CA 20.6

While Selma may be correct in assuming that the termination of non-vested employees would decrease

its pension-related liabilities and associated expenses, she is callous to suggest that firing employees is

FINANCIAL REPORTING PROBLEM

(a) M&S has funded pension plans (defined–benefit) for UK employees

and the majority of employees oversees. This plan applies to

(c) Impact on 2016 financial statements: credit to pension expense

decreased net income by £86.7 million; a net retirement benefit asset of

£824.1 million for Marks & Spencer UK retirement benefit, and a

remeasurement of retirement benefit schemes of £346.2 million less tax

effects of £45.6 million recognized in comprehensive income.

(d) M&S’s Analysis of assets portion of its pension footnote details the

major categories of assets, which are debt investments, Scottish

COMPARATIVE ANALYSIS CASE

(a) adidas has defined-benefit plans comprising a variety of post–

employment benefit arrangements (including defined contribution

plans).

Puma has both defined-benefit and defined contribution plans.

(d) Relevant rates used to compute pension information:

adidas

Discount rate

2.8%

Expected pension increases

1.7%

Expected rate of salary increase

3.1%

Puma

Future salary increases

Future pension increases

20–75 Copyright © 2018 Wiley Kieso, IFRS, 3/e, Solutions Manual (For Instructor Use Only)

ACCOUNTING, ANALYSIS, AND PRINCIPLES (Continued)

Journal entry:

PENCOMP, AG

Income Statement for the year ended Dec. 31, 2019

Revenues:

Sales ……………………………………………………………….. €3,000.00

Expenses:

ACCOUNTING, ANALYSIS, AND PRINCIPLES (Continued)

PENCOMP, AG

Statement of Financial Position

at December 31, 2019

Assets:

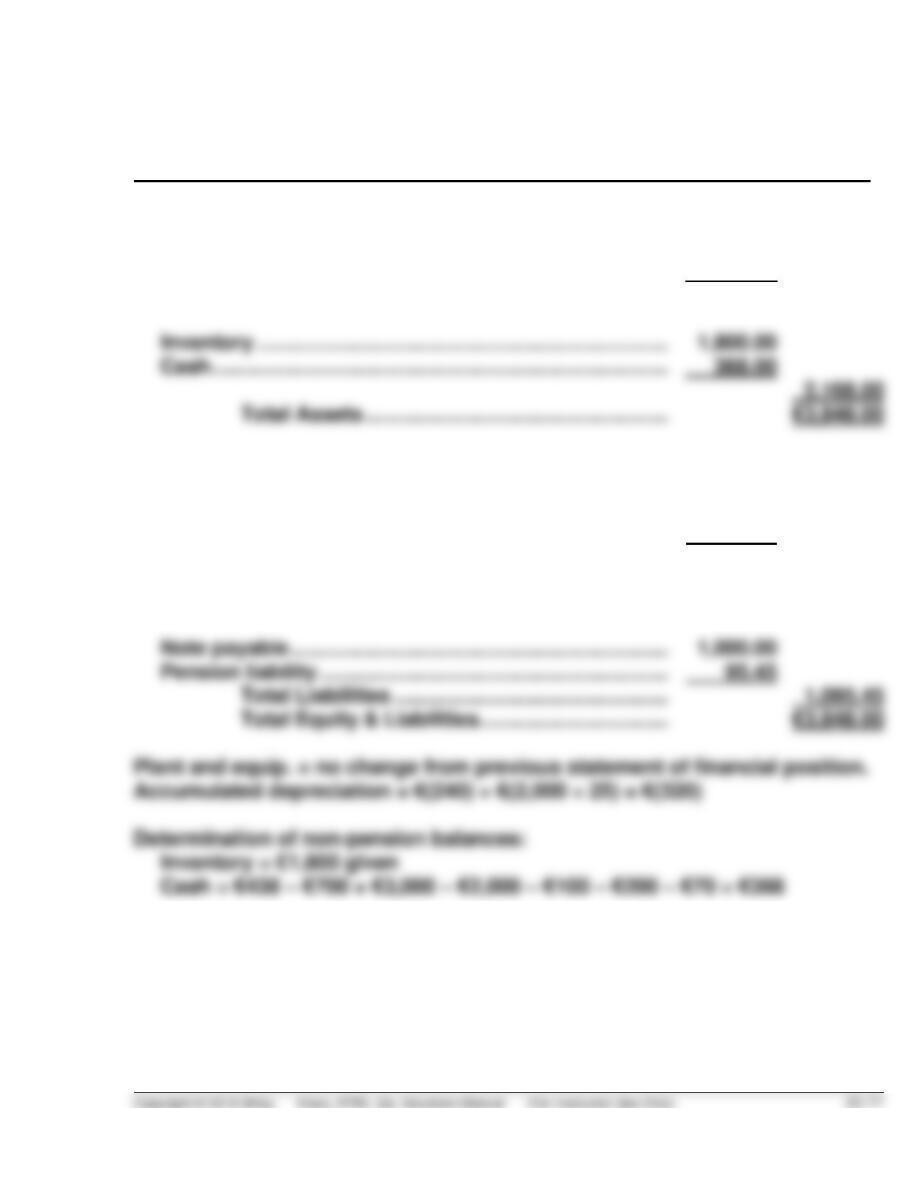

Plant and equipment …………………………..………………… €2,000.00

Accumulated depreciation ……………………………………. (320.00)

€1,680.00

Equity:

Share capital ………………………………………………………… €2,000.00

Retained earnings ………………………………………………… 752.55

Total Equity ……………………………………………… €2,752.55

Liabilities:

Note payable = no change from previous statement of financial position.

Share capital = no change from previous statement of financial position.

Retained earnings = €896.0 + €67.80 – €200 – €11.25 = €752.55

ACCOUNTING, ANALYSIS, AND PRINCIPLES (Continued)

ANALYSIS

ROE = €67.80 ÷ €2,752.55 = 0.0246 or 2.46%.

In this example, only the loss on plan assets ‘skipped’ the income

statement and went to other comprehensive income. Had this item been

PRINCIPLES

The effects of plan amendments and asset/liability gains and losses in a

given year can be thought of as fairly transitory items with respect to

RESEARCH CASE

(a) According to IAS 19, (pars 127-130) 127 Remeasurements of the net defined benefit liability

(asset) comprise: (a) actuarial gains and losses (see paragraphs 128 and 129); (b) the return on

plan assets (see paragraph 130), excluding amounts included in net interest on the net defined

benefit liability (asset) (see paragraph 125); and (c) any change in the effect of the asset ceiling,

excluding amounts included in net interest on the net defined benefit liability (asset) (see

paragraph 126).

According to par. 122: Remeasurements of the net defined benefit liability (asset) recognised in

other comprehensive income shall not be reclassified to profit or loss in a subsequent period.

However, the entity may transfer those amounts recognised in other comprehensive income

within equity.

(b) The IASB made the following points in it basis for conclusion for amendments to IAS 19 (pars

BC99 – BC99):

BC90 The Board confirmed the proposal made in the 2010 ED that an entity should recognise

remeasurements in other comprehensive income. The Board acknowledged that the Conceptual

CASE RESEARCH (Continued)

With respect to recycling these amounts into net income in subsequent periods:

BC99 Both before and after the amendments made in 2011, IAS 19 prohibits subsequent

reclassification of remeasurements from other comprehensive income to profit or loss. The

Board prohibited such reclassification because:

(c) According to IAS 19 (pars. 63-65),

63 An entity shall recognise the net defined benefit liability (asset) in the statement of financial

position.

64 When an entity has a surplus in a defined benefit plan, it shall measure the net defined

benefit asset at the lower of: (a) the surplus in the defined benefit plan; and (b) the asset ceiling,

determined using the discount rate specified in paragraph 83.

GAAP CONCEPTS AND APPLICATION

GAAP 20.1.The underlying concepts for the accounting for postretirement

benefits are similar between U.S. GAAP and IFRS—both U.S. GAAP

and IFRS view pensions and other postretirement benefits as forms

of deferred compensation. Other similarities include: (1) IFRS and

U.S. GAAP separate pension plans into defined contribution plans

GAAP 20.2. The IASB and the FASB have worked collaboratively on a

postretirement benefit project. The recent amendments issued by

the IASB moves IFRS closer to U.S. GAAP with respect to

GAAP 20.3.

(a) Asset and liability gains and losses are amortized as are past service

costs under U.S. GAAP. This is shown as “Amortization” by Zarle.

Under IFRS, asset gains and losses are reported as part of

comprehensive income and past service costs are recognized as part

of pension expense as incurred.

(b) Under IFRS, no amortization of past service costs results in higher

pension expense with respect to prior (past) service costs in the year

past service costs are granted and lower expense in other years.

Depending on whether the company has unrealized gains or losses,

these are not recorded in net income, which reduces the volatility of