CA 23.1 (Continued)

6. The details of changes in long-term debt should be shown separately. Payments should not be

netted against increases in long-term borrowings. The long-term borrowing of $620,000 should

CA 23.2

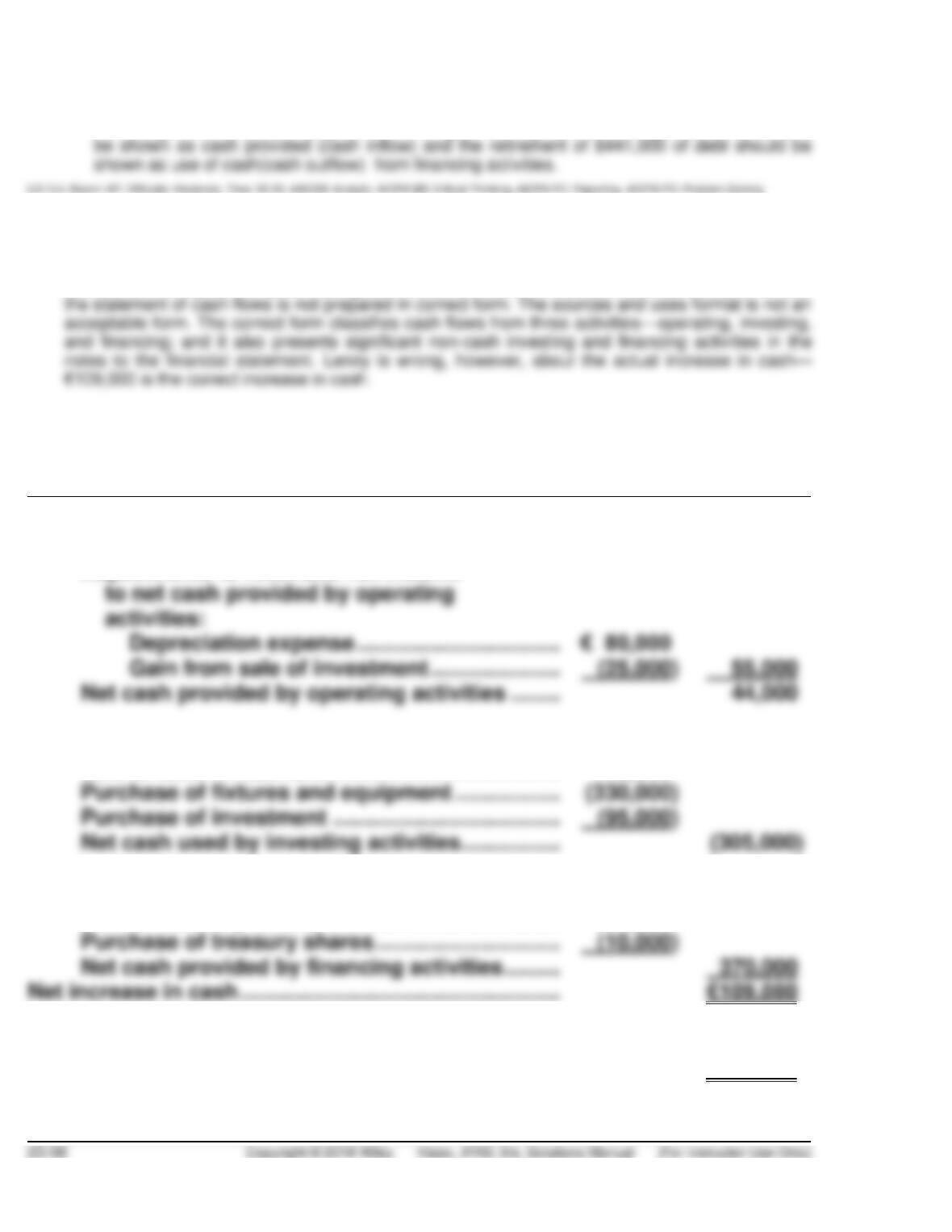

(a) From the information given, it appears that from an operating standpoint PANAKA Clothing Store

did not have a superb first year, having suffered an €11,000 net loss (see below). Lenny is correct;

(b) PANAKA CLOTHING STORE

Statement of Cash Flows

For the Year Ended January 31, 2019

Cash flows from operating activities

Net loss ……………………………………………………….

€ (11,000)*

Adjustments to reconcile net income

to net cash provided by operating

activities:

Depreciation expense …………………………...

Gain from sale of investment …………………

Net cash provided by operating activities ……..

Cash flows from investing activities

Sale of debt investment ………………………………..

120,000

Purchase of fixtures and equipment ……………..

Purchase of investment ……………………………….

Net cash used by investing activities …………….

Cash flows from financing activities

Sale of ordinary shares ………………………………..

380,000

Purchase of treasury shares …………………………

Net cash provided by financing activities ………

Supplemental disclosure of cash flow information:

Cash paid for interest …………………………………..

€ 3,000

CA 23.2 (Continued)

Significant non-cash investing and financing activities

(presented in the notes).

Issuance of note for truck ………………………………..

€ 30,000

*Computation of net income (loss)

Sales of merchandise ………………………………………

€382,000

Interest on investments …………………………………..

8,000

Total revenues………………………………………….

Merchandise purchases …………………………..………

Depreciation ……………………………………………………

Interest expense ……………………………………………..

Total expenses …………………………………………

Net loss ………………………………………………………….

€ (11,000)

CA 23.3

1. The loss of $110,000 should be added back to the net income of $700,000 as an adjustment to

.

2. The $315,000 depreciation expense is neither a source nor a use of cash. Because depreciation is

an expense, it was deducted in the computation of net income. Accordingly, the $315,000 must be

3. The writeoff of uncollectible accounts receivable against the allowance account has no effect on

cash because the net accounts receivable remain unchanged. An adjustment to income is only

necessary if the net receivable amount increases or decreases. Because the net receivable amount

4. The $6,000 gain realized on the sale of the machine is deducted from net income as an

CA 23.3 (Continued)

5. In this case, no cash flow resulted from the lightning damage. The net loss (a non-cash event) must

be added back to net income (under the indirect method) as one of the adjustments to reconcile

net income to net cash flow provided by operating activities.

CA 23.4

Where to Present

How to Present

1.

Investing and operating

Cash provided by sale of fixed assets, R4,750 as an investing

activity. In addition, the loss of R2,250 [(R20,000 x 31/2) ÷ 10] –

R4,750 on the sale would be added back to net income.

2.

Operating

The impairment reduced earnings from operations but did not use

cash. The amount of R15,000 is added back to net income.

3.

Financing

Cash provided by the issuance of ordinary shares for R16,000.

5.

Not reported in statement.

6.

Investing and operating

Cash provided by the sale of the investment, R10,600 as an

investing activity. The loss of R1,400 is added back to net income.

R24,240 (R24,000 x 1.01). Additionally, the gain of R1,760 =

[(R24,000 + R2,000) – R24,240] is deducted from net income in

the operating activities section as an adjustment.

CA 23.5

(a) The primary purpose of the statement of cash flows is to provide information concerning the cash

receipts and cash payments of a company during a period. The information contained in the

statement of cash flows, together with related disclosures in other financial statements, may help

investors and creditors:

1. assess the company’s ability to generate future net cash inflows.

CA 23.5 (Continued)

(b) The statement of cash flows classifies cash inflows and outflows as those resulting from operating

activities, investing activities, and financing activities.

Cash inflows from operating activities include receipts from the sale of goods and services,

receipts from returns on loans and equity securities (interest and dividends), and all other receipts

(c) Cash flows from operating activities may be presented using the direct method or the indirect

method. Under the direct method, the major classes of operating cash receipts and cash payments

are shown separately. The indirect method involves adjusting net income to net cash flow from

operating activities by removing the effects of deferrals of past cash receipts and payments,

accruals of future cash receipts and payments, and non-cash items from net income.

CA 23.6

(a) It is true that selling current assets, such as receivables and notes to factors, will generate cash flows

for the company, but this practice does not cure the systemic cash problems for the organization.

In short, it may be a bad business practice to liquidate assets, incurring expenses and losses, in

order to “window dress” the cash flow statement.

The ethical implications are that Brockman creates a short-term cash flow at the longer-term

expense of the company’s operations and financial position. Barbara’s idea creates the deceiving

illusion that the company is successfully generating positive cash flows.

(b) Barbara Brockman should be told that if she executes her plan, the company may not survive.

While the factoring of receivables and the liquidation of inventory will indeed generate cash, the

FINANCIAL REPORTING PROBLEM

(a) M&S uses the indirect method to compute and report net cash provided

by operating activities. The amounts of net cash provided by operating

(b) The most significant item in the investing activities section is the

(c) M&S does not report deferred income taxes on its statement of cash

flows. It does report income tax expense as an add-back to net income

COMPARATIVE ANALYSIS CASE

(a) Both Puma and adidas use the indirect method of computing and

reporting net cash provided by operating activities.

(b) The most significant investing activities items in 2015:

Puma

Purchase of property and equipment €79.0 million

(c) Puma decreased net cash from operating activities from a positive

€126.4 million in 2014 to a negative €37.1 million in 2015, a decrease of

(d) Both Puma and adidas report depreciation and amortization in the

operating activities section:

COMPARATIVE ANALYSIS CASE (Continued)

(e)

Puma

adidas

1.

Current cash

€-37.1

Cash debt

€1,090

(f) The current cash debt coverage uses cash generated from operations

during the period and provides a better representation of liquidity on

an average day. adidas ratio of €.22 of cash flow from operations for

FINANCIAL STATEMENT ANALYSIS CASE

(a) Telefónica uses the direct method to prepare the operating cash flow

section of its statement of cash flows. Telefónica reports cash

(b) Adjustments that would explain the difference between net income

and operating cash flow include non-cash expenses (depreciation and

(c) Telefónica reports interest received (paid), taxes paid, and dividends

received as operating activities. It shows under investing activities

payments made on various investments and proceeds from

disposals, and dividends paid as a financing activity. IFRS allows

ACCOUNTING, ANALYSIS, AND PRINCIPLES

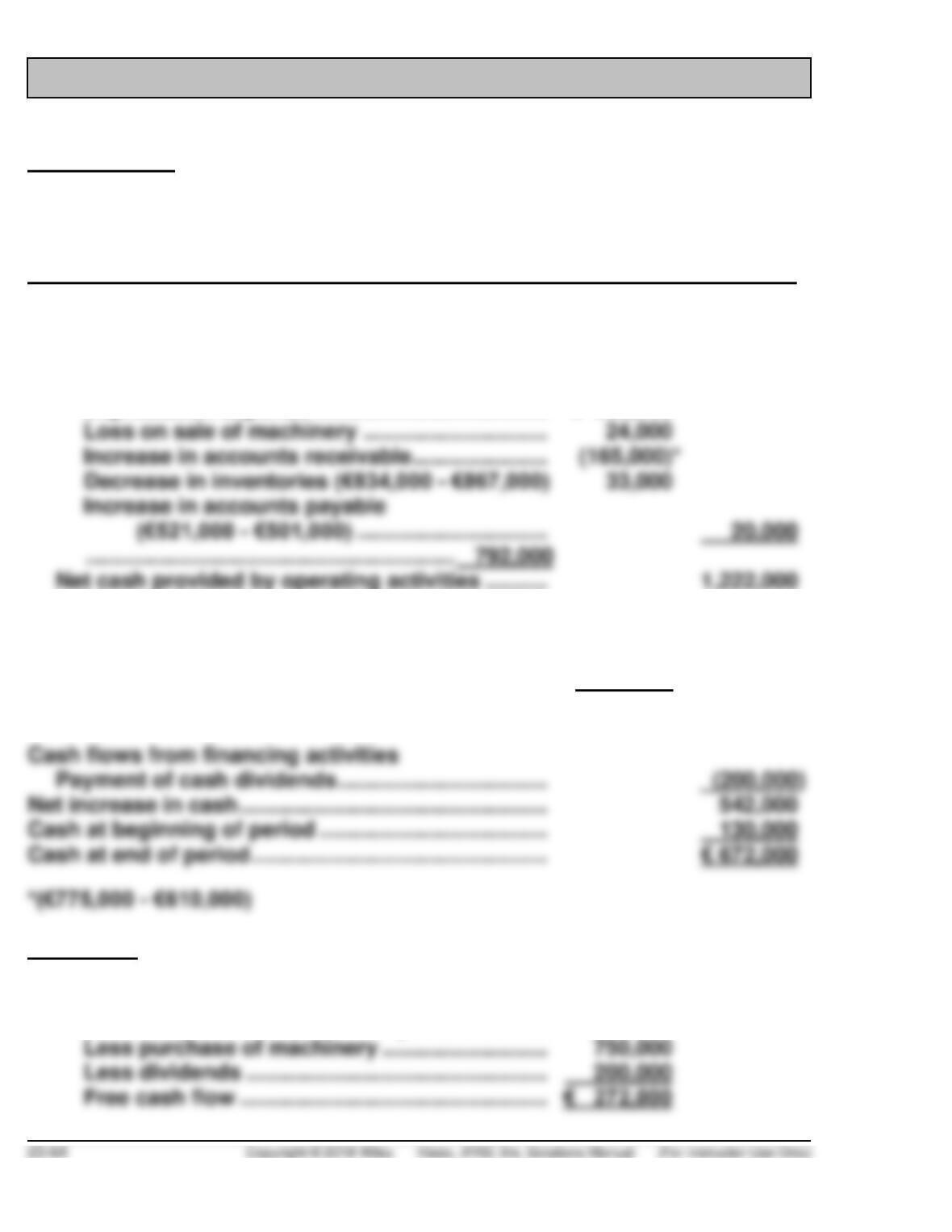

ACCOUNTING

LASKOWSKI AG

Statement of Cash Flows—Indirect Method

For the Year Ended December 31, 2019

Cash flows from operating activities

Net income …………………………………………………… € 430,000

Adjustments to reconcile net income to net cash

provided by operating activities:

Depreciation expense ……………………………….. € 880,000

Cash flows from investing activities

Sale of machinery …………………………………………. 270,000

Purchase of machinery………………………………….. (750,000)

Net cash used by investing activities ……………… (480,000)

ANALYSIS

Laskowski’s free cash flow is:

Net cash provided by operating activities …… €1,222,000

ACCOUNTING, ANALYSIS, AND PRINCIPLES (Continued)

Laskowski’s free cash flow for the current year (€272,000) is less than the

amount needed for expansion next year (€500,000). Thus, assuming

PRINCIPLES

According to IAS 7, “Information about the cash flows of an entity is useful

in providing users of financial statements with a basis to assess the ability

of the entity to generate cash and cash equivalents and the needs of the

RESEARCH CASE

(a) According to IAS 7, “Information about the cash flows of an entity is

useful in providing users of financial statements with a basis to

assess the ability of the entity to generate cash and cash equivalents

and the needs of the entity to utilise those cash flows. The economic

(b) According to paragraph 10, “The statement of cash flows shall report

cash flows during the period classified by operating, investing and

financing activities.” Further, paragraph 11 states “An entity presents

(c) According to paragraph 14, “Cash flows from operating activities are

primarily derived from the principal revenue-producing activities of

the entity. Therefore, they generally result from the transactions and

other events that enter into the determination of profit or loss. Examples

of cash flows from operating activities are:

(a) cash receipts from the sale of goods and the rendering of

RESEARCH CASE (Continued)

(e) cash receipts and cash payments of an insurance entity for

premiums and claims, annuities and other policy benefits;

GAAP CONCEPTS AND APPLICATION

23.1. As in U.S. GAAP, the statement of cash flows is a required statement

for IFRS. In addition, the content and presentation of an IFRS

statement of cash flows is similar to one used for U.S. GAAP.

However, the disclosure requirements related to the statement of cash

flows are more extensive under U.S. GAAP.

Other similarities include: (1) Companies preparing financial

statements under IFRS must prepare a statement of cash flows as

an integral part; (2) Both IFRS and U.S. GAAP require that the

Notable differences are (1) The definition of cash equivalents used in

IFRS is similar to that used in U.S. GAAP. A major difference is that

in certain situations bank overdrafts are considered part of cash and

cash equivalents under IFRS (which is not the case in U.S. GAAP).

Under U.S. GAAP, bank overdrafts are classified as financing

23.2. The following table relates to the classification of interest, dividends,

and taxes and indicates relative degree of choice inherent under

GAAP CONCEPTS AND APPLICATION (Continued)

Item

U.S. GAAP

IFRS

Interest paid

Operating

Operating or financing

Interest received

Operating

Operating or investing

Dividends paid

Financing

Operating or financing

Dividends received

Operating

Operating or investing

23.3. Presently, the FASB and the IASB are involved in a joint project on

the presentation and organization of information in the financial

23.4. VERMONT TEDDY BEAR CO.

(a) Vermont’s statement of cash flows has the same 3 categories

(operating, investing, and financing) as an IFRS statement does. IFRS

GAAP CONCEPTS AND APPLICATION (Continued)

(b) Even though prior year income exceeded the current year income by

$821,432 ($838,955 – $17,523), the current year cash flow from opera-

tions exceeded prior year’s cash flow from operations by $937,437

($236,480 + $700,957). This apparent paradox can be explained by

evaluating the components of cash from operating activities. Significant

contributors to the positive cash flow figure in the current year were

(c) Liquidity: current cash debt coverage (net cash provided by operating

activities ÷ average current liabilities).

All of these ratios are very low. This is not surprising, however, for a

company like the Vermont Teddy Bear Company that is still in a growth

stage. When a company is in growth phase of its main product, it will

LO: 6, Bloom: AP, Difficulty: Simple, Time: 10-15, AACSB: Analytic, AICPA BB: Critical Thinking, AICPA FC: Reporting, AICPA PC: Problem Solving