performance obligation for installation recorded)

October 15, 2019

Cash ………………………………………………………………. 400

Unearned Service Revenue ……………………………… 554

EXERCISE 18.11 (20–25 minutes)

(a) July 1, 2019

No entry – neither party has performed under the contract.

Allocation

Windows ($2,000 ÷ $2,480) X $2,400 = $1,935

Installation ($480 ÷ $2,480) X $2,400 = 465

EXERCISE 18.11 (continued)

September 1, 2019

Cash ……………………………………………………………….. 2,000

Accounts Receivable ……………………………………….. 400

October 15, 2019

Cash ……………………………………………………………….. 400

Unearned Service Revenue ………………………………. 465

(b) If Geraths cannot estimate the costs for installation, then the residual

approach is used. In this approach, the total fair value of the contract

Geraths makes the following entries for delivery and installation.

September 1, 2019

Cash ……………………………………………………………….. 2,000

Accounts Receivable ……………………………………….. 400

EXERCISE 18.11 (continued)

October 15, 2019

Cash ………………………………………………………………. 400

EXERCISE 18.12 (10–15 minutes)

(a) The entry to record the sale and related cost of goods sold is as

follows.

January 2, 2019

Accounts Receivable ………………………………. 410,000

(b) First Quarter

Sales revenue …………………………………………. £370,000

EXERCISE 18.13 (25–30 minutes)

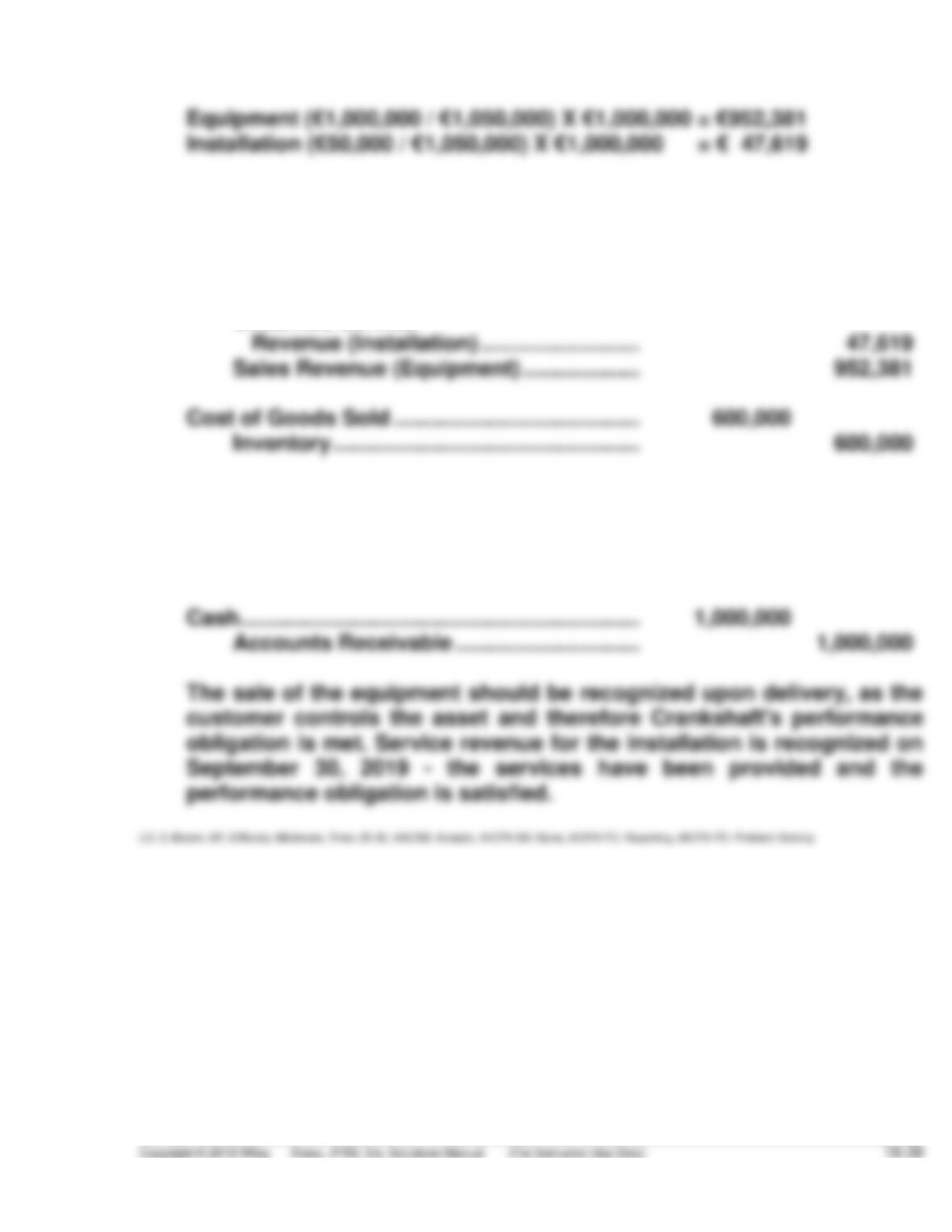

(a) The total revenue of €1,000,000 should be allocated to the two

EXERCISE 18.13 (continued)

(b) Crankshaft makes the following entries.

June 1, 2019

Accounts Receivable ……………………………….. 1,000,000

Unearned Service

September 30, 2019

Unearned Service Revenue ………………………. 47,619

Service Revenue (Installation) …………… 47,619

EXERCISE 18.14 (25–30 minutes)

(a) The total revenue of €1,000,000 should be allocated to the two

performance obligations based on their standalone selling prices. In

(b) Crankshaft makes the following entries.

June 1, 2019

Accounts Receivable ………………………………. 1,000,000

September 30, 2019

Unearned Service Revenue ……………………… 43,062