CHAPTER 9

Inventories: Additional Valuation Issues

LEARNING OBJECTIVES

1. Describe and apply the lower-of-cost-or-net realizable value rule.

2. Identify other inventory valuation issues.

CHAPTER REVIEW

1. Chapter 9 concludes the discussion of inventories by addressing certain unique valuation

Lower-of-Cost-or-Net Realizable Value (LCNRV)

2. (L.O. 1) When the future revenue-producing ability associated with inventory is below its

original cost, the inventory should be written down to reflect this loss. Thus, the historical

3. The term “net realizable value” is the difference between the estimated selling price of

4. For example, consider the following illustration:

Historical cost ………………………………………. €190

5. The LCNRV rule may be applied (a) on an item-by-item basis, (b) on a group basis,

6. Two methods may be used to record inventory at net realizable value. The two methods

are the cost-of-goods-sold method and the loss method. The cost-of-goods-sold

7. Instead of crediting the inventory account for net realizable adjustments, companies

generally use an allowance account, Allowance to Reduce Inventory to Net Realizable

8. In periods following a write-down, the net realizable value of inventory previously written

9. The LCNRV rule suffers some conceptual deficiencies: (a) the decrease in the value of

the inventory and the loss are recognized in the period of the loss, not the period of sale.

Valuation Bases

10. There are some situations where companies depart from the LCNRV rule. Such treatment

may be justified in situations where cost is difficult to determine, the items are readily

11. Under IFRS net realizable value measurement is used for inventory when the inventory is

12. Biological assets are measured at initial recognition and at the end of each reporting

13. Agricultural produce (which is harvested from biological assets) is measured at NRV

(fair value less cost to sell) at the point of harvest. The NRV debited to an inventory account

14. Commodity broker-traders buy and sell commodities (e.g., grains, precious metals, oil,

etc.) for others or on their own account in order to generate profit from fluctuations in

Other Inventory Valuation Issues

15. (L.O. 2) When a group of varying inventory items is purchased for a lump sum price,

16. Purchase commitments represent contracts for the purchase of inventory at

a specified price in a future period. If material, the details of the contract should be disclosed

The Gross Profit Method

17. (L.O. 3) The gross profit method is used to estimate the amount of ending inventory. Its

use is not appropriate for financial reporting purposes; however, it can serve a useful

purpose when an approximation of ending inventory is needed. Such approximations are

18. The major disadvantages of the gross profit method are: (a) it provides an estimate,

therefore companies must take a physical count to verify the inventory; (b) it uses past

19. (L.O. 4) The retail inventory method is an inventory estimation technique based upon

an observable pattern between cost and sales price that exists in most retail concerns.

20. Basically, the retail method requires the computation of the cost–to-retail ratio of inventory

available for sale. This ratio is computed by dividing the cost of the goods available for

sale by the retail value (selling price) of goods available for sale. Once the ratio is

21. To obtain the appropriate inventory figures under the retail inventory method, proper

22. When the cost-to-retail ratio is computed after net markups (markups less markup

cancellations) have been added, the retail inventory method approximates lower of cost

23. The retail inventory method becomes more complicated when such items as freight-in,

purchase returns and allowances, and purchase discounts are involved. In essence,

24. Other items that require careful consideration include transfers-in, normal shortages,

abnormal shortages, and employee discounts. Transfers-in from another department

25. The retail inventory method is widely used (a) to permit the computation of net income without

a physical count of inventory, (b) as a control measure in determining inventory shortages,

Presentation and Analysis

26. (L.O. 5) Inventories normally represent one of the most significant assets held by a

business entity. Therefore, the accounting profession has mandated certain disclosure

LECTURE OUTLINE

This chapter describes inventory valuation problems and estimation techniques. The chapter

can be covered in three to four class sessions.

Emphasize that the Chapter 9 inventory techniques do not represent complete departures from

the FIFO and average cost bases of valuing inventory. For example, the LCNRV rule results in

The following lecture outline is appropriate for this chapter.

A. (L.O. 1) Lower-of-Cost-or-Net Realizable Value (LCNRV)

1. The general rule is that the historical cost principle is abandoned when the future utility

of the asset is no longer as great as its original cost.

4. Companies may apply the LCNRV rule using one of three methods:

a. An item-by-item basis, which produces the lowest valuation, and is most often used.

5. There are two methods that can be used to record inventory at NRV.

a. The cost-of–goods-sold method, which records the loss directly to the Cost of

6. An allowance account, “Allowance to Reduce Inventory to Net Realizable Value” is

used instead of crediting the Inventory account for the write-down.

a. The entry to record the write-down is:

7. If NRV increases in subsequent periods, the amount of the write-down is reversed. The

journal entry is:

8. The LCNRV rule suffers some conceptual deficiencies:

a. The decrease in the value of the asset and the charges to expense are

recognized in the period in which the loss in value occurs, not the period of sale.

B. Other Inventory Valuation Bases.

1. Agricultural Inventory. Under IFRS, net realizable value measurement is used for

inventory related to agricultural activity.

2. Biological asset (a long-term asset) is a living animal or plant.

4. Commodity broker-traders buy and sell commodities for others and themselves to

generate a profit from fluctuations in price.

5. (L.O. 2) Valuation using the relative standalone sales value method—When several

6. Purchase Commitments.

b. Accounting for formal purchase orders for which a firm price has been

established:

(1) If the market price exceeds the contract price—disclose the existence of the

contract in the notes, if material.

(2) If the market price is less than the contract price—

(a) Debit a loss account and credit a liability account (Purchase Commitment

Liability).

C. (L.O. 3) The Gross Profit Method.

1. This method is used when an estimate of a firm’s inventory is required. The resulting

estimate is acceptable for interim reporting purposes but not generally for annual

reporting.

2. Point out that four items of information are sufficient to estimate the cost of ending

inventory:

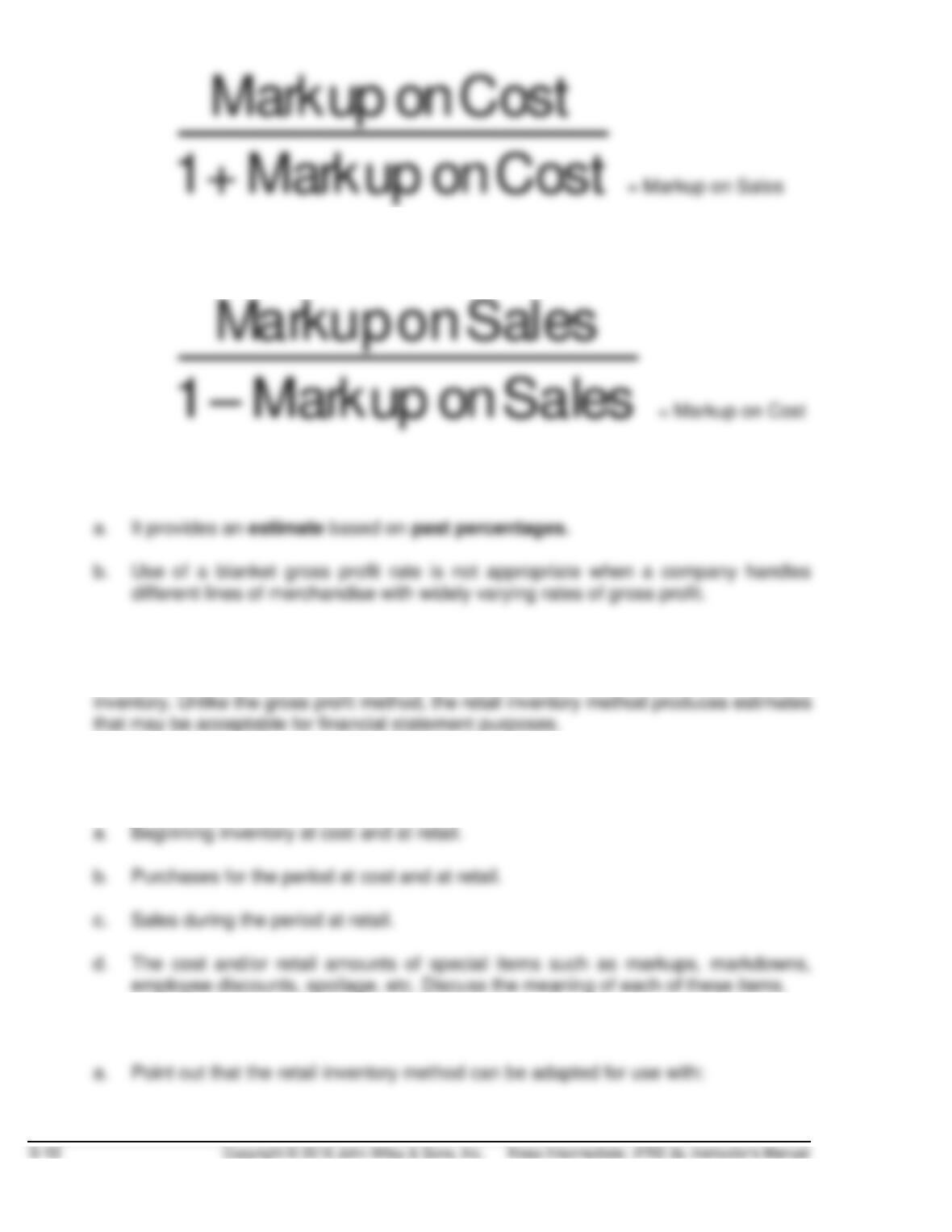

3. Point out that in this context the terms “gross margin,” “gross profit,” and “markup” are

synonymous. Discuss the distinction between markup expressed as a percentage of

cost and markup expressed as a percentage of sales. Describe how the percentage

markup is computed.

4. Describe how to convert a markup on cost to a markup on sales.

a. From markup on cost to markup on sales.

b. From markup on sales to markup on cost.

5. Appraisal of the gross profit method.

D. (L.O. 4) The Retail Inventory Method.

1. Like the gross profit method, the retail inventory method provides an estimate of ending

2. More detailed records are required for the retail inventory method than for the gross

profit method. Under the retail inventory method, records must be kept of the following.

3. Variations of the retail inventory method:

(1) either of the major inventory cost flow assumptions: FIFO or Average.

4. The conventional method computes the cost-to-retail ratio after markups and markup

cancellations but before markdowns. It approximates the lower-of-average-cost-or-net

realizable value.

5. The cost method computes the cost-to-retail ratio after both net markups and net

markdowns. It approximates cost.

6. Special items related to computing the cost–to-retail ratio and ending inventory at retail

are as follows:

a. Freight costs are part of the purchase cost.

b. Purchase returns are deducted under both the cost and retail columns.

7. Point out that there are three basic steps in computing ending inventory using the retail

method.

a. Compute ending inventory at retail. This step is the same for either method.

8. Appraisal of the Retail Inventory Method.

a. The method permits:

(1) the computation of net income without a physical count of inventory.

b. The method has an averaging effect on varying rates of gross margin. Problems

may arise when the averages being used are not reflective of underlying conditions.

E. (L.O. 5) Presentation and Analysis

1. IFRS require the following disclosures:

a. The accounting policies adopted for measuring inventories.

b. The total carrying amount of inventories and the carrying amount in classifications.

2. There are two ratios related to inventory management.

a. Inventory turnover, which measures the number of times on average a

company, sells inventory during the period.

b. Average days to sell inventory represents the average number of days inventory

is held.