PROBLEM 15.12 (Continued)

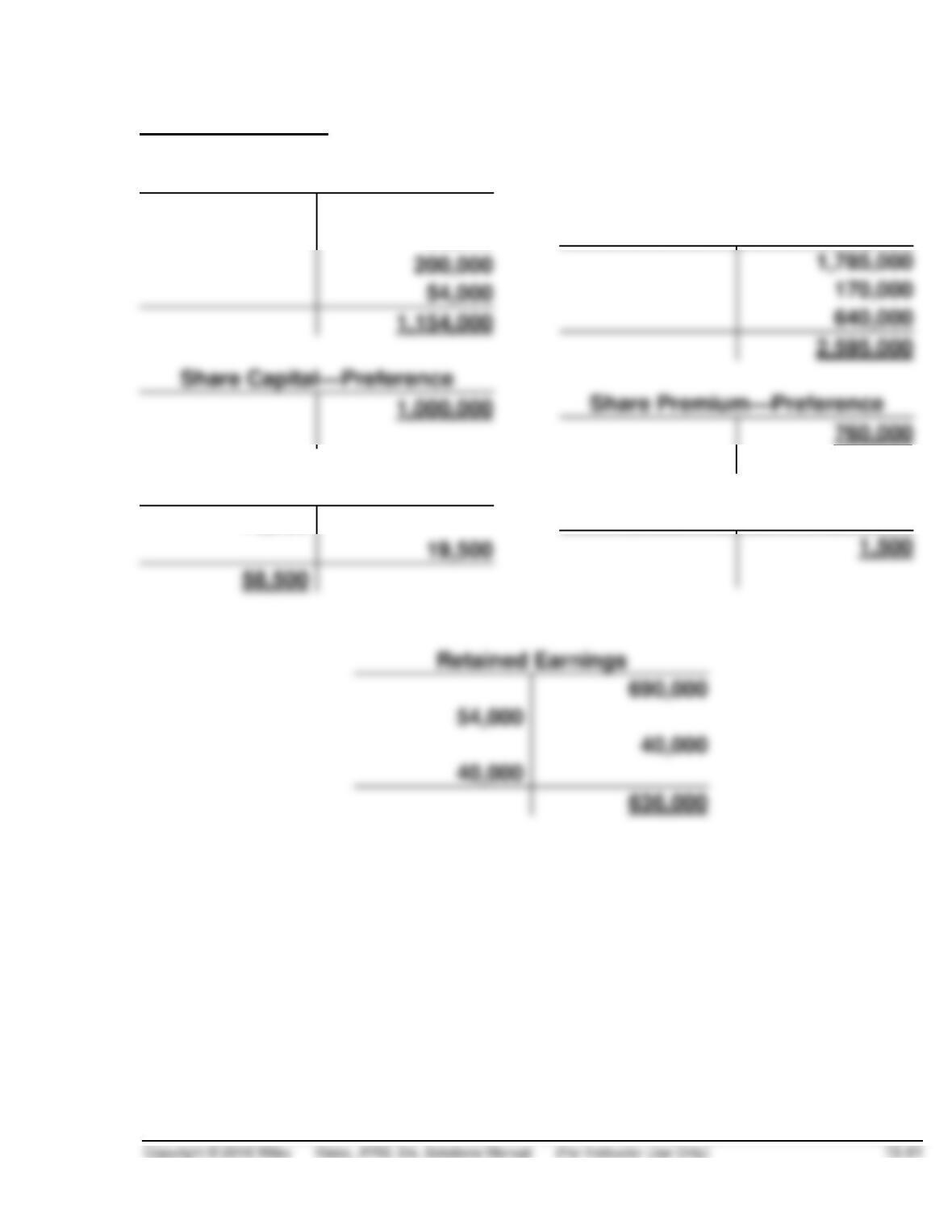

Account Balances

Share Capital—Ordinary

850,000

50,000

200,000

54,000

1,154,000

Share Capital—Preference

1,000,000

1,785,000

170,000

640,000

2,595,000

760,000

Treasury Shares

78,000

19,500

58,500

1,500

690,000

54,000

40,000

40,000

Share Premium—Ordinary

Share Premium—T.S.

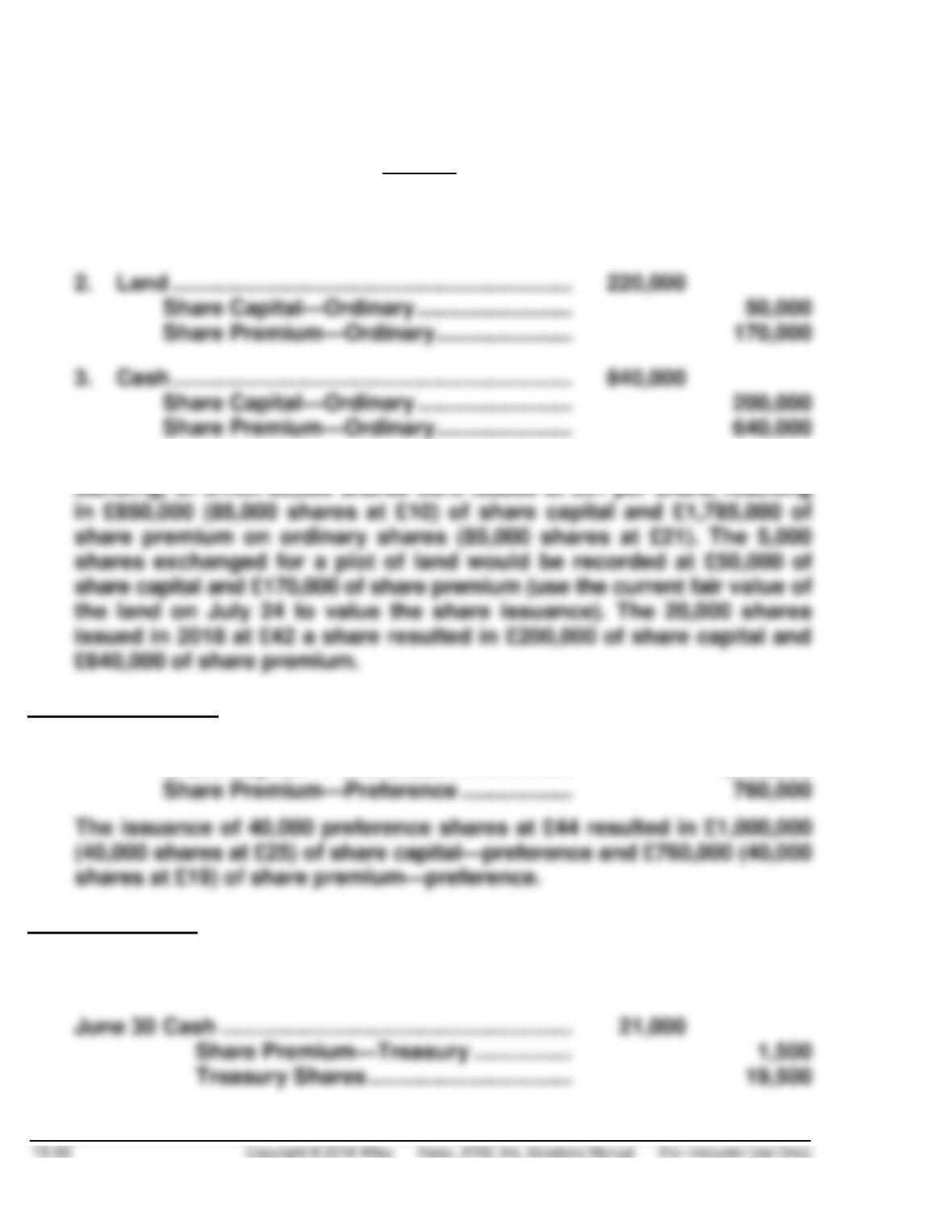

Note that the Penzi PLC is authorized to issue 300,000 shares of

£10 par value ordinary shares and 100,000 shares of £25 par value,

cumulative and non-participating preference shares.

PROBLEM 15.12 (Continued)

Entries supporting the balances.

Entries

1. Cash ……………………………………………………….. 2,635,000

Share Capital—Ordinary ……………………. 850,000

Share Premium—Ordinary …………………. 1,785,000

At the beginning of the year, Penzi had 110,000 ordinary shares out–

Preference Shares

Cash ……………………………………………………….. 1,760,000

Share Capital—Preference …………………. 1,000,000

Treasury Shares

Nov. 30 Treasury Shares ……………………………….. 78,000

Cash ……………………………………………. 78,000

PROBLEM 15.12 (Continued)

The 2,000 treasury shares purchased resulted in a debit balance of

treasury shares of £78,000. Later, 500 shares were sold at £21,000,

Share Dividend

Dec. 15 Retained Earnings …………………………….. 54,000

Share Capital—Ordinary ……………….. 54,000*

*Shares outstanding, beginning of year: 110,000

Retained Earnings

The cash dividends only affect the retained earnings. Note that the

preference shares are in arrears for the dividends that should have

TIME AND PURPOSE OF CONCEPTS FOR ANALYSIS

CA 15.1 (Time 10–20 minutes)

Purpose—to provide the student with some familiarity with the applications of the ordinary share

CA 15.2 (Time 15–20 minutes)

Purpose—to provide the student with an opportunity to discuss the bases for recording the issuance of

shares in exchange for non-monetary assets.

CA 15.3 (Time 25–30 minutes)

Purpose—to provide a five-part theory case on equity based on the IASB conceptual framework. It

CA 15.4 (Time 25–30 minutes)

Purpose—to provide the student with an understanding of the conceptual framework which underlies

CA 15.5 (Time 15–20 minutes)

Purpose—to provide the student with an understanding of the theoretical concepts and implications that

CA 15.6 (Time 20–25 minutes)

Purpose—to provide the student with a situation containing a cash dividend declaration, a share

dividend, and a reacquisition and reissuance of shares requiring the student to explain the accounting

treatment.

CA 15.7 (Time 10–15 minutes)

Purpose—to provide an opportunity for the student to consider and discuss the ethical issues involved

SOLUTIONS TO CONCEPTS FOR ANALYSIS

CA 15.1

(a) To share proportionately in any new issues of shares of the same class (the preemptive right).

(b) Derek Wallace bought an additional £100,000 par value shares. His original ownership was

(c) No information is given with respect to the fair value of the shares. In this situation, an estimate

for fair value could be developed based on market transactions involving comparable assets.

Otherwise, discounted expected cash flows could be used to approximate fair value. In this

CA 15.2

(a) The general rule to be applied when shares are issued for services or property other than cash is

that companies should record the shares issued at the fair value of the goods or services

received, unless that fair value cannot be measured reliably. If the fair value of the goods or

(b) If the fair value of the land can be measured reliably, it is used as a basis for recording the

exchange. The fair value could be determined by observing the cash sales price of similar pieces

of property or through independent appraisals.

(c) If the fair value of the land cannot be measured reliably, but the fair value of the shares issued is

determinable, the fair value of the shares is used as a basis for recording the exchange. If the

CA 15.3

(a) Equity, or net assets, is the residual interest in the assets of the entity after deducting all its

liabilities; in other words, equity equals assets less liabilities. Assets are resources controlled by

the entity as the result of past events and from which future economic benefits are expected to

(d) Dividends generally initially cause an increase in liabilities but eventually cause a decrease in

assets in addition to the decrease in equity. The purchase of treasury shares causes a decrease

in assets in addition to the decrease in equity.

CA 15.4

(a) A share dividend is the issuance by a corporation of its own shares to its shareholders on a

(1) From the legal standpoint a share split is distinguished from a share dividend in that a split

results in an increase in the number of shares outstanding and a corresponding decrease in

(2) The major distinction is that a share dividend requires a journal entry to decrease retained

earnings and increase paid-in capital, while there is no entry for a share split. Also, from the

accounting standpoint the distinction between a share dividend and a share split is

(b) The usual reason for issuing a share dividend is to give the shareholders something on a

dividend date and yet conserve working capital.

A share dividend that is charged to retained earnings reduces the total accumulated earnings,

CA 15.4 (Continued)

A share dividend also may be issued for the purpose of obtaining a wider distribution of the

shares. Although this is the main consideration in a share split, it may be a secondary

CA 15.5

Instructors who assign this case may wish to assign students additional outside material on the

(a) The case against treating an ordinary share dividend as income is supported by a majority of

accounting authorities. It is based upon “entity” and “proprietary” interpretations.

If the corporation is considered an entity separate from shareholders, the income of the corpora–

tion is corporate income and not income to shareholders, although the equity of the shareholders

(b) The case against issuing share dividends on treasury shares rests principally upon the argument

that shares reacquired by the corporation is a “reduction of equity” through the payment of cash

to reduce the number of outstanding shares. According to this view, the corporation cannot

obtain a proprietary interest in itself when it reacquires its own shares. The retained earnings are

CA 15.6

(a) Mask Company should account for the purchase of the treasury shares on August 15, 2019, by

debiting Treasury Shares and crediting Cash for the cost of the purchase (1,000 shares X €18

per share). Mask should account for the sale of the treasury shares on September 14, 2019, by

CA 15.6 (Continued)

(b) Mask should account for the share dividend by debiting Retained Earnings for €10 per share (the

par value of the shares in October 2019, the date of the share dividend) multiplied by the

(c) Mask should account for the cash dividend on December 20, 2019, the declaration date, by

CA 15.7

(a) The stakeholders are the dissident shareholders, the other shareholders, potential investors,

creditors, and Kenseth.

(b) The ethical issues are honesty, job security, and personal responsibility to others. That is, by

using her inside information and her authority to do the buy-back, she can benefit herself at the

FINANCIAL REPORTING PROBLEM

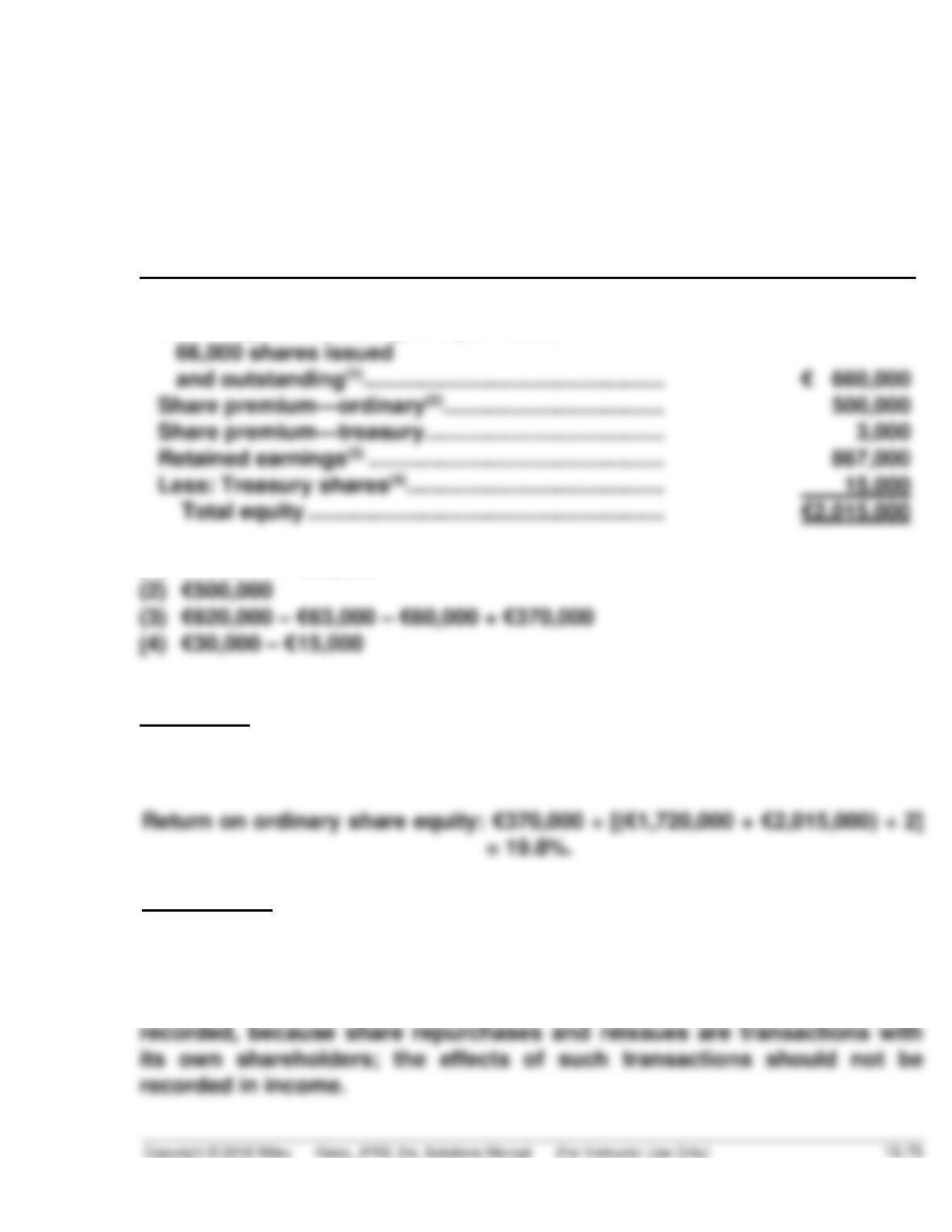

(a) M&S does not have any preference shares.

(d) At fiscal year-end 2016 and 2015, M&S had 1,622.96 million and

1,647.81 million ordinary shares outstanding, respectively.

There is no indication of treasury shares.

(e) The cash dividends caused M&S’s Retained Earnings to decrease by

£301.7 million.

(f) Return on ordinary share equity:

COMPARATIVE ANALYSIS CASE

(a) Par value:

adidas, No par.

Puma, No par.

(b) Number of authorized shares issued:

(d) Ordinary shares outstanding, year-end 2015:

adidas, 201.2 million.

Puma, 14.939 million.

(e) adidas declared cash dividends of €1.60 per share in 2015, reducing

(f) Rate of return on ordinary share equity.

2015 (€000,000):

COMPARATIVE ANALYSIS CASE (Continued)

2014:

adidas

€496

= 8.8%

€5,618*

(g) Payout ratios for 2015 (€000,000).

adidas

€309

= 48.3%

€640

Puma

= 80.2%

FINANCIAL STATEMENT ANALYSIS CASES

CASE 1

(a) Management might purchase treasury shares to provide to share–

holders a tax-efficient method for receiving cash from the corporation.

In addition, it might have to repurchase shares to have them available

(b) Earnings per share is calculated by dividing net income by the weighted–

average number of shares outstanding during the year.

If shares are reduced by treasury share purchases, the denominator

(c) One measure of solvency is the ratio of debt divided by total assets.

This ratio shows how many dollars of assets are backing up each dollar

of debt, should the company become financially troubled. For the

current prior year, this can be calculated as follows:

FINANCIAL STATEMENT ANALYSIS CASES

CASE 2

(a) The date of record marks the time when ownership of the outstanding

shares is determined for dividend purposes. This in turn identifies

which shareholders will receive the share dividend. This date is also

used when a share split occurs. The date of distribution is when the

ACCOUNTING, ANALYSIS, AND PRINCIPLES

ACCOUNTING

January 15, 2019

Retained Earnings (€1.05 X 60,000) …………….. 63,000

Cash ………………………………………………. 63,000

November 15, 2019

Cash (€18 X 1,000) …………………………………….. 18,000

Share Premium—Treasury ………………. 3,000

Treasury Shares ……………………………… 15,000

ACCOUNTING, ANALYSIS, AND PRINCIPLES (Continued)

The balances are indicated in the following partial statement of financial

position:

NADAL SE

Statement of Financial Position (partial)

December 31, 2019

Equity

Share capital—ordinary, €10 par value,

(1) €600,000 + €60,000

ANALYSIS

Payout ratio: €63,000 ÷ €370,000 = 17%

PRINCIPLES

Treasury shares sold above or below cost do not result in gains or losses

because treasury shares do not meet the definition of an asset. Rather,

they are unissued equity. Furthermore, gains or losses should not be

RESEARCH CASE

(b) An entity shall disclose the following, either in the statement of

financial position or the statement of changes in equity, or in the

notes:

(a) for each class of share capital:

(i) the number of shares authorised;

(ii) the number of shares issued and fully paid, and issued but

not fully paid;

(iii) par value per share, or that the shares have no par value;

(iv) a reconciliation of the number of shares outstanding at the

(b) a description of the nature and purpose of each reserve within

equity (para. 79).

An entity shall present, either in the statement of changes in equity or in

the notes, the amount of dividends recognised as distributions to owners

RESEARCH CASE (Continued)

Changes in an entity’s equity between the beginning and the end of the

reporting period reflect the increase or decrease in its net assets during the

period. Except for changes resulting from transactions with owners in their

IAS 8 requires retrospective adjustments to effect changes in accounting

policies, to the extent practicable, except when the transition provisions in

another IFRS require otherwise. IAS 8 also requires restatements to correct

GAAP CONCEPTS AND APPLICATION

GAAP15.1. No, Mary should not make that conclusion. While IFRS allows

unrealized losses on non-trading equity investments to be

GAAP15.2. Key similarities between IFRS and U.S. GAAP for transactions

related to equity pertain to (1) issuance of shares, (2) purchase

Major differences relate to terminology used, introduction of

items such as revaluation surplus, and presentation of

stockholder equity information. In addition, the accounting for

treasury stock retirements differs between IFRS and U.S.

GAAP. Under U.S. GAAP a company has the option of charging

dividends (less than 20–25%) are accounted for using the fair

value of shares issued in determining the transfer from retained

earnings. An IFRS/U.S. GAAP difference relates to the account

GAAP15.3. It is likely that the statement of stockholders’ equity and its

presentation will be examined closely in the financial statement