CA 24.3 (Continued)

Situation 3

The fact that a company chooses to self-insure the contingency of injury to others caused by its vehicles

is not enough of a basis to accrue a loss contingency that has not occurred at the date of the financial

statements. An accrual or “reserve” cannot be made for the amount of insurance premium that would

CA 24.4

1. The financial statements should be adjusted for the expected loss pertaining to the remaining

receivable of £240,000. Such adjustment should reduce accounts receivable to their realizable

value as of December 31, 2018.

4. This case is a difficult problem. If this event is of the second type which provides evidence with

respect to conditions that did not exist at December 31, 2018, then appropriate disclosures should

indicate that:

5. Adjust the inventory figure as of December 31, 2018, as required by a market price of £2 instead

of £1.40, applying the lower-of-cost-or-net realizable value principle. The actual quotation was a

transitory error and no purchases had been made at this quotation.

CA 24.5

To: Anthony Reese, Accountant

From: Student

Date: Current date

Subject: Determination of reportable segments for Winsor Corp.

I have analyzed the segment information which you gave me and determined that the funeral, the

cemetery, and the real estate segments must be reported separately. The remaining three—the

limousine, floral, and dried whey segments—can be combined under the category of other.

Second, a segment is considered significant enough to be reported separately if its absolute operating

profit or operating loss is 10% or more of the greater, in absolute amount of: (a) the combined operating

profit of all segments without an operating loss or (b) the combined operating loss of all segments that

incurred a loss. Combined operating profit for all profitable segments totals $96,000. Both the funeral and

the cemetery segments have operating profits exceeding 10% of total profits whereas the real estate

segment’s operating loss in absolute amount is greater than 10 percent of total profits. Thus, all three

must be separately reported.

Third, a segment must be reported separately if its identifiable assets are greater than or equal to

10 percent of the combined identifiable assets for all segments. Again, the funeral, the cemetery, and

CA 24.6

(a) 1. The company should report its quarterly results as if each interim period is discrete.

2. Under the discrete approach the amounts should be reported as the company’s revenue

and expenses as follows on its quarterly report prepared for the first quarter of the 2018–

2019 fiscal year:

Sales Revenue ……………………………………………………………………………… ¥60,000,000

(b) The financial information to be disclosed to its shareholders in its quarterly reports as a minimum

include:

1. Statement that the same accounting policies and methods of computation are followed in

the interim financial statements as compared with the most recent annual financial

statements or, if those policies or methods have been changed, a description of the nature

and effect of the change.

2. Explanatory comments about the seasonality or cyclicality of interim operations.

3. The nature and amount of items affecting assets, liabilities, equity, net income, or cash

CA 24.7

(a) Acceptable. The use of estimated gross profit rates to determine the cost of goods sold is accept–

able for interim reporting purposes as long as the method and rates utilized are reasonable. The

company should disclose the method employed and any significant adjustments which result

from reconciliations with annual physical inventory.

(d) Not acceptable. Gains on the sale of investments would not be deferred if they occurred at year–

end. Consequently, they should not be deferred to future interim periods but should be reported

in the quarter the gain was realized.

CA 24.8

(a) Arguments for requiring published forecasts:

1. Investment decisions are based on future expectations; therefore, information about the

future would facilitate better decisions.

(b) The purpose of a safe harbor rule is to provide protection to an enterprise that presents an

erroneous projection as long as the projections were prepared on a reasonable basis and were

disclosed in good faith. An enterprise’s concern with the safe harbor rule is that a jury’s definition

of reasonable might be at some variance from a company’s or, for that matter, the SEC’s.

(c) An enterprise’s concerns about preparing a forecast are as follows:

1. No one can foretell the future. Therefore forecasts, while conveying an impression of precision

about the future, will inevitably be wrong.

LO: 4, Bloom: AP, Difficulty: Moderate, Time: 25–30, AACSB: Ethics, Analytic, AICPA BB: Critical Thinking, AICPA FC: Reporting, AICPA PC: Problem Solving

CA 24.9

(a) The controller notes that the financial vice president is misrepresenting the financial condition of

the company by suggesting that the company has become more efficient when, in fact, the

improved ratio is gained through manipulation of estimates. The controller, however, hesitates

because estimating does not follow precise, clear-cut rules. The dilemma exists because Lilly is

asked to weigh the benefits that may accrue to the company if its profit margin on sales appears

much improved against the accountant’s normal requirement to present financial information

fairly (that is, in a manner that is consistent with previous reporting).

CA 24.10

(a) The ethical issues involved are profitability, long-term versus short-term performance, and integrity

of financial reporting.

(b) Form should not dictate substance. The bonds should be issued when the company needs the

*CA 24.11

FINANCIAL REPORTING PROBLEM

(a) The specific items M&S discusses in Note 1 are basis of preparation;

new accounting standards adopted by the Group; New accounting

standards in issue but not yet effective; accounting convention; basis

of consolidation; subsidiaries; revenue; supplier income; dividends;

(b) M&S reported segments for its UK and International. International was

segmented into owned stores and franchised stores. Revenue was

COMPARATIVE ANALYSIS CASE

Puma versus adidas

(a) 1. Puma commented on the following list of items in its note on

accounting policies:

Note 2 – Significant Consolidation, Accounting and Valuation

Principles

• Consolidation principles

• Group consolidated companies

• Non-current investments

• Property, plant and equipment

• Goodwill

• Other intangible assets

• Impairment of assets

• Holdings in associated companies

• Product development

• Financial results

• Income taxes

• Deferred taxes

COMPARATIVE ANALYSIS CASE (Continued)

2. adidas commented on the following list of items in its note on

accounting policies:

Note 2 – Summary of significant accounting policies

• Principles of consolidation

• Principles of measurement

• Leases

• Goodwill

• Intangible assets (except goodwill)

• Research and development

• Financial assets

• Borrowings and other liabilities

• Other provisions and accrued liabilities

(b) Puma has four geographic segments – EMEA (Europe, Middle East,

and Africa), Americas (North and Latin America), Asia/Pacific, and

Central units/consolidation. adidas segments are divided

COMPARATIVE ANALYSIS CASE (Continued)

(c) Both companies received unqualified audit opinions. That is, their

*FINANCIAL STATEMENT ANALYSIS CASE

RNA INC.

(a) The calculation of selected financial ratios for RNA for the fiscal year

2019 is as follows:

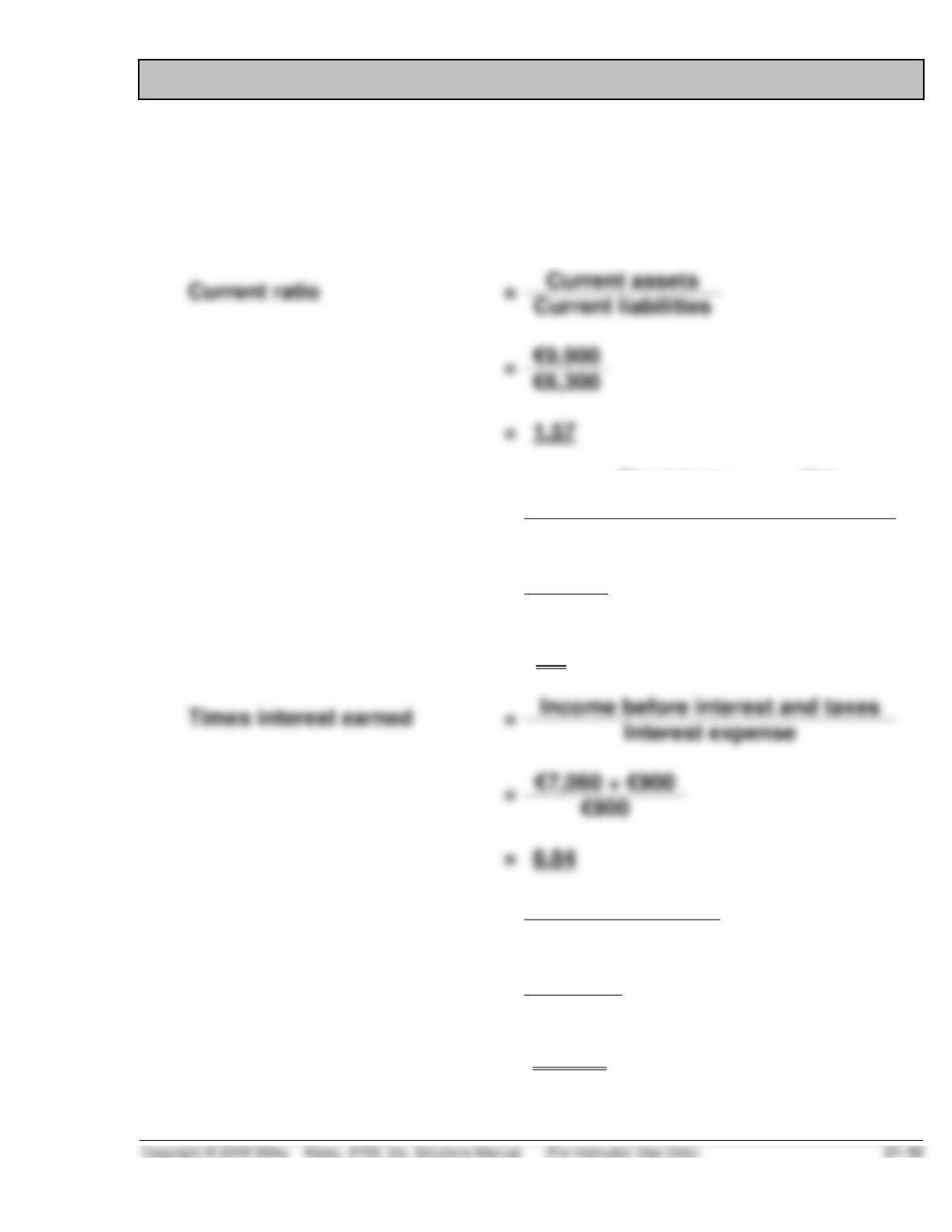

Current ratio

=

Current assets

€9,900

€6,300

Acid-test ratio

=

Short-term Net

Cash + Investments + Receivables

Current liabilities

=

€3,900

€6,300

=

.62

Times interest earned

=

=

=

8.84

Profit margin on sales

=

Net income

Net sales

=

€4,260

€30,500

=

13.97%

*FINANCIAL STATEMENT ANALYSIS CASE (Continued)

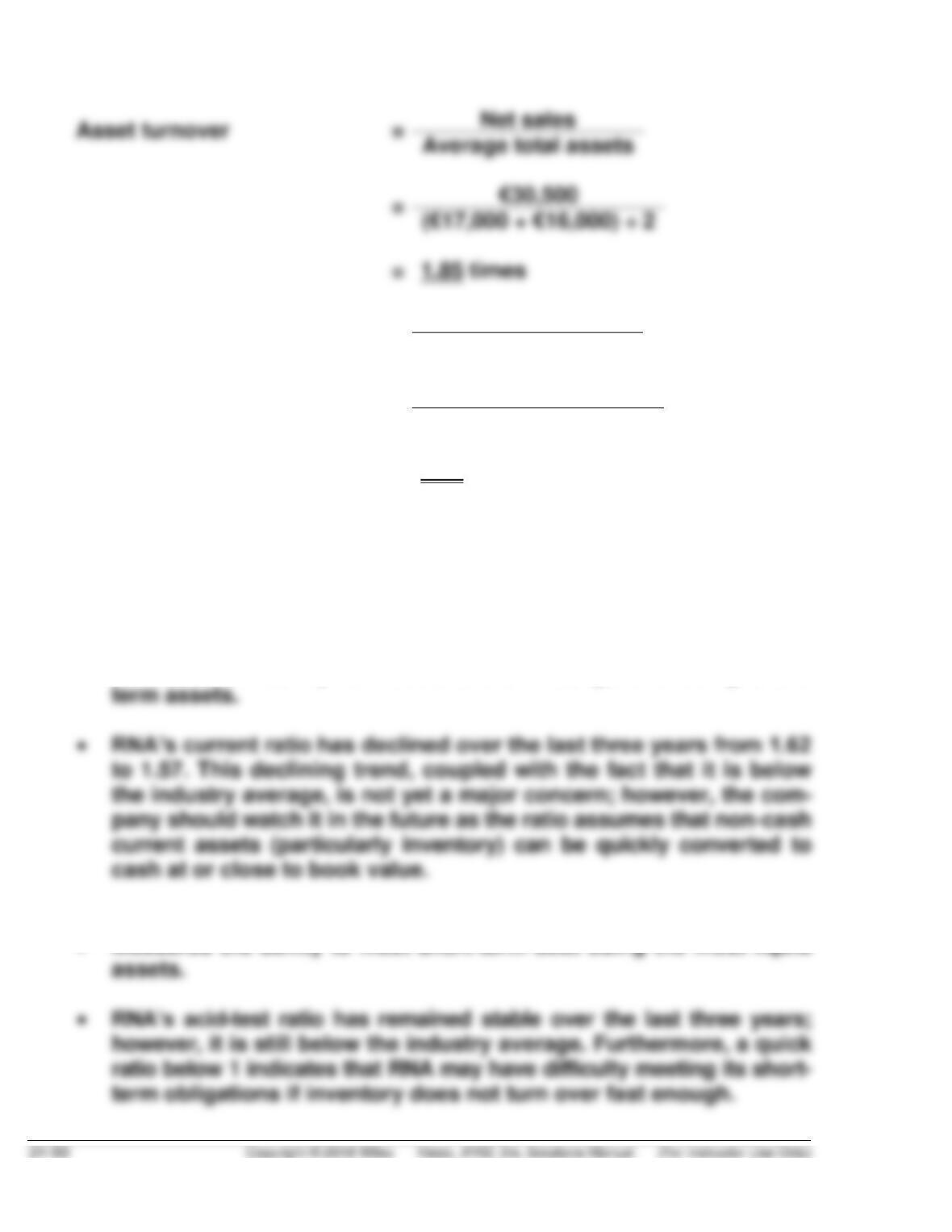

Asset turnover

=

=

€30,500

=

1.85 times

Inventory turnover

=

Cost of goods sold

Average inventory

=

€17,600

(€6,000 + €5,400) ÷ 2

=

3.09 times

(b) The analytical use of each of the six ratios presented above and what

investors can learn about RNA’s financial stability and operating

efficiency are presented below.

Current ratio

• Measures the ability to meet short-term obligations using short-

Acid-test ratio

• Measures the ability to meet short-term debt using the most liquid

*FINANCIAL STATEMENT ANALYSIS CASE (Continued)

Times interest earned

• Measures the ability to meet interest commitments from current

Profit margin on sales

• Measures the net income generated by each dollar of sales. It pro–

Total asset turnover

• Measures the efficiency of resource use; i.e., the ability to generate

Inventory turnover

• Measures how quickly inventory is sold, as well as how effectively

*FINANCIAL STATEMENT ANALYSIS CASE (Continued)

(c) Limitations of ratio analysis include:

• Difficulty making comparisons among firms in the same industry

ACCOUNTING, ANALYSIS, AND PRINCIPLES

ACCOUNTING

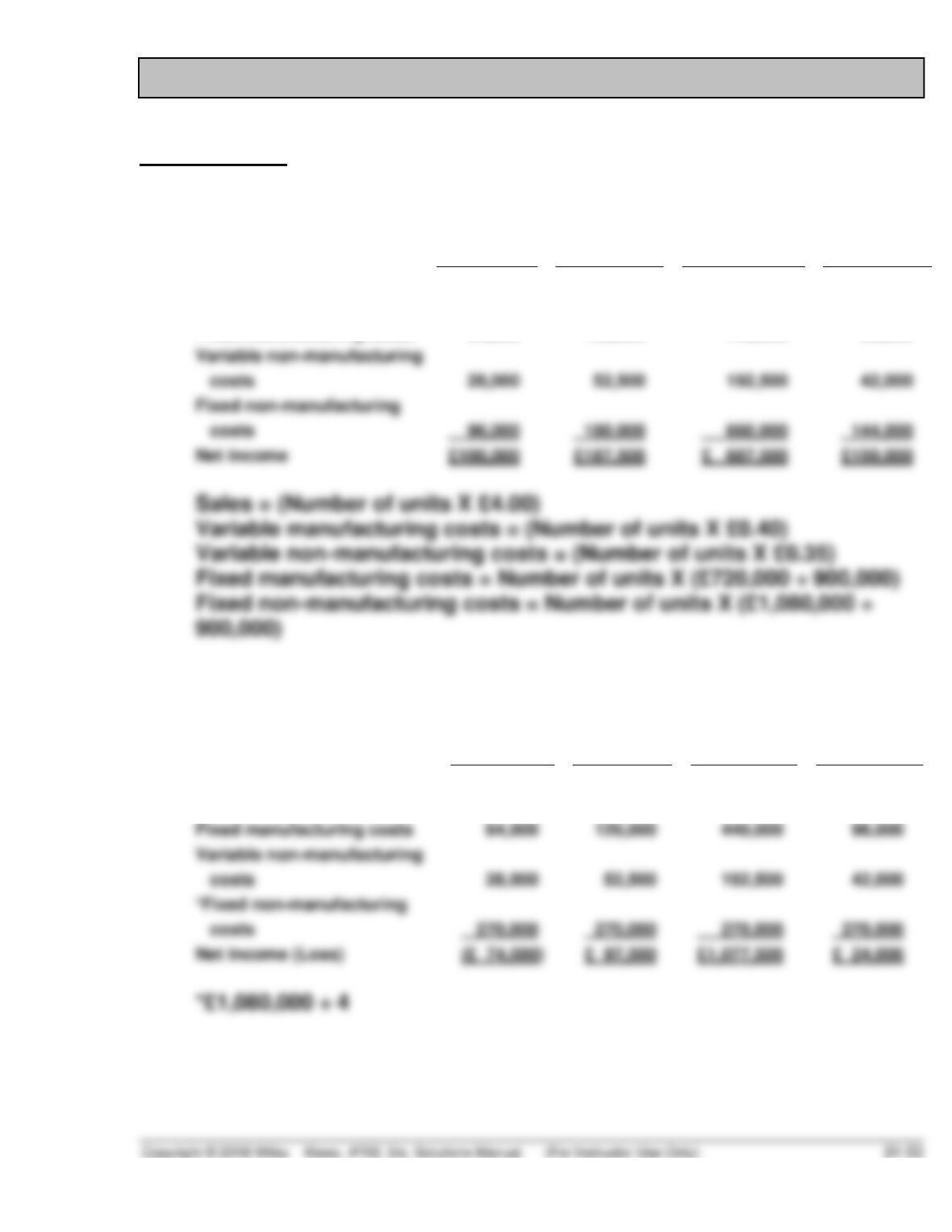

(1) Integral Approach

1st Quarter

2nd Quarter

3rd Quarter

4th Quarter

Sales

£320,000

£600,000

£2,200,000

£480,000

Variable manufacturing costs

32,000

60,000

220,000

48,000

Fixed manufacturing costs

64,000

120,000

440,000

96,000

Net income

(2) Discrete Approach

1st Quarter

2nd Quarter

3rd Quarter

4th Quarter

Sales

£320,000

£600,000

£2,200,000

£480,000

Variable manufacturing costs

32,000

60,000

220,000

48,000

Fixed manufacturing costs

64,000

440,000

96,000

Net income (Loss)

ACCOUNTING, ANALYSIS, AND PRINCIPLES (Continued)

ANALYSIS

Profit margin on sales = Net income ÷ sales

(1) Integral approach:

1st Quarter

2nd Quarter

3rd Quarter

4th Quarter

Net income (Loss)

£100,000

£187,500

£687,500

£150,000

Sales

480,000

Profit margin on sales

(2) Discrete approach:

1st Quarter

2nd Quarter

3rd Quarter

4th Quarter

Net income (Loss)

£ (74,000)

£97,500

£1,077,500

£24,000

Sales

320,000

600,000

2,200,000

480,000

Profit margin on sales

ACCOUNTING, ANALYSIS, AND PRINCIPLES (Continued)

PRINCIPLES

IFRS requires companies to follow the discrete approach. However, compa-

nies should use the same accounting policies for interim reports and for

annual reports.

The concept underlying the integral approach is that an individual quarter

RESEARCH CASE

(a) According to IAS 1, paragraph 117, “An entity shall disclose in the

summary of significant accounting policies:

(1) the measurement basis (or bases) used in preparing the financial

(b) (1) A few examples taken from IAS 1:

• Paragraph 118: It is important for an entity to inform users of the

measurement basis or bases used in the financial statements

• Paragraph 124: Some of the disclosures made in accordance

with paragraph 122 are required by other IFRSs. For example,

IAS 27 requires an entity to disclose the reasons why the entity’s

ownership interest does not constitute control, in respect of an

GAAP CONCEPTS AND APPLICATION

24.1 Following are the key similarities and differences between U.S.

GAAP and IFRS related to disclosures.

Similarities

• U.S. GAAP and IFRS have similar standards on post-statement of

financial position (subsequent) events. That is, under both sets of

standards, events that occurred after the statement of financial

position date, and which provide additional evidence of

conditions that existed at the statement of financial position date,

required.

• Neither U.S. GAAP nor IFRS require interim reports. Rather, the

U.S. SEC and securities exchanges outside the United States

establish the roles. In the United States, interim reports generally

are provided on a quarterly basis; outside the United States, six

month interim reports are common.

Differences

• Due to the narrower range of judgements allowed in more rules-

based U.S. GAAP, more disclosures generally are less expansive

GAAP CONCEPTS AND APPLICATION (Continued)

• As indicated in the About the Numbers section below, U.S. GAAP

uses the date when financial statements are “issued” when

determining the reporting of subsequent events. Subsequent (or

24.2 While U.S. GAAP has a preference for the integral approach, IFRS

leans toward the discrete approach to interim reports. Thus, if an