PROBLEM 18.3 (Continued)

In this case, Grill Masters should reduce revenue recognized by $3,360

which is computed as the selling price of the grills $52,640 [($280 X

200) – ($56,000 X .06)], because it is probable (almost certain) that it

will provide the discounted price amounting to 6%.

(c) 1. September 1, 2019

Accounts Receivable

[$20,000 – (3% X $20,000)] ………………………… 19,400

Accounts Receivable …………………………... 19,400

2. September 1, 2019

Accounts Receivable

[$20,000 – (3% X $20,000)] ………………………… 19,400

October 15, 2019

Cash ($1,000 X 20) ………………………………………. 20,000

PROBLEM 18.3 (Continued)

(d) October 1, 2019

Notes Receivable ……………………………………………… 4,000

Sales Revenue ($5,324 X .75132 [ PV i=10%, n=3]) … 4,000

December 31, 2019

Grill Masters records revenue of $4,000 on October 1, 2019, which is

PROBLEM 18.4

(a) The entry to record the sale is as follows:

June 1, 2019

Accounts Receivable ………………………………… 70,000

June 1, 2019

Accounts Receivable ………………………………… 70,000

Allowance for Sales Returns and

(b) 1. May 1, 2019

2. August 1, 2019

Cash …………………………………………………… 432,000

PROBLEM 18.4 (Continued)

(c) The introduction of the bonus payment gives rise to a change in the

May 1, 2019

Cash (20% X $540,000) ……………………………… 108,000

Unearned Sales Revenue …………………… 108,000

July 1, 2019

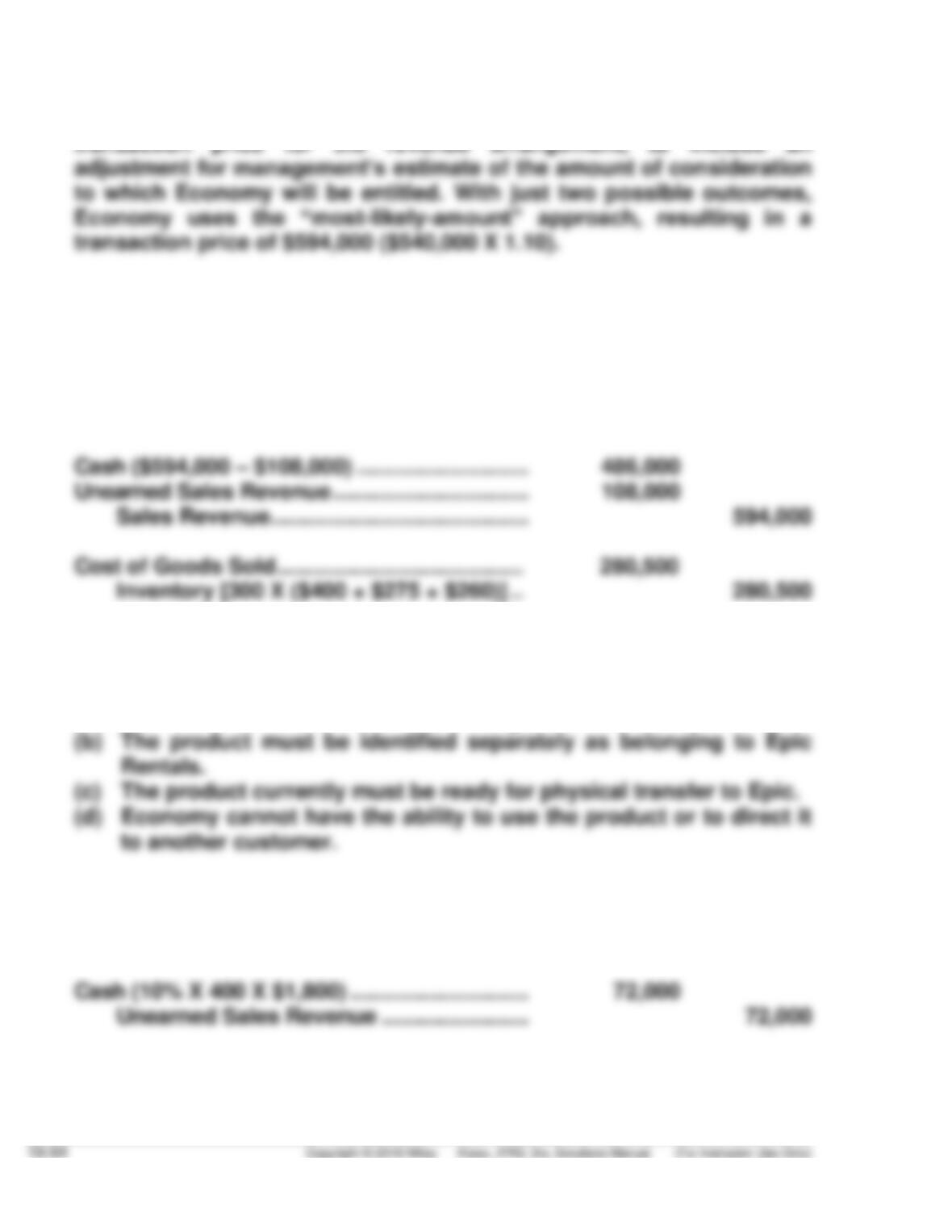

(d) This is a bill and hold arrangement. It appears that the criteria for Epic

to have obtained control of the appliance bundles have been met:

(a) The reason for the bill-and-hold arrangement must be substantive.

Economy makes the following entries.

February 1, 2019

PROBLEM 18.4 (Continued)

April 1, 2019

Accounts Receivable ($720,000 – $72,000) … 648,000

Unearned Sales Revenue……………………………… 72,000

Sales Revenue ………………………………….. 720,000

PROBLEM 18.5

(a) If sales with returns are recorded gross at point of sale, the following

entries are made.

January 1, 2019

Notes Receivable ……………………………………… 48,000

Sales Revenue (40 X $1,200) ………………. 48,000

January 1, 2019

Notes Receivable (Mills) …………………………….. 48,000

Allowance for Sales Returns and

(b) August 10, 2019

Cash (16 X $3,600*) …………………………………… 57,600

Sales Revenue …………………………………… 57,600

PROBLEM 18.5 (Continued)

(c) This revenue arrangement has 3 different performance obligations:

(1) the sale of the dryers, (2) installation, and (3) the maintenance plan.

The total revenue of $45,200 should be allocated to the three

performance obligations based on their relative standalone selling

price:

The allocation for a single contract is as follows.

Dryers $41,091 ($42,000 / $46,200) X $45,200

Ritt makes the following entries.

June 20, 2019

Cash (20% X $45,200) …………………………………… 9,040

PROBLEM 18.5 (Continued)

October 1, 2019

Cash (80% X $45,200)……………………………….. 36,160

Accounts Receivable ………………………… 36,160

Cost of Goods Sold …………………………………. 33,000

Inventory (3 X $11,000) ……………………. 33,000

December 31, 2019

(d) Entries for Ritt

April 25, 2019

Inventory (Consignments) (100 X $800)………… 80,000

Finished Goods Inventory …………………. 80,000

June 30, 2019

PROBLEM 18.5 (Continued)

Entries for Farm Depot April 25, 2019

No entry – Inventory continues to be controlled by Ritt.

Summary Entry for Consignment Sales

PROBLEM 18.6

(a) Warranty Performance Obligations

1. To transfer 70 specialty winches to customers with a total

transaction price of $21,000.

2. To provide extended warranty services for 20 winches after the

assurance warranty period with a value of $8,000 (20 X $400) for

2 years.

With respect to the bonus points program, Hale has a performance

obligation for:

(b)

Cash …………………………………………………………….. 29,000

Unearned Warranty Revenue

(20 X $400) …………………………………….. 8,000

Sales Revenue ………………………………….. 21,000

To reduce inventory and recognize cost of goods sold:

Cost of Goods Sold …………………………………. 16,000

Inventory ………………………………………….. 16,000

Hale records Warranty Expense account over the first three years as

(c) Because the points provide a material right to a customer that it would

PROBLEM 18.6 (Continued)

The standalone selling price:

Purchased products: $100,000

To record sales of products subject to bonus points:

Cash ……………………………………………………….. 100,000

(d) Additional Sales Revenue from bonus point redemptions, if 4,500

points have been redeemed: (4,500 points ÷ 9,500 points X $8,676) =

$4,110.

PROBLEM 18.7

(a) The transaction price is allocated to the products and loyalty points, as

follows:

Total

Standalone Percent Transaction Allocated

Selling Prices Allocated Price Amounts

Product Purchases €300,000 80% €300,000 €240,000

(b) July 2, 2019

Cash …………………………..…………………………... 300,000

Unearned Sales Revenue……… …………. 60,000

Sales Revenue ……………………… …….. 240,000

PROBLEM 18.8

(a) Sales with financing

January 1, 2019

Notes Receivable …………………………………….. 4,450

Sales Revenue

($5,000 X .89000 [PV n=2; i=6%]) ……………… 4,450

$4,717

(b) Gift Cards

March 1, 2019

Cash ……………………………………………………….. 2,000

Unearned Sales Revenue (20 X $100) ….. 2,000

March 31, 2019

April 30, 2019

Unearned Sales Revenue …………………………. 600

PROBLEM 18.8 (Continued)

June 30, 2019

Unearned Sales Revenue …………………………. 100

Sales Revenue (0.05 X 20 X $100) ………. 100

June 30, 2019

Unearned Sales Revenue …………………………. 200

Sales Revenue (0.10 X 20 X $100) ………. 200

*PROBLEM 18.9

(a)

2019

2020

2021

Contract price

$900,000

$900,000

$900,000

Less estimated cost:

Costs to date

270,000

450,000

610,000

Estimated cost to complete

—

Estimated total cost

Estimated total gross profit

$300,000

$300,000

$290,000

Gross profit recognized in—

2019:

$270,000

X $300,000 =

$135,000

$600,000

2020:

$450,000

X $300,000 =

$225,000

$600,000

(b) In 2019 and 2020, no gross profit would be recognized.

Total revenues ……………………………. $900,000

Total cost……………………………………. (610,000)

Gross profit recognized in 2021 …… $290,000

.

*PROBLEM 18.10

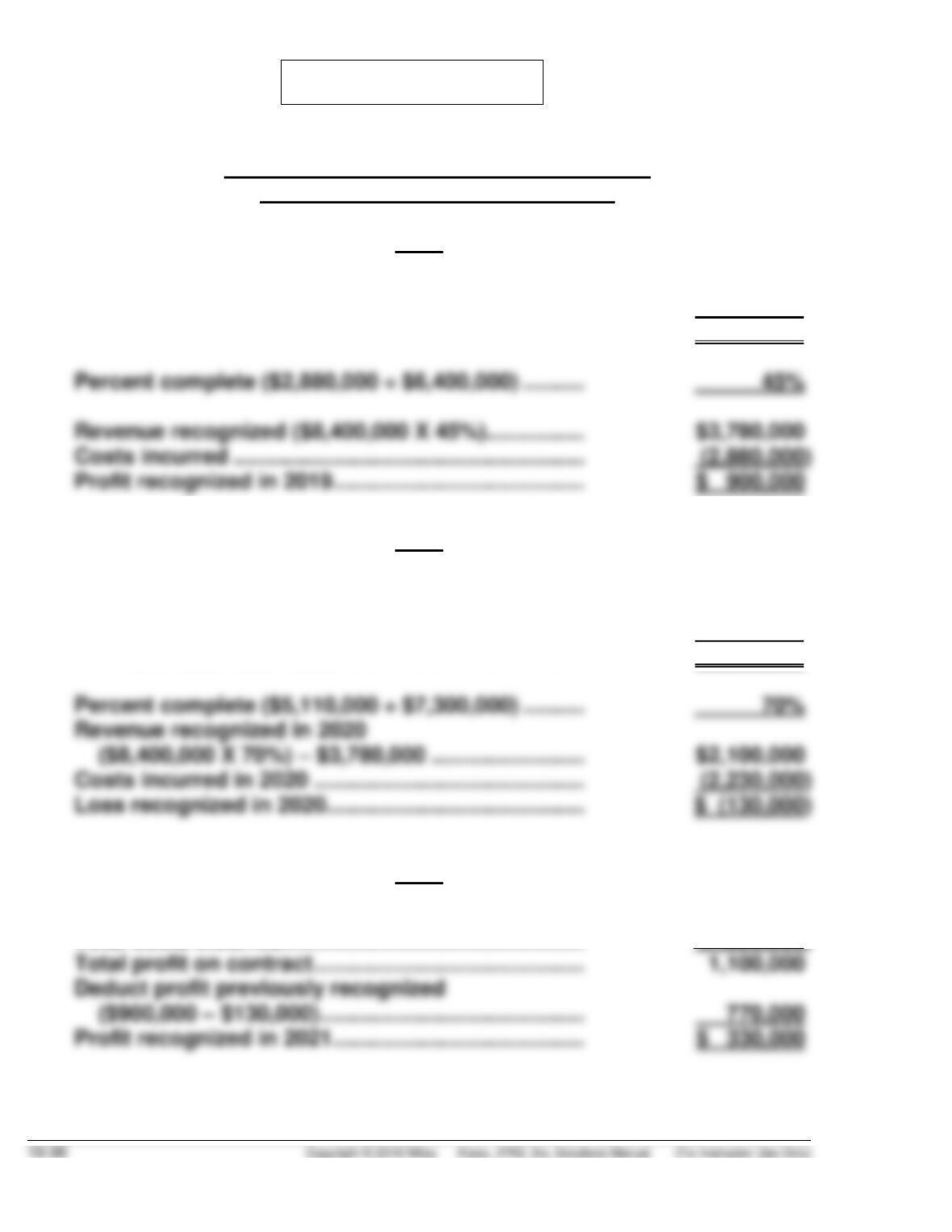

(a) Computation of Recognizable Profit/Loss

Percentage-of–Completion Method

2019

Costs to date (12/31/19) ……………………………………. $2,880,000

Estimated costs to complete ……………………………. 3,520,000

Estimated total costs ………………………………… $6,400,000

2020

Costs to date (12/31/20)

($2,880,000 + $2,230,000) ………………………………. $5,110,000

Estimated costs to complete ……………………………. 2,190,000

Estimated total costs ………………………………… $7,300,000

2021

Total revenue recognized …………………………………. $8,400,000

Total costs incurred …………………………………………. (7,300,000)

PROBLEM 18.10 (Continued)

(b) No profit or loss recognized in 2019 and 2020

2021

Contract price …………………………………………………. $8,400,000

*PROBLEM 18.11

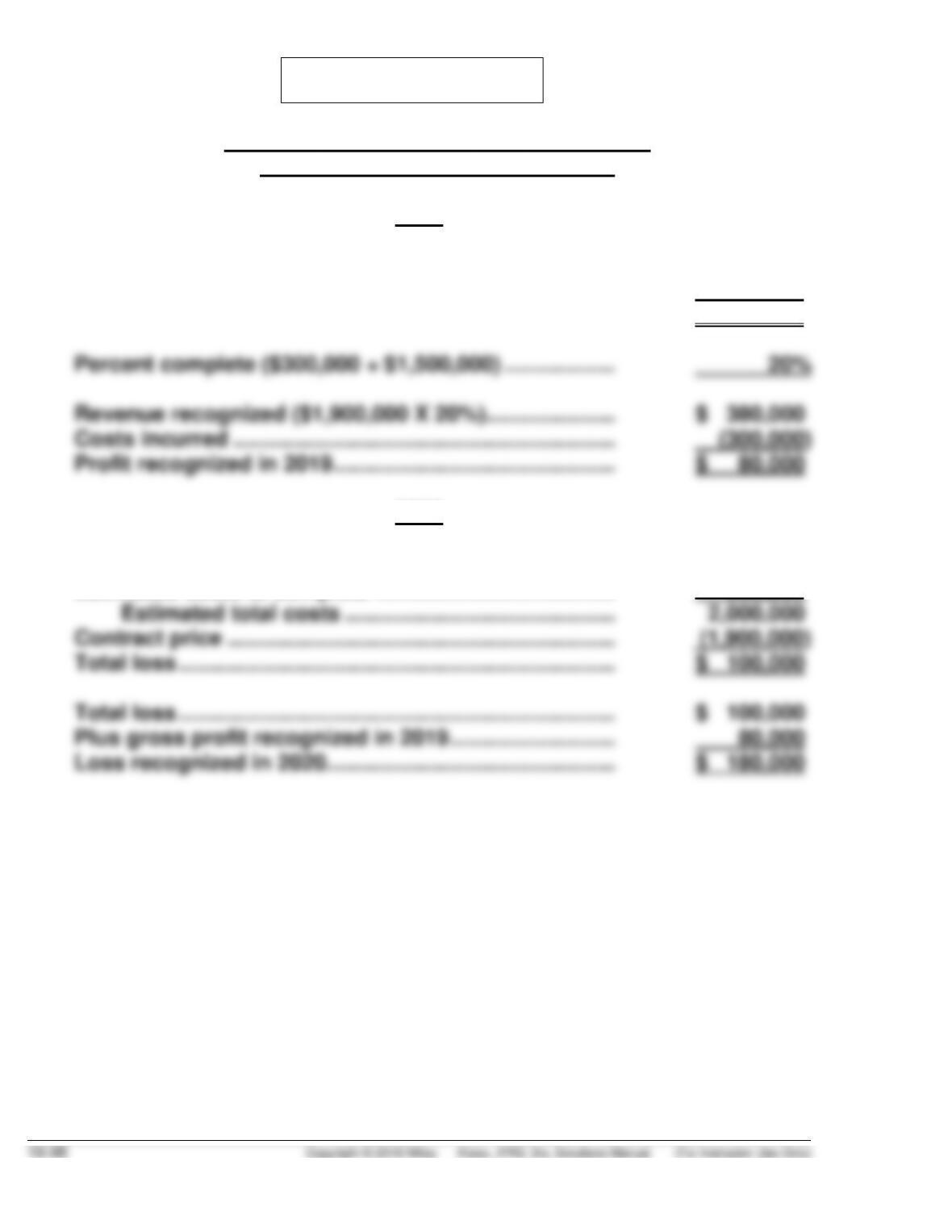

(a) Computation of Recognizable Profit/Loss

Percentage-of–Completion Method

2019

Costs to date (12/31/19) ………………………………………… $ 300,000

Estimated costs to complete ………………………………… 1,200,000

Estimated total costs …………………………………….. $1,500,000

2020

Costs to date (12/31/20) ………………………………………… $1,200,000

Estimated costs to complete ………………………………… 800,000

PROBLEM 18.11 (Continued)

2021

Costs to date (12/31/21) …………………………………. $2,100,000

Estimated costs to complete …………………………. 0

(b) No profit or loss in 2019

2020

Contract price ………………………………………………. $1,900,000

2021

Contract price ………………………………………………. $1,900,000

Costs incurred …………………………..…………………. (2,100,000)

*PROBLEM 18.12

(a) A company recognizes revenue in the accounting period when a

performance obligation is satisfied—the revenue recognition principle.

A key element of the revenue recognition principle is that a company

Companies satisfy performance obligations either at a point in time or

over a period of time. Companies recognize revenue over a period of

time if one of the following two criteria is met.

1. The customer receives and consumes the benefits as the seller

performs.

2. The customer controls the asset as it is created or enhanced (e.g.,

In the case of a franchise, fees related to rights to use the intellectual

property generally are recognized at a point in time, usually when the

franchise begins operation. That is because at that time, the customer

controls the product or service when it has the ability to direct the use