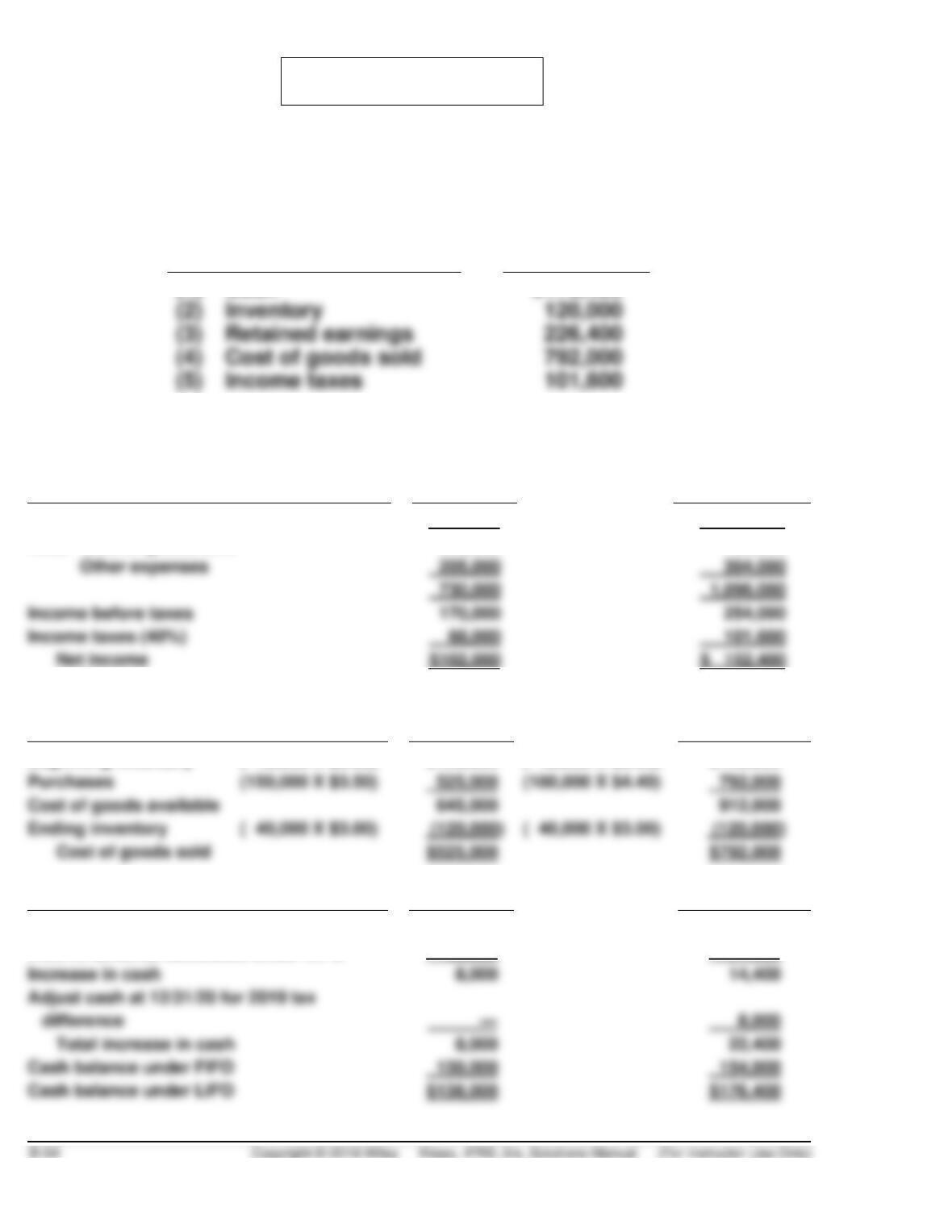

*PROBLEM 8.10

The accounts in the 2020 financial statements which would be affected by

a change to LIFO and the new amount for each of the accounts are as

follows:

Account

New amount

for 2020

(1)

Cash

$176,400

(2)

Inventory

(3)

Retained earnings

(4)

Cost of goods sold

(5)

Income taxes

The calculations for both 2019 and 2020 to support the conversion to LIFO

are presented below.

Income for the Years Ended

12/31/19

12/31/20

Sales

$900,000

$1,350,000

Less: Cost of goods sold

525,000

792,000

Other expenses

205,000

304,000

730,000

Income before taxes

170,000

254,000

Cost of Good Sold and

Ending Inventory for the Years Ended

12/31/19

12/31/20

Beginning inventory

( 40,000 X $3.00)

$120,000

( 40,000 X $3.00)

$120,000

Purchases

(150,000 X $3.50)

525,000

(180,000 X $4.40)

792,000

Cost of goods available

645,000

912,000

Ending inventory

( 40,000 X $3.00)

(120,000)

( 40,000 X $3.00)

Cost of goods sold

Determination of Cash at

12/31/19

12/31/20

Income taxes under FIFO

$ 76,000

$116,000

Income taxes as calculated under LIFO

68,000

101,600

Increase in cash

8,000

14,400

difference

—

8,000

Total increase in cash

8,000

22,400

*PROBLEM 8.10 (Continued)

Determination of Retained Earnings at

12/31/19

12/31/20

Net income under FIFO

$114,000

$174,000

Net income under LIFO

Reduction in retained earnings

12,000

21,600

2019 reduction

12,000

Total reduction in retained earnings

12,000

33,600

Retained earnings under FIFO

TIME AND PURPOSE OF CONCEPTS FOR ANALYSIS

CA 8.1 (Time 15–20 minutes)

CA 8.2 (Time 15–25 minutes)

Purpose—to provide the student with four questions about the carrying value of inventory. These

questions must be answered and defended with rationale. The topics are shipping terms, freight–in,

gross vs. net treatment of discounts, and consigned goods.

CA 8.3 (Time 25–35 minutes)

Purpose—to provide a number of difficult financial reporting transactions involving inventories. This case

CA 8.4 (Time 15–25 minutes)

Purpose—to provide the student with the opportunity to discuss the acceptability of alternative methods

of reporting cash discounts.

CA 8.5 (Time 15–20 minutes)

CA 8.6 (Time 20–25 minutes)

SOLUTIONS TO CONCEPTS FOR ANALYSIS

CA 8.1

(a) Purchased merchandise in transit at the end of an accounting period to which legal title has

passed should be recorded as purchases within the accounting period. If goods are shipped f.o.b.

for the merchandise and the freight.

(b) Inventory ………………………………………………………………………………….. 35,300

Accounts Payable—Supplier …………………………………………………… 35,300

(c) Possible reasons to postpone the recording of the transaction might include:

1. Desire to maintain a current ratio at a given level which would be affected by the additional

CA 8.2

(a) If the terms of the purchase are f.o.b. shipping point (manufacturer’s plant), Strider Enterprises

should include in its inventory goods purchased from its suppliers when the goods are shipped.

For accounting purposes, title is presumed to pass at that time.

(b) Freight-in expenditures should be considered an inventoriable cost because they are part of the

price paid or the consideration given to acquire the asset.

CA 8.3

(a) According to IFRS, cost generally means that the sum of the applicable expenditures and charges

directly or indirectly incurred in bringing an article to its existing condition and location. With

respect to inventory, selling expenses are not part of the inventory costs. To the extent that

warehousing is a necessary function of importing merchandise before it can be sold, certain

elements of warehousing costs might be considered an appropriate cost of inventory in the

warehouse. For example, if goods must be brought into the warehouse before they can be made

(b) It is correct to conclude that obsolete items are excludable from inventory. Cost attributable to

such items is “nonuseful” and “nonrecoverable” cost (except for possible scrap value) and should

be written off. If the cost of obsolete items was simply excluded from ending inventory, the resultant

cost of goods sold would be overstated by the amount of these costs. The cost of obsolete items, if

immaterial, should be commingled with cost of goods sold. If material, these costs should be

separately disclosed.

CA 8.4

(a) Cash discounts should not be accounted for as financial income when payments are made.

Income should be recognized when the performance obligation is satisfied (when the company

CA 8.4 (Continued)

(b) Cash discounts should not be accounted for as a reduction of cost of goods sold for the period

when payments are made. Cost of goods sold should be reduced when the earnings process is

CA 8.5

(a) The average-cost method assumes that inventories are sold or issued evenly from the stock on

hand; and the FIFO method assumes that goods are sold or used in the order in which they are

purchased (i.e., the first goods purchased are the first sold or used.)

(b) The weighted-average cost method combines the cost of all the purchases in the period with the

CA 8.6

(a) Major stakeholders are investors, creditors, Wilkens’ management (including the president and

plant accountant), and other employees of Wilkens Company. The inventory purchase in this instance

reduces net income substantially and lowers Wilkens Company’s tax liability. Current shareholders and

(b) No, the president would not recommend a year-end inventory purchase because under FIFO there

would be no effect on net income.

FINANCIAL STATEMENT ANALYSIS CASE 1

(a)

Sales ………………………………………………………………

€618,876,000

Cost of goods sold* …………………………………………

476,746,000

Gross profit …………………………………………………….

142,130,000

Selling and administrative expenses …………………

102,112,000

Income from operations …………………………………..

Other expense …………………………………………………

24,712,000

Income before income tax ………………………………..

€ 15,306,000

€475,476,000

AC effect (€5,263,000 – €3,993,000) …………………..

(b) €15,306,000 income before income tax X 46.6% tax = €7,132,596 tax;

€15,306,000 – €7,132,596 tax = €$8,173,404 net income as compared to

(c) No, the use of different costing methods does not necessarily mean

that there is a difference in the physical flow of goods. As explained

FINANCIAL STATEMENT ANALYSIS CASE 2

(a) The most likely physical flow of goods for a pharmaceutical manufac–

turer would be FIFO; that is, the first goods manufactured would be the

(b) Noven should consider first whether the inventory costing method

will make a difference. If the prices in the economy, especially if the

(c) This amount is likely not shown in a separate inventory account

because it is immaterial; that is, it is not large enough to make a differ–

*FINANCIAL STATEMENT ANALYSIS CASE 3

Feb. 26

Feb. 25

Feb. 24

2018

2019

2020

Revenues ………………………….

$19,543

$19,864

$37,406

Cost of sales ……………………..

16,681

16,977

29,267

Ending inventories at FIFO …

Ending inventories at LIFO …

LIFO reserve ………………

149

178

FIFO adjusted cost of sales …

$29,249

(a)

2019

2020

(i)

Inventory turnover @LIFO

17.10

15.81

(ii)

Inventory turnover @FIFO

14.78

14.48

(b)

2019

2020

(i)

Inventory turnover using sales and LIFO

20.00

20.20

(ii)

Inventory turnover using sales and FIFO

17.31

18.51

(c) It appears that Superstore calculates its Inventory Turnover using

LIFO inventory with the standard formula of Cost of Sales/Average

Inventory.

ACCOUNTING, ANALYSIS, AND PRINCIPLES

ACCOUNTING

(a) FIFO:

Residential pumps:

Ending inventory cost = (300 X £500) + (200 X £475) = £245,000

Commercial pumps:

Ending inventory at cost = (500 X £1,000) = £500,000

(b) Average Cost:

Residential pumps:

Date

No. Units

Unit Cost

Total Cost

Mar. 1

200

£400

£ 80,000

400

ACCOUNTING, ANALYSIS, AND PRINCIPLES (Continued)

Commercial pumps:

Date

No. Units

Unit Cost

Total Cost

Mar. 1

600

£800

£ 480,000

3

600

500,000

£1,805,000

Average cost/unit = £1,805,000 ÷ 2,000 = £902.50

ANALYSIS

(a) The purpose of a current ratio is to provide some indication of the

(b) An analyst would be better able to compare results of companies

using different inventory methods by attempting to convert one of the

ACCOUNTING, ANALYSIS, AND PRINCIPLES (Continued)

PRINCIPLES

(a) Companies can change from one inventory accounting method to

another, but not back and forth. Changes in accounting method (when

not mandated by a regulatory body such as the IASB or FASB) should

(b) U.S. GAAP allows use of LIFO. So, if U.S. companies adopt IFRS,

RESEARCH CASE

(a) The recent standard (IFRS 15), Revenue for Contracts with Customers,

provides guidance for revenue recognition when right of return exists.

(c) Returns are allowed to satisfy customers and to encourage them to

order larger quantities. Yes, industries such as publishing, music, and

toys often permit purchasers to return inventory for a full or partial

refund.