*PROBLEM 3.11 (Continued)

(b) COOKE NV

Statement of Financial Position

September 30, 2019

Assets

Noncurrent assets

Property, plant, and equipment

Land ……………………………………………………….

€80,000

Equipment ……………………………………………………….

Current assets

Supplies ……………………………………………………….

Prepaid insurance ……………………………………………………….

Cash ……………………………………………………….

Total current assets …………………………..

Equity and Liabilities

Equity

Share capital-ordinary ………………………………………………….

€108,700

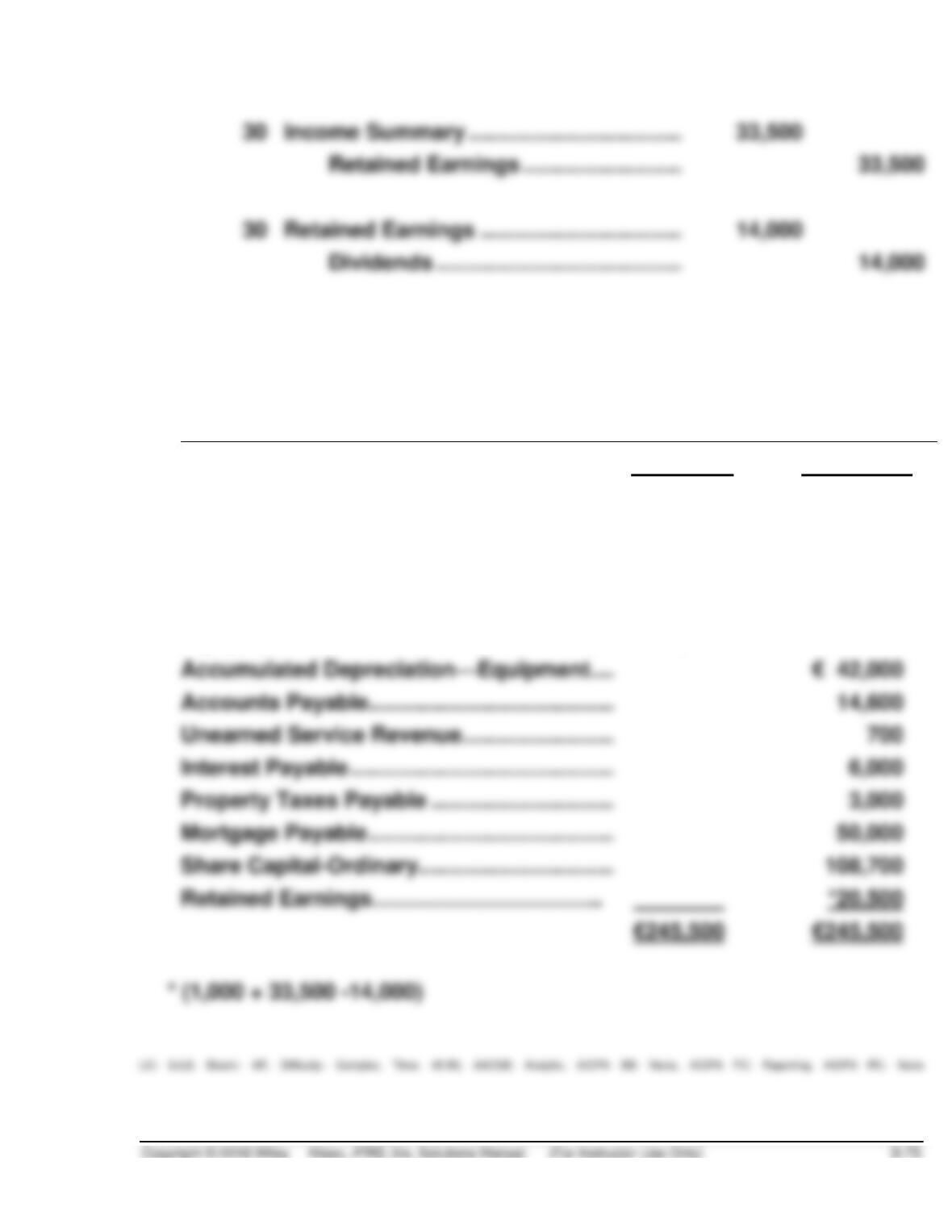

Retained earnings (€1,000 + €33,500 – €14,000) ……………

Liabilities

20,500

129,200

Mortgage payable (50,000 – 10,000) …………………………..

40,000

Current liabilities

Accounts payable ……………………………………………………….

Current maturity of long-term debt …………………………..

Interest payable ……………………………………………………..

Property taxes payable…………………………..

Unearned service revenue …………………………..

Total current liabilities …………………………..

Total liabilities ……………………………………………………

*PROBLEM 3.11 (Continued)

(c)

Sep. 30

Insurance Expense ……………………………………………………….

28,000

Prepaid Insurance …………………………..

28,000

30

Supplies Expense …………………………..…………………………..

14,400

Supplies ……………………………………………………….

14,400

Depreciation Expense …………………………..

5,800

Equipment ……………………………………………………….

5,800

30

Unearned Service Revenue …………………………..

2,000

Service Revenue ……………………………………………………….

2,000

30

Property Tax Expense …………………………..

3,000

Property Taxes Payable …………………………..

3,000

30

Interest Expense …………………………..…………………………..

6,000

Interest Payable ……………………………………………………….

6,000

(d)

Sep. 30

Service Revenue ……………………………………………………….

280,500

Income Summary …………………………..

280,500

30

Income Summary ……………………………………………………….

247,000

Salaries and Wages Expense …………………………..

109,000

Maintenance and Repairs Expense …………………………..

30,500

Insurance Expense …………………………..

28,000

Property Tax Expense …………………………..

21,000

Supplies Expense …………………………..

14,400

Utilities Expense ……………………………………………………….

16,900

Interest Expense ……………………………………………………….

12,000

Advertising Expense …………………………..

9,400

Depreciation Expense …………………………..

5,800

*PROBLEM 3.11 (Continued)

Income Summary ……………………………………………………….

Retained Earnings …………………………..

Retained Earnings ……………………………………………………….

Dividends ……………………………………………………….

(e) COOKE NV

Post-Closing Trial Balance

September 30, 2019

Debit

Credit

Cash ……………………………………………………….

€ 37,400

Supplies ……………………………………………………….

4,200

Prepaid Insurance ……………………………………………………

3,900

Land ……………………………………………………….

80,000

Equipment ……………………………………………………….

120,000

Accumulated Depreciation—Equipment …………………….

Accounts Payable …………………………………………………….

Unearned Service Revenue…………………………..

Interest Payable ……………………………………………………….

Property Taxes Payable …………………………..

Mortgage Payable …………………………………………………….

Share Capital-Ordinary …………………………..

Retained Earnings…………………………..

FINANCIAL REPORTING PROBLEM

(a) April 2, 2016 total assets: £8,476.4 million.

March 28, 2015 total assets: £8,196.1 million.

(e) An adjusting entry for deferrals is necessary when the receipt/

disbursement precedes the recognition in the financial statements.

Accounts such as property, plant, and equipment and depreciation

expense on property, plant, and equipment, for example, is a classic

adjusting entry related to a deferral.

COMPARATIVE ANALYSIS CASE

(a) adidas percentage increase is computed as follows:

Total assets (December 31, 2015) ……………………………………………..

€ 13,343

Total assets (December 31, 2014) ……………………………………………..

(€12,417)

Total assets (December 31, 2015) ……………………………………………..

Total assets (December 31, 2014) ……………………………………………..

(b) adidas has a loss from discontinued operators, net of tax of €46

million. Puma did not have any discontinued operators. Since

discontinued operations are considered to be nonrecurring, they

should be excluded before comparing results between the two

companies.

FINANCIAL STATEMENT ANALYSIS CASE

ACCOUNTING ANALYSIS, AND PRINCIPLES

ACCOUNTING

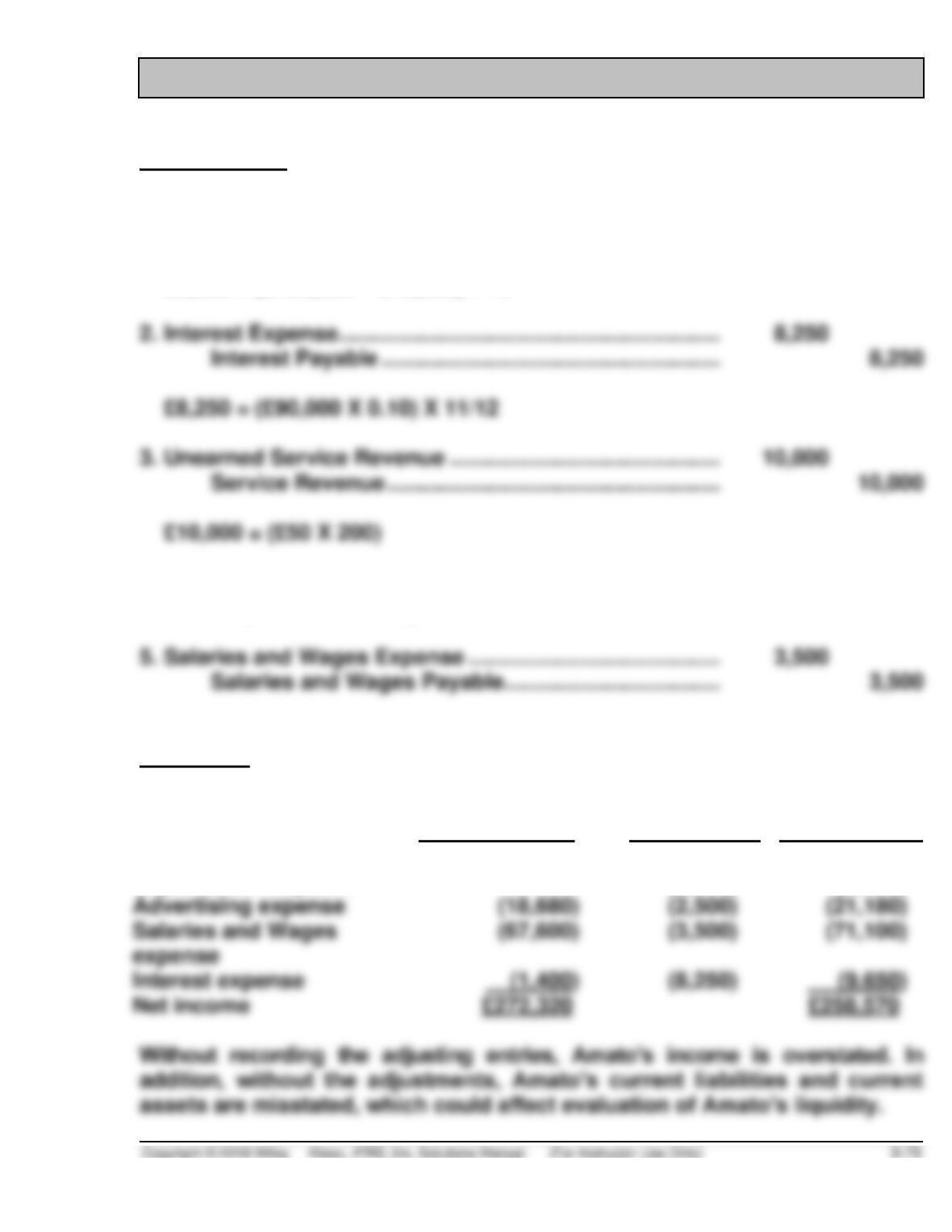

1. Depreciation Expense …………………………………………….. 9,500

Accumulated Depreciation—Equipment ……………. 9,500

£9,500 = (£192,000 – £40,000) ÷ 16

4. Advertising Expense ………………………………………………. 2,500

Prepaid Advertising …………………………………………. 2,500

ANALYSIS

Income before

Adjustments

Adjustments

Income after

Adjustments

Service revenue

£360,000

£10,000

£370,000

Depreciation expense

(9,500)

(9,500)

Net income

£272,320

£258,570

ACCOUNTING ANALYSIS PRICIPLES (Continued)

PRINCIPLES

The tradeoffs are between the timeliness of the reports, which contributes

to relevance, and verifiability, the lack of which detracts from faithful

RESEARCH CASE

(a) Assets

53 The future economic benefit embodied in an asset is the potential to

contribute, directly or indirectly, to the flow of cash and cash

equivalents to the entity. The potential may be a productive one that is

55 The future economic benefits embodied in an asset may flow to the

entity in a number of ways. For example, an asset may be:

a. used singly or in combination with other assets in the production of

(b) Liabilities

60 An essential characteristic of a liability is that the entity has a

present obligation. An obligation is a duty or responsibility to act or

perform in a certain way. Obligations may be legally enforceable as a

consequence of a binding contract or statutory requirement. This is

RESEARCH CASE (Continued)

61 A distinction needs to be drawn between a present obligation and a

future commitment. A decision by the management of an entity to

acquire assets in the future does not, of itself, give rise to a present

62 The settlement of a present obligation usually involves the entity

giving up resources embodying economic benefits in order to satisfy

the claim of the other party. Settlement of a present obligation may occur

in a number of ways, for example, by:

a. payment of cash;

(c) Accrual basis

22 In order to meet their objectives, financial statements are prepared on

the accrual basis of accounting. Under this basis, the effects of

transactions and other events are recognised when they occur (and not

GAAP Concepts and Application

GAAP 3.1

No, all international companies are not subject to the same internal control

GAAP 3.2

There is concern that the cost of complying with the higher internal control

provisions is making U.S. markets less competitive as a place to list

GAAP 3.3

As with accounting standards, there are differences in auditing standards

across international jurisdictions. In the U.S., auditors of public companies

are regulated by the Public Company Accounting Oversight Board