EXERCISE 10.24 (15–20 minutes)

1/30

Accumulated Depreciation—Buildings ……………………..

95,200*

Loss on Disposal of Machinery …………………………..

21,900**

Buildings ……………………………………………………….

Cash ……………………………………………………….

5,100

**($112,000 – $95,200) + $5,100

3/10

Cash ($2,900 – $300) ………………………………………………..

2,600

Accumulated Depreciation—Machinery …………………….

Loss on Disposal of Machinery …………………………..

Machinery ……………………………………………………….

**($16,000 – $11,200) + $300 – $2,900

3/20

Maintenance and Repairs Expense …………………………..

3,000

Cash ……………………………………………………….

3,000

5/18

Machinery ……………………………………………………….

5,500

Accumulated Depreciation—Machinery …………………….

2,400*

Loss on Disposal of Machinery …………………………..

1,600**

Machinery ……………………………………………………….

4,000

Cash ……………………………………………………….

5,500

**($4,000 – $2,400)

6/23

Maintenance and Repairs Expense …………………………..

6,900

Cash ……………………………………………………….

6,900

EXERCISE 10.25 (10–15 minutes)

(a) C

(b) E, assuming immaterial

EXERCISE 10.26 (20–25 minutes)

(a)

Depreciation Expense (8/12 X ¥72,000) …………………….

48,000

Accumulated Depreciation—Machinery ……………

48,000

Loss on Disposal of Machinery

(¥1,300,000 – ¥408,000) – ¥630,000 ………………………..

Cash ………………………………………………………………………

Accumulated Depreciation—Machinery

(¥360,000 + ¥48,000) …………………………..…………………

Machinery ………………………………………………………

(b)

Depreciation Expense (3/12 X ¥72,000) …………………….

18,000

Accumulated Depreciation—Machinery ……………

18,000

Cash ……………………………………………………………………..

Accumulated Depreciation—Machinery

(¥360,000 + ¥18,000) …………………………..…………………

Machinery ………………………………………………………

Gain on Disposal of Machinery

EXERCISE 10.26 (Continued)

(c)

Depreciation Expense (7/12 X ¥72,000) ……………………..

42,000

Accumulated Depreciation—Machinery …………….

42,000

Contribution Expense ………………………………………………

Accumulated Depreciation—Machinery

(¥360,000 + ¥42,000) ……………………………………………..

402,000

Machinery ……………………………………………………….

Gain on Disposal of Machinery …………………………

202,000*

EXERCISE 10.27 (15–20 minutes)

April 1

Cash ………………………………………………………………………

410,000

Accumulated Depreciation—Buildings ……………………..

160,000

Land ……………………………………………………….

60,000

Buildings ……………………………………………………….

280,000

Gain on Disposal of Plant Assets …………………….

230,000*

Aug. 1

Land ………………………………………………………………………

Buildings ……………………………………………………….

380,000

Cash ……………………………………………………….

470,000

Problem 10.1 (Time 35–40 minutes)

Purpose—to provide a problem involving the proper classification of costs related to property, plant,

and equipment. Property, plant, and equipment must be segregated into land, buildings, leasehold

improvements, and machinery and equipment for purposes of the analysis. Such costs as demolition

costs, real estate commissions, imputed interest, minor and major repair work, and royalty payments

are presented. An excellent problem for reviewing the first part of this chapter.

Problem 10.2 (Time 40–55 minutes)

Purpose—to provide a problem involving the proper classification of costs related to property, plant,

Problem 10.3 (Time 35–45 minutes)

Purpose—to provide a problem involving the proper classification of costs related to land and buildings.

Problem 10.4 (Time 35–40 minutes)

Purpose—to provide a problem involving the method of handling the disposition of certain properties.

Problem 10.5 (Time 20–30 minutes)

Purpose—to provide the student with a problem in which schedules must be prepared for the costs of

acquiring land and the costs of constructing a building. Interest costs are included.

Problem 10.6 (Time 25–35 minutes)

Problem 10.7 (Time 20–30 minutes)

Problem 10.8 (Time 35–45 minutes)

Purpose—to provide the student with a problem involving the exchange of machinery. Four different

Problem 10.9 (Time 30–40 minutes)

Problem 10.10 (Time 30–40 minutes)

Purpose—to provide the student with a problem involving the exchange of productive assets. The

exchange of assets have and do not commercial substance.

Problem 10.11 (Time 35–45 minutes)

SOLUTIONS TO PROBLEMS

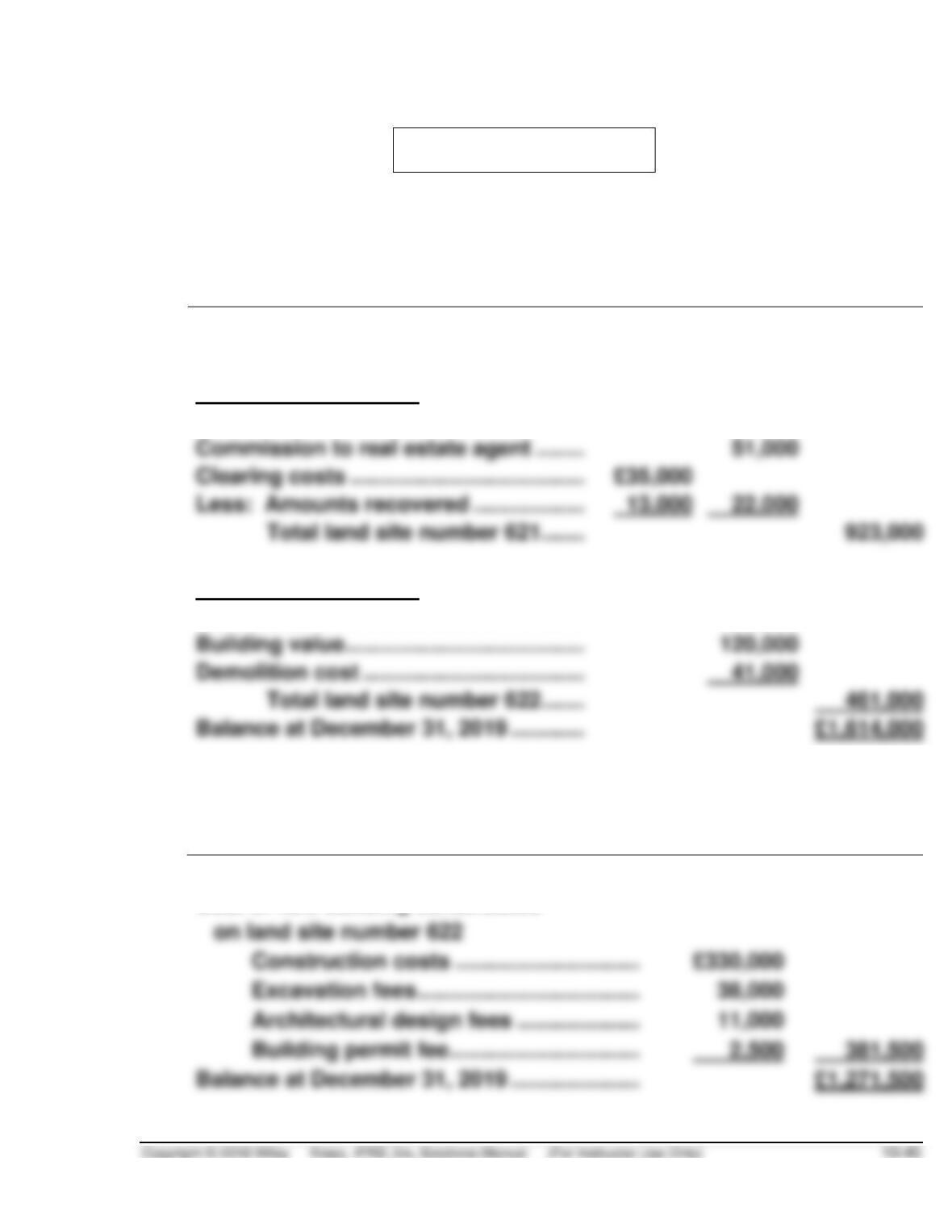

PROBLEM 10.1

(a) REAGAN LTD

Analysis of Land Account

for 2019

Balance at January 1, 2019 ………………

£ 230,000

Land site number 621

Acquisition cost ……………………………..

£850,000

Commission to real estate agent ……..

Clearing costs ………………………………..

Less: Amounts recovered ………………

22,000

Total land site number 621 …….

Land site number 622

Land value ……………………………………..

300,000

Building value …………………………………

120,000

Demolition cost ………………………………

41,000

Total land site number 622 …….

461,000

REAGAN LTD

Analysis of Buildings Account

for 2019

Balance at January 1, 2019 ………………………

£ 890,000

Cost of new building constructed

on land site number 622

Construction costs …………………………

Architectural design fees ………………..

Building permit fee ………………………….

PROBLEM 10.1 (Continued)

REAGAN LTD

Analysis of Leasehold Improvements Account

for 2019

Balance at January 1, 2019 ……………………………………….

£660,000

Office space ……………………………………………………….

89,000

REAGAN LTD

Analysis of Machinery and Equipment Account

for 2019

Balance at January 1, 2019 ……………………………………….

£875,000

Cost of the new machines acquired

Invoice price …………………………………………………..

Freight costs ………………………………………………….

Installation costs …………………………………………….

92,700

(b) Items in the fact situation which were not used to determine the

answer to (a) above are as follows:

1. Interest imputed on equity financing is not permitted by IFRS and

thus does not appear in any financial statement.

PROBLEM 10.2

(a) LOBO CORPORATION

Analysis of Land Account

2019

Balance at January 1, 2019 ………………………………………

$300,000

LOBO CORPORATION

Analysis of Land Improvements Account

2019

Balance at January 1, 2019 ………………………………………

$140,000

LOBO CORPORATION

Analysis of Buildings Account

2019

Balance at January 1, 2019 ………………………………………

$1,100,000

PROBLEM 10.2 (Continued)

LOBO CORPORATION

Analysis of Equipment Account

2019

Balance at January 1, 2019 …………………………..

$ 960,000

Invoice price …………………………………………………..

Freight and unloading costs …………………………..

Sales taxes …………………………………………………….

Installation costs …………………………………………….

459,000

1,419,000

Deduct cost of machines disposed of

Machine scrapped June 30, 2019 ……………………..

$ 80,000*

Machine sold July 1, 2019 …………………………..

44,000*

124,000

Balance at December 31, 2019 …………………………..

PROBLEM 10.2 (Continued)

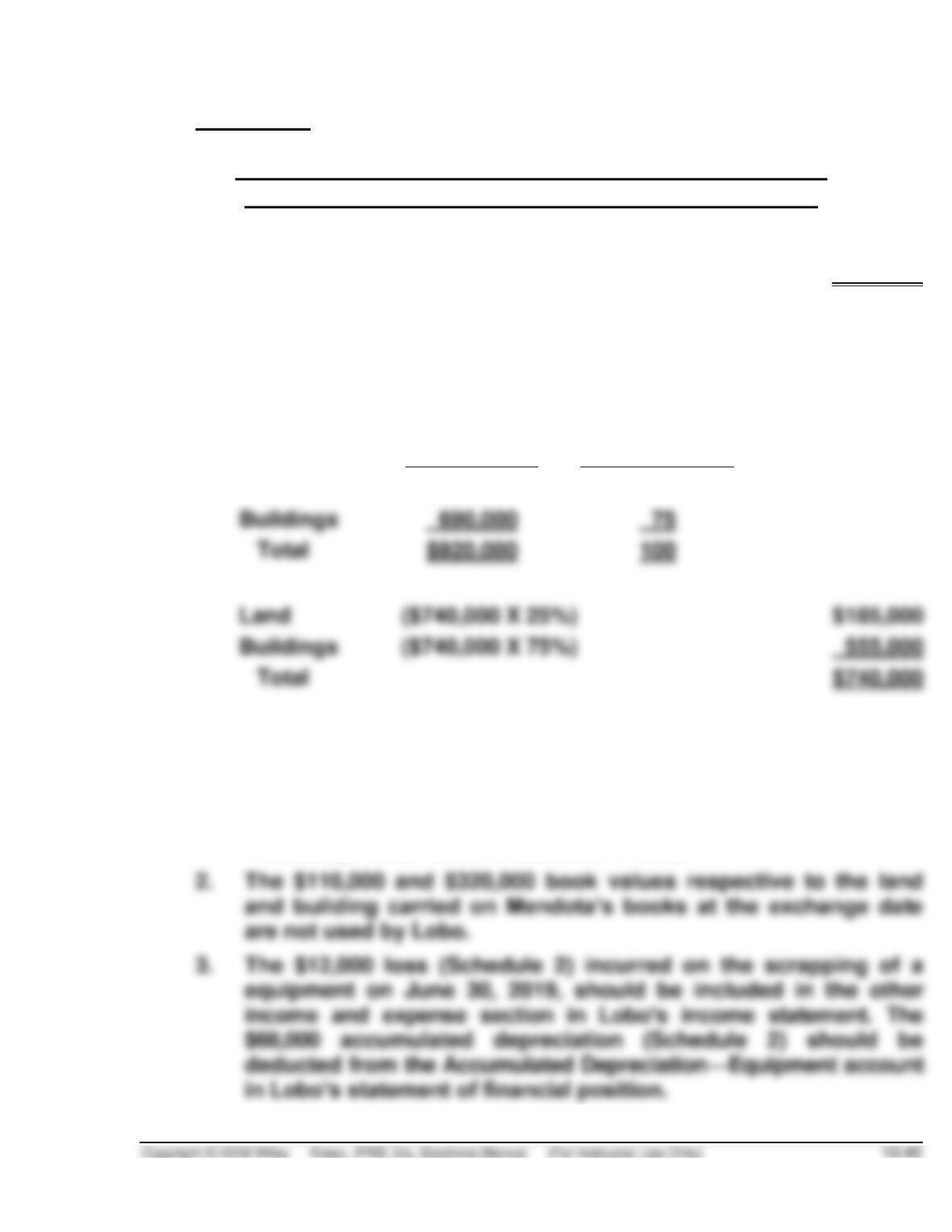

Schedule 1

Computation of Fair Value of Plant Facility Acquired from

Mendota Company and Allocation to Land and Building

20,000 shares of Lobo ordinary shares at $37 quoted

market price on date of exchange (20,000 X $37)

$740,000

Allocation to land and building accounts in proportion

to appraised values at the exchange date:

Amount

Percentage

of total

Land

$230,000

25

Buildings

75

Land

($740,000 X 25%)

Buildings

($740,000 X 75%)

(b) Items in the fact situation that were not used to determine the answer

to (a) above, are as follows:

1. The tract of land, which was acquired for $150,000 as a potential

future building site, should be included in Lobo’s statement of

financial position as an investment in land.

PROBLEM 10.2 (Continued)

4. The $3,000 loss on sale of equipment on July 1, 2019 (Schedule

3) should be included in the other income and expenses section

Schedule 2

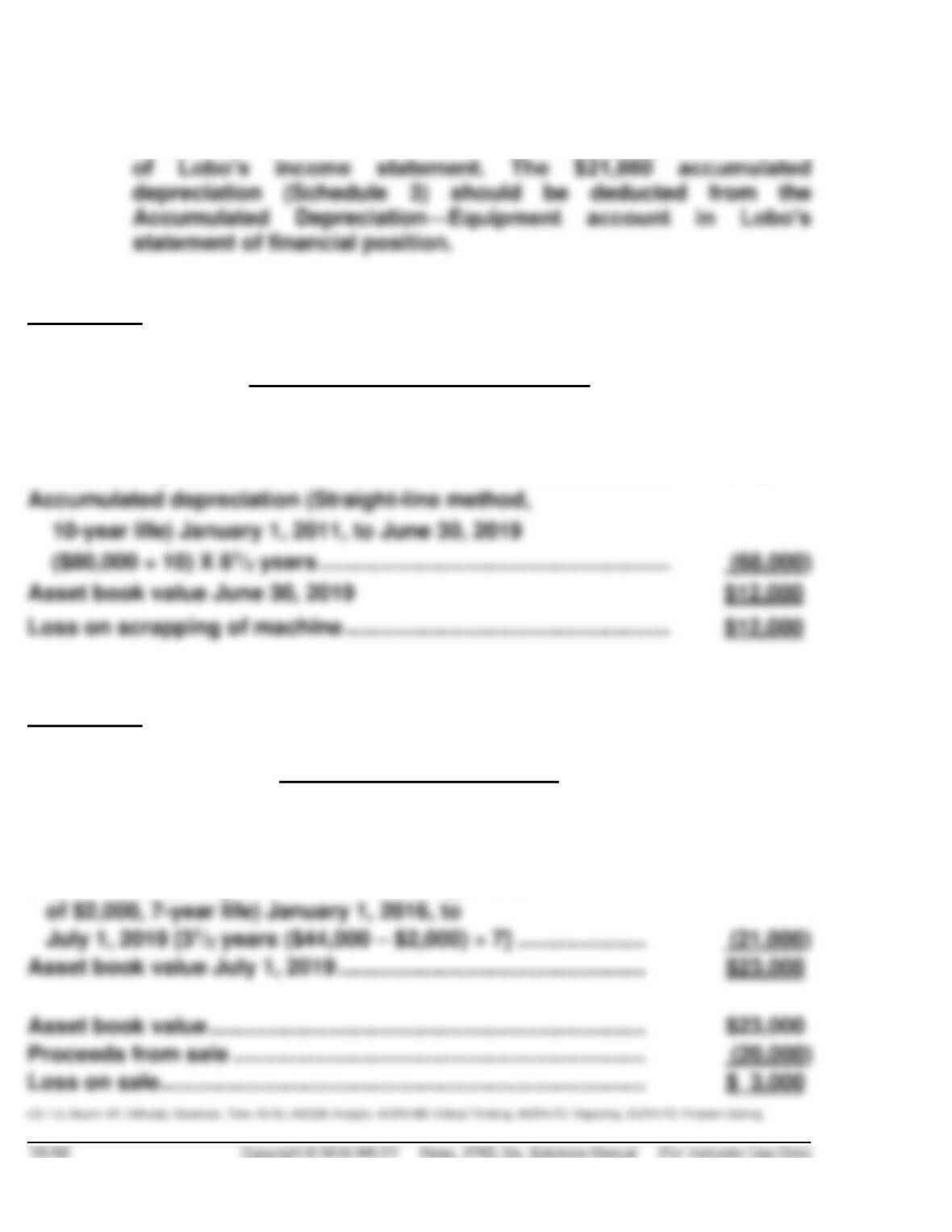

Loss on Scrapping of Equipment

June 30, 2019

Cost, January 1, 2011 …………………………………………………………..

$80,000

Schedule 3

Loss on Sale of Equipment

July 1, 2019

Cost, January 1, 2016 …………………………..…………………………..

$44,000

Asset book value ……………………………………………………………..

$23,000

Proceeds from sale …………………………..……………………………..

Depreciation (straight-line method, salvage value

PROBLEM 10.3

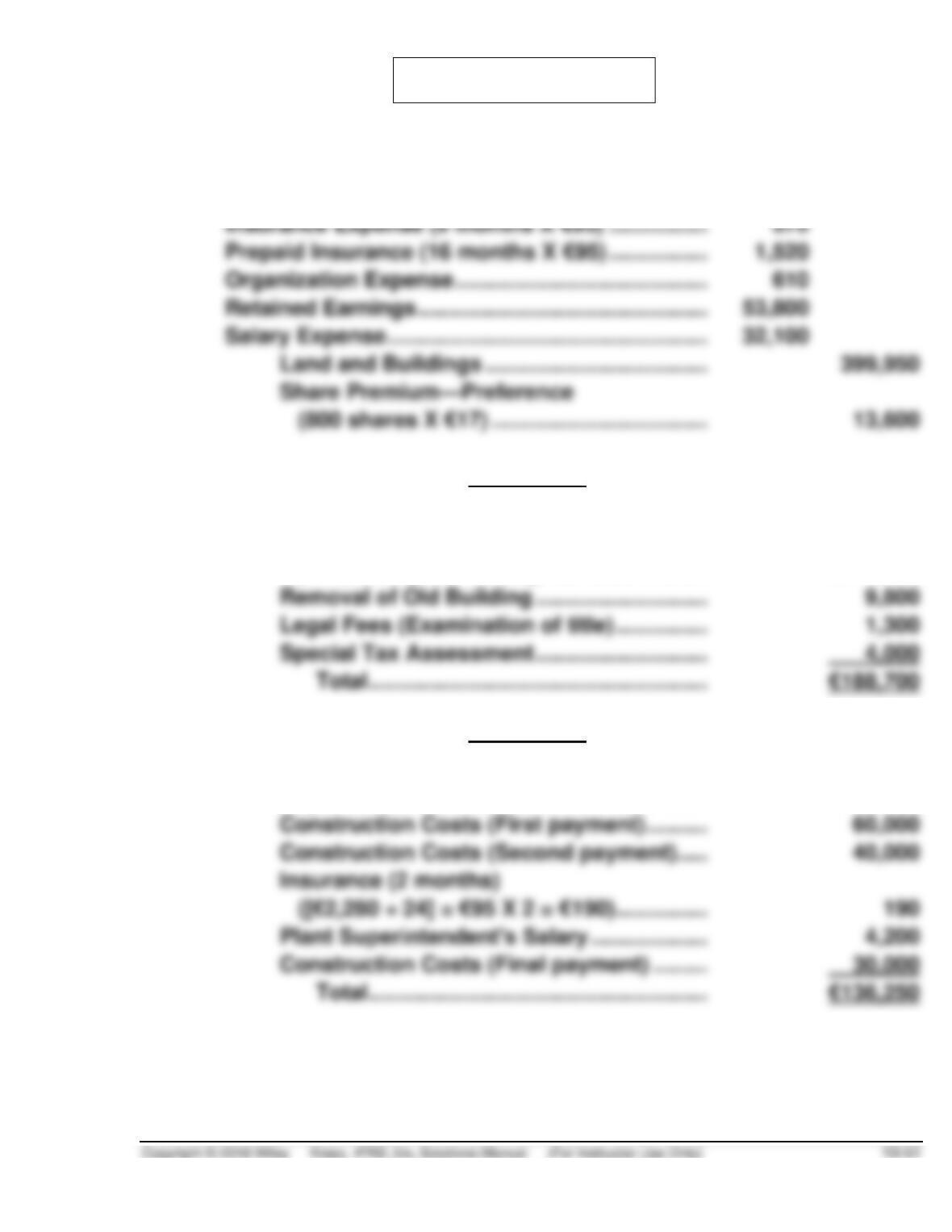

(a)

1.

Land (Schedule A) ………………………………………..

188,700

Buildings (Schedule B) …………………………………

136,250

Insurance Expense (6 months X €95) …………….

Prepaid Insurance (16 months X €95) …………….

Organization Expense …………………………………..

Retained Earnings ………………………………………..

Salary Expense …………………………………………….

Land and Buildings ………………………………

Share Premium—Preference

(800 shares X €17) ……………………………..

Schedule A

Amount Consists of:

Acquisition Cost

(€80,000 + [800 X €117]) ……………………..

€173,600

Removal of Old Building ……………………….

9,800

Legal Fees (Examination of title) ……………

1,300

Special Tax Assessment ……………………….

Schedule B

Amount Consists of:

Legal Fees (Construction contract)………..

€ 1,860

Construction Costs (First payment) ……….

Construction Costs (Second payment) …..

Insurance (2 months)

([€2,280 ÷ 24] = €95 X 2 = €190) ……………

Plant Superintendent’s Salary ……………….

4,200

Construction Costs (Final payment) ………

2.

Land and Buildings ………………………………………

4,000

Depreciation Expense …………………………..

2,637

Accumulated Depreciation—Building …….

1,363

PROBLEM 10.3 (Continued)

Schedule C

Depreciation adjustment …………………..

(b)

Plant, Property, and Equipment:

Land ………………………………………………………..

€188,700

Less: Accumulated depreciation ………………

Total ……………………………………………….

€323,587

PROBLEM 10.4

The following accounting treatment appears appropriate for these items:

Land—The loss on the condemnation of the land of $9,000 ($40,000 – $31,000)

should be reported as an other income and expense item on the income

statement. The $35,000 land purchase has no income statement effect.

Warehouse—The gain on the destruction of the warehouse should be reported

as other income and expense item. The gain is computed as follows:

Insurance proceeds …………………………..……

$74,000

Deduct: Cost ………………………………………..

$70,000

Less: Accumulated depreciation ……….

Machine—The unrecognized gain on the transaction would be computed as

follows:

Fair value of old machine ………………………..

Deduct: Book value of old machine

Cost ………………………………………………….

Less: Accumulated depreciation ………..

PROBLEM 10.4 (Continued)

This gain would be deducted from the fair value of the new machine in

computing the new machine’s cost. The cost of the new machine would be

capitalized at $4,300.

Thus, there is no income effect in the year of the exchange.

Furniture—The contribution of the furniture would be reported as a contri–

PROBLEM 10.5

(a) BLAIR CORPORATION

Cost of Land (Site #101)

As of September 30, 2020

Cost of land and old building ………………………………..

$500,000

Legal fees …………………………………………………………….

Title insurance ……………………………………………………..

(b) BLAIR CORPORATION

Cost of Building

As of September 30, 2020

Fixed construction contract price ………………………….

$3,000,000

Plans, specifications, and blueprints ……………………..

Interest capitalized during 2019 (Schedule) ……………

Interest capitalized during 2020 (Schedule) ……………

Cost of building ……………………………………………….

Schedule

Interest Capitalized During 2019 and 2020

Weighted-Average

Accumulated Construction

Interest to be

PROBLEM 10.6

INTEREST CAPITALIZATION

Balance in the Land Account

Purchase Price ……………………………………………………………..

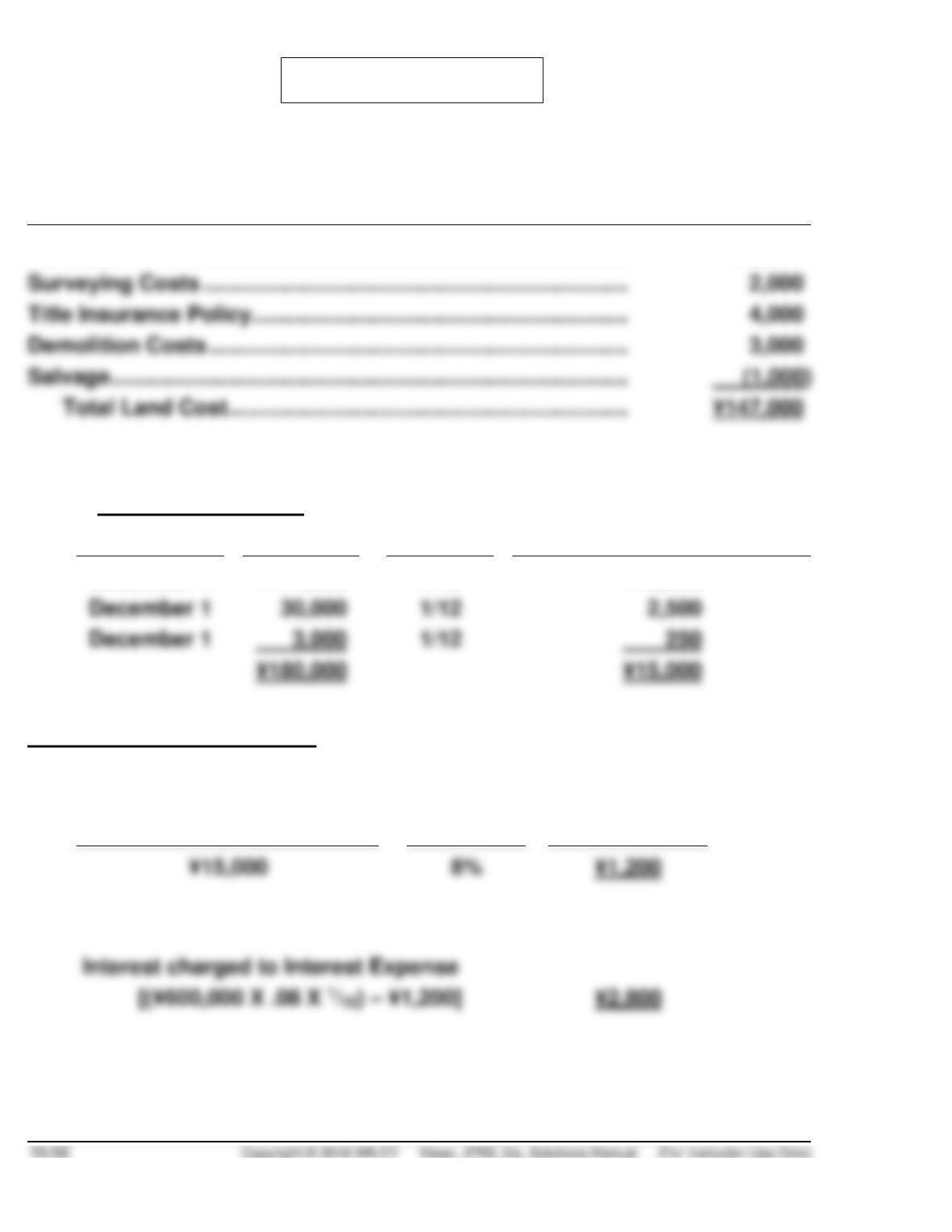

¥139,000

Surveying Costs ……………………………………………………………

Title Insurance Policy …………………………………………………….

Demolition Costs …………………………………………………………..

Salvage …………………………………………………………………………

(1,000)

Expenditures (2019)

Weighted-Average

Accumulated Expenditures

Date

Amount

Fraction

December 1

¥147,000

1/12

¥12,250

December 1

30,000

1/12

2,500

December 1

3,000

1/12

250

Interest Capitalized for 2019

Weighted-Average

Accumulated Expenditures

Interest

Rate

Amount

Capitalizable

PROBLEM 10.6 (Continued)

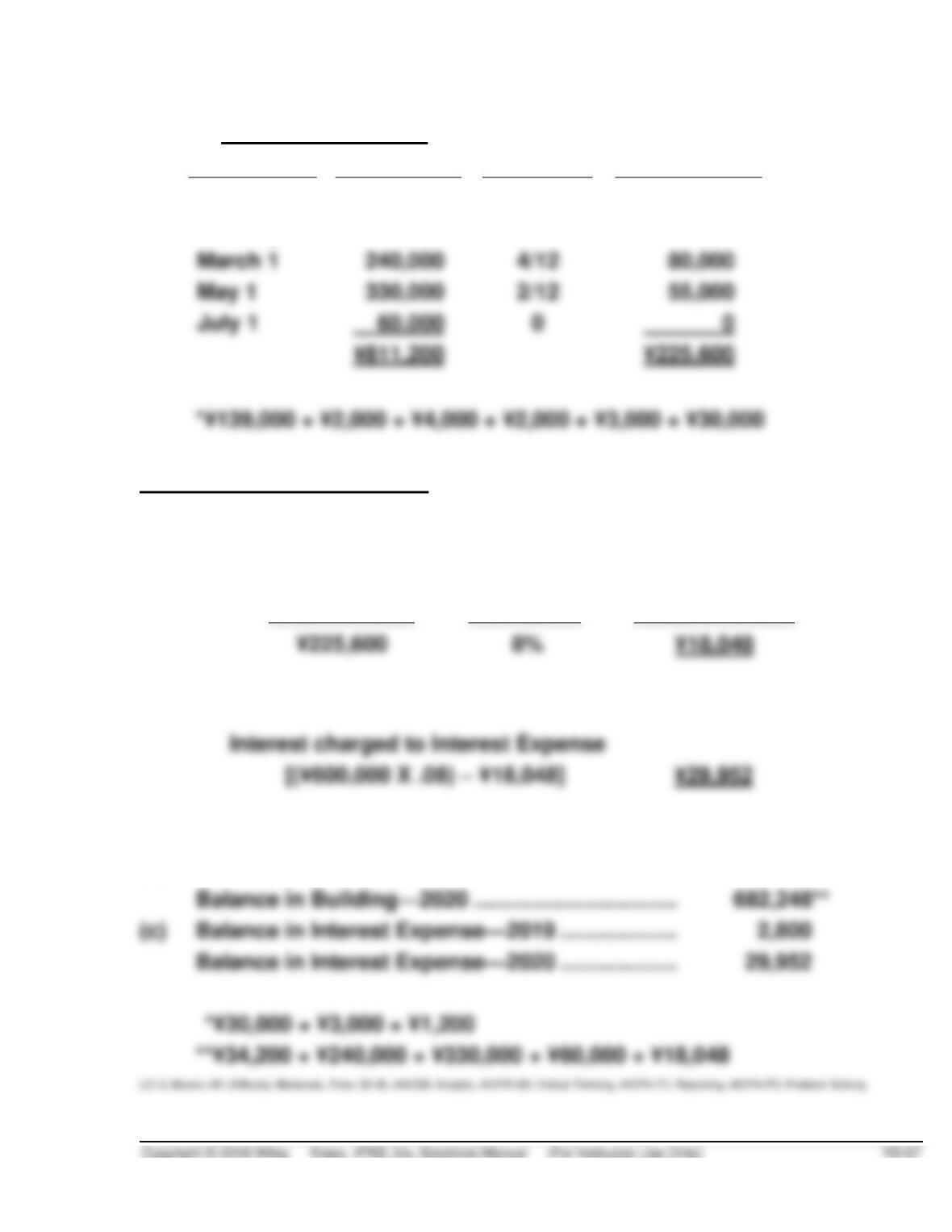

Expenditures (2020)

Fraction

Weighted

Expenditure

Date

Amount

January 1

¥180,000 *

6/12

¥ 90,000

January 1

1,200

6/12

600

March 1

4/12

80,000

May 1

2/12

55,000

July 1

60,000

0

Interest Capitalized for 2020

Weighted-

Average

Expenditure

Interest

Rate

Amount

Capitalizable

(a) Balance in Land Account—2019 and 2020 …….. 147,000

(b) Balance in Building—2019 …………………………... 34,200*

PROBLEM 10.7

(a) Computation of Weighted-Average Accumulated Expenditures

Expenditures

Date

Amount

X

Capitalization

Period

=

Weighted-Average

Accumulated Expenditures

July 30, 2019

₺ 900,000

10/12

₺ 750,000

January 30, 2020

May 30, 2020

(b)

Weighted-Average

Accumulated Expenditures

X

Capitalization

Rate

=

Avoidable

interest

₺1,250,000

11.2%*

₺140,000

Loans Outstanding During Construction Period

(c) (1) and (2)

Total actual interest cost

₺560,000

Less: Total interest capitalized

₺140,000

PROBLEM 10.8

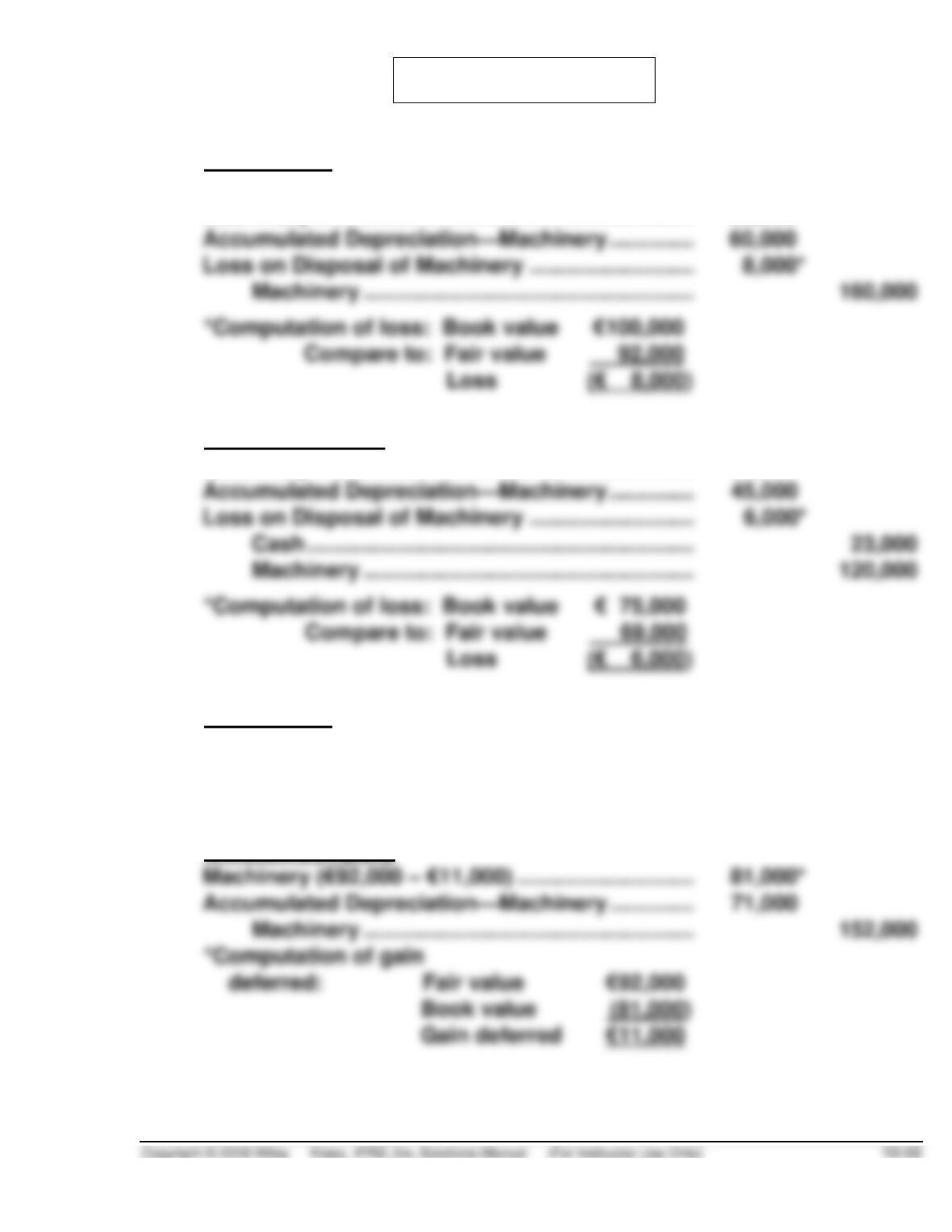

1.

Holyfield SA

Cash ………………………………………………………………

23,000

Machinery …………………………..………………………….

69,000

Accumulated Depreciation—Machinery ……………

60,000

Loss on Disposal of Machinery ……………………….

Machinery ……………………………………………….

160,000

*Computation of loss: Book value

Compare to: Fair value

Dorsett Company

Machinery …………………………..………………………….

92,000

Accumulated Depreciation—Machinery ……………

45,000

Loss on Disposal of Machinery ……………………….

Cash ……………………………………………………….

Machinery ……………………………………………….

120,000

*Computation of loss: Book value

2.

Holyfield SA

Machinery …………………………..………………………….

100,000

Accumulated Depreciation—Machinery ……………

60,000

Machinery ……………………………………………….

160,000

Winston Company

Machinery (€92,000 – €11,000) …………………………

81,000*

Accumulated Depreciation—Machinery ……………

71,000

Machinery ……………………………………………….

152,000

Book value