CHAPTER 17

Investments

ASSIGNMENT CLASSIFICATION TABLE (BY TOPIC)

Topics

Questions

Brief

Exercises

Exercises

Problems

Concepts

for Analysis

1. Debt investments.

1, 2, 3, 4, 11,

12

1, 9

4, 7

(b) Trading.

5, 8,

9, 10

3, 5

4

1, 3, 4, 7

1, 4

2. Bond amortization.

7, 8

1, 2, 3, 4

3, 4, 5

1, 2

3. Equity investments.

1, 13, 14, 16

1

4, 7

(a) Non-trading.

17, 23

8, 9

13

10

15, 17, 23

13, 14,

17, 18, 19

10, 11

10, 11, 12,

5, 6, 8, 9,

3

4. Disclosures of investments.

24

10, 11

5, 8, 9, 10,

11

5. Fair value option.

11, 12, 27

6

7, 8, 19

2, 7

6. Impairments.

25

11, 12

21, 22, 23

1, 3

7. Recycling, Reclassifications

26

13

1, 3, 7

*This material is dealt with in an Appendix to the chapter.

ASSIGNMENT CLASSIFICATION TABLE (BY LEARNING OBJECTIVE)

Learning Objectives

Brief

Exercises

Exercises

Problems

Concepts

for

Analysis

1. Describe the accounting for debt

investments.

1, 2, 3, 4, 5,

6

1, 2, 3, 4, 5,

6, 7, 8

1, 2, 3, 4, 7

1, 3, 7

13, 14, 15, 17

9, 10, 11

accounting.

10

8

5, 6

4. Evaluate other major issues related to

debt and equity investments.

11, 12, 13

9, 21, 22, 23

7

7

*5. Describe the uses of and accounting

for derivatives.

24

12, 13, 14

15, 16, 17

accounting problems.

8. Describe required fair value

disclosures.

ASSIGNMENT CHARACTERISTICS TABLE

Item

Description

Level of

Difficulty

Time

(minutes)

E17.1

Investment classifications.

Simple

5–10

E17.2

Debt investments.

Simple

10–15

E17.3

Debt investments.

Simple

15–20

E17.4

Debt investments.

Simple

10–15

E17.5

Debt investments.

Simple

10–15

presentation

E17.7

Fair value option.

Simple

5–10

E17.8

Fair value option.

Moderate

15–20

E17.9

Comprehensive income disclosure

Moderate

20–25

E17.10

Entries for equity investments.

Simple

10–15

E17.11

Equity investments.

Simple

10–15

E17.12

Equity investment entries and reporting.

Simple

presentation.

E17.14

Equity investment entries.

Moderate

20–25

E17.15

Journal entries for fair value and equity methods.

Moderate

15–20

E17.16

Equity method.

Moderate

10–15

E17.17

Equity investments—trading.

Moderate

10–15

E17.18

Equity investments—trading.

Moderate

15–20

E17.19

Fair value and equity method compared.

Moderate

15–20

E17.20

Equity method.

Simple

10–15

E17.21

Impairment.

Moderate

15–20

E17.22

Impairment.

Moderate

10–15

E17.23

Impairment.

Moderate

20–25

*E17.24

Derivative transaction.

Moderate

15–20

*E17.25

Fair value hedge.

Moderate

20–25

*E17.26

Cash flow hedge.

Moderate

20–25

*E17.27

Fair value hedge.

Moderate

15–20

*E17.28

Call option.

Moderate

20–25

*E17.29

Cash flow hedge.

Moderate

25–30

P17.1

Debt investments.

Moderate

20–30

P17.2

Debt investments, fair value option.

Moderate

30–40

P17.3

Debt and equity investments.

Moderate

25–30

P17.4

Debt investments.

Moderate

25–35

P17.5

Equity investment entries and disclosures.

Moderate

25–35

P17.6

Equity investments.

Moderate

25–35

P17.7

Debt investment entries.

Moderate

25–35

P17.8

Fair value and equity method.

Moderate

20–30

P17.9

Financial statement presentation of equity investments.

Moderate

20–30

ASSIGNMENT CHARACTERISTICS TABLE (Continued)

Item

Description

Level of

Difficulty

Time

(minutes)

P17.10

Equity investments.

Complex

30–40

P17.11

Investments—statement presentation.

Moderate

20–30

Derivative financial instrument.

Moderate

20–25

Derivative financial instrument.

Moderate

20–25

Free-standing derivative.

Moderate

20–25

Fair value hedge interest rate swap.

Moderate

30–40

Cash flow hedge.

Moderate

25–35

Fair value hedge.

Moderate

25–35

CA17.1

Issues raised about investments.

Moderate

25–30

CA17.2

Equity investments.

Moderate

25–30

CA17.3

Financial statement effect of investments.

20–30

CA17.4

Equity investments.

Moderate

20–25

CA17.5

Investment accounted for under the equity method.

15–25

CA17.6

Equity investments.

Moderate

25–35

CA17.7

Fair value.

Moderate

25–35

ANSWERS TO QUESTIONS

1. The two criteria for determining the valuation of financial assets are the (1) company’s business

2. Only debt investments such as loans and bond investments are valued at amortized cost. A

company should use amortized cost if it has a business model whose objective is to hold assets

3. Amortized cost is the initial recognition amount of the investment minus repayments, plus or

minus cumulative amortization and net of any reduction for uncollectibility.

4. Companies group investments in debt securities into three separate categories for accounting

and reporting purposes.

• Held-for-collection: Investments held (1) with the objective of holding assets in order to

collect contractual cash flows, and (2) the contractual terms of the financial asset give rise

5. Lady Gaga should classify this investment as a trading investment because companies frequently

buy and sell this type of investment to generate profits in short term differences in price.

LO: 1, Bloom: K, Difficulty: Simple, Time: 3-5, AACSB: None, AICPA BB: None, AICPA FC: Reporting, AICPA PC: Communication

6. (a) If Lady Gaga plans to hold the investment to collect interest and receive the principal at

maturity, it should account for this investment at amortized cost.

7. €3,604,062 X 10% = €360,406; €360,406 ÷ 2 = €180,203. Wheeler would make the following entry:

Questions Chapter 17 (Continued)

8. Fair Value Adjustment ……………………………………………………………………. 75,735

Unrealized Holding Gain or Loss—Income

9. (a) Unrealized holding gains and losses for trading investments should be included in net income

for the current period. (b) Unrealized holding gains and losses are not recognized for held-for-

10. (a) Unrealized Holding Gain or Loss—Income ………………………………….. 60,000

Fair Value Adjustment ………………………………………………………. 60,000

11. The fair value option allows companies the choice of reporting debt investments at fair value. If

this option is chosen, the company records in net income unrealized gains and losses with

12. No, Franklin cannot use the fair value option for this investment. This option is generally available

13. Investments in equity securities can be classified as follows:

(a) Holdings of less than 20% (fair value method)—investor has passive interest.

14. Investments in shares do not have contractual cash flows (nor a maturity date) and therefore

Questions Chapter 17 (Continued)

15. Equity Investments (10,000 X $26) ………………………………………………. 260,000

16. Gross selling price of 10,000 shares at $27.50 ………………………………. $275,000

Less: Brokerage commissions ……………………………………………………. (1,770)

Proceeds from sale ……………………………………………………………………. 273,230

17. Both trading and non-trading equity investments are reported at fair value. However, any

18. Significant influence over an investee may result from representation on the board of directors,

participation in policy-making processes, material intercompany transactions, interchange of

19. Under the equity method, the investment is originally recorded at cost, but is adjusted for

changes in the investee’s net assets. The investment account is increased (decreased) by the

20. The following information is reported under the equity method:

1. Investments originally recorded at cost with adjustment for the investor’s share of the

Questions Chapter 17 (Continued)

21. Dividends subsequent to acquisition should be accounted for as a reduction in the equity

22. Ordinarily, Raleigh Corp. should discontinue applying the equity method and not provide for

additional losses beyond the carrying value of £170,000. However, if Raleigh Corp.’s loss is not

23. Trading equity investments are reported as a current asset while non-trading investments are

reported as a long-term investment. Trading investments are expected to be disposed of within

24. Recycling adjustments are necessary to insure that double counting does not result when

25. A debt investment is impaired when “it is probable that the investor will be unable to collect all

amounts due according to the contractual terms.” When an impairment has occurred, the

26 When an investment is transferred from one category to another, the transfer should be recorded

27. Major unresolved issues related to fair value accounting include measurement based on

Questions Chapter 17 (Continued)

*28. An underlying is a special interest rate, security price, commodity price, index of prices or rates,

or other market-related variable. Changes in the underlying determine changes in the value of

*29. See illustration below:

Feature

Traditional Financial Instrument

(e.g., Trading Security)

Derivative Financial Instrument

(e.g., Call Option)

Payment Provision

Initial Investment

Share price times the number

Change in share price (underlying)

*30. The purpose of a fair value hedge is to hedge (offset) the exposure to changes in the fair value of

*31. The unrealized holding gain or loss on non-trading equity investments should be reported as

income when this security is designated as a hedged item in a qualifying fair value hedge. If the

*32. This is likely a setting where the company is hedging the fair value of a fixed-rate debt obligation.

The fixed payments received on the swap will offset fixed payments on the debt obligation. As a

result, if interest rates decline, the value of the swap contract increases (a gain), while at the

Questions Chapter 17 (Continued)

*33. A cash flow hedge is used to hedge exposures to cash flow risk, which is exposure to the

variability in cash flows. The cash flows received on the hedging instrument (derivative) will offset

*34. Derivatives used in cash flow hedges are accounted for at fair value on the statement of financial

*35. A hybrid security is a security that has characteristics of both debt and equity and often is a

combination of traditional and derivative financial instruments. A convertible bond is a hybrid

SOLUTIONS TO BRIEF EXERCISES

BRIEF EXERCISE 17.1

January 1, 2019

(a) Debt Investments ………………………………………………. 74,086

Cash ………………………………………………………….. 74,086

BRIEF EXERCISE 17.2

January 1, 2019

(a) Debt Investments ………………………………………………. 74,086

Cash ………………………………………………………….. 74,086

BRIEF EXERCISE 17.3

(a) Debt Investments ………………………………………………. 74,086

Cash ………………………………………………………….. 74,086

BRIEF EXERCISE 17.4

(a) Debt Investments ……………………………………………… 65,118

Cash …………………………………………………………. 65,118

BRIEF EXERCISE 17.5

Unrealized Holding Gain or Loss—Income ……………… 672

BRIEF EXERCISE 17.6

(a) Debt Investments ……………………………………………… 50,000

Cash …………………………………………………………. 50,000

BRIEF EXERCISE 17.7

(a) Equity Investments …………………………………………. 13,200

Cash ……………………………………………………….. 13,200

BRIEF EXERCISE 17.8

(a) Equity Investments …………………………………………. 13,200

Cash ……………………………………………………….. 13,200

BRIEF EXERCISE 17.9

Equity Investment ……………………………………………………. 700

BRIEF EXERCISE 17.10

Equity Investments ……………………………………………….. 300,000

BRIEF EXERCISE 17.11

Loss on Impairment ($70,000 – $60,000) ……………. 10,000

BRIEF EXERCISE 17.12

Case 1 The total fair value adjustments is $10,000 ($40,000−$30,000), of

which $5,000 is due to expected credit losses. The entry to record the

Case 2 No impairment results, because the fair value is greater than

amortized cost

BRIEF EXERCISE 17.13

January 1, 2020

Debt Investments ……………………………………………… 10,325

SOLUTIONS TO EXERCISES

EXERCISE 17.1 (5–10 minutes)

EXERCISE 17.2 (10–15 minutes)

(a) January 1, 2019

Debt Investments ………………………………………. 300,000

Cash ………………………………………………….. 300,000

EXERCISE 17.3 (15–20 minutes)

(a) January 1, 2019

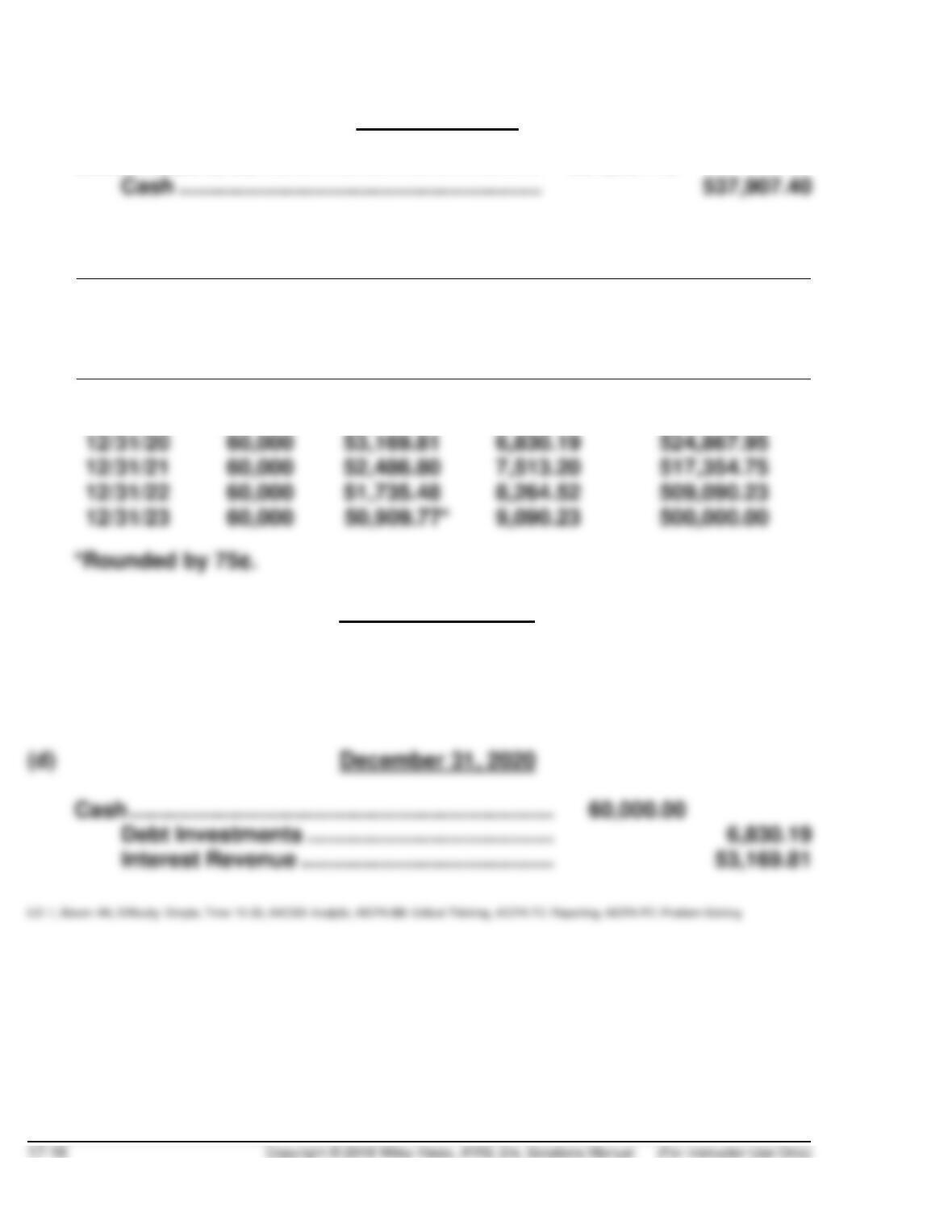

Debt Investments ………………………………………. 537,907.40

(b) Schedule of Interest Revenue and Bond Premium Amortization

12% Bonds Sold to Yield 10%

Date

Cash

Received

(1)

Interest

Revenue

@ 10%

(2)

Premium

Amortized

(1–2)

Carrying Amount

of Bonds

1/1/19

—

—

—

$537,907.40

12/31/19

$60,000

$53,790.74

$6,209.26

531,698.14

(c) December 31, 2019

Cash …………………………………………………………… 60,000.00

Debt Investments …………………………………. 6,209.26

Interest Revenue ………………………………….. 53,790.74

EXERCISE 17.4 (10–15 minutes)

(a) January 1, 2019

Debt Investments …………………………………………. 537,907.40

Cash ………………………………………………….. 537,907.40

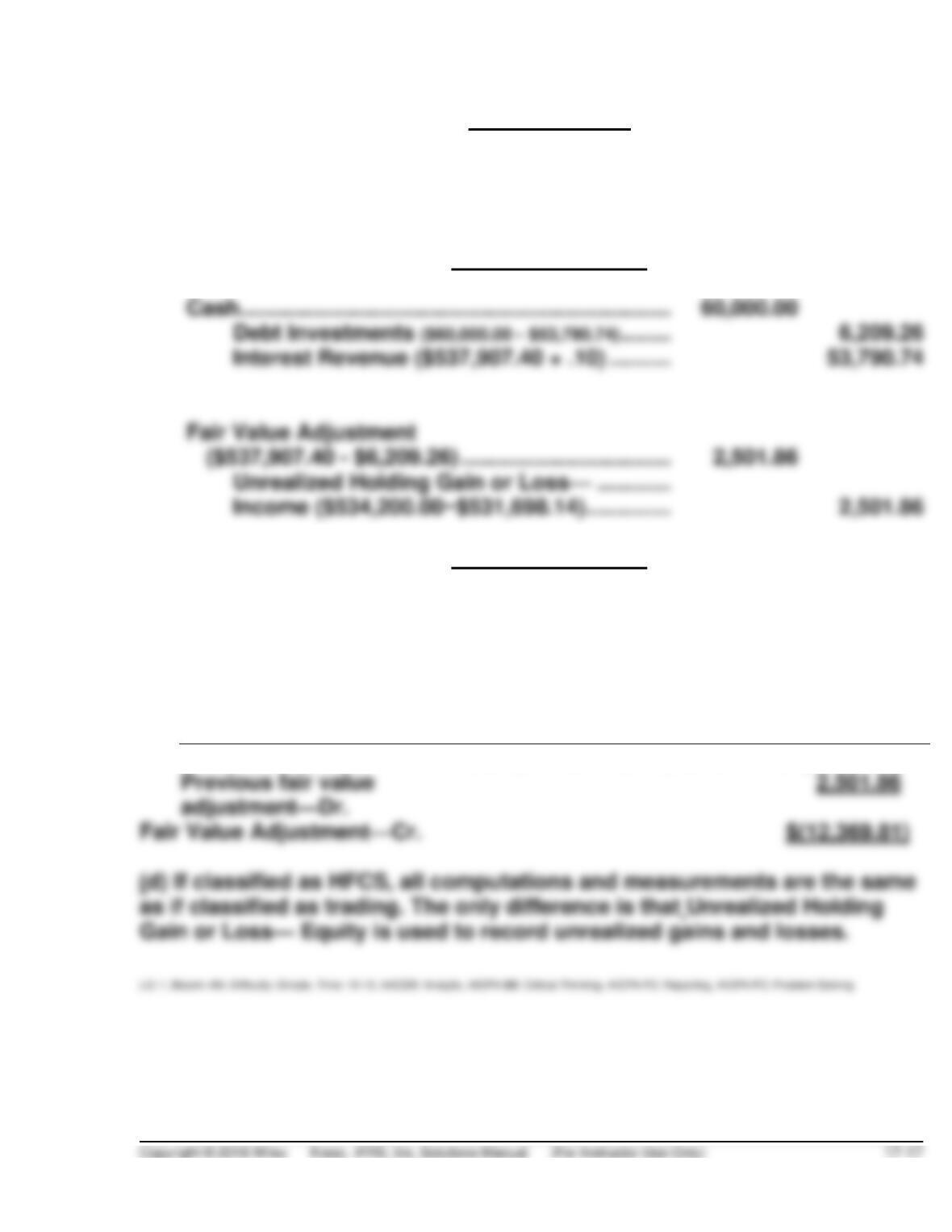

(b) December 31, 2019

(c) December 31, 2020

Unrealized Holding Gain or Loss— Income 12,369.81

Fair Value Adjustment ……………………… 12,369.81

Amortized

Cost

Fair Value

Unrealized

Holding

Gain (Loss)

Debt investments

$524,867.95

$515,000.00

($ (9,867.95)

EXERCISE 17.5 (10–15 minutes)

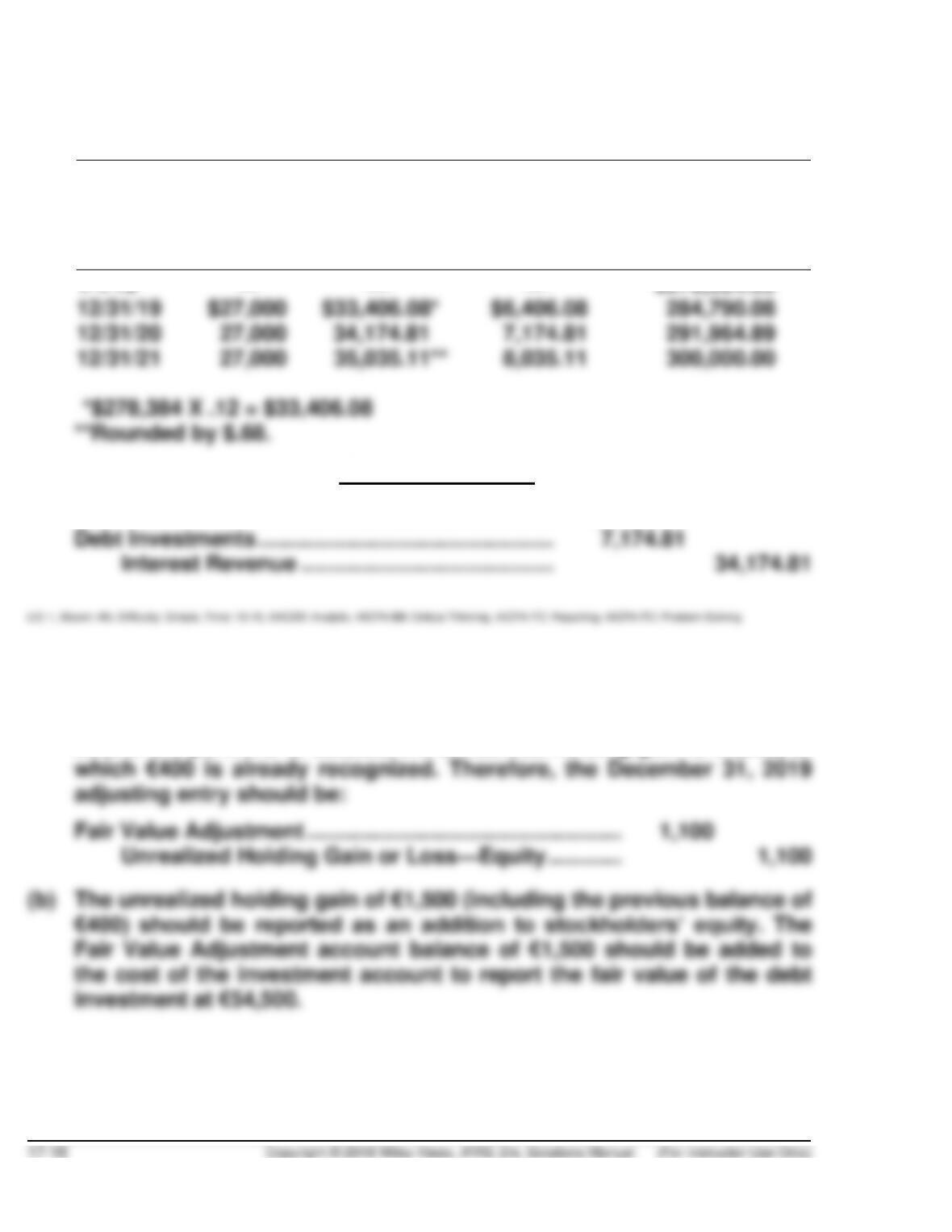

(a) Schedule of Interest Revenue and Bond Discount Amortization

9% Bond Purchased to Yield 12%

Date

Cash

Received

(1)

Interest

Revenue

@12%

(2)

Bond Discount

Amortization

(2–1)

Carrying Amount

of Bonds

(b) December 31, 2020

Cash …………………………………………………………… 27,000.00

EXERCISE 17.6 (10–15 minutes)

(a) The portfolio should be reported at the fair value of €54,500. Since the

cost of the portfolio is €53,000, the unrealized holding gain is €1,500, of

EXERCISE 17.6 (Continued)

STEFFI GRAF, SA

Balance Sheet

As of December 31, 2019

_____________________________________________________________

Current assets:

Debt investments €54,500*

Stockholders’ equity:

(c) Computation of realized gain or loss on sale of debt security:

Net proceeds from sale of security A €15,100

Cost of security A (17,500)

EXERCISE 17.7 (5–10 minutes)

(a) December 31, 2019

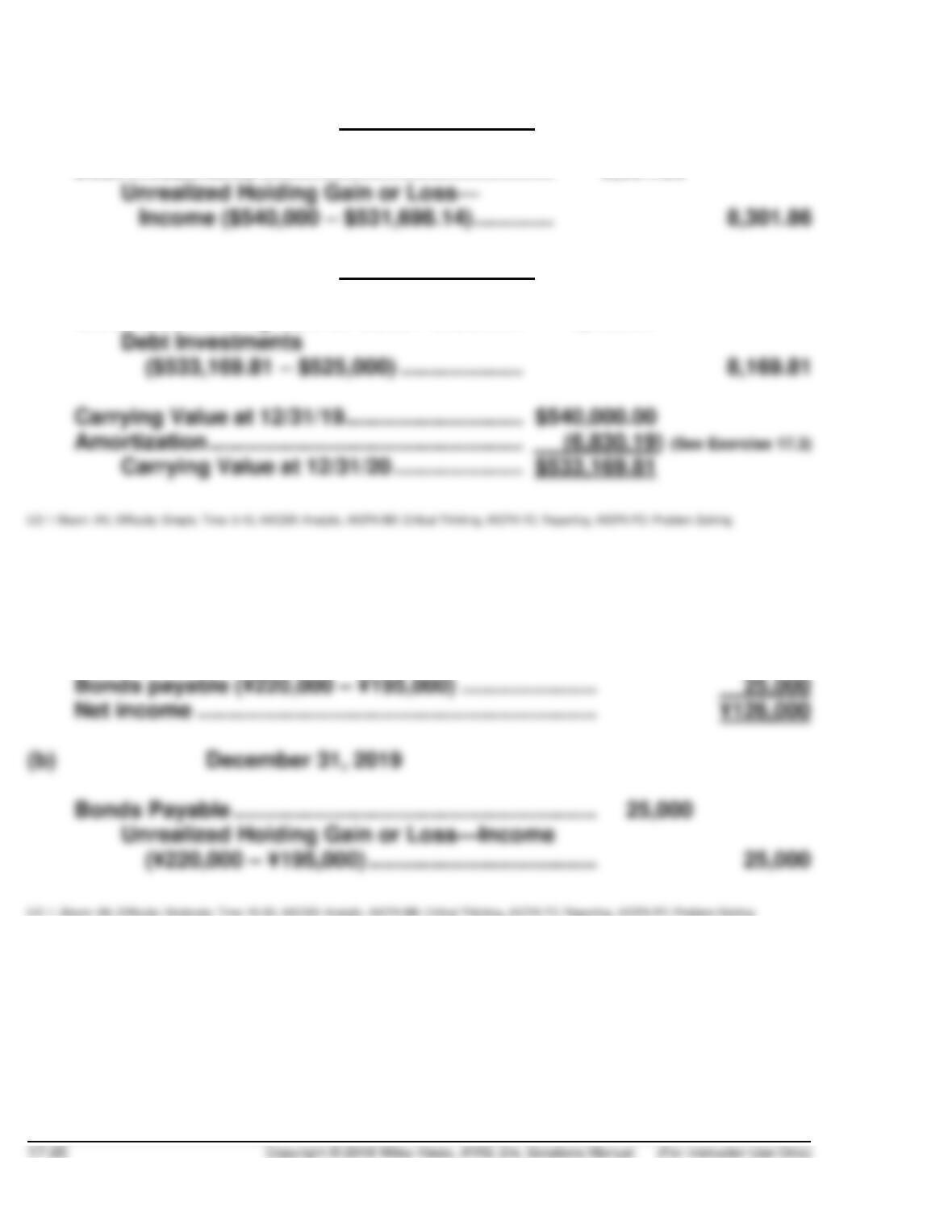

Debt Investments ………………………………………… 8,301.86

(b) December 31, 2020

Unrealized Holding Gain or Loss—Income .. 8,169.81

EXERCISE 17.8 (15-20 minutes)

(a) Net income before gains and losses …………………… ¥100,000

Debt investments (¥41,000 – ¥40,000) …………………. 1,000