EXERCISE 20.8 (Continued)

(c) Accumulated OCI at December 31, 2019 is €1,700; this amount is

comprised of the following:

Gain/Loss

Balance Jan. 1, 2019

€ 0

Asset loss*

Balance Dec. 31, 2019

€ 1,700 Dr.

20–23 Copyright © 2018 Wiley Kieso, IFRS, 3/e, Solutions Manual (For Instructor Use Only)

(a) WEBB CORP.

Pension Worksheet

General Journal Entries

Memo Record

Items

Annual

Pension

Expense

Cash

OCI—

Gain/Loss

Pension

Asset/

Liability

Defined

Benefit

Obligation

Plan Assets

EXERCISE 20.9 (20–25 minutes)

EXERCISE 20.10 (20–30 minutes)

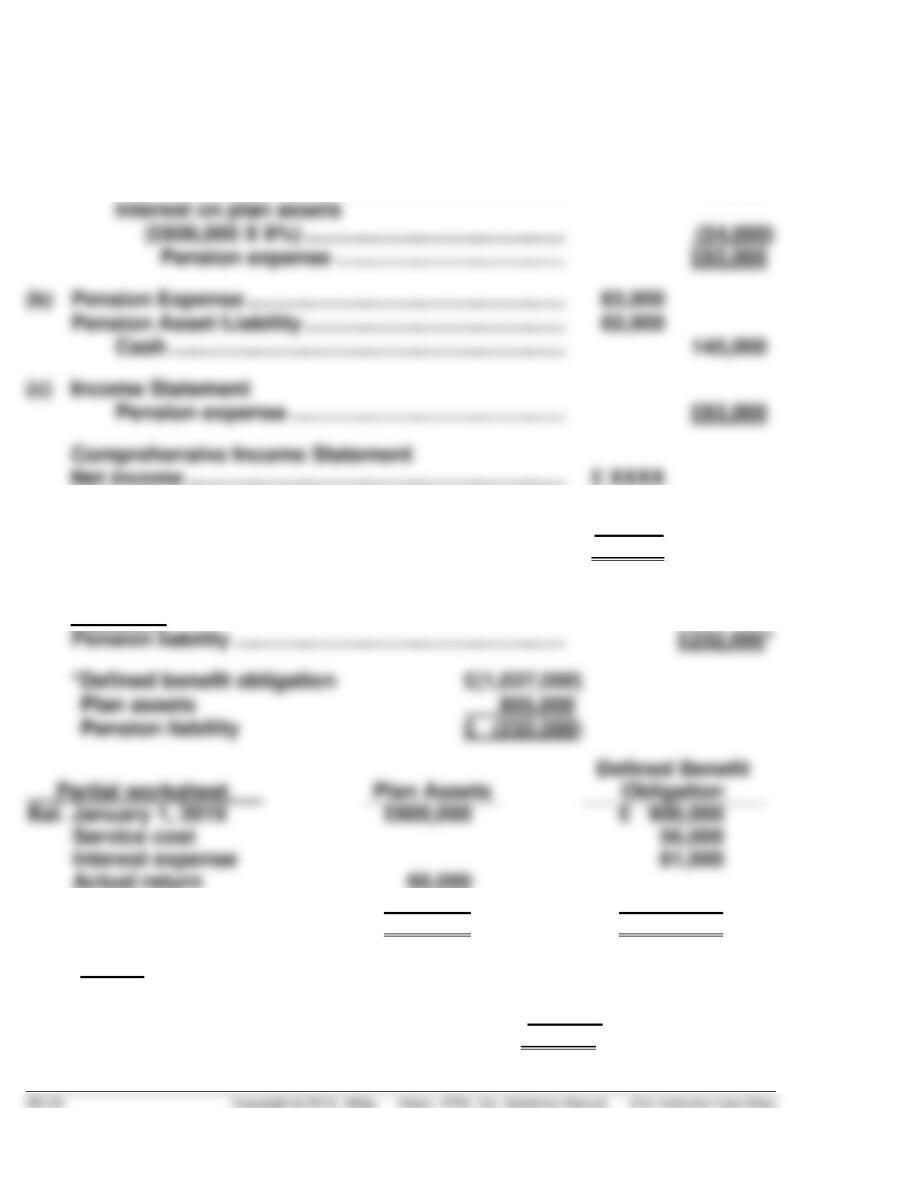

(a) Pension expense for 2019 composed of the following:

Service cost ………………………………………………. £56,000

Interest expense

(9% X £900,000) ……………………………………… 81,000

Other comprehensive income

Asset gain (£60,000 – £54,000) ………………………… 6,000

Comprehensive income…………………………………….. £ XXXX

Statement of Financial Position

Liabilities

Partial worksheet

Bal. January 1, 2019

£ 900,000

Service cost

Interest expense

Actual return

Contribution

145,000

Bal. December 31, 2019

£805,000

£1,037,000

Equity

Accumulated OCI (G/L) Jan. 1, 2019 £40,000 (Loss)

Asset gain 6,000

Accumulated OCI (G/L) Dec. 31, 2019 £34,000 (Loss)

LO: 5, Bloom: AP, Difficulty: Moderate, Time: 20–30, AACSB: Analytic, AICPA BB: Critical Thinking, AICPA FC: Reporting, AICPA PC: Problem Solving

EXERCISE 20.11 (20–30 minutes)

(a) Pension expense for 2019 composed of the following:

Service cost …………………………………………… € 77,000

Interest expense

(c) Income Statement:

Pension expense ……………………………………. € 147,000

Comprehensive Income Statement

Net income …………………………………………….. € XXXX

Other comprehensive income (loss)

Liability gain …………………………………….. 200,000

LO: 3,4,5, Bloom: AP, Difficulty: Moderate, Time: 20–30, AACSB: Analytic, AICPA BB: Critical Thinking, AICPA FC: Reporting, AICPA PC: Problem Solving

EXERCISE 20.12 (35–45 minutes)

(a) Actual Return = (Ending – Beginning) – (Contributions – Benefits)

Fair value of plan assets,

(b) Computation of pension liability gains and losses and pension asset gains and losses.

1. Difference between 12/31/19 actuarially computed DBO and 12/31/19 recorded

defined benefit obligation (DBO):

DBO at end of year …………………………………. £3,300

2. Difference between actual and expected fair value of

plan assets

12/31/19 actual fair value

of plan assets …………………………………. 2,620

Expected fair value

(c) The amount recorded in other comprehensive income is the asset gain and

liability loss:

EXERCISE 20.13 (Continued)

Journal entries 12/31/19

Other Comprehensive Income (G/L) ……………….. 100

Pension Expense …………………………………………… 480

EXERCISE 20.14 (15–20 minutes)

(a) Computation of pension expense:

Service cost …………………………………………… $ 80,000

Interest expense ($700,000 X .10) ……………. 70,000

(b) Income Statement:

Pension expense ……………………………………. 82,500

Statement of Financial Position:

EXERCISE 20.15 (20–25 minutes)

(a) Below is the completed worksheet, indicating debit and credit entries.

General Journal Entries

Memo Record

Annual

Pension

Expense

Cash

OCI—Gain/

Loss

Pension

Asset/Liability

Defined

Benefit

Obligation

Plan

Assets

Balance, Jan. 1, 2019

1,100 Cr.

2,800 Cr.

1,700 Dr.

Service cost

500 Dr.

500 Cr.

Interest expense

280 Dr.

280 Cr.

Interest revenue

170 Cr.

Contributions

Benefits

200 Dr.

Asset gain

Liability loss

365 Cr.

Accumulated OCI, Dec. 31, 2018

Balance, Dec. 31, 2019

1,225 Cr.

3,745 Cr.

2,520 Dr.

(b) Pension Expense …………………………………… 610

EXERCISE 20.16 (5–10 minutes)

Postretirement benefit expense is comprised of the following:

Service cost ……………………………………………………..

P

–

45,000

EXERCISE 20.17 (25–30 minutes)

General Journal Entries

Memo Record

Annual

Postretirement

Expense

Cash

Postretirement

Asset/Liability

DPBO

Plan Assets

Balance, Jan. 1, 2019

220,000 Cr.

330,000 Cr.

110,000 Dr.

Service cost

Interest expense

Interest revenue

Contributions

10,000 Cr.

Benefits

Journal entry for 2019

10,000 Cr.

Balance, Dec. 31, 2019

272,600 Cr.

381,400 Cr.

108,800 Dr.

EXERCISE 20.18 (10–12 minutes)

Service cost …………………………………………………………. $ 83,000

Interest expense

EXERCISE 20.19 (10–12 minutes)

Service cost …………………………………………………………. € 90,000

Interest expense

EXERCISE 20.20 (15–20 minutes)

See worksheet on next page.

20–33 Copyright © 2018 Wiley Kieso, IFRS, 3/e, Solutions Manual (For Instructor Use Only)

ENGLEHART AG

Postretirement Benefit Worksheet—2019

General Journal Entries

Memo Record

100 Dr.

EXERCISE 20.21 (25–30 minutes)

(a) Below is the completed worksheet, indicating debit and credit entries.

General Journal Entries

Memo Record Entries

Annual

Expense

Cash

Other

Comprehensive

Income—G/L

Postretirement

Asset/Liability

DPBO

Plan

Assets

Balance, Jan. 1, 2019

290,000 Cr.

410,000 Cr.

120,000 Dr.

Service cost

56,000 Dr.

56,000 Cr.

Interest expense

36,900 Dr.

36,900 Cr.

Interest revenue

10,800 Cr.

10,800 Dr.

Contributions

66,000 Dr.

Benefits

Asset loss

Accumulated OCI, Dec. 31, 2018

18,200 Dr.

Balance, Dec. 31, 2019

27,000 Dr.

314,900 Cr.

497,900 Cr.

183,000 Dr.

(b) Postretirement Expense …………………………….. 82,100

Other Comprehensive Income (G/L) …………… 8,800

Cash …………………………………………………… 66,000

Postretirement Asset/Liability ……………… 24,900

TIME AND PURPOSE OF PROBLEMS

Problem 20.1 (Time 40–50 minutes)

Purpose—to provide a problem that requires preparation of a pension worksheet for two separate

years’ pension transactions. Included in the problem are an asset loss.

Problem 20.2 (Time 45–55 minutes)

Purpose—to provide a problem that requires preparation of a pension worksheet for three separate years’

Problem 20.3 (Time 40–50 minutes)

Purpose—to provide a problem that requires computation of the annual pension expense, preparation of

Problem 20.4 (Time 30–40 minutes)

Purpose—to provide a problem that requires computation of pension expense and preparation of the

pension journal entries.

Problem 20.5 (Time 45–55 minutes)

Problem 20.6 (Time 45–60 minutes)

Problem 20.7 (Time 35–45 minutes)

Purpose—to provide a problem that requires preparation of a worksheet.

Problem 20.8 (Time 45–60 minutes)

covering all facets of pension accounting.

Problem 20.9 (Time 40–45 minutes)

Purpose—to provide a problem that requires preparation of a worksheet for two years, journal entries,

Problem 20.10 (Time 25–30 minutes)

Problem 20.11 (Time 35–45 minutes)

Purpose—to provide a problem that requires preparation of a worksheet, journal entries, and indicates

Time and Purpose of Problems (Continued)

Problem 20.12 (Time 35–45 minutes)

Problem 20.13 (Time 30–35 minutes)

Problem 20.14 (Time 40–45 minutes)

20–37 Copyright © 2018 Wiley Kieso, IFRS, 3/e, Solutions Manual (For Instructor Use Only)

SOLUTIONS TO PROBLEMS

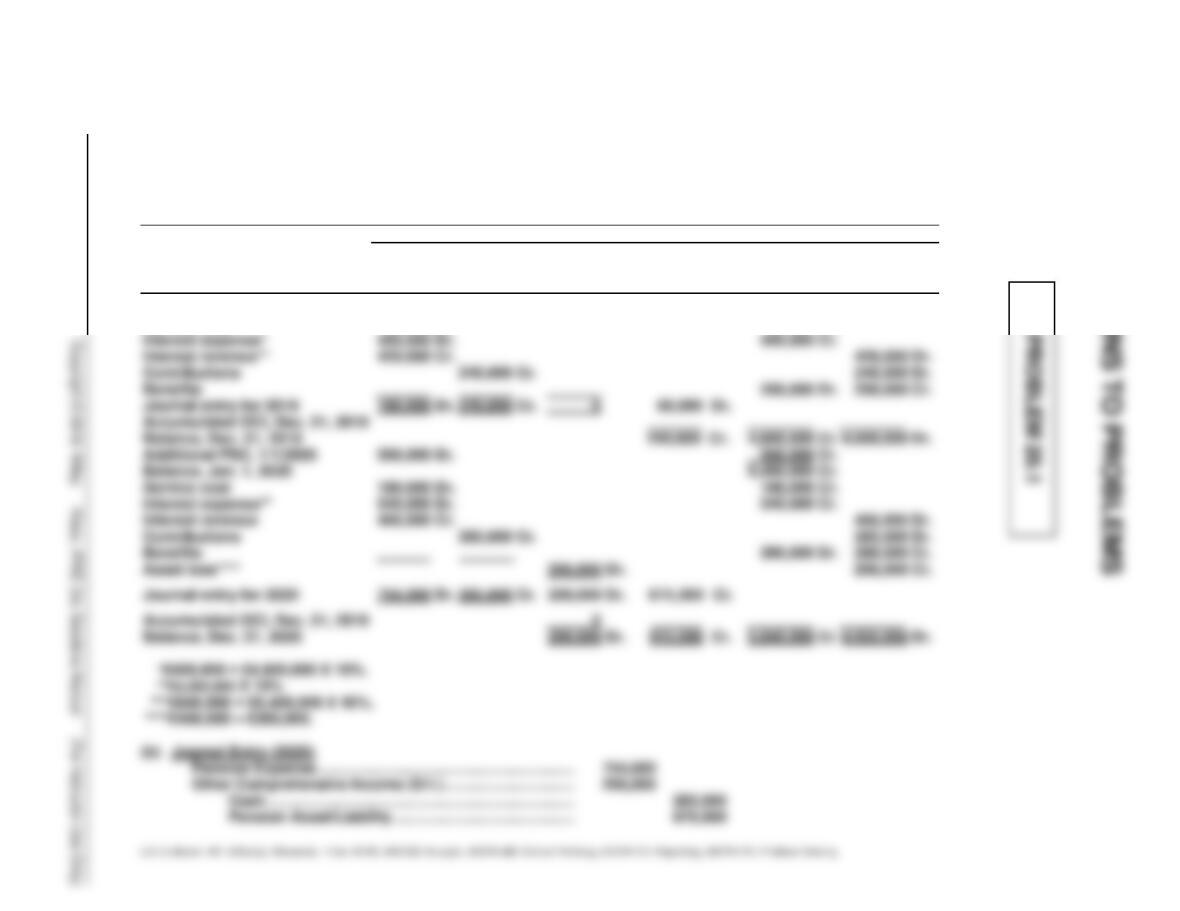

(a)

HARRINGTON SA

Pension Worksheet––2019 and 2020

Items

General Journal Entries

Memo Record

Annual

Pension

Expense

Cash

OCI—Gain/

Loss

Pension

Asset/Liability

Defined

Benefit

Obligation

Plan

Assets

Balance, Jan. 1, 2019

300,000 Cr.

4,500,000 Cr.

4,200,000 Dr.

Service cost

150,000 Dr.

150,000 Cr.

PROBLEM 20.1

450,000 Dr.

450,000 Cr.

Interest revenue**

420,000 Cr.

Contributions

240,000 Cr.

200,000 Dr.

Journal entry for 2019

180,000 Dr.

240,000 Cr.

60,000 Dr.

Accumulated OCI, Dec. 31, 2018

240,000 Cr.

4,900,000 Cr.

4,660,000 Dr.

Additional PSC, 1/1/2020

500,000 Dr.

5,400,000 Cr.

Service cost

180,000 Dr.

180,000 Cr.

540,000 Dr.

540,000 Cr.

466,000 Cr.

Contributions

285,000 Cr.

280,000 Dr.

5,840,000 Cr.

4,925,000 Dr.

Service cost

26,000 Dr.

26,000 Cr.

Interest expense(f)

48,330 Dr.

48,330 Cr.

Interest revenue(g)

26,760 Cr.

26,760 Dr.

Contributions

48,000 Cr.

48,000 Dr.

Benefits

21,000 Dr.

21,000 Cr.

Asset loss(h)

2,760 Dr.

2,760 Cr.

Liability gain(i)

16,630 Cr.

16,630 Dr.

Journal entry for 2020

47,570 Dr.

48,000 Cr.

13,870 Cr.

14,300 Dr.

Accumulated OCI, Dec. 31, 2019

200 Dr.

Balance, Dec. 31, 2020

13,670 Cr.

201,400 Cr.

520,000 Cr.

318,600 Dr.

Expense

Gain/Loss

Obligation

Balance, Jan. 1, 2018

50,000 Cr.

250,000 Cr.

200,000 Dr.

Service cost

16,000 Dr.

16,000 Cr.

Interest expense(a)

25,000 Dr.

25,000 Cr.

Interest revenue(b)

20,000 Cr.

20,000 Dr.

Contributions

16,000 Cr.

16,000 Dr.

Benefits

14,000 Dr.

14,000 Cr.

Journal entry for 2018

21,000 Dr.

16,000 Cr.

Balance, Dec. 31, 2018

55,000 Cr.

277,000 Cr.

222,000 Dr.

Additional PSC, 1/1/2019

160,000 Dr.

160,000 Cr.

Balance, Jan. 1, 2019

437,000 Cr.

Service cost

19,000 Cr.

Interest expense(c)

43,700 Dr.

43,700 Cr.

Interest revenue(d)

22,200 Cr.

22,200 Dr.

Contributions

40,000 Cr.

40,000 Dr.

Benefits

16,400 Dr.

16,400 Cr.

Asset loss(e)

200 Cr.

Journal entry for 2019

200,500 Dr.

40,000 Cr.

160,700 Cr.

Accumulated OCI, Dec. 31, 2018

Balance, Dec. 31, 2019

215,700 Cr.

483,300 Cr.

267,600 Dr.

PROBLEM 20.2 (Continued)

Worksheet computations:

(a)$25,000 = $250,000 X 10%

(b)$200,000 X 10%

(c)$43,700 = $437,000 X 10%

(b) Journal entries:

2018

Pension Expense …………………………………………….. 21,000

Cash ………………………………………………………… 16,000

Pension Asset /Liability …………………………….. 5,000

2019

PROBLEM 20.2 (Continued)

(c) Financial Statements—2020

Income Statement

Pension expense ………………………………………. $ 47,570

Comprehensive Income Statement

Net Income …………………………..…………………… $ XXXX

Other comprehensive income (loss)