PROBLEM 19.8 (Continued)

Solving for X; X – ¥120,000,000 = ¥325,000,000; X = ¥445,000,000 pretax

financial income.

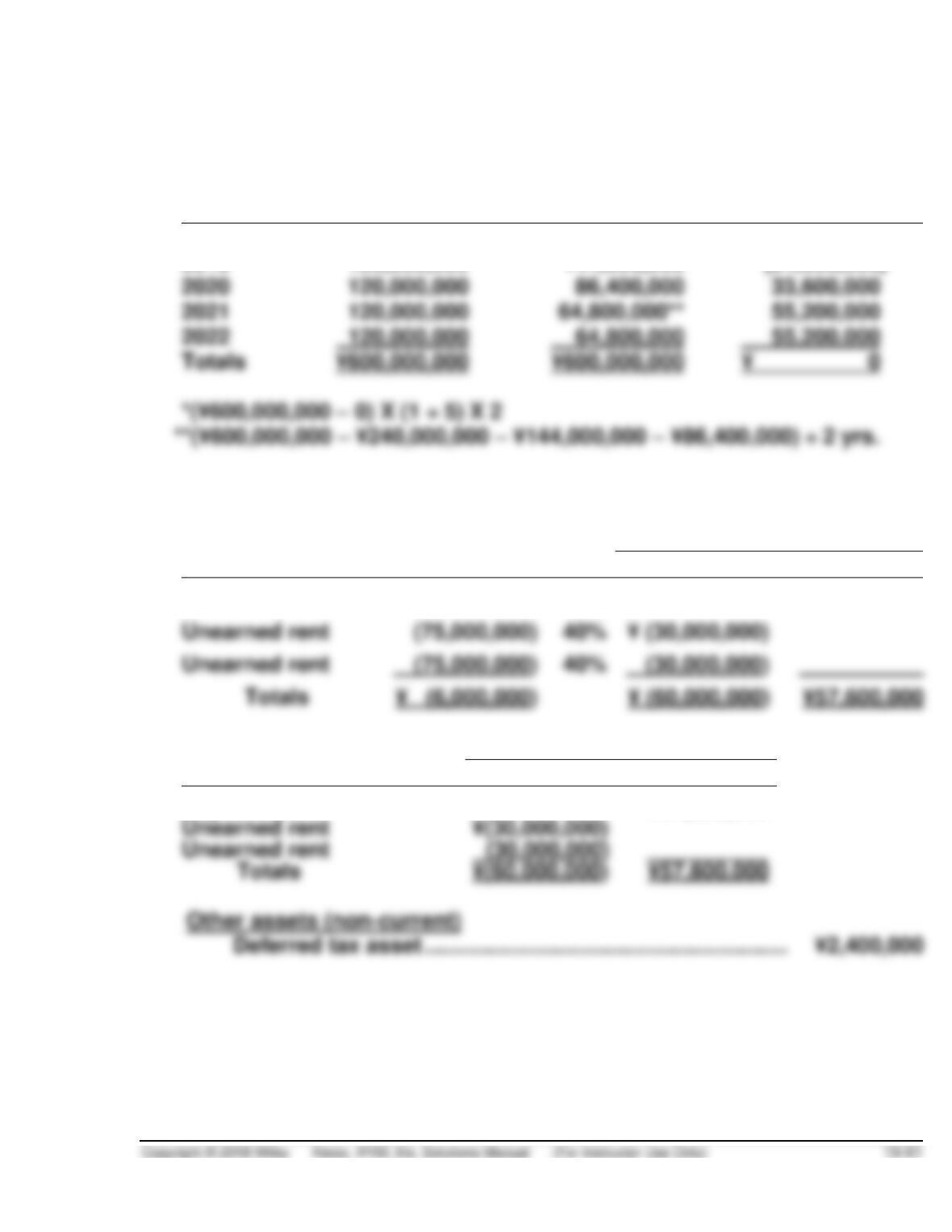

Book Depreciation

Tax Depreciation

bDifferenceb

2018

¥120,000,000

¥240,000,000*

(¥(120,000,000)

2019

120,000,000

144,000,000

(24,000,000)

2020

2021

2022

64,800,000

¥600,000,000

¥600,000,000

(d)

Temporary

Difference

Future Taxable

(Deductible)

Amounts

Tax

Rate

Deferred Tax

(Asset)

Liability

Depreciation

¥144,000,000

40%

¥57,600,000

40%

¥ (6,000,000)

Temporary

Difference

Resulting Deferred Tax

(Asset)

Liability

Depreciation

¥57,600,000

Unearned rent

Unearned rent

¥57,600,000

PROBLEM 19.8 (Continued)

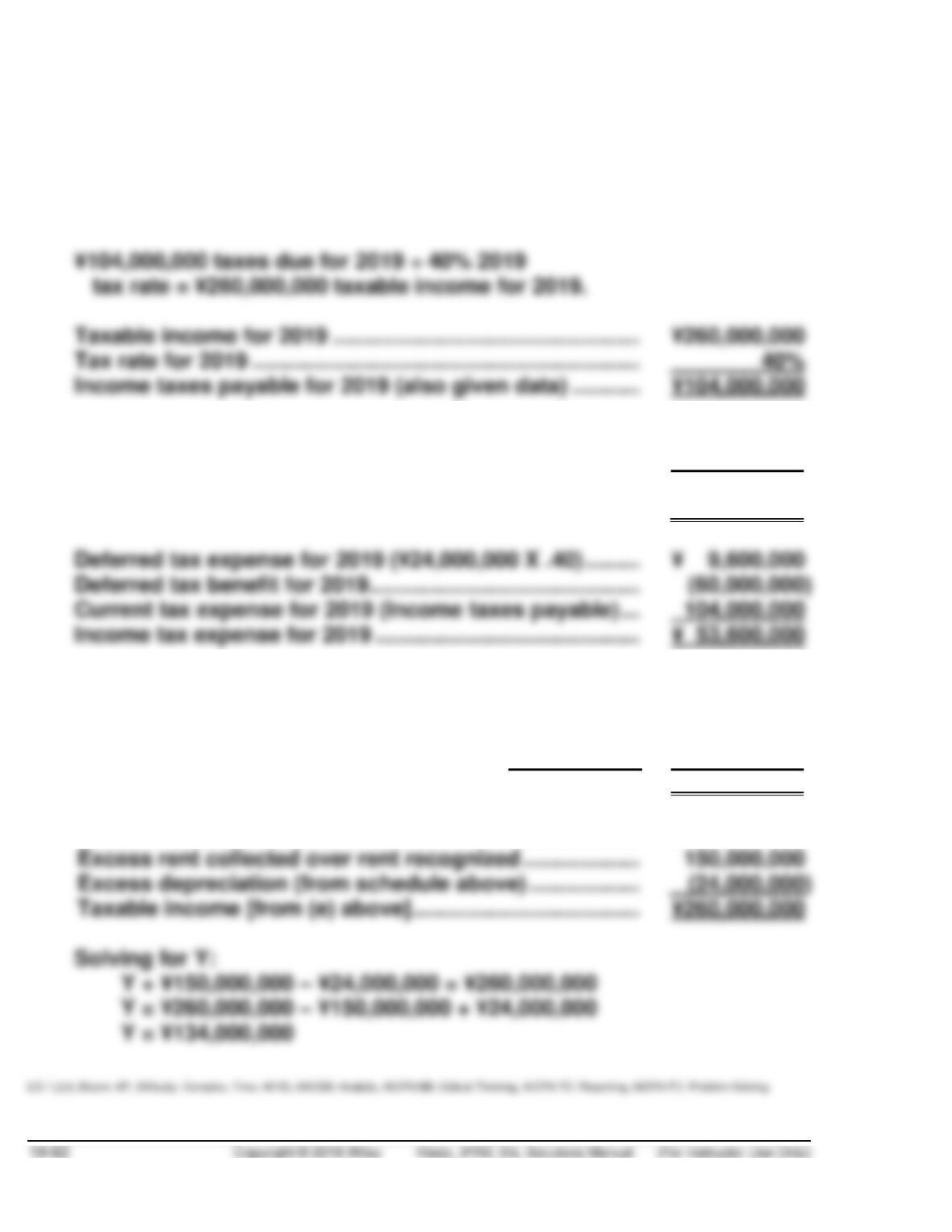

(e) Income Tax Expense ………………………………. 53,600,000

Deferred Tax Asset …………………………………. 60,000,000

Income Taxes Payable ……………………… 104,000,000

Deferred Tax Liability ……………………….. 9,600,000

Deferred tax asset at the end of 2019 ………………………… ¥ 60,000,000

Deferred tax asset at the beginning of 2019 ………………. 0

Deferred tax benefit for 2019 (increase in

deferred tax asset) ……………………………………………….. ¥ (60,000,000)

(f) Income before income taxes ………………. ¥134,000,000c

Income tax expense

Current ………………………………………. ¥104,000,000

Deferred …………………………………….. (50,400,000) 53,600,000

Net income ……………………………………….. ¥ 80,400,000

cPretax financial income……………………………………………. ¥ Y

PROBLEM 19.9

(a) Pretax financial income …………………………………………………. €100,000

Permanent differences:

Fine for pollution …………………………..……………………….. 3,500

Tax-exempt interest ……………………………………………….. (1,500)

(b)

Temporary

Difference

Future Taxable

(Deductible) Amounts

Tax

Rate

Deferred Tax

(Asset)

Liability

Warranty costs

€ (5,000)

40%

€(2,000)

Construction profits

40%

Depreciation

40%

Totals

€(2,000)

(c) Income Tax Expense …………………………………………. 40,800

Deferred Tax Asset ……………………………………………. 2,000

Deferred Tax Liability ………………………………….. 18,000

Income Taxes Payable ………………………………… 24,800

PROBLEM 19.9 (Continued)

Deferred tax asset at the end of 2019 ……………………………… € 2,000

Deferred tax asset at the beginning of 2019 ……………………. 0

Deferred tax benefit for 2019 ………………………………………….. € (2,000)

Deferred tax expense for 2019 ……………………………………….. € 18,000

(d) Income before income taxes ……………………………. €100,000

Income tax expense

Current ……………………………………………………. €24,800

TIME AND PURPOSE OF CONCEPTS FOR ANALYSIS

CA 19.1 (Time 15–20 minutes)

Purpose—to provide the student an opportunity to explain the objectives in accounting for income taxes

CA 19.2 (Time 20–25 minutes)

Purpose—to provide the student an opportunity to discuss the principles of the asset-liability method,

CA 19.3 (Time 20–25 minutes)

Purpose—to develop an understanding of temporary and permanent differences. The student is

CA 19.4 (Time 20–25 minutes)

Purpose—to develop an understanding of deferred taxes. The student is required to indicate whether

deferred income taxes should be recognized for each of four items.

CA 19.5 (Time 20–25 minutes)

CA 19.6 (Time 20–25 minutes)

Purpose—to develop an understanding of the concept of future taxable amounts and future deductible

CA 19.7 (Time 20–25 minutes)

Purpose—to provide the student an opportunity to examine the income effects of deferred taxes, including

ethical issues.

SOLUTIONS TO CONCEPTS FOR ANALYSIS

CA 19.1

(a) The objectives in accounting for income taxes are:

1. To recognize the amount of taxes payable or refundable for the current year.

(b) To implement the objectives, the following basic principles are applied in accounting for income

taxes at the date of the financial statements:

1. A current tax liability or asset is recognized for the estimated taxes payable or refundable

on the tax return for the current year.

(c) The procedures for the annual computation of deferred income taxes are as follows:

1. Identify: (1) the types and amounts of existing temporary differences and (2) the nature and

amount of each type of operating loss and tax credit carryforward and the remaining length

of the carryforward period.

CA 19.2

(a) The following basic principles are applied in accounting for income taxes at the date of the

financial statements:

1. A current tax liability or asset is recognized for the estimated taxes payable or refundable

on the tax return for the current year.

2. A deferred tax liability or asset is recognized for the estimated future tax effects attributable

(b) Dexter should do the following in accounting for the temporary differences.

1. Identify the types and amounts of existing temporary differences. The depreciation policies

give rise to a temporary difference that will result in net future taxable amounts (because

CA 19.2 (Continued)

3. Measure the total deferred tax asset for the deductible temporary difference using the

enacted tax rate.

(c) Deferred tax accounts are reported on the statement of financial position as assets or liabilities.

They should be classified in a net non-current amount.

Dexter’s deferred tax liability from the depreciation difference and deferred tax asset from the

CA 19.3

(a) 1. Temporary difference. The full estimated three years of warranty costs reduce the current

year’s pretax financial income, but will reduce taxable income in varying amounts each

respective year, as paid. Assuming the estimate as to each warranty is valid, the total

2. Temporary difference. The difference between the tax basis and the reported amount (book

basis) of the depreciable property will result in taxable or deductible amounts in future years

when the reported amount of the asset is recovered (through use or sale of the asset);

hence, it is a temporary difference.

3. Temporary difference and permanent difference. The investor’s share of earnings of an

investee (other than subsidiaries and corporate joint ventures) accounted for by the equity

method is included in pretax financial income. In some countries dividends from one

4. Temporary difference. For financial reporting purposes, any gain experienced in an involun–

tary conversion of a non-monetary asset to a monetary asset must be recognized in the

CA 19.3 (Continued)

(b) Deferred tax assets and deferred tax liabilities are separately recognized and measured but are

CA 19.4

(a) Deferred income taxes are reported in the financial statements when temporary differences exist

at the statement of financial position date. Deferred taxes are never reported for permanent

differences.

The tax consequences of most events recognized in the financial statements for a year are

included in determining income taxes currently payable. However, tax laws often differ from the

recognition and measurement requirements of financial accounting standards, and differences

can arise between: (1) the amount of taxable income and pretax financial income for a year and

A deferred tax liability is reported for the increase in taxes payable in future years as a result of

taxable temporary differences existing at the statement of financial position date. A deferred tax

asset is reported for the increase in taxes refundable in future years as a result of deductible

temporary differences existing at the statement of financial position date. The most common

temporary differences arise from including revenues or expenses in taxable income in a period

later or earlier than the period in which they are included in pretax financial income.

(b) 1. Income on installment sales—Deferred income taxes would be recognized when income on

installment sales is included in pretax financial income in the year of sale and included in

taxable income when later collected.

2. Revenues on long-term construction contracts—Deferred income taxes would be recog-

CA 19.5

(a) The 45% tax rate would be used in computing the deferred tax liability at December 31, 2018, if a

tax rate is 45% in 2018). (See discussion on the next page.)

(b) The 40% tax rate would be used in computing the deferred tax liability at December 31, 2018, if

which the future taxable amount is expected to occur). (See discussion on the next page.)

CA 19.5 (Continued)

(c) The 34% tax rate would be used in computing the deferred tax liability at December 31, 2018, if a

net operating loss (an NOL) is expected in 2019 that is to be carried forward to 2020 (the tax rate

enacted for 2016 is 34%). (See discussion below.)

Discussion:

In determining the future tax consequences of temporary differences, it is helpful to prepare a schedule

which shows in which future years existing temporary differences will result in taxable or deductible

amounts. The appropriate enacted tax rate is applied to these future taxable and deductible amounts.

For future taxable amounts:

1. If taxable income is expected in the year that a future taxable amount is scheduled, use the

enacted rate for that future year to calculate the related deferred tax liability.

For future deductible amounts:

1. If taxable income is expected in the year that a future deductible amount is scheduled, use the

enacted rate for that future year to calculate the related deferred tax asset.

CA 19.6

(a) Future taxable amounts increase taxable income relative to pretax financial income in the future

due to temporary differences existing at the statement of financial position date. Future deductible

(b) The carryback and carryforward provisions will affect the amounts to be reported for the resulting

deferred tax asset and deferred tax liability.

In computing deferred tax account balances to be reported at a statement of financial position

CA 19.6 (Continued)

For future taxable amounts:

1. If taxable income is expected in the year that a future taxable amount is scheduled, use the

enacted rate for that future year to calculate the related deferred tax liability.

For future deductible amounts:

1. If taxable income is expected in the year that a future deductible amount is scheduled, use

the enacted rate for that future year to calculate the related deferred tax asset.

CA 19.7

(a) To realize a sizable deferred tax liability, Acme must have used an accelerated depreciation

method for tax purposes while using straight-line depreciation for its financial statements. Once

(b) The deferral of income taxes means that due to temporary differences caused by the difference

in financial accounting principles and tax laws, a company will be able to defer paying its income

(c) The primary stakeholders who could be harmed by Acme’s income tax practice are the federal

government, which receives fewer taxes as a result of this practice. Ultimately, other taxpayers

have to pay more. In addition, if replacement plant assets are very costly to acquire, positive cash flow

is reduced. Though the impact should not be great, investors and creditors are affected negatively.

FINANCIAL REPORTING PROBLEM

(a) 1. Per M&S’s 2016 income statement:

“Total income tax expense ……………………….. £84.4 million”

2. Per M&S’s 2 April, 2016 statement of

financial position:

(b) M&S’s effective tax rates per note 7:

2016: (17.3%), 2015: (19.7%)

(c) Income tax expense per note 7:

Current ………………………………………………………….. £117.9

Deferred Tax Assets/(Liabilities)

Land and buildings temporary differences ……………………… £ (46.8)

COMPARATIVE ANALYSIS CASE

(a) 2015 provision for income taxes (In Millions):

adidas: Current portion (€ 439)

(b) 2015 income tax payments (In Millions):

adidas € 386

Puma € 38.4

(d)

(In Millions)

adidas

Puma

1.

Gross deferred tax assets

€731

€251.0

Gross deferred tax liabilities

462

95.4

(e) Net operating loss carryforwards at year-end 2015:

adidas discloses (note 34) that it recognizes a deferred tax asset

related to loss carryforwards in the amount of €56 million. However, it

FINANCIAL STATEMENT ANALYSIS CASE

(a) Of the total provision for income taxes (reported in the income

statement) the “current taxes” portion represents the taxes payable in

(b) Future taxable amounts increase taxable income relative to pretax

financial income in the future due to temporary differences existing at

the statement of financial position date. Future deductible amounts

(c) The carryback and carryforward provisions will affect the amounts to

be reported for the resulting deferred tax asset and deferred tax liability.

In computing deferred tax account balances to be reported at a state–

For future taxable amounts:

1. If taxable income is expected in the year that a future taxable

amount is scheduled, use the enacted rate for that future year to

calculate the related deferred tax liability.

FINANCIAL STATEMENT ANALYSIS CASE (Continued)

2. If an NOL is expected in the year that a future taxable amount is

scheduled, use the enacted rate of what would be the prior year

1. If taxable income is expected in the year that a future deductible

2. If an NOL is expected in the year that a future deductible amount is

scheduled, use the enacted rate of what would be the prior year

ACCOUNTING, ANALYSIS, AND PRINCIPLES

ACCOUNTING

Taxable income for 2019:

Pretax financial income for 2019 ……………………… €500,000

Permanent differences:

498,000

Temporary differences:

Excess gross profit per books

Adler has future taxable amounts arising from temporary differences as

follows:

Year

Future taxable amount

Tax rate

Deferred tax

The €179,200 is a deferred tax liability because the temporary difference

is from future taxable amounts. The total deferred tax liability is

$219,200 ($40,000 + $179,200).

Additional deferred tax liability needed = €219,200 – €40,000 = €179,200

ACCOUNTING, ANALYSIS, AND PRINCIPLES (Continued)

ANALYSIS

The €179,200 deferred tax liability would be classified as a non-current

liability. Income taxes payable would be classified as a current liability.

The income tax expense portion of the income statement could look as

follows:

Income before income taxes …………………………... €500,000

Income tax expense:

PRINCIPLES

We can use the Conceptual Framework to determine that deferred taxes

RESEARCH CASE

(a) According to IAS 12, paragraph 34, “A deferred tax asset shall be

recognised for the carryforward of unused tax losses and unused tax

balance.

(b) This question relates to the information found in paragraph 36, which

states “An entity considers the following criteria in assessing the

probability that taxable profit will be available against which the

unused tax losses or unused tax credits can be utilised:

(1) whether the entity has sufficient taxable temporary differences

relating to the same taxation authority and the same taxable

(2) whether it is probable that the entity will have taxable profits

before the unused tax losses or unused tax credits expire;

(3) whether the unused tax losses result from identifiable causes

which are unlikely to recur; and

RESEARCH CASE (Continued)

(c) Paragraph 30 discusses tax planning opportunities: “Tax planning

opportunities are actions that the entity would take in order to create

or increase taxable income in a particular period before the expiry of a

tax loss or tax credit carryforward. For example, in some jurisdictions,

taxable profit may be created or increased by:

(1) electing to have interest income taxed on either a received or

receivable basis;

(2) deferring the claim for certain deductions from taxable profit;

(3) selling, and perhaps leasing back, assets that have appreciated

GAAP CONCEPTS and APPLICATION

GAAP 19.1 Both IFRS and U.S. GAAP use the asset and liability approach for

recording deferred tax assets and liabilities. In general, the

differences between IFRS and U.S. GAAP involve limited differences

in the exceptions to the asset-liability approach, some minor

differences in the recognition, measurement and disclosure criteria,

and differences in implementation guidance. The classification of

deferred taxes under GAAP and IFRS is always non-current.

Following are some key elements for comparison.

• Under IFRS, an affirmative judgment approach is used by which a

deferred tax asset is recognized up to the amount that is probable

• IFRS uses the enacted tax rate or substantially enacted tax rate

(Substantially enacted means virtually certain). For U.S. GAAP,

the enacted tax rate must be used.

• The tax effects related to certain items are reported in equity

under IFRS. That is not the case under U.S. GAAP, which charges

or credits the tax effects to income.

GAAP CONCEPTS and APPLICATION (Continued)

GAAP19.2 The IASB and the FASB have been working to address some of

the differences in the accounting for income taxes. Some of the

issues under discussion are the term “probable” under IFRS for

recognition of a deferred tax asset, which might be interpreted to

mean “more likely than not”. If changed, the reporting for

impairments of deferred tax assets will be essentially the same

between U.S. GAAP and IFRS. In addition, the IASB is considering

adoption of the classification approach used in U.S. GAAP for