CHAPTER 12

Intangible Assets

ASSIGNMENT CLASSIFICATION TABLE (BY TOPIC)

Topics

Questions

Brief

Exercises

Exercises

Problems

Concepts

for Analysis

1.

Intangible assets;

concepts, definitions;

items comprising

intangible assets.

1, 2, 3, 4, 5, 6,

7, 8, 9, 10, 11,

12, 13, 14, 25

14

1, 2, 3,

5, 6

1, 2, 3

ASSIGNMENT CLASSIFICATION TABLE (BY LEARNING OBJECTIVE)

Learning Objectives

Brief

Exercises

Exercises

Problem

s

Concept

s for

Analysis

1.

Discuss the characteristics, valuation, and

amortization of intangible assets.

14

1, 2, 3

5

1, 2, 3

2.

Describe the accounting for various types of

intangible assets.

1, 2, 3, 4

1, 2, 3, 4, 5,

6, 7, 9, 10,

1, 2, 3, 6

2, 3

3.

Identify the accounting issues for recording

goodwill.

5, 8, 9

12, 13, 15

5, 6

4.

Explain impairment procedures and

presentation requirements for intangible

assets.

6, 7, 8, 9,

13, 14

7, 14, 15

5, 6

5.

Describe accounting and presentation for

research and development and similar costs.

10, 11, 12,

4, 5, 6, 8, 9,

10, 16, 17

4

1, 2, 4, 5

ASSIGNMENT CHARACTERISTICS TABLE

Item

Description

Level of

Difficulty

Time

(minutes)

E12.1

Classification issues—intangibles.

Moderate

15–20

E12.2

Classification issues—intangibles.

Simple

10–15

E12.3

Classification issues—intangibles.

Moderate

10–15

E12.4

Intangible amortization.

Moderate

15–20

E12.5

Correct intangible asset account.

Moderate

15–20

E12.6

Recording and amortization of intangibles.

Simple

15–20

E12.7

Accounting for trade name.

Simple

10–15

E12.8

Accounting for organization costs.

Simple

10–15

E12.9

Accounting for patents, franchises, and R&D.

Moderate

15–20

E12.10

Accounting for patents.

Moderate

15–20

E12.11

Accounting for patents.

Moderate

20–25

E12.12

Accounting for goodwill.

Moderate

20–25

E12.13

Accounting for goodwill.

Simple

10–15

E12.14

Copyright impairment.

Simple

15–20

E12.15

Goodwill impairment.

Simple

15–20

E12.16

Accounting for R&D costs.

Moderate

15–20

E12.17

Accounting for R&D costs.

Moderate

10–15

P12.1

Correct intangible asset account.

Moderate

15–20

P12.2

Accounting for patents.

Moderate

20–30

P12.3

Accounting for franchise, patents, and trademark.

Moderate

20–30

P12.4

Accounting for R&D costs.

Moderate

15–20

P12.5

Goodwill, impairment.

25–30

P12.6

Comprehensive intangible assets.

Moderate

30–35

CA12.1

Development costs.

Moderate

15–20

CA12.2

Accounting for pre-opening costs.

Moderate

20–25

CA12.3

Accounting for patents.

Moderate

25–30

CA12.4

Accounting for research and development costs.

Moderate

25–30

CA12.5

Accounting for research and development costs.

Moderate

20–25

ANSWERS TO QUESTIONS

1. The three main characteristics of intangible assets are:

(a) they are identifiable.

2. If intangibles are acquired for shares, the cost of the intangible is the fair value of the consideration

3. Limited-life intangibles should be amortized by systematic charges to expense over their useful

life. An intangible asset with an indefinite life is not amortized.

LO: 1, Bloom: K, Difficulty: Simple, Time: 3-5, AACSB: None, AICPA BB: None, AICPA FC: Reporting, AICPA PC: Communication

4. When intangibles are created internally, it is often difficult to determine the validity of any future

service potential. To permit deferral of these types of costs would lead to a great deal of subjectivity

5. Companies cannot capitalize self-developed, self-maintained, or self-created goodwill. These expen-

6. Factors to be considered in determining useful life are:

(a) The expected use of the asset by the entity.

(b) The effects of obsolescence, demand, competition, and other economic factors.

7. The amount of amortization expensed for a limited-life intangible asset should reflect the pattern in

which the asset is consumed or used up, if that pattern can be reliably determined. If the pattern of

8. This trademark is an indefinite life intangible and, therefore, should not be amortized.

LO: 1,2, Bloom: K, Difficulty: Simple, Time: 3-5, AACSB: None, AICPA BB: None, AICPA FC: Reporting, AICPA PC: Communication

9. The $190,000 should be expensed as research and development expense in 2019. The $91,000 is

expensed as selling and promotion expense in 2019. The $45,000 of costs to legally obtain the

Questions Chapter 12 (Continued)

10. Patent Amortization Expense (£350,000 10) ………………………….. 35,000

11. Artistic-related intangible assets involve ownership rights to plays, pictures, photographs, and

video and audiovisual material. These ownership rights are protected by copyrights. Contract related

12. Varying approaches are used to define goodwill. They are

(a) Goodwill should be measured initially as the excess of the fair value of the acquisition cost

over the fair value of the net assets acquired. This definition is a measurement definition but

does not conceptually define goodwill.

(b) Goodwill is sometimes defined as one or more unidentified intangible assets and identifiable

13. Goodwill is recorded only when an entire business is acquired by purchase. Goodwill acquired in a

14. Companies that recognize goodwill in a business combination consider it to have an indefinite life

and therefore should not amortize it. Although goodwill may decrease in value over time,

predicting the actual life of goodwill and an appropriate pattern of amortization is extremely

difficult. In addition, investors find the amortization charge of little use in evaluating financial

Questions Chapter 12 (Continued)

amortization of goodwill combined with an adequate impairment test should provide the most

useful financial information to the investment community.

LO: 1,3, Bloom: K, Difficulty: Simple, Time: 3-5, AACSB: None, AICPA BB: None, AICPA FC: Reporting, AICPA PC: Communication

15. Accounting standards require that if events or changes in circumstances indicate that the carrying

amount of such assets may not be recoverable, then the carrying amount of the asset should be

16. Yes, Zeno should record the recovery of the impairment loss from last year.

LO: 4, Bloom: K, Difficulty: Simple, Time: 3-5, AACSB: None, AICPA BB: None, AICPA FC: Reporting, AICPA PC: Communication

17. Impairment losses are reported as part of income from continuing operations, generally in the

“Other income and expense” section. Impairment losses (and recovery of losses) are similar to

18. The amount of goodwill impaired is HK$400,000, computed as follows:

Recorded goodwill …………………………..……………. HK$4,000,000

19. Research and development costs are incurred to develop new products or processes, to improve

present products, or to discover new knowledge. Development costs can be capitalized once

20. (a) Personnel (labor) type costs incurred in R&D activities should be expensed as incurred.

(b) Materials and equipment costs should be expensed immediately unless the items have

21. See Illustration 12-15.

(a) Expense as R&D.

22. Each of these items should be charged to current operations as expense when incurred.

Questions Chapter 12 (Continued)

24. These costs are referred to as start-up costs, or more specifically organizational costs in this case.

The accounting for start up costs is straightforward—expense these costs as incurred. The

25.The total life, per revised facts, is 40 years (10 + 30). There are 30 (40 – 10) remaining years for

amortization purposes. Original amortization:

$540,000

= $18,000 per year; $18,000 X 10 years

SOLUTIONS TO BRIEF EXERCISES

BRIEF EXERCISE 12.1

Patents …………………………………………………………………..

54,000

Cash ………………………………………………………………

Patent Amortization Expense …………………………………..

Patents ($54,000 X 1/10 = $5,400) ……………………..

BRIEF EXERCISE 12.2

Patents …………………………………………………………………..

24,000

Cash ………………………………………………………………

Patent Amortization Expense …………………………………..

Patents [($43,200 + $24,000) X 1/8 = $8,400] …………

BRIEF EXERCISE 12.3

Trade Name …………………………………………………………….

68,000

Cash ………………………………………………………………

Trade Name Amortization Expense …………………………..

Trade Name (€68,000 X 1/8 = €8,500) ………………..

BRIEF EXERCISE 12.4

Franchise ……………………………………………………………….

120,000

Cash ………………………………………………………………

120,000

Franchise Amortization Expense …………………………..

Franchise (£120,000 X 1/8 X 9/12 = £11,250) ………

BRIEF EXERCISE 12.5

Purchase price …………………………………………………….

£700,000

Fair value of assets ………………………………………………

Fair value of liabilities …………………………………………..

Fair value of net assets …………………………………………

(600,000)

BRIEF EXERCISE 12.6

Loss on Impairment ………………………………………………..

190,000

Patents ($300,000 – $110,000) ………………………….

190,000

BRIEF EXERCISE 12.7

Patents [$130,000 – ($110,000 – $11,000*)] ………………..

31,000

BRIEF EXERCISE 12.8

Because the recoverable amount of the division exceeds the carrying

BRIEF EXERCISE 12.9

Loss on Impairment (HK$800,000 – HK$750,000) ………

50,000

Goodwill ……………………………………………………….

50,000

BRIEF EXERCISE 12.10

Organization Cost Expense ……………………………………..

60,000,000

Cash ………………………………………………………………

BRIEF EXERCISE 12.11

Intangible Asset (Capitalized Costs) …………………………

75,000

Research and Development Expense ……………………….

Cash ………………………………………………………………

BRIEF EXERCISE 12.12

(a) Capitalize

(b) Expense

Copyright © 2018 Wiley Kieso, IFRS, 3/e, Solutions Manual (For Instructor Use Only) 12–11

BRIEF EXERCISE 12.13

Carrying

Amount

Life in

Months

Amortization

Per Month

Months

Amortization

Patent (1/1/19)

$288,000

96*

$3,000

12

BRIEF EXERCISE 12.14

Copyright No. 1 for €9,900 should be expensed and therefore not reported

on the statement of financial position.

Legal costs (12/1/19)

85,000

85

$1,000

$373,000

EXERCISE 12.1 (15–20 minutes)

(b) 1. Long-term investments in the statement of financial position.

2. Property, plant, and equipment in the statement of financial position.

3. Research and development expense in the income statement.

4. Current asset (prepaid rent) in the statement of financial position.

5. Property, plant, and equipment in the statement of financial position.

6. Research and development expense in the income statement.

EXERCISE 12.2 (10–15 minutes)

The following items would be classified as an intangible asset:

Cable television franchises Film contract rights

Music copyrights Customer lists

Goodwill Covenants not to compete

EXERCISE 12.2 (Continued)

Investments in associated companies would be classified as part of the

investments section of the statement of financial position.

EXERCISE 12.3 (10–15 minutes)

(a)

Trademarks …………………………..………………………………….

€20,000

(b) Organization costs, €24,000, should be expensed.

Bonds payable, €35,000, should be reported in the non-current liabilities

section.

EXERCISE 12.4 (15–20 minutes)

1. Palmiero should report the patent at $900,000 (net of $600,000 accu–

mulated amortization) on the statement of financial position. The

Amortization for 2017 and 2018 ($1,500,000/10) X 2 …….

2. Palmiero should amortize the franchise over its estimated useful life.

Because it is uncertain that Palmiero will be able to retain the franchise

3. These costs should be expensed as incurred. Therefore $275,000 of

4. Because the license can be easily renewed (at nominal cost), it has an

EXERCISE 12.5 (15–20 minutes)

Research and Development Expense ………………………..

940,000

Patents ……………………………………………………………………

75,000

Rent Expense [(5 ÷ 7) X HK$91,000] …………………………..

65,000

Prepaid Rent [(2 ÷ 7) X HK$91,000] …………………………...

Advertising Expense ………………………………………………..

Income Summary (or a loss account) ………………………..

Bonds Payable …………………………………………………………

Interest Expense ………………………………………………………

Share Premium—Ordinary ………………………………….

Intangible Assets ……………………………………………….

Patent Amortization Expense [(HK$75,000 ÷ 12) X 1/2] ….

3,125

EXERCISE 12.6 (15–20 minutes)

Patents (380,0000 + 55,000) …………………………..

435,000

Goodwill …………………………………………………………………

360,000

Franchise ……………………………………………………….

450,000

Copyright ……………………………………………………….

156,000

Intangible Assets ……………………………………………

Amortization Expense ……………………………………………..

Patents (£380,000/8) + (£55,000 X 4/88)* ……………

Franchise (£450,000/10 X 6/12) …………………………

Copyright (£156,000/5 X 5/12) …………………………..

Research and Development Expense

EXERCISE 12.7 (10–15 minutes)

(a) 2018 amortization: $18,000 ÷ 10 = $1,800.

12/31/18 book value: $18,000 – $1,800 = $16,200.

2019 amortization: ($16,200 + $7,800) ÷ 9 = $2,667.

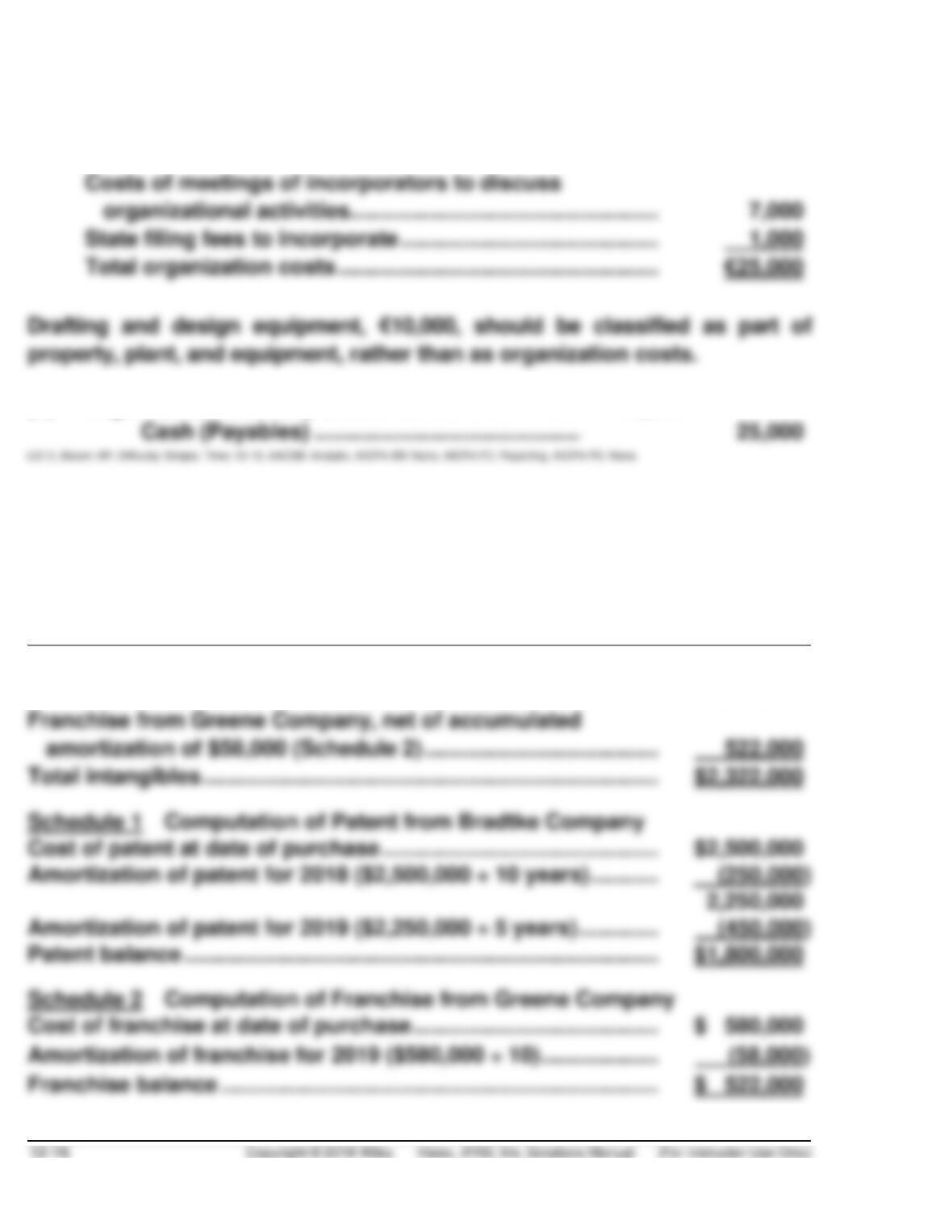

EXERCISE 12.8 (10–15 minutes)

(a)

Attorney’s fees in connection with organization

of the company ……………………………………………………….

€17,000

Costs of meetings of incorporators to discuss

organizational activities …………………………………………..

State filing fees to incorporate …………………………..……….

(b)

Organization Cost Expense ……………………………………..

25,000

Cash (Payables) ……………………………………………..

EXERCISE 12.9 (15–20 minutes)

(a) DEVON HARRIS COMPANY

Intangibles Section of Statement of Financial Position

December 31, 2019

Patent from Bradtke Company, net of accumulated

amortization of $700,000 (Schedule 1) ………………………………

$1,800,000

Franchise from Greene Company, net of accumulated

amortization of $58,000 (Schedule 2) ………………………………..

522,000

EXERCISE 12.9 (Continued)

(b) DEVON HARRIS COMPANY

Income Statement Effect

For the Year Ended December 31, 2019

Patent from Bradtke Company:

Amortization of patent for 2019

($2,250,000 ÷ 5 years) ……………………………………..

$ 450,000

Franchise from Greene Company:

Amortization of franchise for 2019

($580,000 ÷ 10) ……………………………………………….

Payment to Greene Company

($2,500,000 X 5%) ……………………………………………

183,000

Research and development costs …………………………..

433,000

EXERCISE 12.10 (15–20 minutes)

(a)

2018

Research and Development Expense ……………………….

170,000

Cash ……………………………………………………….

170,000

Patents ……………………………………………………….

Cash ……………………………………………………….

Patents [(¥24,000 ÷ 10) X 3/12] ………………………….

2019

Patent Amortization Expense …………………………..

Patents (¥24,000 ÷ 10) …………………………..

EXERCISE 12.10 (Continued)

(b)

2020

Patents ……………………………………………………….

12,400

Cash ……………………………………………………….

12,400

Patent Amortization Expense …………………………..

2,575

Patents (¥$1,000 + ¥1,575) …………………………..

2,575

[Jan. 1–June 1: (¥24,000 ÷ 10) X

5/12 = ¥1,000

June 1–Dec. 31: (¥24,000 – ¥600 –

¥2,400 – ¥1,000 + ¥12,400) = ¥32,400;

(¥32,400 ÷ 12) X 7/12 = ¥1,575]

2021

Patent Amortization Expense …………………………..

2,700

Patents (¥32,400 ÷ 12) …………………………..

2,700

(c)

2022 and 2023

Patent Amortization Expense …………………………..

14,063

Patents (¥28,125 ÷ 2) …………………………..

14,063

(¥32,400 – ¥1,575 – ¥2,700) = ¥28,125

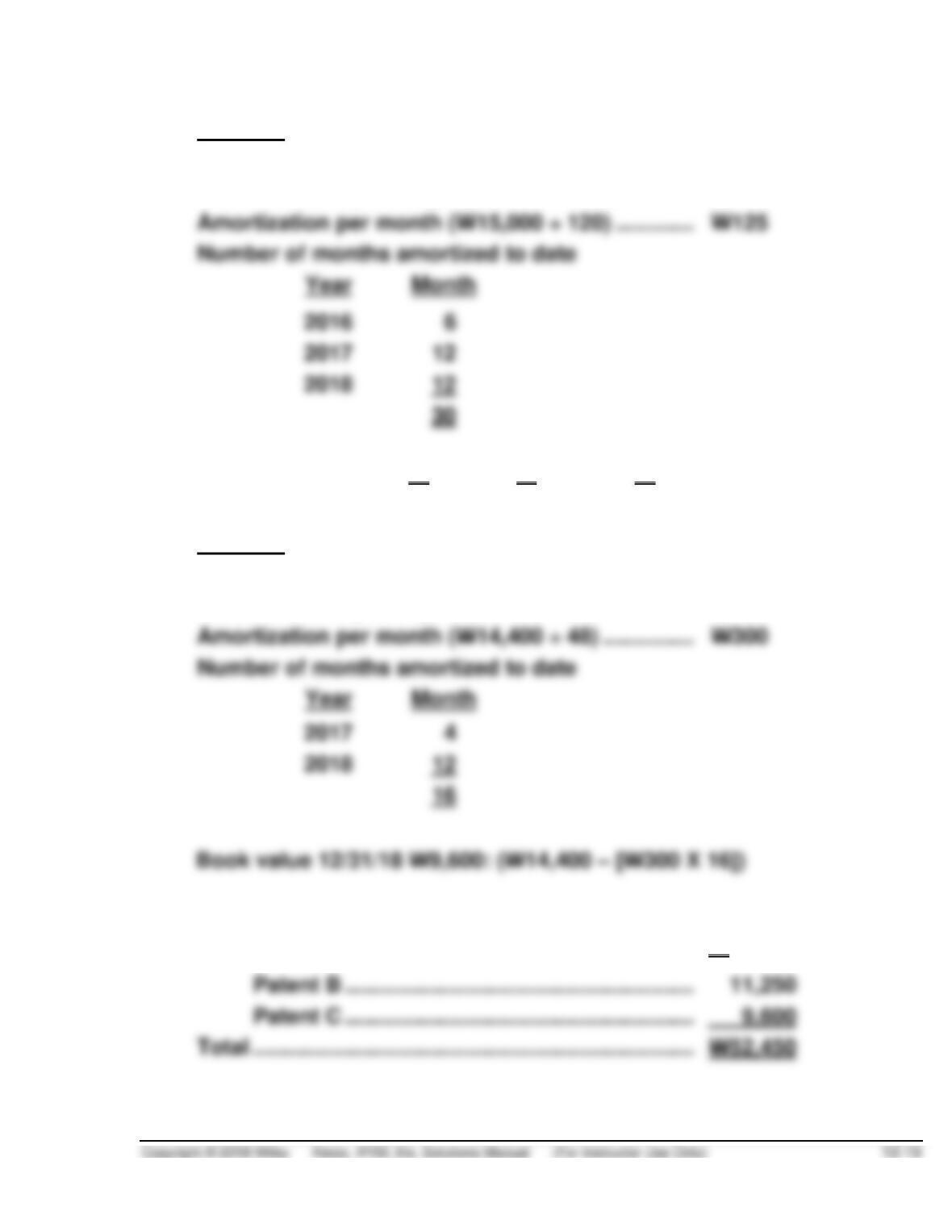

EXERCISE 12.11 (20–25 minutes)

(a)

Patent A

Life in years ……………………………………………………..

17

Life in months (12 X 17) …………………………………….

204

Amortization per month (W40,800 ÷ 204)…………….

W200

Number of months amortized to date

EXERCISE 12.11 (Continued)

Patent B

Life in years …………………………………………………….

10

Life in months (12 X 10) ……………………………………

120

Amortization per month (W15,000 ÷ 120) …………..

Number of months amortized to date

Book value 12/31/18 W11,250: (W15,000 – [W125 X 30])

Patent C

Life in years …………………………………………………….

4

Life in months (12 X 4) ……………………………………..

48

Amortization per month (W14,400 ÷ 48) …………….

Number of months amortized to date

At December 31, 2018

Patent A ………………………………………………….

W31,600

Patent B ………………………………………………….

Patent C ………………………………………………….

9,600

EXERCISE 12.11 (Continued)

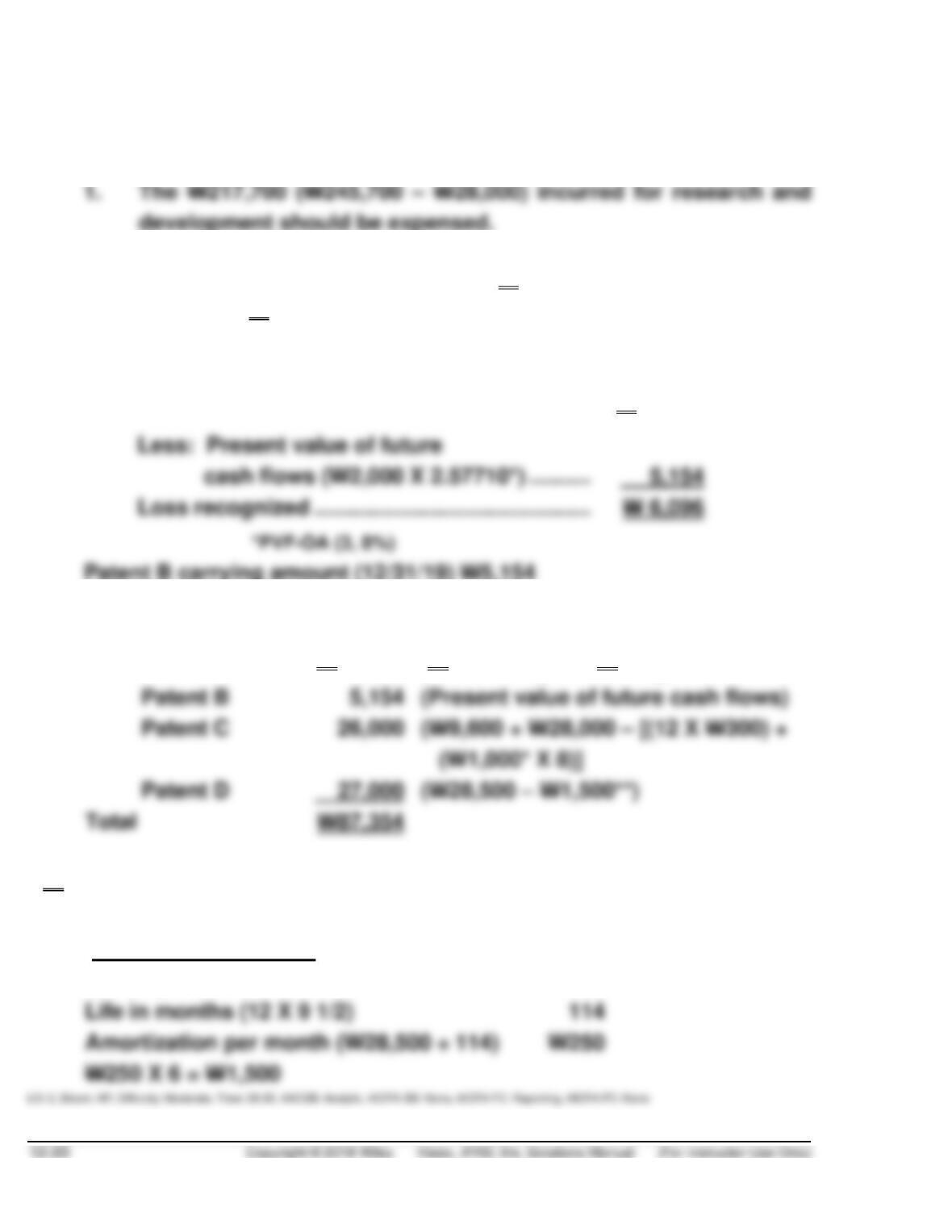

(b) Analysis of 2019 transactions

2. The book value of Patent B is W11,250 and its recoverable

amount is W5,154; therefore Patent B is impaired. The impairment

loss is computed as follows:

Book value ………………………………………………

W11,250

Less: Present value of future

cash flows (W2,000 X 2.57710*) ……….

Patent B carrying amount (12/31/19) W5,154

At December 31, 2019

Patent A

W29,200

(W31,600 – [12 X W200])

Patent B

(Present value of future cash flows)

(W1,000* X 8)]

Patent D

(W28,500 – W1,500**)

*(W28,000 ÷ 28 mon.)

**Patent D amortization

Life in years

9 1/2

Life in months (12 X 9 1/2)

Amortization per month (W28,500 ÷ 114)