EXERCISE 12.12 (20–25 minutes)

Net assets of Terrell as reported

($575,000 – $350,000) ………………………………………….

$225,000

Adjustments to fair value

Increase in land value ……………………………………

Decrease in equipment value …………………………

Net assets of Terrell at fair value …………………………...

Selling price ………………………………………………………….

Amount of goodwill to be recorded ………………………..

The journal entry to record this transaction is as follows:

Building ………………………………………………………………..

200,000

Equipment ($175,000 – $5,000) ……………………………….

170,000

Copyright ……………………………………………………………..

120,000

Cash …………………………………………………………………….

100,000

Goodwill ……………………………………………………………….

110,000

Accounts Payable …………………………………………

Long-term Notes Payable ………………………………

Cash …………………………………………………………….

EXERCISE 12.13 (10–15 minutes)

(a)

Buildings ……………………………………………………….

75,000

Equipment ……………………………………………………….

70,000

Trademarks ……………………………………………………….

15,000

Land ………………………………………………………………………

80,000

Inventory ……………………………………………………….

Receivables ……………………………………………………….

90,000

Cash ………………………………………………………………………

50,000

Accounts Payable …………………………………………..

Notes Payable ………………………………………………..

Cash ……………………………………………………….

EXERCISE 12.13 (Continued)

(b)

Trademark Amortization Expense …………………………..

1,500

Trademarks [(€15,000 – €3,000)] X 1/4 X 6/12] ……….

EXERCISE 12.14 (15–20 minutes)

(a)

December 31, 2019

Loss on Impairment ………………………………………………..

900,000*

Copyrights ……………………………………………………..

900,000

*Carrying amount …………………

Recoverable amount ……………

(b)

Copyright Amortization Expense …………………………..

340,000*

Copyrights ……………………………………………………..

340,000

EXERCISE 12.15 (15–20 minutes)

(a)

December 31, 2019

Loss on Impairment …………………………

25,000,000*

Goodwill ………………………………….

25,000,000

*HK$360,000,000 – HK$335,000

EXERCISE 12.15 (Continued)

EXERCISE 12.16 (15–20 minutes)

(a) In accordance with IFRS, the €325,000 is a research and development

(b)

Patents ……………………………………………………….

36,000

Research and Development Expense ……………………….

74,000

Cash, Accts. Payable, etc. …………………………..

110,000

(To record research and

development costs)

Patents ……………………………………………………….

24,000

Cash, Accts. Payable, etc. …………………………..

(To record legal and administrative

costs incurred to obtain patent

#472-1001–84)

Patent Amortization Expense …………………………..

12,000

Patents ……………………………………………………….

[To record one year’s amortization

expense (€60,000* ÷ 5 = €12,000)]

EXERCISE 12.16 (Continued)

(c)

Patents ……………………………………………………….

47,200

Cash, Accts. Payable, etc. …………………………..

47,200

(To record legal cost of successfully

defending patent)

The cost of defending the patent is capitalized because the defense

was successful and because it extended the useful life of the patent.

Patent Amortization Expense …………………………..

11,900

Patents ……………………………………………………….

11,900

(To record one year’s amortization

Expense:

(d) Additional engineering and consulting costs required to advance the

design of a product to the manufacturing stage are R&D costs. As

LO: 5, Bloom: AP, Difficulty: Moderate, Time: 15-20, AACSB: Analytic, AICPA BB: None, AICPA FC: Reporting, AICPA PC: None

EXERCISE 12.17 (10–15 minutes)

Depreciation of equipment acquired that will have alternate

uses in future R&D projects over

the next 5 years ($330,000 ÷ 5) ……………………………………………

$ 66,000

Materials consumed in R&D projects …………………………………….

Consulting fees paid to outsiders for R&D projects ………………..

Personnel costs of persons involved in R&D projects …………….

Indirect costs reasonably allocable to R&D projects

50,000

Total to be expensed in 2019 for research and

TIME AND PURPOSE OF PROBLEMS

Problem 12.1 (Time 15–20 minutes)

Purpose—to provide the student with an opportunity to appropriately reclassify amounts charged to a

Problem 12.2 (Time 20–30 minutes)

Purpose—to provide the student with an opportunity to compute the carrying value of a patent at three

Problem 12.3 (Time 20–30 minutes)

Problem 12.4 (Time 15–20 minutes)

Purpose—to provide the student with an opportunity to determine income statement and statement of

Problem 12.5 (Time 25–30 minutes)

Purpose—to provide the student with an opportunity to determine the amount of goodwill in a business

combination and to determine the goodwill impairment.

Problem 12.6 (Time 30–35 minutes)

SOLUTIONS TO PROBLEMS

PROBLEM 12.1

Franchises ……………………………………………………………

48,000

Prepaid Rent …………………………………………………………

24,000

Retained Earnings (Organization Costs of

€6,000 (€5,000 + €1,000) in 2014) ………………………….

6,000

Retained Earnings (€16,000 – €6,000) ……………………..

10,000

Patents (€84,000 + €12,650 + €45,000) …………………….

(€75,000 + €160,000 – €45,000) …………………………….

Goodwill ……………………………………………………………….

Intangible Assets ………………………………………….

Franchise Amortization Expense-2019 (€48,000 ÷ 8) ..

6,000

Retained Earnings- 2018 (€48,000 ÷ 8 X 6/12) …………..

3,000

Franchises ……………………………………………………

9,000

Rent Expense (€24,000 ÷ 2) ……………………………………

12,000

Retained Earnings (€24,000 ÷ 2 X 3/12) ……………………

3,000

Prepaid Rent …………………………………………………

15,000

Patent Amortization Expense …………………………………

10,777

Patents (€84,000 ÷ 10) + (€12,650 X 7/115) +

(€45,000 X 4/112) ………………………………………..

10,777

PROBLEM 12.2

(a)

Costs to obtain patent Jan. 2013 ………………

HK$59,500

2013 amortization (HK$59,500 ÷ 17) …………..

(3,500)

(b)

1/1/14 carrying value of patent …………………………..

HK$ 56,000

2014 amortization (HK$59,500 ÷ 17) ………………………….

HK$3,500

2015 amortization ……………………………………………………

3,500

(7,000)

49,000

Legal fees to defend patent 12/15 …………………………..

42,000

Carrying value, 12/31/15 ………………………………………….

91,000

Capitalized development costs 4/16 …………………………

49,000

(c)

1/1/18 carrying value …………………………..…………………..

HK$120,000

2018 amortization (HK$120,000 ÷ 5) ………………………….

HK$24,000

2019 amortization ……………………………………………………

24,000

2020 amortization ……………………………………………………

PROBLEM 12.3

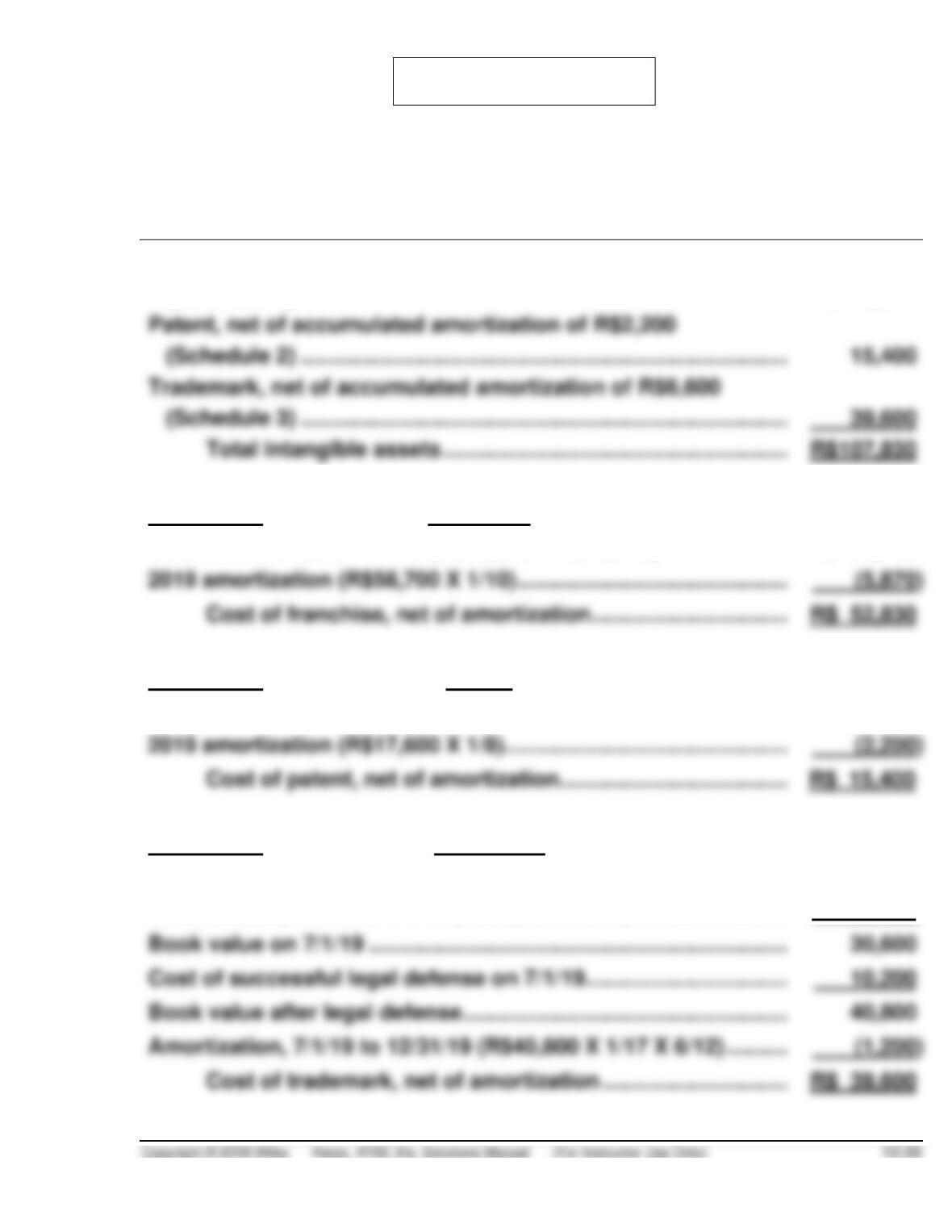

(a)

SANDRO SA

Intangible Assets

December 31, 2019

Franchise, net of accumulated amortization of R$5,870

(Schedule 1) …………………………………………………………………….

R$ 52,830

Patent, net of accumulated amortization of R$2,200

(Schedule 2) …………………………………………………………………….

Trademark, net of accumulated amortization of R$6,600

(Schedule 3) …………………………………………………………………….

39,600

Total intangible assets ………………………………………………..

R$107,830

Schedule 1 Franchise

Cost of franchise on 1/1/19 (R$15,000 + R$43,700) ………………..

R$ 58,700

Cost of franchise, net of amortization …………………………..

R$ 52,830

Schedule 2 Patent

Cost of securing patent on 1/2/19 …………………………………………

R$ 17,600

Cost of patent, net of amortization ……………………………….

Schedule 3 Trademark

Cost of trademark on 7/1/16 …………………………………………………

R$ 36,000

Amortization, 7/1/16 to 7/1/19 (R$36,000 X 3/20) …………………….

(5,400)

Book value on 7/1/19 …………………………………………………………..

Cost of successful legal defense on 7/1/19…………………………...

Book value after legal defense……………………………………………..

Amortization, 7/1/19 to 12/31/19 (R$40,800 X 1/17 X 6/12) ……….

PROBLEM 12.3 (Continued)

(b)

SANDRO SA

Expenses Resulting from Selected Intangible Assets Transactions

For the Year Ended December 31, 2019

Interest expense (R$43,700 X 14%) ………………………………………

$ 6,118

Franchise amortization (Schedule 1) ……………………………………

Franchise fee (R$900,000 X 5%) …………………………………………..

45,000

Patent amortization (Schedule 2) …………………………………………

Trademark amortization (Schedule 4)…………………………………..

Total intangible assets ……………………………………………….

Note: The R$65,000 of research and development costs incurred in

developing the patent would have been expensed prior to 2019.

Schedule 4 Trademark Amortization

Amortization, 1/1/19 to 6/30/19 (R$36,000 X 1/20 X 6/12) …………

$ 900

Amortization, 7/1/19 to 12/31/19 (R$40,800 X 1/17 X 6/12) ……….

Total trademark amortization ……………………………………….

$2,100

PROBLEM 12.4

(a) Income statement items and amounts for the year ended December 31,

2019:

Research and development expenses* ……………………..

$148,000

Amortization of patent ($88,000 ÷ 10 years) ……………….

8,800

*The research and development expenses could be listed by the

($320,000 ÷ 20 years) …………………………..………………..

Salaries and employee benefits ($195,000 – $90,000) …

Other expenses ($77,000 – $50,000) ………………………….

(b) Statement of financial position items and amounts as of December 31,

2019:

Land ……………………………………………………………………….

$ 60,000

Building (net of accumulated depreciation

of $16,000) ……………………………………………………………

304,000

Patent (net of amortization of $15,400)* …………………….

72,600

Capitalized development costs ($90,000 + $50,000) ……

140,000

PROBLEM 12.5

(a) Goodwill = Excess of the cost of the division over the fair value of the

net identifiable assets:

(c) Computation of impairment:

Goodwill impairment = Recoverable amount of division less the carrying

Carrying value of division ………………………..

(d) Loss on Impairment …………………………………

$50,000

Goodwill …………………………………………..

50,000

Copyright © 2018 Wiley Kieso, IFRS, 3/e, Solutions Manual (For Instructor Use Only) 12–33

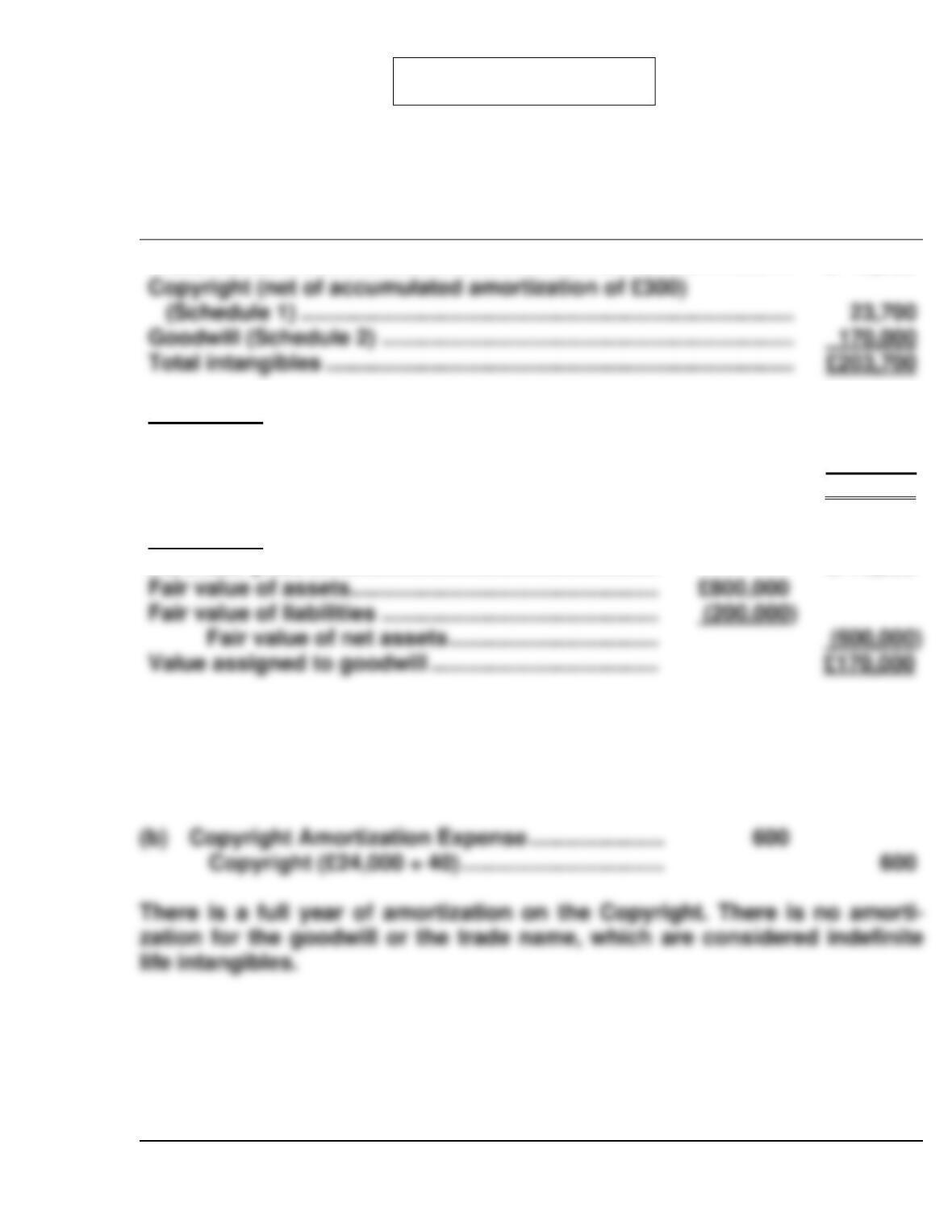

PROBLEM 12.6

(a)

MONTANA MATT’S GOLF LTD.

Intangibles Section of Statement of Financial Position

December 31, 2018

Trade name ………………………………………………………………………….

£ 10,000

Schedule 1 Computation of Value of Old Master Copyright

Cost of copyright at date of purchase …………………………..……….

£ 24,000

Amortization of Copyright for 2018 [(£24,000 ÷ 40) X 1/2 year] ……

(300)

Cost of copyright at December 31 …………………………………

£ 23,700

Schedule 2 Goodwill Measurement

Purchase price …………………………………………………

£770,000

Fair value of assets …………………………………………..

Fair value of liabilities ………………………………………

Fair value of net assets …………………………….

Value assigned to goodwill ……………………………….

Amortization expense for 2018 is £300 (see Schedule 1). There is no amor–

tization for the goodwill or the trade name, both of which are considered

indefinite life intangible assets.

Copyright (£24,000 ÷ 40) ……………………………..

Goodwill (Schedule 2) ………………………………………………………….

Total intangibles ………………………………………………………………….

£203,700

PROBLEM 12.6 (Continued)

MONTANA MATT’S GOLF LTD.

Intangibles Section of Statement of Financial Position

December 31, 2019

Trade name …………………………………………………………………………..

£ 10,000

Goodwill ……………………………………………………………………………….

Total intangibles……………………………………………………………………

Schedule 1 Computation of Value of Old Master Copyright

Cost of Copyright at date of purchase ……………………………………

£ 24,000

Cost of copyright at December 31 ………………………………….

£ 23,100

(c) Loss on Impairment ……………………………………………

87,000

Goodwill ………………………………………………………….

80,000*

Trade name (£10,000 – £3,000) ………………………….

7,000

Carrying value of the reporting unit …………… (500,000)

Impairment ………………………………………………. £ 80,000

*Recoverable amount of Old Master

TIME AND PURPOSE OF CONCEPTS FOR ANALYSIS

CA 12.1 (Time 15–20 minutes)

Purpose—to provide the student with an opportunity to determine which development costs are expensed

and which are capitalized. The student is required to discuss how the accounting for development costs

impacts a company’s income statement and statement of financial position. Finally, the student must

identify the criteria for determining “economic viability”.

CA 12.2 (Time 20–25 minutes)

Purpose—to provide the student with an opportunity to determine the proper classification of certain

CA 12.3 (Time 25–30 minutes)

Purpose—to present an opportunity for the student to discuss accounting for patents from a theoretical

CA 12.4 (Time 25–30 minutes)

Purpose—to provide the student with an opportunity to discuss the theoretical support for and practical

CA 12.5 (Time 20–25 minutes)

Purpose—to provide the student with an opportunity to examine the ethical issues related to expensing

research and development costs.

SOLUTIONS TO CONCEPTS FOR ANALYSIS

CA 12.1

(a) Research and Development Costs

Research and Development

Expense

Capitalized

Patent

Dogwood incurred legal and processing fees

to file and record a patent for the

technology ………………………………………………. €10,000

As indicated, Dogwood records as Research and Development Expense all Research and

Development costs incurred in the project prior to meeting the economic viability criteria (€57,000).

(b) By capitalizing the €10,000 legal fees and the €45,000 final development costs, Dogwood’s current

period income and intangible assets are higher. In future periods, Dogwood’s income and intangible

assets will decrease by the amount of amortization recorded on the capitalized costs (€55,000).

CA 12.2

Interest on mortgage bonds. An amount equal to the interest cost incurred in 2018 ($720,000) is a

cost which can be associated with the normal construction period and can be regarded as a normal

element of the cost of the physical assets of the shopping center because the construction period would

have ended at the end of the year if the tornado had not occurred. The decision to use debt capital to

In lieu of treating interest during construction as an element of the cost of the physical assets, it can be

argued that it represents an element of the general cost of bringing the business to the point of revenue

production and should therefore be treated as an organization expense. This view regards interest