*PROBLEM 11.13

(a) December 31, 2018

Land (HK$215,000 – HK$200,000) …………………. 15,000

Unrealized Gain on Revaluation—Land …. 15,000

(b)

Dec. 31, 2019

Dec. 31, 2020

Land

HK$185,000

HK$205,000

Impairment Loss

(c) December 31, 2019

Unrealized Gain on Revaluation—Land …………. 15,000

(d) January 15, 2021

Cash …………………………………………………………… 220,000

Land ……………………………………………………. 205,000

Gain on Disposal of Land……………………… 15,000

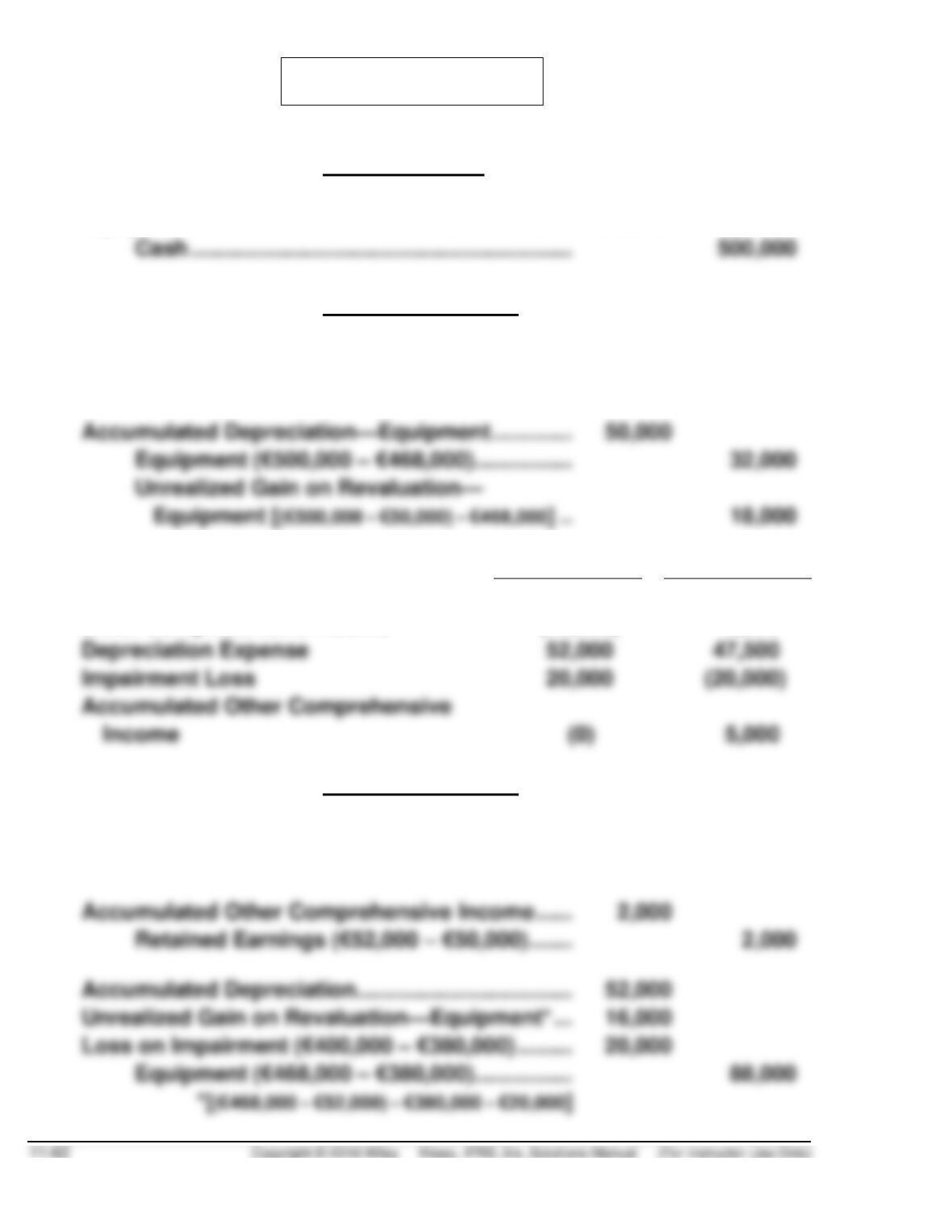

*PROBLEM 11.14

(a) January 2, 2019

Equipment ……………………………………………………. 500,000

December 31, 2019

Depreciation Expense (€500,000 ÷ 10) ……………. 50,000

Accumulated Depreciation—Equipment …… 50,000

(b)

Dec. 31, 2020

Dec. 31, 2021

Equipment

€380,000

€355,000

Other Comprehensive Income

(16,000)

2,500

Depreciation Expense

Impairment Loss

20,000

5,000

(c) December 31, 2020

Depreciation Expense (€468,000 ÷ 9) ……………… 52,000

Accumulated Depreciation—Equipment …. 52,000

*PROBLEM 11.14 (Continued)

(c) December 31, 2021

Depreciation Expense (€380,000 ÷ 8) ………………. 47,500

Accumulated Depreciation—Equipment ….. 47,500

(d) December 31, 2022

Cash …………………………………………………………….. 330,000

Loss on Disposal of Equipment ……………………… 25,000

Equipment …………………………………………….. 355,000

TIME AND PURPOSE OF CONCEPTS FOR ANALYSIS

CA 11.1 (Time 25–35 minutes)

Purpose—to provide the student with an understanding of the basic objective of depreciation accounting. In

CA 11.2 (Time 25–35 minutes)

Purpose—to provide the student with an understanding of a number of unstructured situations involving

depreciation accounting. The first situation considers whether depreciation should be recorded during a

CA 11.3 (Time 25–35 minutes)

Purpose—to provide the student with an understanding of the objectives of depreciation and the

theoretical basis for accelerated depreciation methods.

CA 11.4 (Time 20–25 minutes)

SOLUTIONS TO CONCEPTS FOR ANALYSIS

CA 11.1

(a) The purpose of depreciation is to distribute the cost (or other book value) of tangible plant assets, less

residual value, over their useful lives in a systematic and rational manner. Under IFRS, depreciation

(b) The proposed depreciation method is, of course, systematic. Whether it is rational in terms of cost

allocation depends on the facts of the case. It produces an increasing depreciation charge, which is

(c) (1) Depreciation charges neither recover nor create funds. Revenue-producing activities are the

sources of funds from operations: if revenues exceed out-of-pocket costs during a fiscal period,

funds are available to cover other than out-of-pocket costs; if revenues do not exceed out-of–

pocket costs, no funds are made available no matter how much, or little, depreciation is charged.

(2) Depreciation may affect funds in two ways. First, depreciation charges affect reported income

CA 11.1 (Continued)

Second, depreciation charges affect reported taxable income and hence affect directly the amount of

income taxes payable in the year of deduction.

Using the proposed method for tax purposes would reduce the total tax bill over the life of the assets

(1) if the tax rates were increased in future years or (2) if the business were doing poorly now but

If Hakodat is not profitable now, it would not benefit from higher deductions now and should consider

an increasing charge method for tax purposes, such as the one proposed. If Hakodat is quite

profitable now, the president should reconsider his proposal because it will delay the availability of

CA 11.2

Situation I. This position relates to the omission of a provision for depreciation during a strike. The same

question could be raised with respect to plant shut-downs for many reasons, such as for a lack of sales or

for seasonal business.

The method of depreciation used should be systematic and rational. The annual provision for depreciation

should represent a fair estimate of the cost expiration arising from wear and usage and also from

obsolescence. Each company should analyze its own facts and establish the best method under the

circumstances. If the company was employing a straight-line depreciation method, for example, it is

inappropriate to stop depreciating the plant asset during the strike.

CA 11.2 (Continued)

(b) In determining the depreciation method to be used for the machine, the objective should be to

allocate the cost of the machine over its useful life in a systematic and rational manner, so that costs

will be matched with the benefits expected to be obtained. In addition to demand, consideration

should be given to the items discussed below, their interrelationships, the relative importance of

each, and the degree of certainty with which each can be predicted:

The expected pattern of costs of repairs and maintenance should be considered. Costs which

vary with use of the machine may suggest the use of the units–of-production method. Costs

Another consideration is the expiration of the physical life of the machine. If the machine wears

out in relation to the passage of time, the straight-line method is indicated. Within this maximum

life, if the usage per period varies, the units-of-production method may be appropriate.

The machine may become obsolete because of technological innovation; it may someday be

more efficient to replace the machine even though it is far from worn out. If the probability is high

Situation III. Depreciation rates should be adjusted in order that the operating sawmills which are to be

replaced will be depreciated to their residual value by the time the new facility becomes available. The

step-up in the depreciation rates should be considered as a change in estimate and prior years’ financial

statements should not be adjusted.

The idle mill should be written off immediately as it appears to have no future service potential.

CA 11.3

To: Phil Perriman, Supervisor of Canning Room

From: Your name, Accountant

Date: January XX, 2019

Subject: Annual depreciation charge to the canning department

This memo addresses the questions you asked about the depreciation charge against your department.

Admittedly this charge of $625,000 [(100% ÷ 12) x 2 x $625,000 x 6 machines) is very high; however, it is

not intended to reflect the wear and tear which the machinery has undergone over the last year. Rather, it

is a portion of the machines’ cost which has been allocated to this period.

You also mentioned that using straight-line depreciation would result in a smaller charge than would

the current double-declining-balance method. This is true during the first years of the equipment’s life.

Straight-line depreciation expenses even amounts of depreciation for each canning machine’s twelve–

year life. Thus the straight-line charge for this and all subsequent years would be $47,500 per machine

for total annual depreciation of $285,000 {6 x [($625,500 – $55,000) ÷12]}.

CA 11.4

(a) The stakeholders are Beeler’s employees, including Prior, current and potential investors and

creditors, and upper-level management.

(b) The ethical issues are honesty and integrity in financial reporting, job security, and the external

users’ right to know the financial picture.

FINANCIAL REPORTING PROBLEM

(a) M&S classifies its property, plant and equipment under three descrip–

tions in its balance sheet: Property, Plant and Equipment.

(c) M&S depreciates property plant and equipment as follows:

• Freehold/leasehold buildings with a remaining lease term > 50 years −

Estimated remaining economic lives.

COMPARATIVE ANALYSIS CASE

(a) Property, plant, and equipment, net of accumulated depreciation:

Puma at 12/31/15 €232.6 million

(b) Puma and adidas depreciate property, plant, and equipment principally

by the straight-line method over the estimated useful lives of the assets.

Depreciation expense was reported by Puma and adidas as follows:

Puma

adidas

50.5 million

(c) (1) Asset turnover:

Puma

adidas