CHAPTER 19

Accounting for Income Taxes

ASSIGNMENT CLASSIFICATION TABLE (BY TOPIC)

Topics

Questions

Brief

Exercises

Exercises

Problems

Concepts

for Analysis

1. Reconcile pretax financial

income with taxable income.

1, 12

1

1, 2, 4, 12, 18

1, 2, 3, 8

2. Identify temporary and

permanent differences.

3, 4, 5

4, 6, 7

1, 2, 3, 4

3, 4, 5

single tax rate.

6, 9

8, 12, 14, 15,

4. Classification of deferred

taxes.

10, 11

3, 15

7, 11, 16, 18,

19, 20, 21, 22

3, 6

2, 3, 5

multiple tax rates.

20, 21

6. Carryback and carryforward

of NOL.

15, 16, 17

12, 13, 14

9, 10, 23,

24, 25

5

7. Change in enacted future

tax rate.

13

11

16

2, 7

5, 6

8. Tracking temporary differences

through reversal.

17

2, 7

12, 16, 19, 23,

24, 25

7, 8, 9

2, 8

7

1, 2, 7

8

7

7, 14, 15, 23,

24, 25

ASSIGNMENT CLASSIFICATION TABLE (BY LEARNING OBJECTIVE)

Learning Objectives

Brief

Exercises

Exercises

Problems

Concepts

for

Analysis

1. Describe the fundamentals of

accounting for income taxes.

1, 2, 3, 4, 5,

6, 7, 9, 14

1, 2, 3, 4, 5, 6,

7, 8, 11, 12,

13, 14, 15, 16,

17, 18, 19, 20,

21, 22

1, 2, 3, 4, 6,

7, 8, 9

1, 2, 3, 4,

5, 6, 7

3, 4, 6, 8, 10,

1, 3, 4, 5, 6, 7,

8, 12, 13, 15,

16, 17, 18, 19,

1, 2, 3, 4, 5,

7, 8, 9

7

3. Explain the accounting for loss

carrybacks and loss carryforwards.

12, 13, 14

9, 10, 23,

24, 25

5

6

4. Describe the presentation of

statements.

7, 8, 11, 16,

19, 20, 21, 22,

23, 24, 25

3, 5, 6, 7, 8,

9

4

ASSIGNMENT CHARACTERISTICS TABLE

Item

Description

Level of

Difficulty

Time

(minutes)

E19.1

One temporary difference, future taxable amounts, one rate, no

beginning deferred taxes.

Simple

15–20

E19.2

Two differences, no beginning deferred taxes, tracked through

2 years.

Simple

15–20

E19.3

One temporary difference, future taxable amounts, one rate,

beginning deferred taxes.

Simple

15–20

E19.4

Three differences, compute taxable income, entry for taxes.

Simple

15–20

E19.5

Two temporary differences, one rate, beginning deferred taxes.

Simple

15–20

E19.6

Identify temporary or permanent differences.

Simple

10–15

E19.7

Terminology, relationships, computations, entries.

Simple

10–15

E19.8

Two temporary differences, one rate, 3 years.

Simple

10–15

E19.9

Carryback and carryforward of NOL, no temporary differences.

Simple

15–20

E19.10

Two NOLs, no temporary differences, entries and income

statement.

Moderate

20–25

E19.11

Three differences, classify deferred taxes.

Simple

10–15

E19.12

Two temporary differences, one rate, beginning deferred taxes,

compute pretax financial income.

Complex

20–25

E19.13

One difference, multiple rates, effect of beginning balance

versus no beginning deferred taxes.

Simple

20–25

E19.14

Deferred tax asset.

Moderate

20–25

E19.15

Deferred tax asset.

20–25

E19.16

Deferred tax liability, change in tax rate, prepare section of

income statement.

Complex

15–20

E19.17

Two temporary differences, tracked through 3 years,

multiple rates.

Moderate

30–35

E19.18

Three differences, multiple rates, future taxable income.

Moderate

20–25

E19.19

Two differences, one rate, beginning deferred balance, compute

pretax financial income.

Complex

25–30

E19.20

Two differences, no beginning deferred taxes, multiple rates.

Moderate

15–20

E19.21

income.

E19.22

Two differences, one rate, first year.

Simple

15–20

E19.23

NOL carryback and carryforward, recognition versus

Complex

30–35

E19.24

NOL carryback and carryforward, non-recognition.

30–35

Two temporary differences, multiple rates, future taxable

Moderate

20–25

ASSIGNMENT CHARACTERISTICS TABLE (Continued)

Item

Description

Level of

Difficulty

Time

(minutes)

P19.1

Three differences, no beginning deferred taxes, multiple rates.

Complex

40–45

P19.2

One temporary difference, tracked for 4 years, one permanent

difference, change in rate.

Complex

50–60

P19.3

Second year of depreciation difference, two differences, single

Complex

40–45

P19.4

Permanent and temporary differences, one rate.

20–25

Recognition of NOL.

P19.6

Two differences, two rates, future income expected.

20–25

P19.7

One temporary difference, tracked 3 years, change in rates,

income statement presentation.

Complex

45–50

P19.8

Two differences, 2 years, compute taxable income and pretax

financial income.

Complex

40–50

P19.9

Five differences, compute taxable income and deferred taxes,

draft income statement.

Complex

40–50

Objectives and principles for accounting for income taxes.

15–20

Basic accounting for temporary differences.

20–25

Identify temporary differences and classification criteria.

Complex

20–25

Accounting for deferred income taxes.

20–25

Explain computation of deferred tax liability for multiple tax rates.

Complex

20–25

Explain future taxable and deductible amounts, how carryback

and carryforward affects deferred taxes.

Complex

20–25

Deferred taxes, income effects.

20–25

ANSWERS TO QUESTIONS

1. Pretax financial income is reported on the income statement and is often referred to as income

2. One objective of accounting for income taxes is to recognize the amount of taxes payable or

refundable for the current year. A second is to recognize deferred tax liabilities and assets for the

3. A permanent difference is a difference between taxable income and pretax financial income that,

under existing applicable tax laws and regulations, will not be offset by corresponding differences

or “turn around” in other periods. Therefore, a permanent difference is caused by an item that:

(1) is included in pretax financial income but never in taxable income, or (2) is included in taxable

income but never in pretax financial income.

4. A temporary difference is a difference between the tax basis of an asset or liability and its

reported (carrying or book) amount in the financial statements that will result in taxable amounts

or deductible amounts in future years when the reported amount of the asset is recovered or

when the reported amount of the liability is settled. The temporary differences discussed in this

chapter all result from differences between taxable income and pretax financial income which will

reverse and result in taxable or deductible amounts in future periods.

5. An originating temporary difference is the initial difference between the book basis and the tax basis

of an asset or liability. A reversing difference occurs when a temporary difference that originated

Questions Chapter 19 (Continued)

6. Book basis of assets €900,000

Tax basis of assets ………………………………………………………………………… 700,000

7.

Book basis of asset

€90,000

Deferred tax liability (end of 2019)

€ 30,600

Tax basis of asset

0

Deferred tax liability (beginning of 2019)

68,000

Future taxable amounts

Deferred tax benefit for 2019

Tax rate

Income taxes payable for 2019

230,000

Deferred tax liability (end of 2019)

€30,600

Total income tax expense for 2019

€192,600

8. A future taxable amount will increase taxable income relative to pretax financial income in future

periods due to temporary differences existing at the statement of financial position date. A future

deductible amount will decrease taxable income relative to pretax financial income in future periods

9.

Taxable income

Future taxable amounts

£70,000

Tax rate

X 40%

Tax rate

40%

Income taxes payable

Deferred tax liability (end of 2019)

£28,000

Deferred tax liability (end of 2019)

Current tax expense

£40,000

Deferred tax expense for 2019

Income tax expense for 2019

£68,000

10. Deferred tax accounts are reported on the statement of financial position as assets and liabilities.

They should be classified in a net non-current amount.

LO: 1,2,4, Bloom: C, Difficulty: Simple, Time: 3-5, AACSB: None, AICPA BB: None, AICPA FC: Reporting, AICPA PC: Communication

11. Deferred tax assets and deferred tax liabilities are separately recognized and measured but are

12. Pretax financial income …………………………………………………………………………… $550,000

Interest income on governmental bonds ……………………………………………………. (70,000)

Questions Chapter 19 (Continued)

13. £200,000 (2021 taxable amount)

X 10% (30% – 20%)

14. Some of the reasons for requiring income tax component disclosures are:

(a) Assessment of the quality of earnings. Many investors seeking to assess the quality of a

company’s earnings are interested in the relation of pre-tax financial income and taxable

15. The loss carryback provision permits a company to carry a net operating loss back two years and

receive refunds for income taxes paid in those years. The loss must be applied to the second

16. The company may choose to carry the net operating loss forward, or carry it back and then

forward for tax purposes. To forego the two-year carryback might be advantageous where a tax-

payer had tax credit carryovers that might be wiped out and lost because of the carryback of the

17. Many believe that future deductible amounts arising from net operating loss carryforwards are

different from future deductible amounts arising from normal operations. One rationale provided

is that a deferred tax asset arising from normal operations results in a tax prepayment—a prepaid

tax asset. In the case of loss carryforwards, no tax prepayment has been made.

Others argue that realization of a loss carryforward is less likely—and thus should require a more

SOLUTIONS TO BRIEF EXERCISES

BRIEF EXERCISE 19.1

2019 taxable income ………………………………………………………. $120,000

BRIEF EXERCISE 19.2

Excess depreciation on tax return ………………………………….. €40,000

BRIEF EXERCISE 19.3

Income Tax Expense …………………………………………. 67,500***

Deferred Tax Liability ………………………………….. 12,000**

BRIEF EXERCISE 19.4

Deferred tax liability, 12/31/19 ………………………………………………. $42,000

Deferred tax liability, 12/31/18 ………………………………………………. (25,000)

BRIEF EXERCISE 19.5

Book value of warranty liability ……………………………………………. £105,000

Tax basis of warranty liability ……………………………………………… 0

BRIEF EXERCISE 19.6

Deferred tax asset, 12/31/19 ………………………………………………… $59,000

BRIEF EXERCISE 19.7

Income Tax Expense ………………………………………………. 60,000

BRIEF EXERCISE 19.8

Income before income taxes …………………………………… $195,000

BRIEF EXERCISE 19.9

Income Tax Expense ………………………………………………. 71,100

BRIEF EXERCISE 19.10

Year

Future taxable amount

X

Tax Rate

=

Deferred tax liability

2019

$ 42,000

34%

$ 14,280

2020

34%

2021

40%

$214,840

BRIEF EXERCISE 19.11

Income Tax Expense ……………………………………….. 120,000,000

BRIEF EXERCISE 19.12

Income Tax Refund Receivable ………………………… 144,000

LO: 3, Bloom: AP, Difficulty: Simple, Time: 5-7, AACSB: Analytic, AICPA BB: Critical Thinking, AICPA FC: Reporting, AICPA PC: Problem Solving

BRIEF EXERCISE 19.13

Income Tax Refund Receivable (€350,000 X .40) … 140,000

BRIEF EXERCISE 19.14

Income Tax Refund Receivable (€350,000 X .40) … 140,000

BRIEF EXERCISE 19.15

Non-current liabilities

SOLUTIONS TO EXERCISES

EXERCISE 19.1 (15–20 minutes)

(a) Pretax financial income for 2018 …………………………………… $400,000

Temporary difference resulting in future taxable

(b)

Future Years

2019

2020

2021

Total

Future taxable (deductible) amounts

$55,000

$60,000

$75,000

$190,000

Tax rate

X 30%

X 30%

X 30%

Deferred tax liability (asset)

$16,500

$18,000

$22,500

$ 57,000

Deferred tax liability at the end of 2018 ……………… $ 57,000

(c) Income before income taxes …………………………….. $400,000

Income tax expense

Current …………………………………………………….. $63,000

EXERCISE 19.2 (15–20 minutes)

(a) Pretax financial income for 2019 ……………………… £350,000

(b) Income Tax Expense …………………………..………….. 140,000

Deferred Tax Asset …………………………………………. 10,000*

Income Taxes Payable (£335,000 X .40) ……… 134,000

**Depreciation

(c) Income Tax Expense …………………………..………….. 136,000*

Deferred Tax Liability (£10,000 X .40) ……………….. 4,000

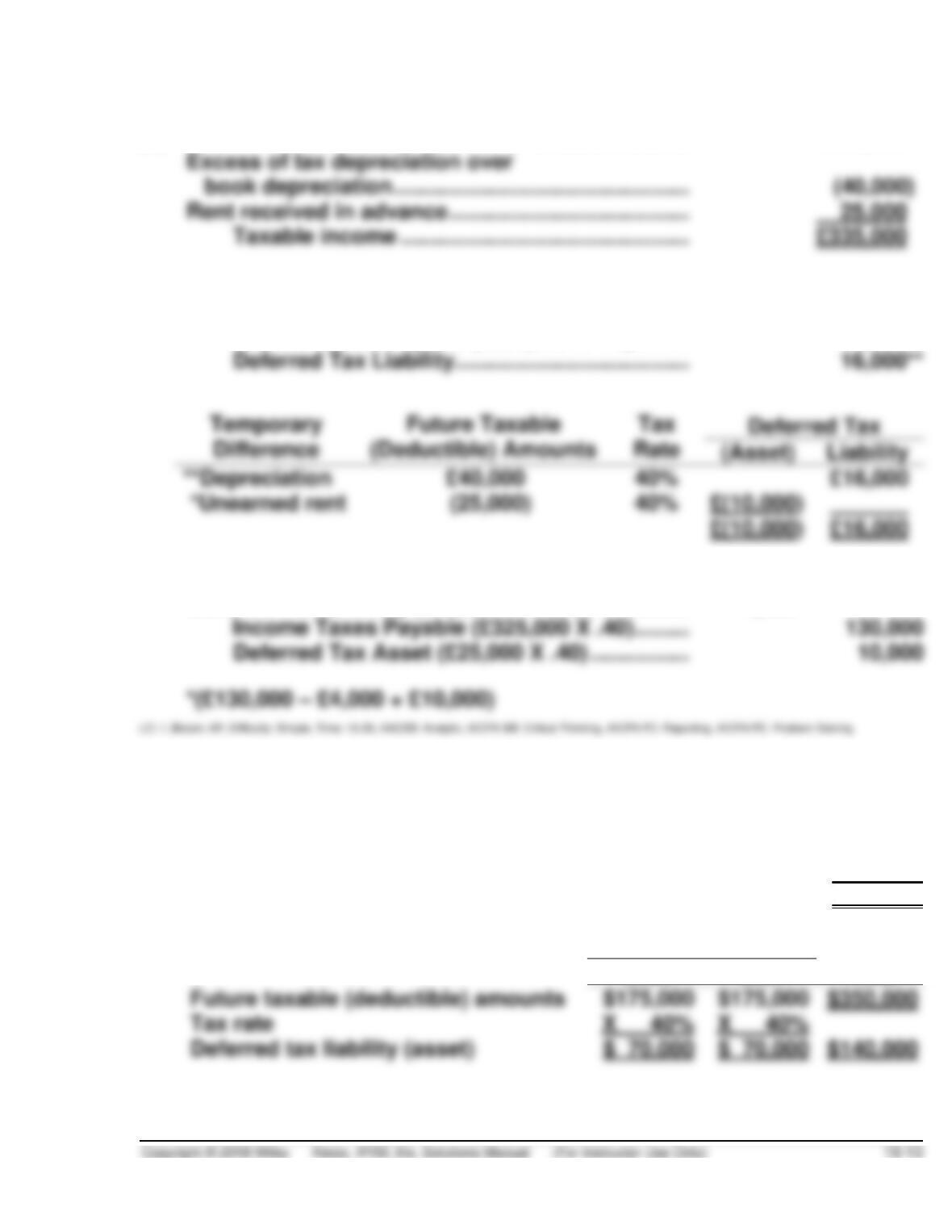

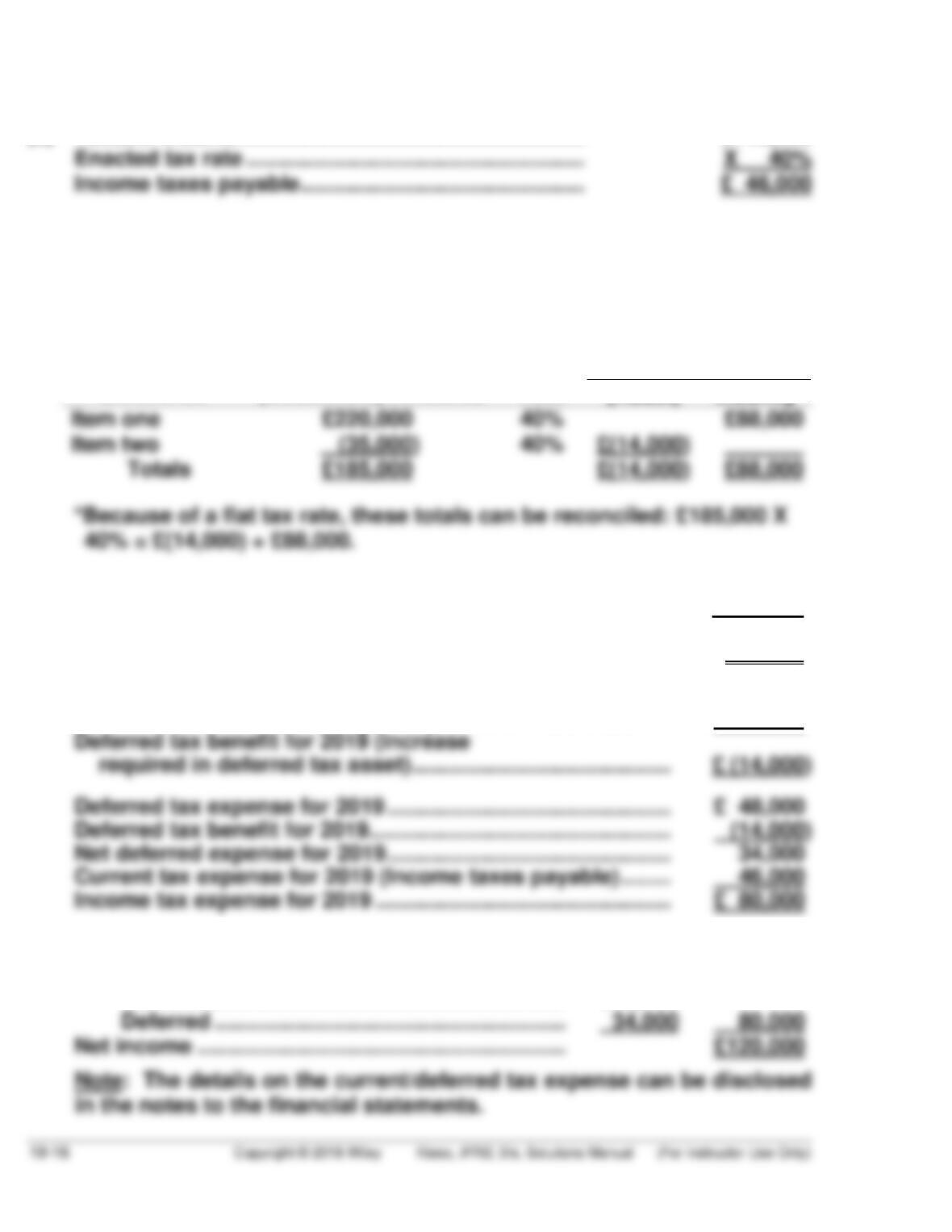

EXERCISE 19.3 (15–20 minutes)

(a) Taxable income for 2019 ………………………………… $400,000

Enacted tax rate …………………………………………….. X 40%

Income taxes payable for 2019 ……………………….. $160,000

(b)

Future Years

2020

2021

Total

Future taxable (deductible) amounts

Tax rate

Deferred tax liability (asset)

EXERCISE 19.3 (Continued)

Deferred tax liability at the end of 2019 …………… $140,000

Deferred tax liability at the beginning of 2019 …. 90,000

(c) Income before income taxes ………………………….. $525,000

Income tax expense

Note to instructor: Because of the flat tax rate for all years, the amount

of cumulative temporary difference existing at the beginning of the

year can be calculated by dividing $90,000 by 40%, which equals

$225,000. The difference between the $225,000 cumulative temporary

difference at the beginning of 2019 and the $350,000 cumulative tem-

porary difference at the end of 2019 represents the net amount of

temporary difference originating during 2019 (which is $125,000). With

this information, we can reconcile pretax financial income with taxable

income as follows:

Pretax financial income ………………………………………………… $525,000

EXERCISE 19.4 (15–20 minutes)

(a) Pretax financial income for 2019 …………………………………… € 80,000

Excess depreciation per tax return ……………………………….. (16,000)

EXERCISE 19.4 (Continued)

(b) Income Tax Expense …………………………..…………… 27,300

Deferred Tax Asset ………………………………………….. 8,100

Income Taxes Payable …………………………..….. 30,600

Deferred Tax Liability ………………………………… 4,800

Temporary

Difference

Future Taxable

(Deductible) Amounts

Tax

Rate

Deferred Tax

(Asset)

Liability

Depreciation

(€ 16,000

30%

€4,800

Unearned rent

( (27,000)

30%

Totals

€4,800*

Deferred tax asset at the end of 2019 …………………………….. € 8,100

Deferred tax asset at the beginning of 2019 …………………… 0

Deferred tax benefit for 2019 (increase

required in deferred tax asset) …………………………………… € (8,100)

(c) Income before income taxes ………………………….. €80,000

Income tax expense

Current ………………………………………………….. €30,600

Deferred ………………………………………………… (3,300) 27,300

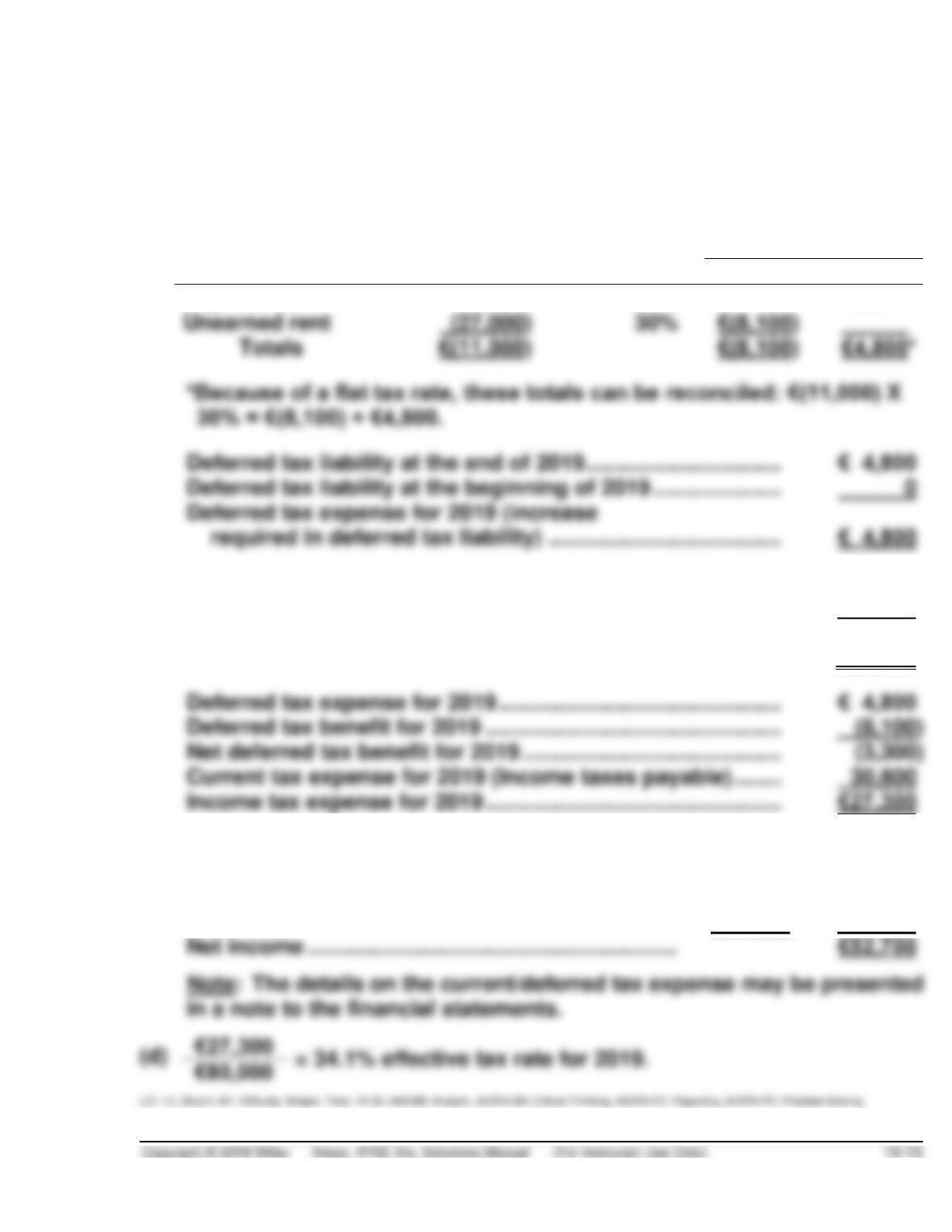

EXERCISE 19.5 (15–20 minutes)

(a) Taxable income ……………………………………………….. £115,000

(b) Income Tax Expense ……………………………………….. 80,000

Deferred Tax Asset …………………………..……………… 14,000

Income Taxes Payable ………………………………. 46,000

Deferred Tax Liability ………………………………… 48,000

Temporary

Difference

Future Taxable

(Deductible) Amounts

Tax

Rate

Deferred Tax

(Asset)

Liability

Deferred tax liability at the end of 2019 ………………………….. £ 88,000

Deferred tax liability at the beginning of 2019 ………………… (40,000)

Deferred tax expense for 2019 (increase

required in deferred tax liability) ………………………………… £ 48,000

Deferred tax asset at the end of 2019 …………………………….. £ (14,000

Deferred tax asset at the beginning of 2019 …………………… 0

(c) Income before income taxes ………………………….. £200,000

Income tax expense

Current ………………………………………………….. £46,000

EXERCISE 19.5 (Continued)

Note to instructor: Because of the flat tax rate for all years, the amount

of cumulative temporary difference existing at the beginning of the

year can be calculated by dividing the £40,000 balance in Deferred Tax

EXERCISE 19.6 (10–15 minutes)

(a) (2) (e) (2) (i) (1)

(b) (1) (f) (3) (j) (1)

EXERCISE 19.7 (10–15 minutes)

(a) greater than

(b) $170,000 = ($68,000 divided by 40%)

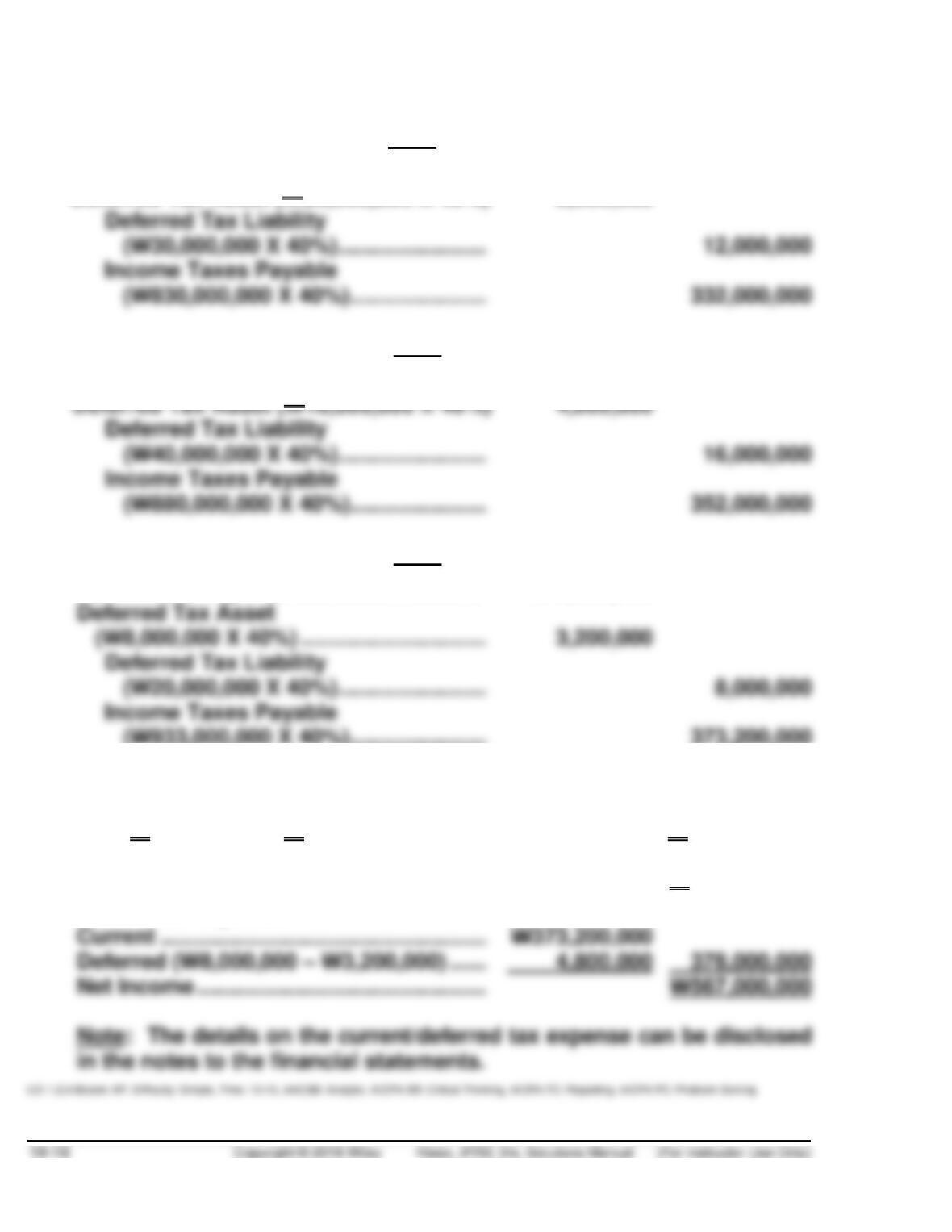

EXERCISE 19.8 (10–15 minutes)

(a) 2018

Income Tax Expense ………………………….. 336,000,000

Deferred Tax Asset (W20,000,000 X 40%) 8,000,000

2019

Income Tax Expense ………………………….. 364,000,000

2020

Income Tax Expense …………………………. 378,000,000

(W933,000,000 X 40%) …………………. 373,200,000

(b) Non-current liabilities

Deferred tax liability

(W36,000,000 – W15,200,000) ………. W 20,800,000

(c) Pretax financial income …………………….. W945,000,000

Income tax expense

EXERCISE 19.9 (15–20 minutes)

2016

Income Tax Expense ……………………………………………….. 36,000

Income Taxes Payable ($90,000 X 40%) ……………… 36,000

2017

Income Tax Refund Receivable

($160,000 X 45%) …………………………………………………. 72,000

Deferred Tax Asset ………………………………………………….. 104,000

Benefit Due to Loss Carryforward

(Income Tax Expense)

[40% X ($350,000 – $90,000)] ………………………….. 104,000

2019

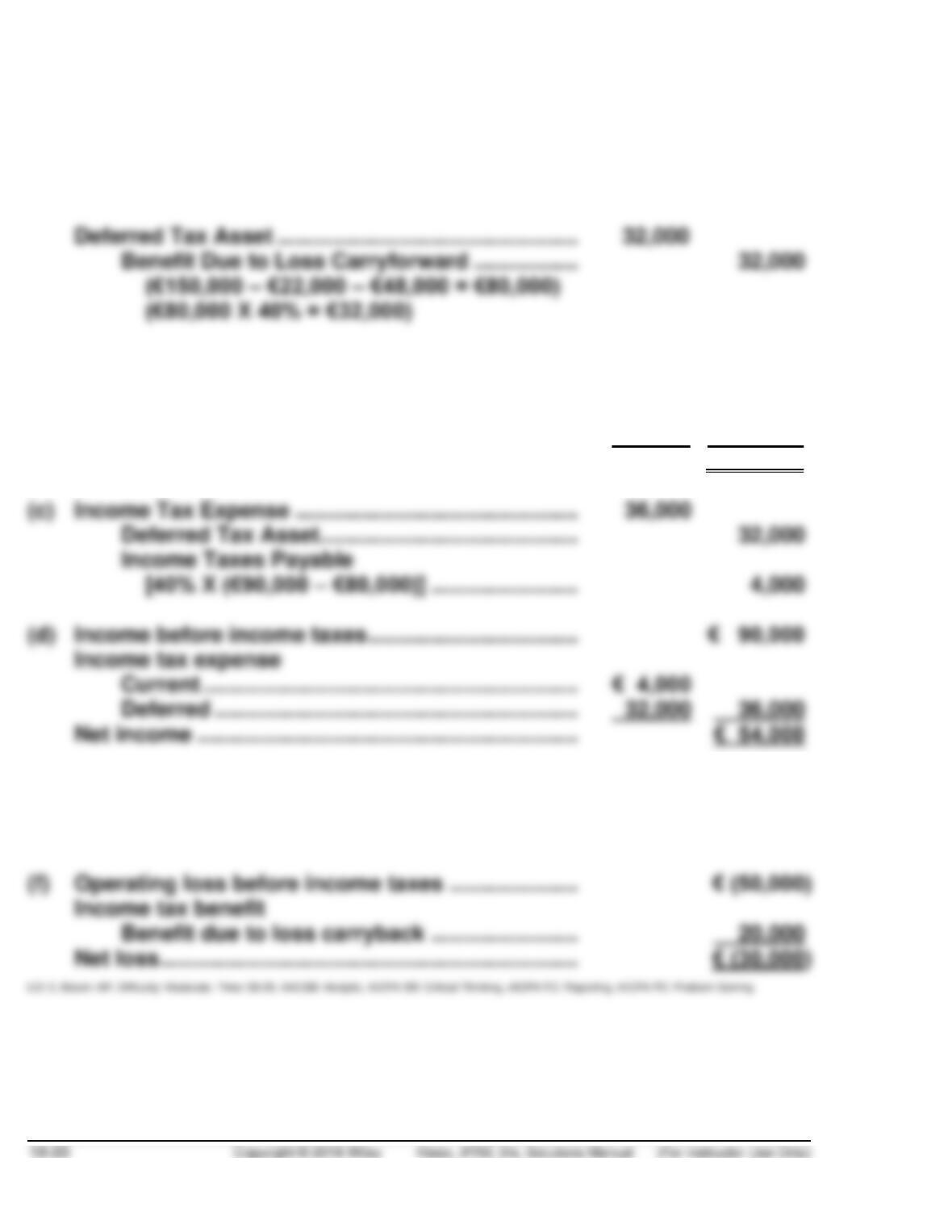

EXERCISE 19.10 (20–25 minutes)

(a) Income Tax Refund Receivable

[(€22,000 X 35%) + (€48,000 X 50%)] ……………… 31,700

Benefit Due to Loss Carryback …………………. 31,700

(b) Operating loss before income taxes ………………… €(150,000)

Income tax benefit

Benefit due to loss carryback …………………… €31,700

Benefit due to loss carryforward ……………….. 32,000 63,700

Net loss ………………………………………………………….. € (86,300)

(e) Income Tax Refund Receivable

(€50,000 X 40%) …………………………………………… 20,000

Benefit Due to Loss Carryback …………………. 20,000