CA 4.7

(a) Separate Statement

Current Year

Prior Year

. . . income components . . .

Statement of Comprehensive Income

Net income ………………………………………………………………….

Unrealized gains …………………………………………………………..

15,000

(b) Combined Format

. . . income components . . .

Net income …………………………………………………………………..

$400,000

$410,000

Other comprehensive income

Unrealized gains ……………………………………………………………

15,000

(c) Nelson can choose either approach, according to IFRS. The method chosen should be based on

FINANCIAL REPORTING PROBLEM

(a) M&S uses a condensed format income statement. This format provides

highlights of a company’s performance without presenting unnecessary

detailed computations.

(c) M&S’s gross profit was £3,985.5m in 2015 and increased to £4,128.4m

in 2016. Gross profit increased in 2016 because Revenue increased

£244m while cost of sales increased only £101.1m.

(e) The directors believe that the underlying profit and earnings per share

measures provide additional useful information for shareholders on

the underlying performance of the business. These measures are

consistent with how underlying business performance is measured

internally. The underlying profit before tax measure is not a recognized

profit measure under IFRS and may not be directly comparable with

adjusted profit measures used by other companies. The adjustments

made to reported profit before tax are to exclude the following:

• Profits and losses on the disposal of properties or impairments of

• Fair value movement in financial instruments;

• Costs relating to strategy changes that are not considered normal

operating costs of the underlying business;

COMPARATIVE ANALYSIS CASE

(a) adidas’ 16.4% increase in revenues from 2014 to 2015 was greater than

Puma’s 10% increase.

(b) adidas had a discontinued operation in 2015, and Puma did not. Since

(c) adidas depreciation expense was 25.6% (£279 ÷ £1,090) of its operating

cash flow and was significantly lower than Puma’s 42.8% (€57.5 ÷

€134.5).

FINANCIAL STATEMENT ANALYSIS CASE 1

(a) Depending on the company chosen, student answers will vary. Given

the ready availability, the analysis for Nokia is provided below:

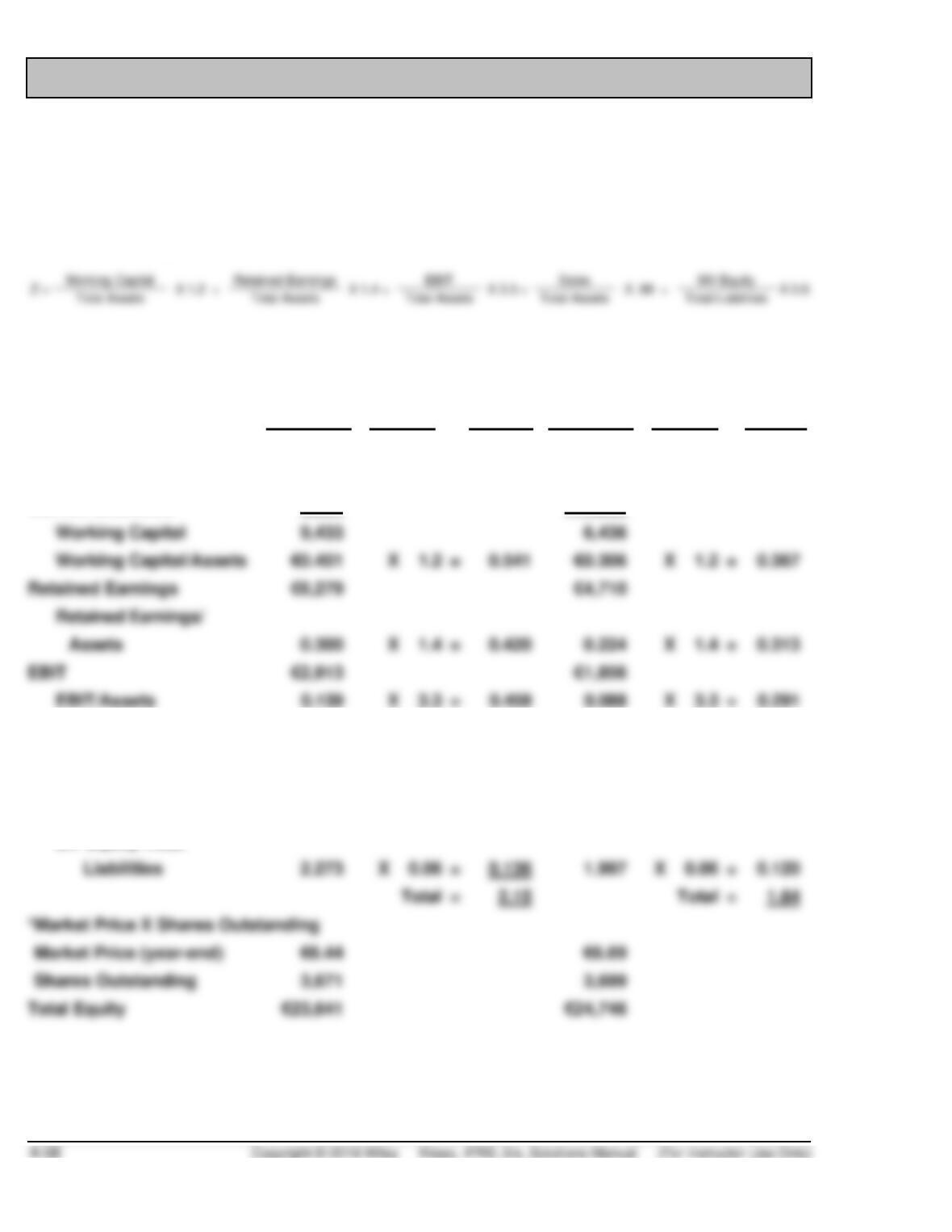

Z-Score Analysis

Nokia ($000,000)

2015

Weights

Z-Score

2015

2014

Weights

Z-Score

2014

Total Assets

€20,926

€21,063

Current Assets

15,824

13,724

Current Liabilities

6,391

7,288

Working Capital

9,433

6,436

Working Capital/Assets

X 1.2

=

X 1.2

=

Retained Earnings

EBIT

EBIT/Assets

X 3.3

=

0.088

X 3.3

=

0.291

Sales

€12,499

€11,762

Sales/Assets

0.597

X 0.99

=

0.591

0.558

X 0.99

=

0.553

MV Equity*

€23,641

€24,746

Total Liabilities

10,402

12,394

Liabilities

2.273

=

=

*Market Price X Shares Outstanding

Market Price (year-end)

Shares Outstanding

Total Equity

€23,641

€24,746

MV Equity/Total

FINANCIAL STATEMENT ANALYSIS CASE 1 (Continued)

(b) Nokia’s Z-score in 2015 has improved but is still below the cutoff

(c) EBIT is an operating income measure. By adding back items less

relevant to predicting future operating results (interest, taxes), it is

viewed as a better indicator of future profitability.

FINANCIAL STATEMENT ANALYSIS CASE 2

(a) Assumptions and estimates related to items such as bad debt expense,

(b) See the table below.

December 31, 2015

Price

EPS

Sales per

Share

P/E

PSR

adidas

.87

Puma

.88

(c) Puma has a higher P/E relative to adidas (almost 4-times). But Puma’s

PSR is slightly higher than that for adidas’. Thus, it would appear that

ACCOUNTING, ANALYSIS, PRINCIPLES

ACCOUNTING

COUNTING CROWS LTD

Statement for the Income

For the Year Ended December 31, 2019

Sales revenue ……………………………………………….. £1,900,000

Cost of goods sold ………………………………………… 850,000

Gross profit …………………………………………………… 1,050,000

Selling expenses …………………………………………… £300,000

Administrative expenses ……………………………….. 240,000 540,000

Earnings per share*:

Income from continuing operations

(£425,700 ÷ 100,000) ……………………………………. £ 4.26

*Rounded

COUNTING CROWS LTD

Statement of Retained Earnings

For the Year Ended December 31, 2019

Retained earnings, January 1 …………………………………….. £600,000

ACCOUNTING, ANALYSIS, PRINCIPLES (Continued)

COUNTING CROWS LTD

Statement of Comprehensive Income

For the Year Ended December 31, 2019

Net income …………………………………………………………………….. £376,200

ANALYSIS

The detailed income statement recognizes important relationships between

income statement elements. For example, by separating operating transac–

tions from nonoperating transactions, the statement user can distinguish

PRINCIPLES

Pro forma reporting is inconsistent with the conceptual framework’s qualita–

Note to instructor: This is the reason the U.S. SEC issued Regulation G,

which requires companies that list securities in U.S. markets and that issue

RESEARCH CASE

(a) International Accounting Standard 1, Presentation of Financial Statements

addresses the statement of comprehensive income reporting. This

standard was issued in September 2007 and includes subsequent

loss’ and of ‘other comprehensive income’ (Paragraph 7).

(c) Paragraphs 85 and 86 provide the rationale for presenting additional

information: An entity shall present additional line items, headings and

Because the effects of an entity’s various activities, transactions and

other events differ in frequency, potential for gain or loss and predict–

ability, disclosing the components of financial performance assists

users in understanding the financial performance achieved and in

making projections of future financial performance. An entity includes

additional line items in the statement of comprehensive income and

RESEARCH CASE (Continued)

(d) When items of income or expense are material, an entity shall disclose

their nature and amount separately (Para. 97).

Circumstances that would give rise to the separate disclosure of items

of income and expense include:

a. write-downs of inventories to net realizable value or of property,

plant and equipment to recoverable amount, as well as reversals

of such write-downs;

GAAP CONCEPTS and APPLICATION

4.1. There is no U.S. GAAP in this area, except the SEC does require

4.2. Bradshaw should report this item in “Other revenues and expenses.”

4.3. As in IFRS, U.S. GAAP provides for two possible reporting formats for

4.4 (a) Some of the differences are:

1. Units of currency—Campbell and all U.S. companies report in

dollars and earnings per share in dollars and cents. International

Some similarities are:

1. Campbell appears to use a function-of-expense approach. It may

provide additional nature-of-expense information in the notes.

(b) Campbell reports no discontinued operations in 2016, but does report

earnings from discontinued operations in 2014. The “Earnings from

discontinued operations” or gain or losses are an example of a non-

recurring item. As in IFRS companies’ income statements, these items