*CA 18.9

(a) Widjaja Group should recognize revenue as it performs the work on the contract (the percentage-

of-completion method) because it meets the criteria for revenue recognition over time.

(b) Progress billings would be accounted for by increasing accounts receivable and increasing progress

(c) The income recognized in the second year of the four-year contract would be determined using

the cost-to-cost method of determining percentage of completion as follows:

1. The estimated total income from the contract would be determined by deducting the estimated

total costs of the contract (the actual costs to date plus the estimated costs to complete) from

the contract price.

(d) Earnings per share in the second year of the four-year contract would be higher using the

percentage-of-completion method instead of the cost-recovery method because income would be

recognized in the second year of the contract using the percentage-of-completion method,

FINANCIAL REPORTING PROBLEM

(a) 2016 Revenues: £10,555.4 million.

(c) M&S’s revenue comprises sales of goods to customers outside the

COMPARATIVE ANALYSIS CASE

(a) For the year 2015, adidas reported net sales of €16,915 million and

(b) Yes, revenue recognition policies are similar because both companies

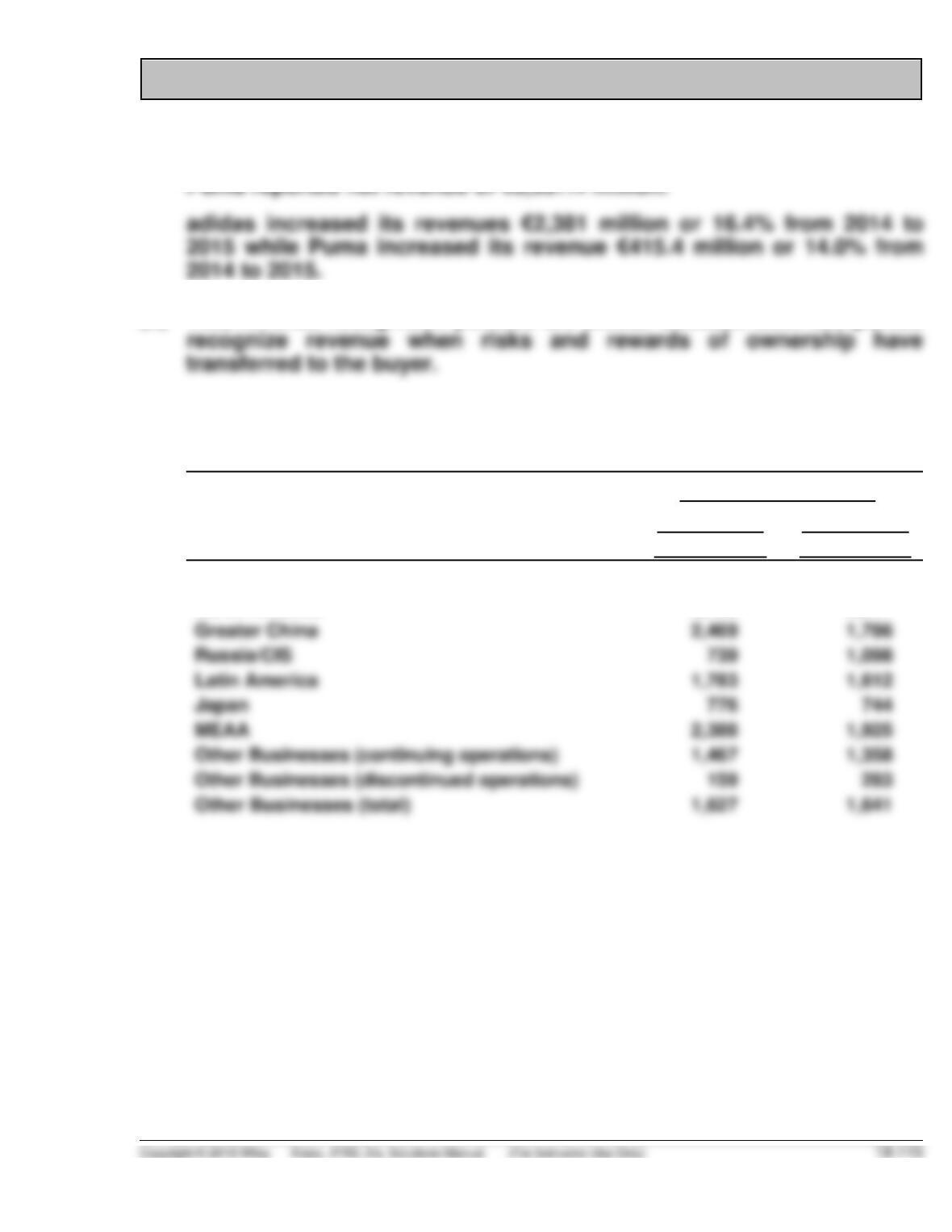

(c) adidas segment revenues for the following geographic regions:

Geographical information (€ in millions)

Net sales (non-Group)

Year ending

Dec 31, 2015

Year ending

Dec 31, 2014

Western Europe

4,539

3,793

North America

2,753

2,217

Greater China

2,469

1,786

Russia/CIS

739

1,098

Latin America

1,783

1,612

Japan

776

744

MEAA

2,388

1,925

Other Businesses (continuing operations)

1,467

1,358

Other Businesses (discontinued operations)

159

283

Other Businesses (total)

1,627

1,641

COMPARATIVE ANALYSIS CASE (Continued)

Puma reported sales by region, as follows:

Region

External Sales

1-12/2015

€ million

EMEA

1,165.8

Central units/consolidation

FINANCIAL STATEMENT ANALYSIS CASE

BRITISH AIRWAYS

(a) British Airways (BA) primarily provides services; it recognizes passen–

ger and cargo revenue when the transportation service is provided.

Specifically, passenger tickets (net of discounts) are recorded as

current liabilities (deferred revenue on ticket sales) until the flights

occur. Other revenue is recognized at the time the service is provided.

(b) BA’s methods are entirely consistent with acceptable IFRS for the

(c) In this disclosure, BA is describing its ticketing operation and the judg-

ments involved to estimate revenue to be recognized on unused

ACCOUNTING, ANALYSIS, AND PRINCIPLES

Accounting

Sales revenue …………………………………………………………….. $9,500,000

* Since the sump-pump and installation bundle are delivered at the same

time, there are two performance obligations. Any discount is applied to

the pump/installation bundle. The total transaction price of $54,600 is

allocated between the equipment and installation ($43,800) and the

service contract ($10,800 [$10 X 36 X 30]).

Sales revenue …………………………………………….. $43,800

** [$7 X 36 X 30]

*** Sales revenue (200 X $1,200) …………………… $240,000

ACCOUNTING, ANALYSIS, AND PRINCIPLES (Continued)

Analysis

Net income ………………………………………………………………………. $1,894,000

Depreciation expense ………………………………………………………. 175,000

Free cash flow …………………………………………………………………. $1,199,000

Principles

Under the 5-step model, a company first identifies the contract with

As indicated, a company satisfies its performance obligation when the

customer obtains control of the good or service. Companies satisfy

performance obligations either at a point in time or over a period of time.

Companies recognize revenue over a period of time if (1) the customer

controls the asset as it is created or the company does not have an

alternative use for the asset, and (2) the company has a right to payment.

Using control as a key element contributes to relevance because it

indicates the cash flows that the seller is entitled to as a result of the

ACCOUNTING, ANALYSIS, AND PRINCIPLES (Continued)

Faithful representation may be sacrificed in situations companies must

allocate the transaction price to more than one performance obligation in a

contract. If an allocation is needed, the transaction price allocated to the

RESEARCH CASE

(a) Sale with a Right of Return is addressed at IFRS 15 para B20.

(b) According to IFRS 15 B20-B22 related to right of return:

In some contracts, an entity transfers control of a product to a

customer and also grants the customer the right to return the product

example, a customer may request an entity to enter into such a

contract because of the customer’s lack of available space for the

product or because of delays in the customer’s production schedules.

(c) According to IFRS 15, para B21:

To account for the transfer of products with a right of return (and for

RESEARCH CASE (Continued)

c. An asset (and corresponding adjustment to cost of sales) for its

right to recover products from customers on settling the refund

liability.

(d) According to IFRS 15, B80:

81 – An entity should determine when it has satisfied its performance

obligation to transfer a product by evaluating when a customer

obtains control of that product (see paragraph IFRS 15 para 35).

For some contracts, control is transferred either when the

product is delivered to the customer’s site or when the product is

In addition to applying the guidance in paragraph IFRS 15 para 35,

for a customer to have obtained control of a product in a bill-and-

hold arrangement, all of the following criteria must be met:

a. The reason for the bill-and-hold arrangement must be

substantive (for example, the customer has requested the

arrangement).

RESEARCH CASE (Continued)

82 – If an entity recognises revenue for the sale of a product on a bill–

and-hold basis, the entity should consider whether it has