PROBLEM 4.4 (Continued)

(a)Computation of income before income tax:

As previously stated ………………………..

€790,000

Uninsured flood loss ………………………..

(90,000)

Gain on sale of securities …………………

Error in computation of depreciation

As computed (€54,000 ÷ 6) ……………………

Corrected (€54,000 – €9,000) ÷ 6 ……………

Note: No adjustment is needed for the inventory method change, since the

PROBLEM 4.5

TWAIN CORPORATION

Income Statement

For the Year Ended June 30, 2019

Revenue

Sales revenue …………………………………………………….

$1,578,500

Less: Sales discounts ………………………………………..

$31,150

Sales returns ……………………………………………

93,450

Net sales …………………………………………………………….

Cost of goods sold …………………………………………………..

896,770

Gross profit ……………………………………………………………..

Selling expenses

Sales commissions ………………………….

$97,600

Salaries and wages expense (sales) ….

56,260

Travel expense ………………………………..

28,930

Entertainment expense …………………….

14,820

Telephone and internet exp. …………….

Maintenance and repairs expense …….

Depreciation expense ………………………

Bad debt expense …………………………...

PROBLEM 4.5 (Continued)

Administrative Expenses

Maintenance and repairs expense ………

9,130

Property tax expense …………………………

7,320

Depreciation expense ………………………..

7,250

Supplies expense …………………………..….

3,450

Telephone and internet expense ………..

2,820

Office expense ………………………………….

Other income and expense

Interest expense………………………………..

Income before income tax ……………………….

323,525

Income tax ………………………………………..

102,000

Net income …………………………..………………..

$221,525

PROBLEM 4.5 (Continued)

TWAIN CORPORATION

Retained Earnings Statement

For the Year Ended June 30, 2019

Retained earnings, July 1, 2018, as reported …………..

$337,000

Retained earnings, July 1, 2018, as adjusted ………….

Add: Net income ………………………………………………….

540,825

Less:

Dividends declared on preference shares ……….

$ 9,000

Dividends declared on ordinary shares …………

37,000

PROBLEM 4.6

1. The impairment of intangibles charge of ¥8,500,000 should be disclosed

separately, assuming it is material. This charge is shown above income

2. The loss on sale of equipment of ¥17,000,000 should be reported in the

3. The adjustment required for correction of an error is inappropriately

labeled and also should not be reported in the retained earnings

4. Earnings per share should be reported on the face of the income

statement and not in the notes to the financial statements. Because

PROBLEM 4.7

(a) ACADIAN CORP.

Retained Earnings Statement

For the Year Ended December 31, 2019

Retained earnings, January 1, as reported …………………………..

$257,600

Correction of error from prior period ………………………………………….

25,400

Adjustment for change in accounting principle ………………………….

Retained earnings, January 1, as adjusted …………………………..

Add: Net income …………………………………………………………………….

Less: Cash dividends declared …………………………………………………

32,000

(b) 1. Gain on sale of investments—body of income statement. This gain

should be shown under other income and expense on the income

statement.

PROBLEM 4.8

WADE NV

Income Statement (Partial)

For the Year Ended December 31, 2019

Income before income tax ……………………..

€1,325,000*

Income tax ……………………………………

265,000**

Income from continuing operations ……….

1,060,000

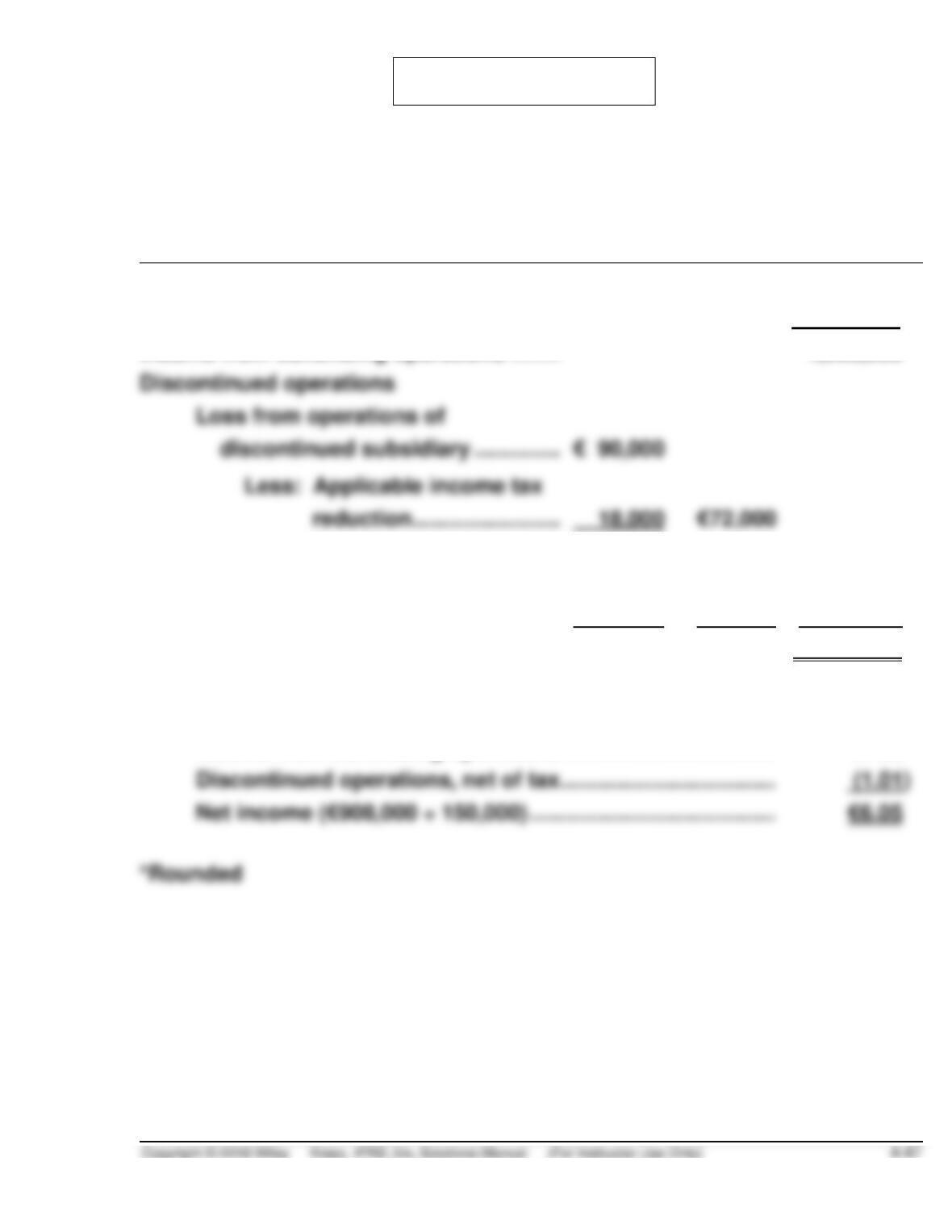

Discontinued operations

Less: Applicable income tax

reduction ……………………..

18,000

Loss from disposal of subsidiary ……..

100,000

Less: Applicable income tax

reduction ……………………..

20,000

80,000

(152,000)

Net income ……………………………………………

€ 908,000

Earnings per share*:

Income from continuing operations …………………………….

€7.06

Discontinued operations, net of tax ……………………………..

PROBLEM 4.8 (Continued)

*Computation of income before income tax:

As previously stated

€1,210,000

Loss on sale of equipment [€40,000 – (€80,000 – €30,000)]

(10,000)

Gain on condemnation of property

Restated

**Computation of income tax expense:

TIME AND PURPOSE OF CONCEPTS FOR ANALYSIS

CA 4.1 (Time 20–25 minutes)

Purpose—to provide the student with the opportunity to comment on deficiencies in an income

statement format. The student is required to comment on such items as inappropriate heading,

incorrect classification of unusual items, proper net of tax treatment, and presentation of per share data.

CA 4.2 (Time 20–25 minutes)

CA 4.3 (Time 15–20 minutes)

Purpose—to provide the student an illustration of how earnings can be managed by how losses are

reported, including ethical issues.

CA 4.4 (Time 30–35 minutes)

CA 4.5 (Time 30–40 minutes)

CA 4.6 (Time 20–25 minutes)

CA 4.7 (Time 10–15 minutes)

SOLUTIONS TO CONCEPTS FOR ANALYSIS

CA 4.1

The deficiencies of O’Malley plc’s income statement are as follows:

2. Dividends and gain on recovery of insurance proceeds should be classified as other income and

expense items.

4. Loss on obsolescence of inventories should be classified as an other income and expense item.

6. Intraperiod income tax allocation is required to relate income tax expense to income from continuing

operations, and loss on discontinued operations.

8. Per share data is a required presentation for income from continuing operations, discontinued

CA 4.2

(a) Earnings management is often defined as the planned timing of revenues, expenses, gains and

losses to smooth out bumps in earnings. In most cases, earnings management is used to increase

(b) Proposed Accounting

2016

2017

2018

2019

2020

Income before warranty expense

€43,000

€43,000

Warranty expense

7,000

3,000

(c) Appropriate Accounting

2016

2017

2018

2019

2020

Income before warranty expense

€43,000

€43,000

Warranty expense

5,000

5,000

CA 4.3

(a) The ethical issues involved are integrity and honesty in financial reporting, full disclosure,

accountant’s professionalism, and job security for Charlie.

CA 4.4

(a) It appears that the sale of the Casino Knights Division would qualify as a discontinued operation.

The operation of gambling facilities appears to meet the criteria for discontinued operations for

CA 4.4 (Continued)

(b) The “walkout” or strike should be reported as an “Other income and expense” item. Events of this

nature are a general risk that any business enterprise takes and should not warrant special

treatment.

CA 4.5

The income statement of Walters plc contains the following weaknesses in classification and

disclosure:

1. Sub-totals for gross profit, operating income, and income from continuing operations are not

provided.

2. Sales taxes. Sales taxes have been erroneously included in both gross sales and cost of goods

sold on the income statement of Walters plc. Failure to deduct these taxes directly from customer

3. Purchase discounts. Purchase discounts should not be treated as revenue by being lumped with

other revenues such as dividends and interest. A purchase discount is more logically a reduction

4. Recoveries of accounts written off in prior years. These collections should be credited to the

allowance for doubtful accounts unless the direct write-off method was used in accounting for bad

debt expense. Generally, the direct write-off method is not allowed.

5. Delivery expense and freight-in. Although delivery expense is an expense of selling and is

therefore reported properly in the statement, freight-in is an inventoriable cost and should have

6. Loss on discontinued styles. This type of loss, though often substantial, should not be treated

7. Loss on sale of marketable securities. This item should be reported as a separate component

of income from continuing operations and not as an unusual item.

CA 4.5 (Continued)

8. Loss on sale of warehouse. This item should be reported as a separate component of income

from continuing operations and not as an unusual item.

CA 4.6

Classification

Rationale

1.

No disclosure in current year.

Other income and expense section.

Material, unusual in nature, and non-recurring.

3.

Depreciation expense in body of income

statement, based on new useful life.

Material item, but change in estimated useful life

is considered part of normal business activity.

Error has “washed out”; that is, subsequent

income statement compensated for the error.

However, prior year income statements should

be restated.

5.

Discontinued operations section.

Sale meet the criteria for the disposal of a

component of a business.

6.

Adjustment to the beginning balance of

retained earnings.

Other income and expense section.

Material, unusual in nature, and non-recurring.

Other income and expense section.

Material, unusual in nature, and non-recurring.

Other income and expense section.

Material, unusual in nature, and non-recurring.

Discontinued operations section.

activities are clearly distinguishable physically,

operationally, and for financial reporting

purposes.

A change in inventory methods is a change in

accounting principle and prior periods are

adjusted.