PROBLEM 17.1 (Continued)

Amortized

Cost

Fair

Value

Unrealized

Gain (Loss)

Spangler Company, 7% bonds

$103,719

$105,650

$1,931

PROBLEM 17.2

(a) January 1, 2019 purchase entry:

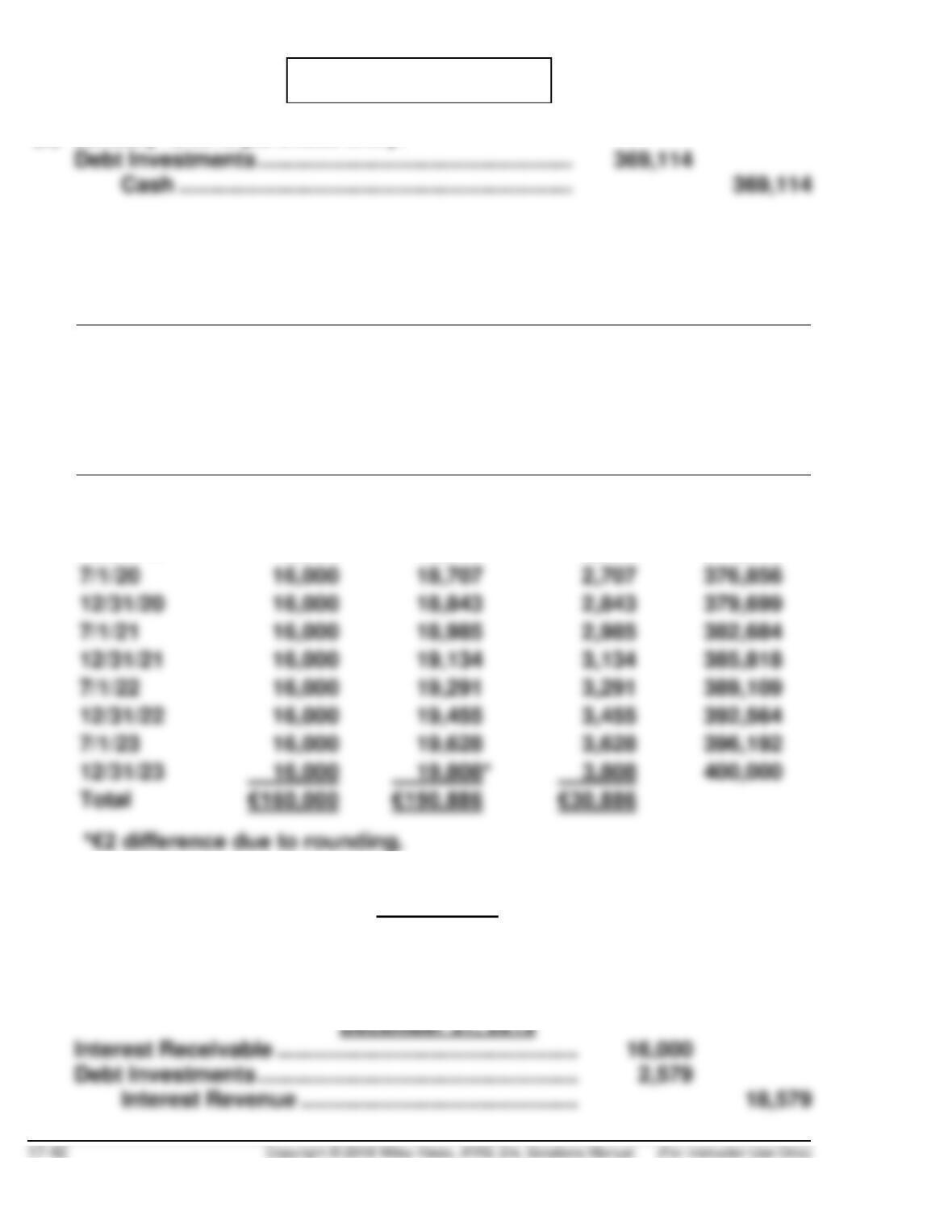

(b) The amortization schedule is as follows:

Schedule of Interest Revenue and Bond

Discount Amortization

8% Bonds Purchased to Yield 10%

Date

Interest

Receivable

Or

Cash Received

(1)

Interest

Revenue

@10%

(2)

Bond

Discount

Amortization

(2–1)

Carrying

Amount of

Bonds

1/1/19

—

—

—

€369,114

7/1/19

€ 16,000

€ 18,456

€ 2,456

371,570

12/31/19

16,000

18,579

2,579

374,149

16,000

18,707

2,707

376,856

16,000

18,843

2,843

379,699

16,000

19,134

3,134

385,818

16,000

19,291

3,291

389,109

16,000

19,455

3,455

392,564

16,000

19,628

3,628

396,192

400,000

Total

(c) Interest entries:

July 1, 2019

Cash ………………………………………………………………. 16,000

Debt Investments ……………………………………………. 2,456

Interest Revenue ……………………………………… 18,456

PROBLEM 17.2 (Continued)

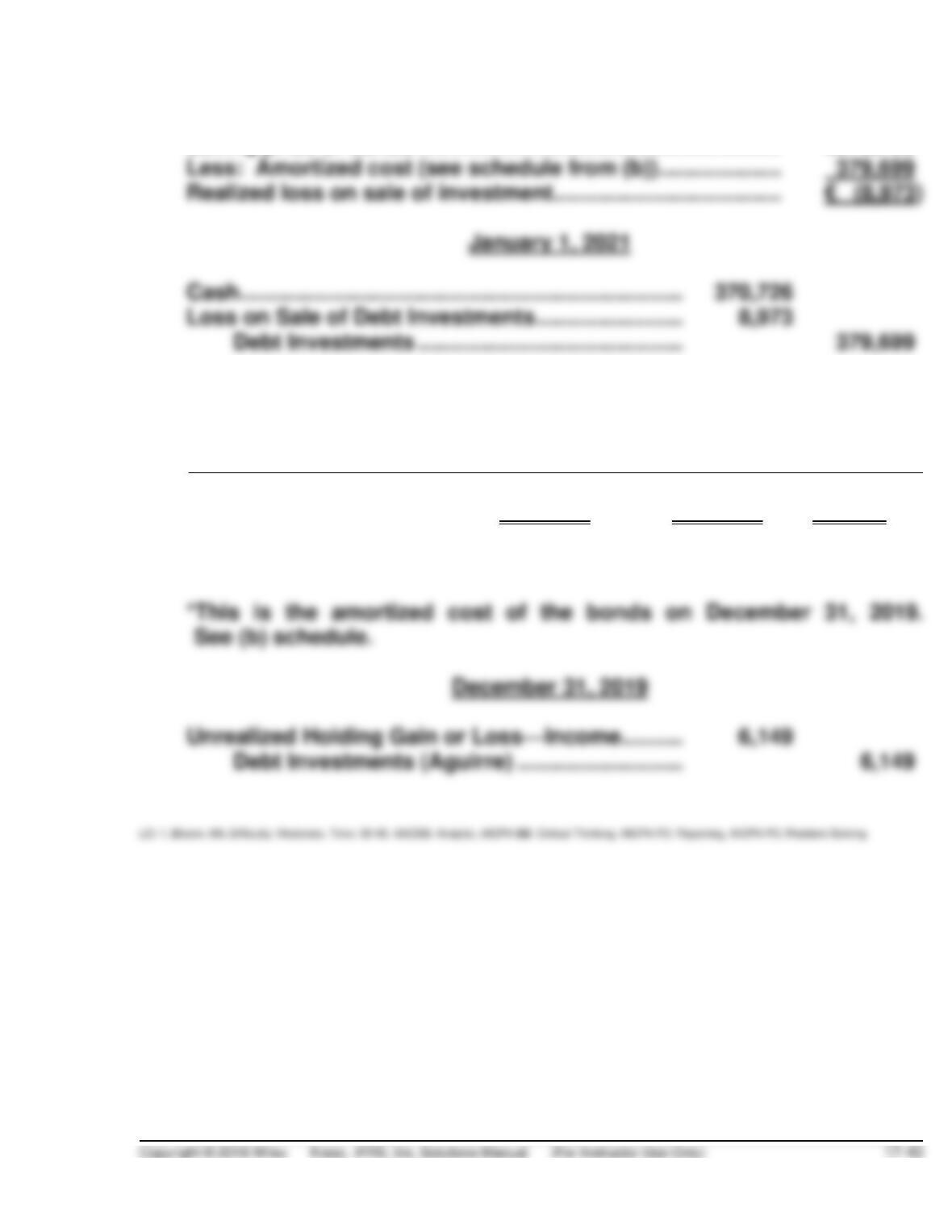

(d) January 1, 2021 sale entry:

Selling price of bonds ………………………………………………….. €370,726

(e) December 31, 2019 adjusting entry:

Securities

Amortized Cost

Fair Value

Unrealized

Gain (Loss)

Aguirre (total portfolio

value)

*

€374,149*

€368,000

€(6,149)

PROBLEM 17.3

(a) Equity Investments ………………………………………… 37,400

(b) December 31, 2019

Interest Receivable ………………………………………… 8,025

(c) December 31, 2019

Investment Portfolio

Investments

Cost

Fair Value

Unrealized

Gain (Loss)

Sharapova Company shares

$ 37,400

$ 31,800

$(5,600)

Fair value adjustment—Dr.

PROBLEM 17.3 (Continued)

Fair Value Adjustment ………………………………….. 15,700

Unrealized Holding Gain or Loss—

PROBLEM 17.4

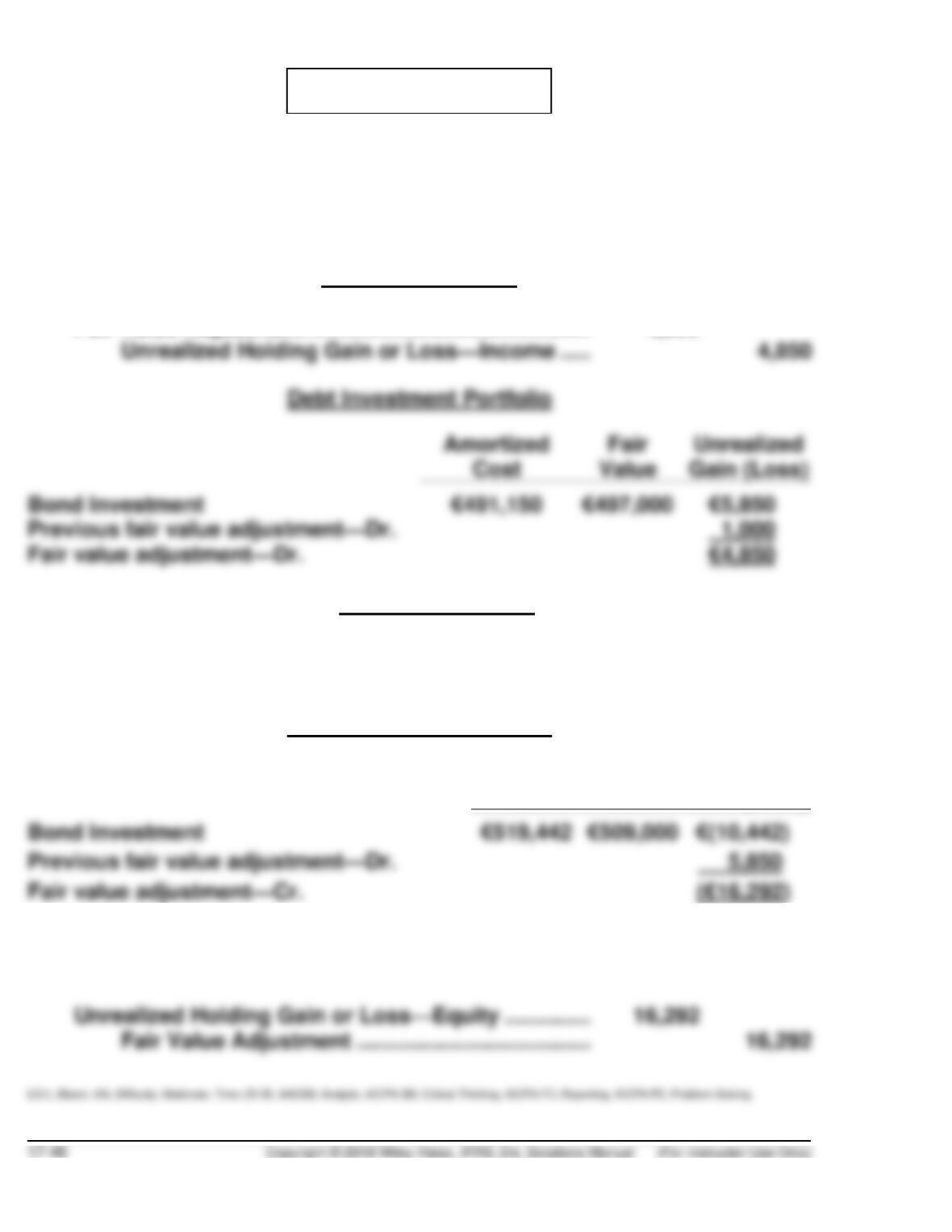

(a) The bonds were purchased at a discount. That is, they were purchased

at less than their face value because the bonds’ amortized cost

increased from €491,150 to €550,000.

(b) December 31, 2019

Fair Value Adjustment ………………………………………. 4,850

(c) December 31, 2020

Unrealized Holding Gain or Loss—Income …………. 16,292

Fair Value Adjustment ……………………………….. 16,292

Debt Investment Portfolio

Amortized

Cost

Fair

Value

Unrealized

Gain (Loss)

(d) The only difference is that the unrealized gain or loss is recorded in

other comprehensive income:

PROBLEM 17.5

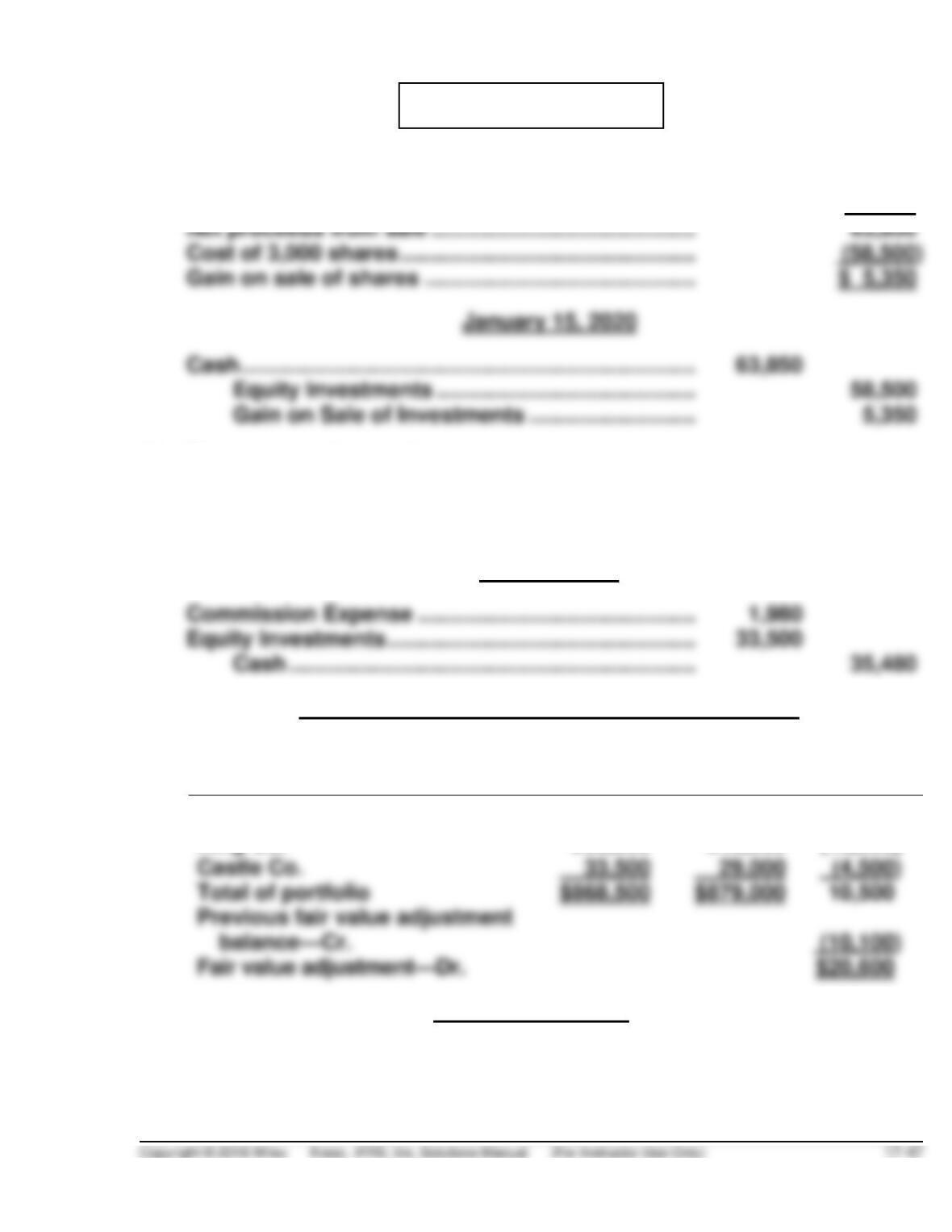

(a) Gross selling price of 3,000 shares at $22 …………. $66,000

Less: Commissions, taxes, and fees ……………….. 2,150

(b) The total purchase price is:

(1,000 X $33.50) = $33,500.

The purchase entry will be:

April 17, 2020

(c) Equity Investment Portfolio—December 31, 2020

Investments

Cost

Fair

Value

Unrealized

Gain (Loss)

Munter Ltd.

$580,000

$610,000

($30,000)

King Co.

255,000

240,000

(15,000)

Castle Co.

Fair value adjustment—Dr.

December 31, 2020

Fair Value Adjustment ……………………………………….. 20,600

Unrealized Holding Gain or Loss—Income …… 20,600

PROBLEM 17.5 (Continued)

(d) The unrealized holding gains or losses account should be reported on

(e) If the King Company preference shares are classified as non-trading,

the unrealized holding loss would be recorded in other comprehensive

PROBLEM 17.6

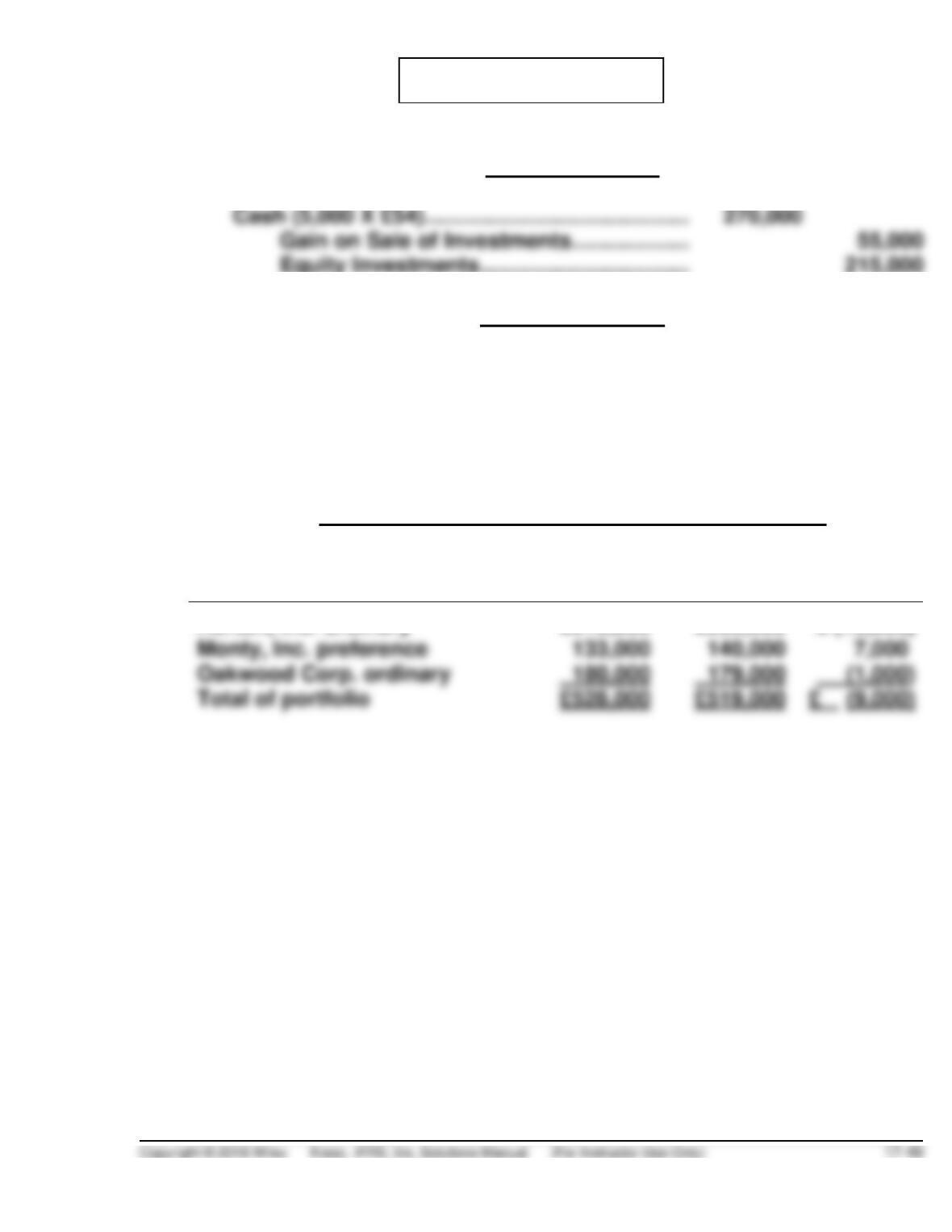

(a) (1) October 10, 2019

(2) November 2, 2019

Equity Investments (3,000 X £54.50) ………….. 163,500

Cash ………………………………………………… 163,500

(3) At September 30, 2019, McElroy had the following fair value

adjustment:

Equity Investment Portfolio—September 30, 2019

Investments

Cost

Fair

Value

Unrealized

Gain (Loss)

Horton, Inc. ordinary

£215,000

£200,000

(£ (15,000)

Monty, Inc. preference

PROBLEM 17.6 (Continued)

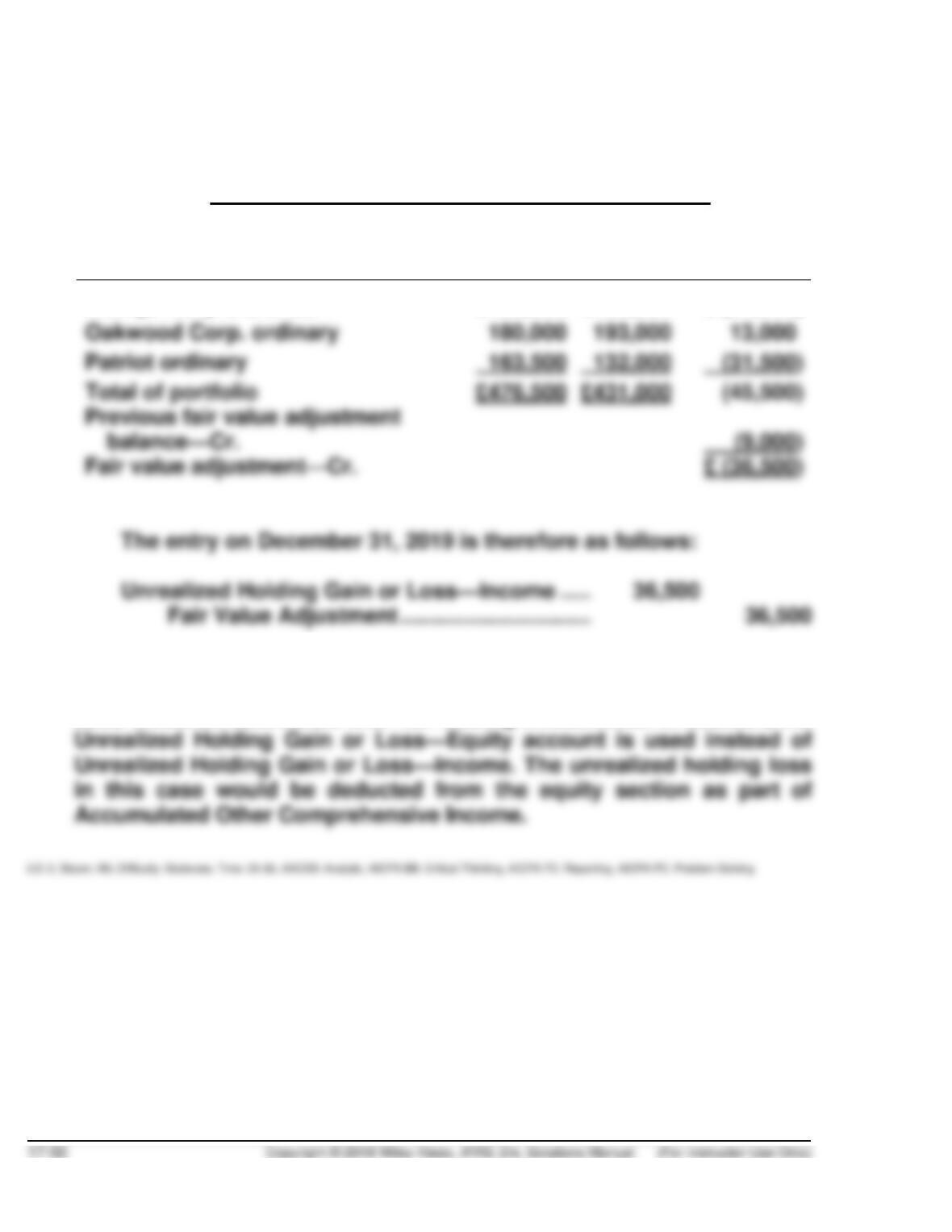

At December 31, 2019, McElroy had the following fair value

adjustment:

Equity Investment Portfolio—December 31, 2019

Investments

Cost

Fair

Value

Unrealized

Gain (Loss)

Monty, Inc. preference

£133,000

£106,000

(£ (27,000)

Oakwood Corp. ordinary

(b) The entries would be the same except that instead of debiting and

crediting accounts associated with trading investments, the accounts

used would be associated with non-trading investments. In addition, the

PROBLEM 17.7

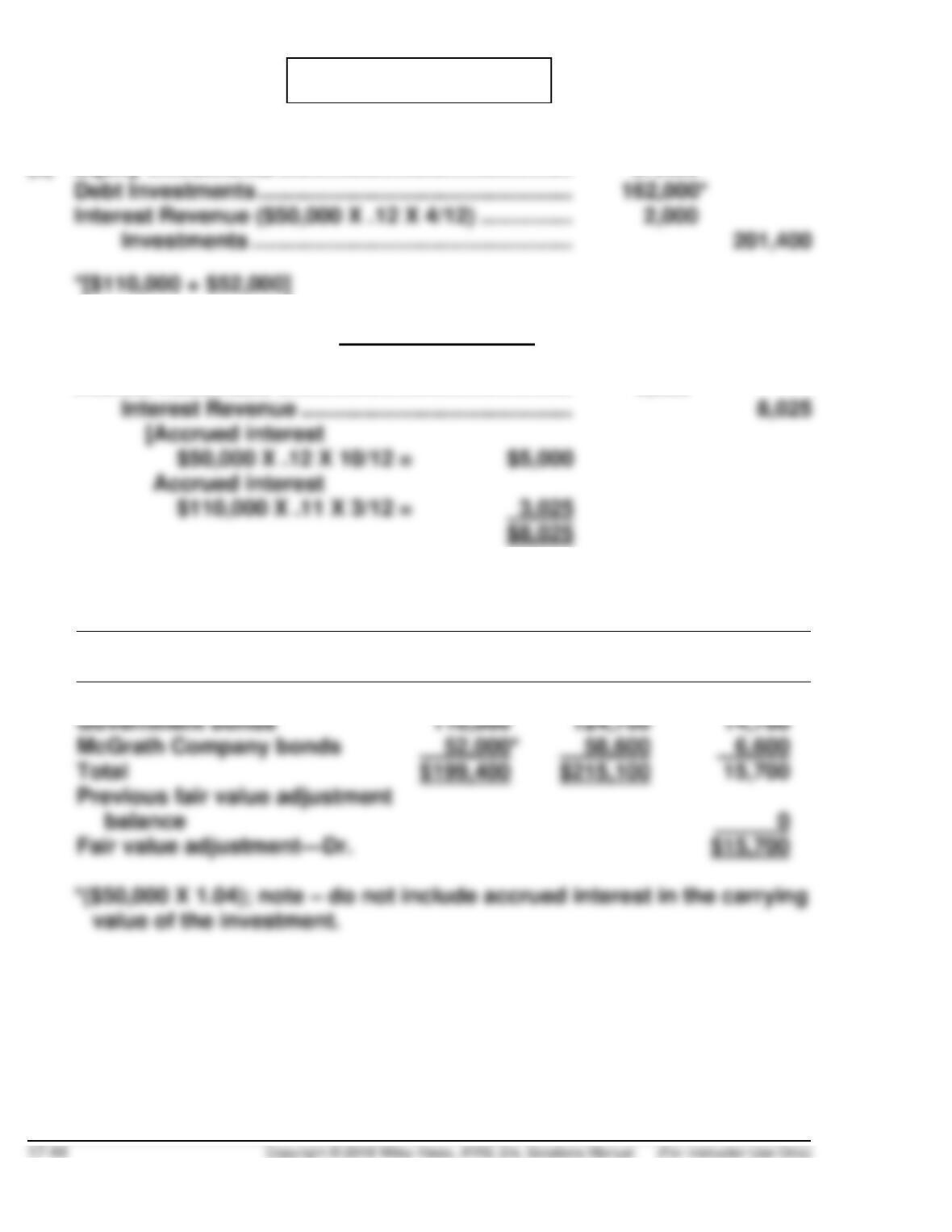

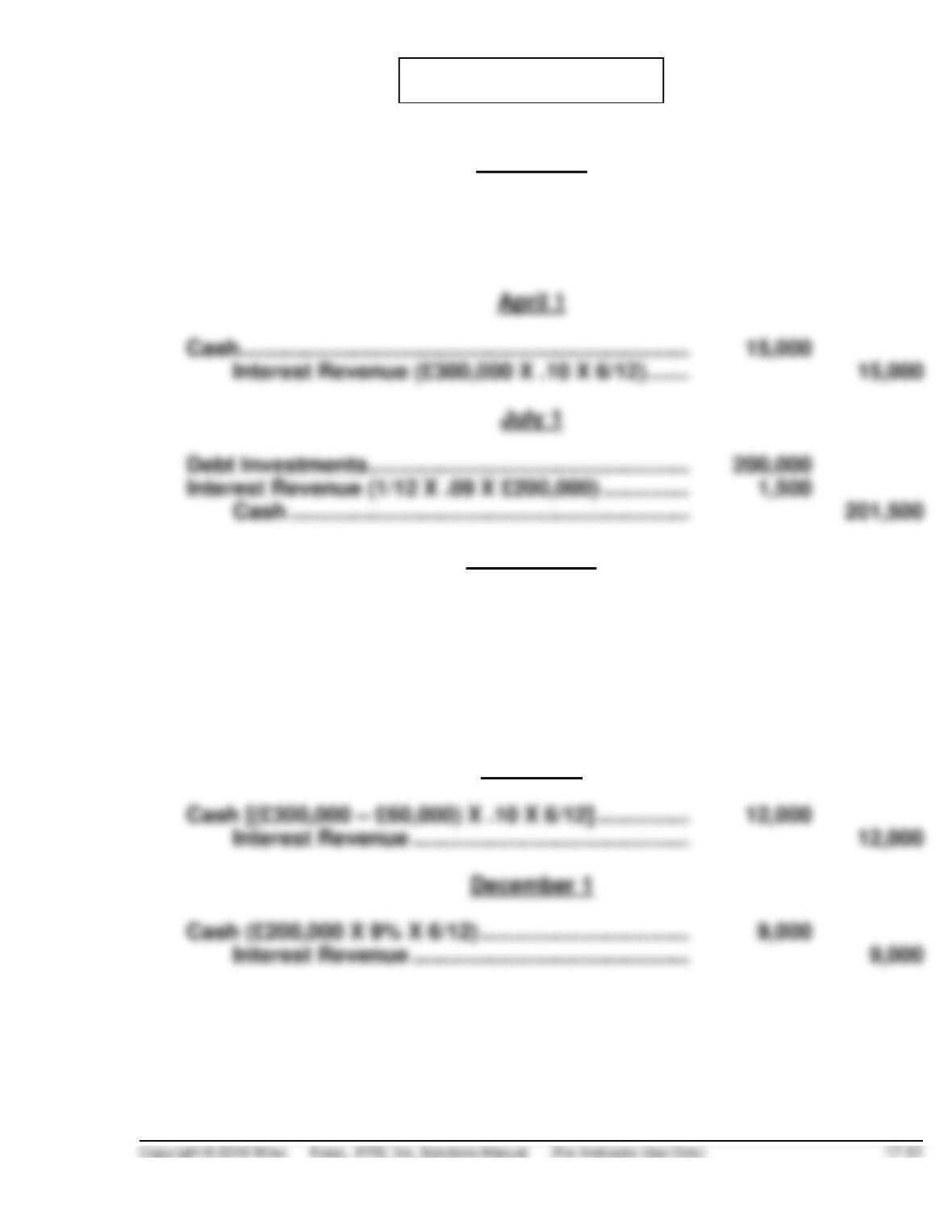

(a) February 1

Debt Investments ……………………………………………. 300,000

Interest Revenue (4/12 X .10 X £300,000) ………….. 10,000

Cash ……………………………………………………….. 310,000

September 1

Cash [(£60,000 X 99%) + (£60,000 X .10 X 5/12)] … 61,900

Loss on Sale of Investments

[(£60,000 x .99) – £60,000] ……………………………… 600

Debt Investments …………………………………….. 60,000

Interest Revenue

(5/12 X .10 X £60,000 = £2,500) ………………. 2,500

October 1

PROBLEM 17.7 (Continued)

December 31

Interest Receivable …………………………………………. 7,500

Interest Revenue ……………………………………… 7,500

December 31

Unrealized Holding Gain or Loss—Income ……….. 26,000

Fair Value Adjustment ……………………………… 26,000

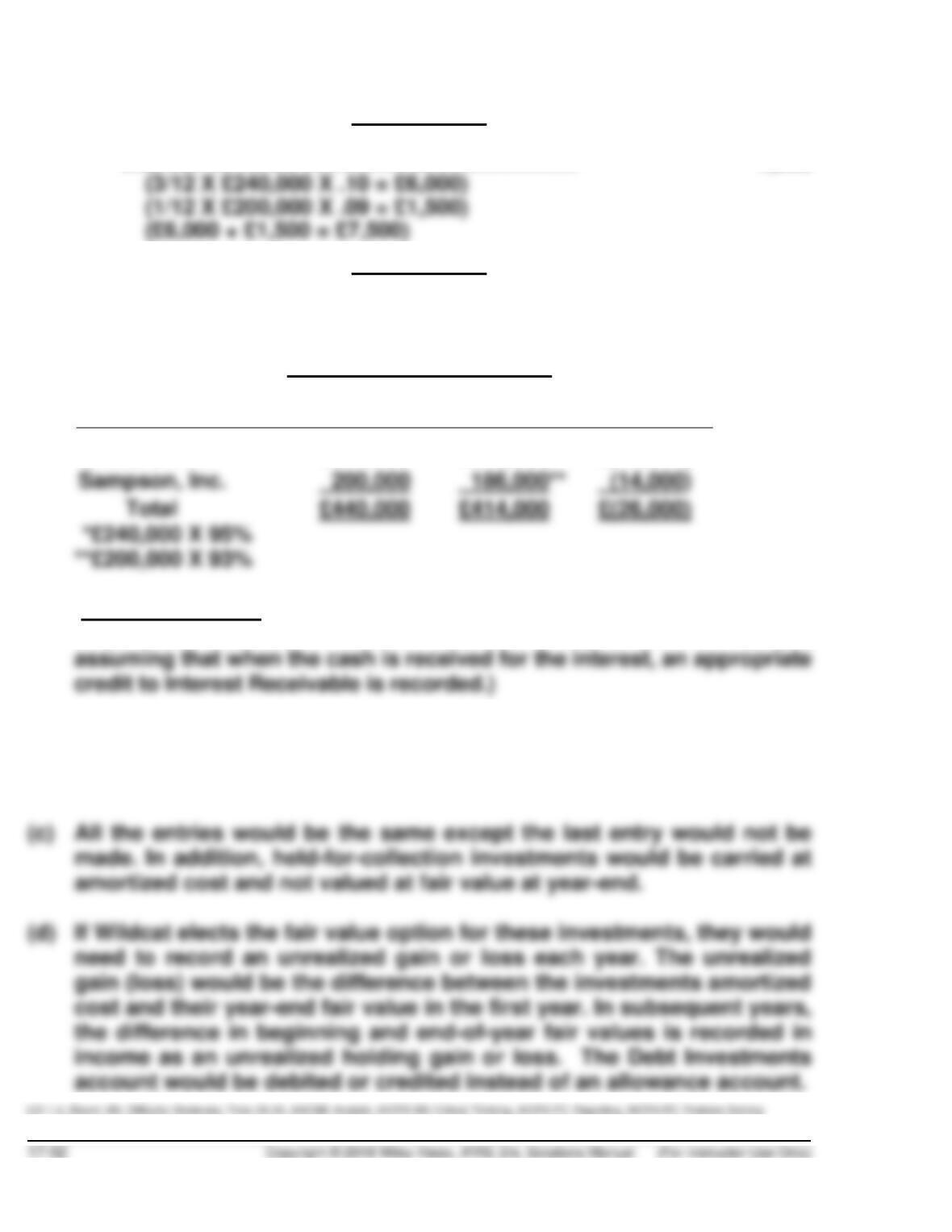

Debt Investment Portfolio

Investments

Cost

Fair Value

Unrealized

Gain (Loss)

Gibbons Co.

£240,000

£228,000*

£(12,000)

Sampson, Inc.

Total

£440,000

£414,000

£(26,000)

(Note to instructor: Some students may debit Interest Receivable at date

of purchase instead of Interest Revenue. This procedure is correct,

(b) If classified as HFCS, all entries are the same, except the unrealized

loss at December 31 will be recorded in other comprehensive income

(equity).

PROBLEM 17.8

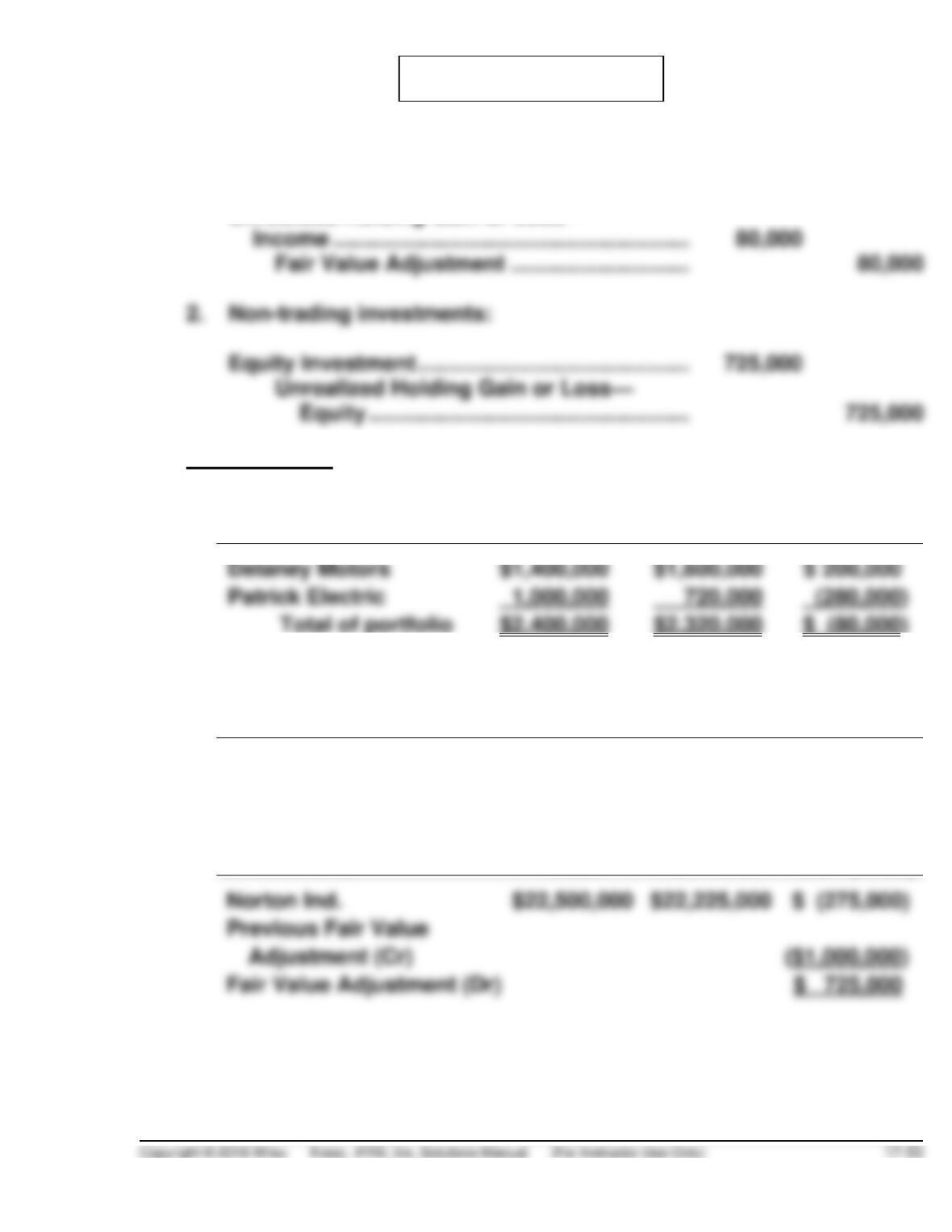

(a) 1. Trading investments:

Unrealized Holding Gain or Loss—

Computations:

1.

Investments

Cost

Fair Value

Unrealized

Gain (Loss)

Delaney Motors

Patrick Electric

Total of portfolio

2.

Computation of Unrealized Gain or Loss in 2018

Investments

Cost

Fair Value

Unrealized

Gain (Loss)

Norton Ind.

$22,500,000

$21,500,000

(($1,000,000)

Computation of Unrealized Gain or Loss in 2019

Investments

Cost

Fair Value

Unrealized

Gain (Loss)

$22,225,000

$ 725,000

PROBLEM 17.8 (Continued)

(b) The unrealized holding loss on the valuation of Brooks’ trading

investments is reported on the income statement. The loss would appear

The unrealized holding gain on the valuation of Brooks’ non-trading

investments is reported as other comprehensive income and as a

(c) Equity Investments ($500,000 X 25%) …………………… 125,000

Investment Revenue ……………………………………. 125,000

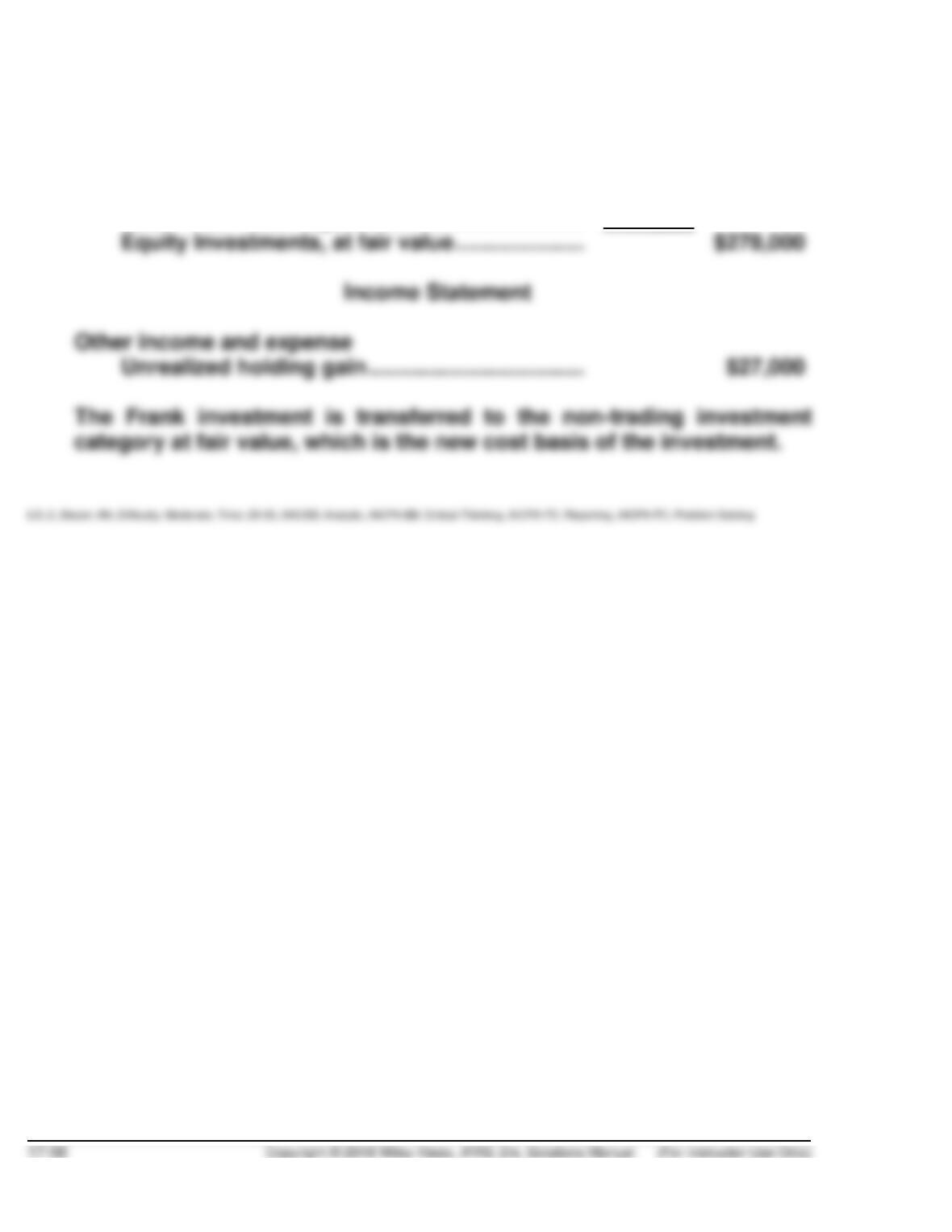

PROBLEM 17.9

(a) Equity Investment Portfolio

Investments

Cost

Fair Value

Unrealized

Gain (Loss)

Frank, Inc.

$ 22,000

$ 32,000

($(10,000)

Ellis Corp.

115,000

95,000

(20,000)

Mendota Company

Total of portfolio

Income Statement

Other income and expense

Unrealized holding loss ……………………… $38,000

(b) Equity Investment Portfolio

Investments

Cost

Fair Value

Unrealized

Gain (Loss)

Ellis Corp.

$115,000

$140,000

($ 25,000

Mendota Company

174,000*

138,000**

( (36,000)

Total of portfolio

$289,000

$278,000

PROBLEM 17.9 (Continued)

Statement of Financial Position—December 31, 2020

Investments:

Equity Investments, at cost ……………………….. $289,000

Less: Fair value adjustment ……………………… 11,000

PROBLEM 17.10

(a)

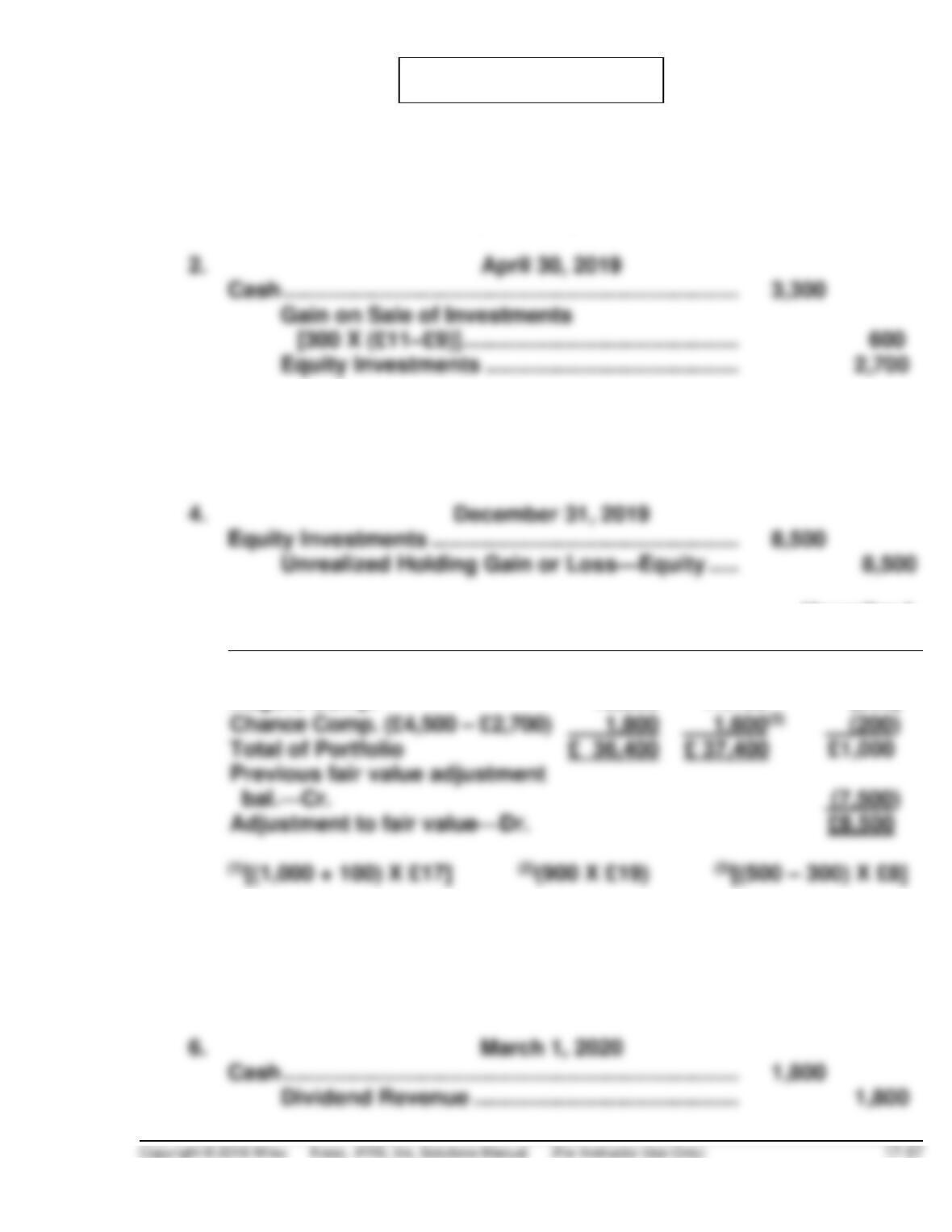

1. March 1, 2019

Cash ……………………………………………………………….. 1,800

Dividend Revenue (900 X £2) …………………….. 1,800

3. May 15, 2019

Equity Investments ………………………………………….. 1,600

Cash (100 X £16) ………………………………………. 1,600

Investments

Cost

Fair Value

Unrealized

Gain (Loss)

Evers Comp. (£15,000 + £1,600)

£ 16,600

£ 18,700(1)

£2,100

Rogers Comp.

18,000

17,100(2)

(900)

Chance Comp. (£4,500 – £2,700)

Total of Portfolio

Adjustment to fair value—Dr.

£8,500

5. February 1, 2020

Cash ……………………………………………………………….. 1,600

Loss on Sale of Investments …………………………….. 200

Equity Investments ……………………………………… 1,800

PROBLEM 17.10 (Continued)

7. December 21, 2020

8. December 31, 2020

Equity Investments ………………………………………… 4,200

Unrealized Holding Gain or Loss—Equity …. 4,200

Investments

Cost

Fair Value

Unrealized

Gain (Loss)

Evers Comp.

£16,600

£20,900(1)

£4,300

Rogers Comp.

900

Previous adjustments to fair

value —Dr.

(b)

Partial Statement of Financial

Position as of

December 31,

2019

December 31,

2020

Equity Investments, at fair value

Current Assets

(c) If the Evers investment was classified as trading, the unrealized

holding gain would not be reported as equity. Instead the unrealized

PROBLEM 17.11

(a) Statement of Financial Position

Equity Investments, at fair value …………………………………… €123,000

(b) Statement of Financial Position

Equity Investments, at fair value …………………………………… € 94,000

Income Statement

Other income and expense

(c) Statement of Financial Position

Equity Investments, at fair value ……………….. € 88,000

PROBLEM 17.11 (Continued)

Income Statement

Other income and expense

The entry made to record the sale of Lindsay Jones’ shares was:

Cash ……………………………………………………………… 39,900