PROBLEM 22.7 (Continued)

(9)

(10)

Amortization Expense ($50,000 ÷ 10) ………………………….. 5,000

Retained Earnings …………………………………………………….. 5,000

Trademarks ……………………………………………………….. 10,000

LO: 3,4, Bloom: AP, Difficulty: Moderate, Time: 25–30, AACSB: Analytic, AICPA BB: Critical Thinking, AICPA FC: Reporting, AICPA PC: Problem Solving

PROBLEM 22.8

Net Income for 2018

Retained Earnings 12/31/19

Item

Understated

Overstated

Understated

Overstated

1.

£14,100

0

0

0

2.

0

0

4.

£28,000

0

£28,000

0

£18,200

0

0

0

Explanations:

1. The net income would be understated in 2018 because interest income

is understated. The net income would be overstated in 2019 because

2. The depreciation expense in 2018 should be £500 for this machine.

Since the machine was bought on July 1, 2018, only one-half of a year’s

3. IFRS requires that all research costs should be expensed when

incurred. Net income in 2018 is overstated £22,000 (£33,000 research

PROBLEM 22.8 (Continued)

4. The security deposit of £20,000 should be a long-term asset, called

refundable deposits. The £8,000 of the last month’s rent is also an

5. £12,000 or one-third of £36,000 should be reported as income each

year. In 2018, £36,000 was reported as income when only £12,000

6. The ending inventory would be understated since the merchandise was

omitted. Because ending inventory and net income have a direct relation-

PROBLEM 22.9

2018

2019

Net income, as reported

€29,000

€37,000

(1) Rent received in 2018, earned in 2019

(1,000)

1,000

(2) Salaries and Wages not accrued, 12/31/17

1,100

Salaries and Wages not accrued, 12/31/18

1,200

Salaries and Wages not accrued, 12/31/19

(3) Inventory of supplies, 12/31/17

Inventory of supplies, 12/31/18

Inventory of supplies, 12/31/19

Corrected net income

PROBLEM 22.10 (Continued)

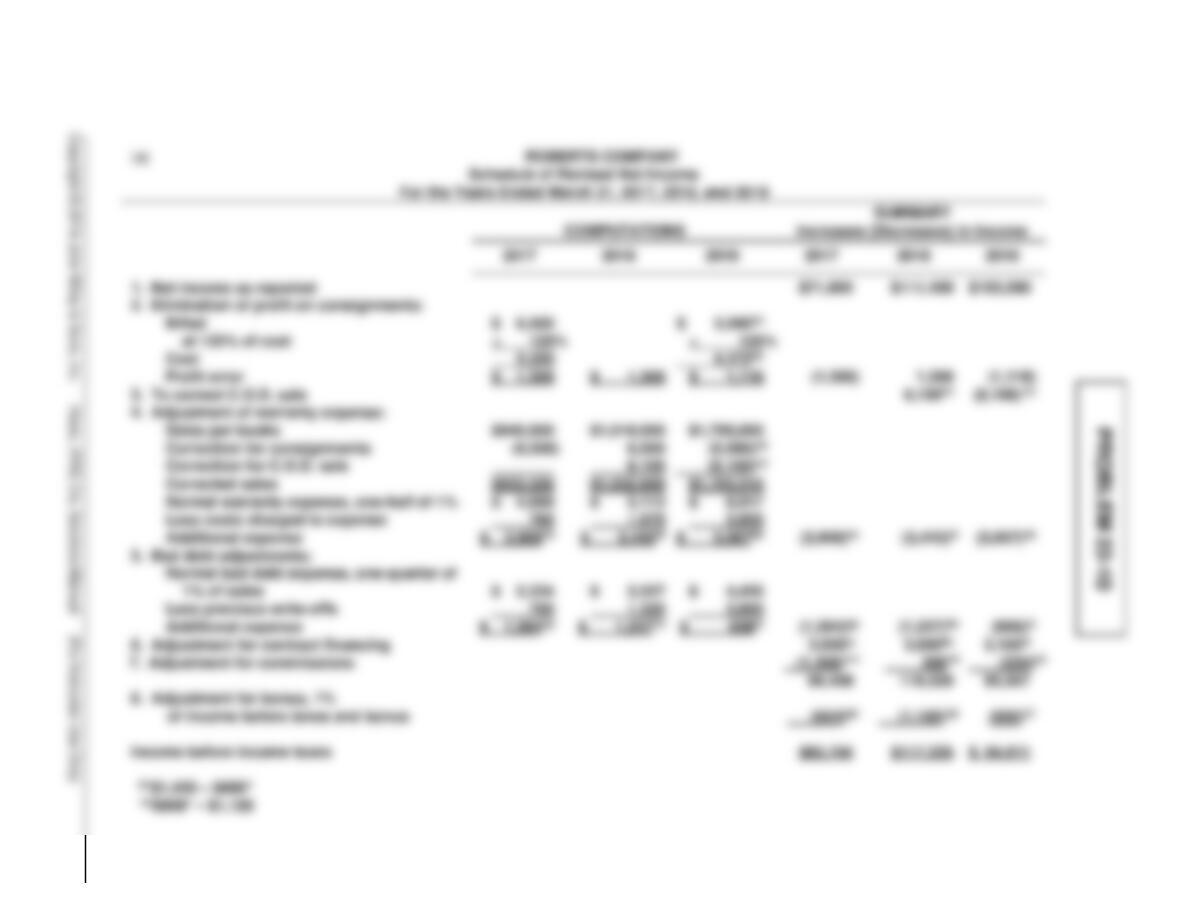

(b) ROBERTS COMPANY

Journal Entries

March 31, 2019

Sales ……………………………………………………………….. 5,590(a)

Inventory on Consignment ………………………………… 4,472(b)

Cost of Goods Sold ……………………………………. 4,472(b)

recorded, 3/31/18)

Warranty Expense …………………………………………….. 5,067(d)

Retained Earnings ($3,908(e) + $3,443(f)) ……………….. 7,351

Estimated Liability Under Warranties ………….. 12,418

($5,067 + $7,351)

(To set up allowance for warranty

expense)

PROBLEM 22.10 (Continued)

Commissions Expense……………………………………………. 220(o)

Retained Earnings ($1,400(m) – $500(m)) ………………………. 900

TIME AND PURPOSE OF CONCEPTS FOR ANALYSIS

CA 22.1 (Time 25–35 minutes)

Purpose—to provide the student with some familiarity with the applications of IFRS related to

correction of an error, plus the necessary reporting requirements for each proposal.

CA 22.2 (Time 20–30 minutes)

Purpose—to provide the student with an understanding of the application and reporting requirements of

CA 22.3 (Time 30–35 minutes)

Purpose—to provide the student with an understanding of IFRS and its respective applications. This case

CA 22.4 (Time 20–30 minutes)

Purpose—to provide the student with an understanding of how changes in accounting can be reflected

in the accounting records to facilitate analysis and understanding of financial statements. This case

treatment that each should be given.

CA 22.5 (Time 20–30 minutes)

Purpose—to provide the student with an opportunity to explain how to account for various accounting

change situations. Explanations for two changes in estimate are communicated in a written letter.

CA 22.6 (Time 20–30 minutes)

SOLUTIONS TO CONCEPTS FOR ANALYSIS

CA 22.1

2. Depreciation.

3. Mathematical Error. This is a correction of an error and prior period adjustment treatment

would be in order.

4. Preproduction Costs—Furniture Division. This should probably be construed as an

inseparability situation in that the change in accounting estimate (period benefited by

5. FIFO to Average-Cost Change. This is a change in accounting policy. Restatement of

6. Percentage-of-Completion. This is a change in accounting policy. Retained earnings

should be adjusted.

(b) The adjustment to the December 31, 2018 retained earnings balance would be computed as

follows:

CA 22.2

Item

Change

Type of Change

Should Prior

Years’ Statements

Be Retrospectively

Applied or Restated?

1.

A change in accounting policy.

Yes

2.

A change in an accounting estimate.

No

3.

in estimate.

4.

Not an accounting change but rather a change in classification.

No

5.

An error correction not involving a change in accounting policy.

accounting.

7.

A change in accounting policy.

Yes

An accounting change involving both a change in accounting

No

CA 22.3

Situation 1.

(a) A change from an accounting policy not generally accepted to one generally accepted is a

correction of an error.

(b) When comparative statements are presented, net income, components of net income, retained

earnings, and any other affected balances for all periods presented should be restated to correct

Situation 2.

(a) The change in method of inventory pricing represents a change in accounting policy, as defined

by IFRS.

CA 22.3 (Continued)

Situation 3.

(a) A change in the depreciable lives of fixed assets is a change in accounting estimate.

CA 22.4

1. This situation is a change in estimate. Whenever it is impossible to determine whether a change

in policy or a change in estimate has occurred, the change should be considered a change in

estimate. A change in estimate employs the current and prospective approach by:

2. This situation is considered a change in estimate because new events have occurred which call

for a change in estimate. The accounting should be the same as discussed in 1.

3. This situation is considered a correction of an error. The general rule is that careful estimates

which later prove to be incorrect should be considered changes in estimates. Where the estimate

was obviously computed incorrectly because of lack of expertise or in bad faith, the adjustment

should be considered an error. Changes due to error should employ the retroactive approach by:

4. No adjustment is necessary—a change in accounting policy is not considered to have happened if

a new policy is adopted in recognition of events that have occurred for the first time.

CA 22.4 (Continued)

6. This situation is considered a change in accounting policy. A change in accounting policy should

employ the retrospective approach by:

CA 22.5

Mr. Joe Davison, CEO Sports-Pro Athletics

Dear Mr. Davison:

You recently contacted me about two accounting changes made at Sports-Pro Athletics, Inc. in 2019.

This letter details how you should account for each change.

CA 22.6

(a) The ethical issues are the honesty and integrity of Frost’s financial reporting practices versus the

Corporation’s and the accounting manager’s profit motives. Shortening the life of fixed assets

from 10 to 6 years may be evidence that depreciation expense during the first five years was

understated. Such a practice distorts Frost’s operating results and misleads users of Frost’s

financial statements. If this practice is intentional, it is unethical.

FINANCIAL REPORTING PROBLEM

(a) According to note 1 (accounting policies – new standards adopted by

the Group), there have been no significant changes to accounting

(b) According to note 1 (accounting policies – critical accounting

estimates and judgements), the estimates M&S discussed in 2016 were

COMPARATIVE ANALYSIS CASE

Puma vs. adidas

(a) and (c) for Puma (according to note 1 – general):

The following new and amended standards and interpretations have been

used for the first time in the current financial year:

(b) and (c) for adidas (according to note 1 – general):

The following new standards and interpretations and amendments to

existing standards and interpretations are applicable for the first time for

financial years beginning on January 1, 2015:

ACCOUNTING, ANALYSIS, AND PRINCIPLES

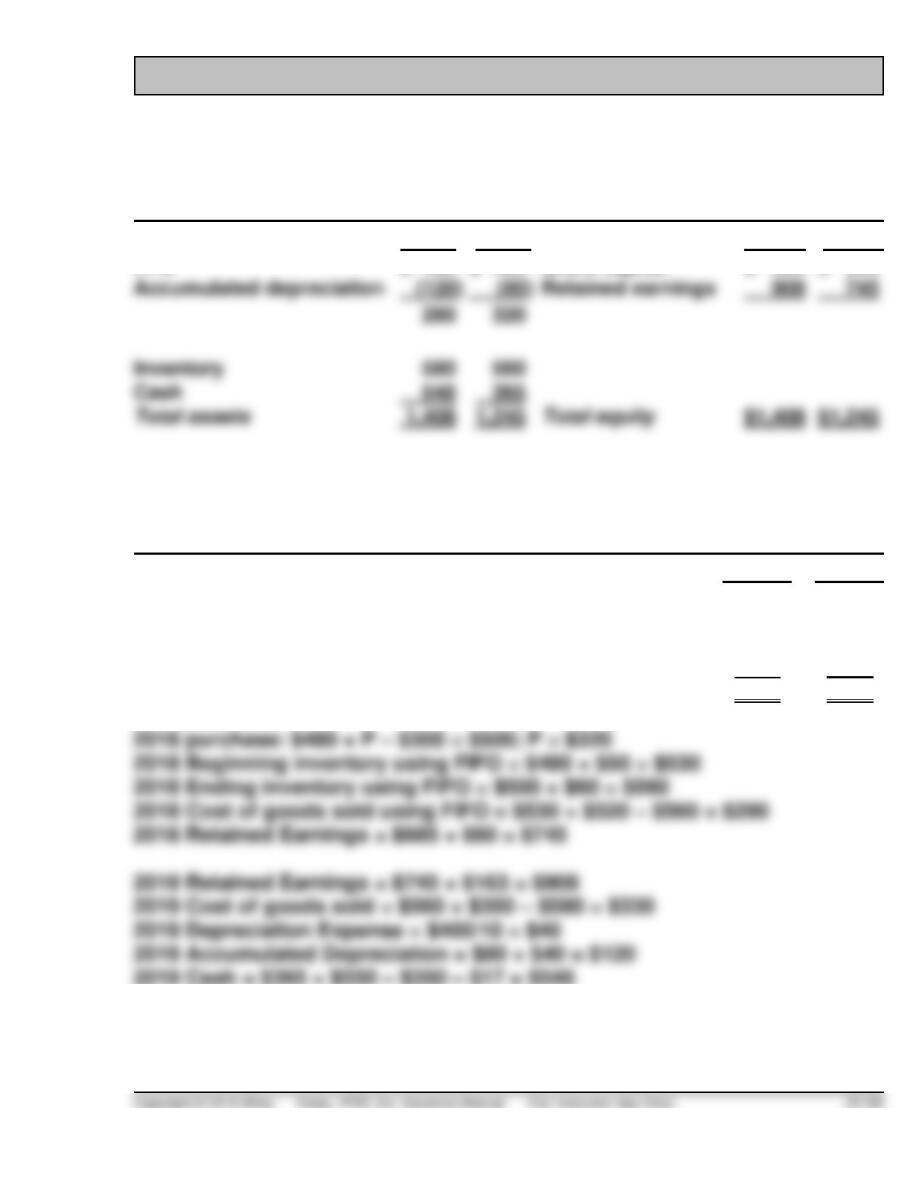

ABC CO.

Statement of Financial Position

at December 31

2019 2018 2019 2018

PPE $ 400 $ 400 Share capital $ 500 $ 500

ABC CO.

Income Statement

for the Year Ended December 31,

2019 2018

Sales ……………………………………………………………………… $550 $500

Cost of goods sold …………………………………………………. 330 290

Depreciation expense …………………………………………….. 40 40

Compensation expense …………………………..……………… 17 15

Net income …………………………………………………………….. $163 $155

ACCOUNTING, ANALYSIS, AND PRINCIPLES (Continued)

ANALYSIS

Average cost (as reported):

Inventory turnover = $300 ÷ $500 = 0.60

FIFO:

PRINCIPLES

The issue is consistency across time. When a company changes accounting

policies, financial statements from one period are not really comparable to

RESEARCH CASE

(b) According to paragraph 14, “An entity shall change in accounting only if

the change:

(1) is required by an IFRS; or

GAAP CONCEPTS and APPLICATION

GAAP22.1 U.S. GAAP absolutely requires restatement of prior financial

statements for all accounting errors while IFRS allows for

GAAP22.2 U.S. GAAP has detailed guidance on the accounting and

reporting of indirect effects. U.S. GAAP requires that indirect

GAAP22.3 There is a difference between U.S. GAAP and IFRS related to

how the investor evaluates the accounting policies of the

investee. For example, if the investee uses an inventory