CA 12.2 (Continued)

The amount of interest cost for the first nine months of 2019 is part of the 2018 loss resulting from the

tornado. The extension of the construction period to October 2019 because of the tornado does not

warrant its capitalization as construction period interest. It is in effect an uninsured loss resulting from

the tornado. Had it not been for the tornado, the entire amount would have been a normal operating

expense chargeable against the rental revenue that would have been earned during the first nine

months of 2019.

Cost of obtaining tenants. Both the 2018 and 2019 costs of obtaining tenants should be expensed as

CA 12.3

(a) A pound to be received in the future is worth less than a pound received today because of an

interest or discount factor—often referred to as the time value of money. The discounted value of

(b) If the royalty receipts are expected to occur at regular intervals and the amounts are to be fairly

constant, their discounted value can be calculated by multiplying the value of one such receipt by

the present value of an annuity of 1 for the number of periods the receipts are expected. On the

other hand, if receipts are expected to be irregular in amount or if they are to occur at irregular

CA 12.3 (Continued)

(c) The basis of valuation for patents that is generally accepted in accounting is cost. Evidently the

cartons were developed and the patents obtained directly by the client corporation. Those costs

(d) Intangible assets represent rights to future benefits. The ideal measure of the value of intangible

(e) The amortization policy is implied in the definition of intangible assets as rights to future benefits.

As the benefits are received by the firm, the cost or other value should be charged to expense or

(f) The litigation can and should be mentioned in notes to the financial statements. Some indication of

the expectations of legal counsel in respect to the outcome can properly accompany the

statements. It would be inappropriate to record a contingent asset reflecting the expected

damages to be recovered. Costs incurred to September 30, 2019, in connection with the litigation

CA 12.4

(a) Research, as defined in IFRS, is “original and planned investigation undertaken with the prospect of

gaining new scientific or technical knowledge and understanding.”

Development, as defined in IFRS, is “application of research findings or other knowledge to a plan

CA 12.4 (Continued)

(b) The current accounting and reporting practices for research and development costs (incurred

before achieving economic viability) were promulgated by the IASB in order to reduce the number

of alternatives that previously existed and to provide useful financial information about research

In reaching this decision, the IASB considered the three pervasive principles of expense recog–

nition: (1) associating cause and effect, (2) systematic and rational allocation, and (3) immediate

recognition. The IASB found little or no evidence of a direct causal relationship between current

(c) The following costs attributable only to research and development should be expensed as incurred:

Design and engineering studies.

Prototype manufacturing costs.

Administrative costs related solely to research and development.

(d) Economic viability indicates that a project is far enough along in the process such that the economic

benefits of the R&D project will probably flow to the company. Development costs incurred from that

CA 12.5

(a) Investors and creditors are concerned with corporate profits, dividends, and cash flow. Employees

in Czeslaw Corporation’s R&D department are concerned about job security if the company begins

(c) Reid should do what is best for Czeslaw Corporation in the long run. He should choose to have the

project done where the work will be done well and at the lowest cost. Whether expenses will appear

in the income statement immediately or will be capitalized and allocated over a period of years should

FINANCIAL REPORTING PROBLEM

(a) M&S shows Intangible Assets on the statement of financial position.

(b) M&S reported selling and administrative expenses of £3,304.8 million

in 2015 and £3,412.9 million in 2016. These expenses were significant

COMPARATIVE ANALYSIS CASE

(a) (1) adidas reports: Goodwill €1,392M, Trademarks €1,628M, and

Other intangibles €188M. Puma reports: Goodwill €240.3M and

(b) (1) adidas amortizes software over 5-7 years and patents,

trademarks, and other 2–15 years. Puma amortizes finite-lived

intangibles over 3–10 years.

(2) adidas had accumulated amortization of €697M and €609M on

(3) adidas identified the composition of its intangible assets as

follows:

Goodwill €1,392M

FINANCIAL STATEMENT ANALYSIS CASE 1

MERCK AND JOHNSON & JOHNSON

(a) The primary intangible assets of a healthcare products company

(b) Many corporate executives complain that investors are too concerned

about the short-term and don’t reward good long-term planning. As a

(c) If a company reports goodwill on its statement of financial position, it

can only have resulted from one thing—the company must have

purchased another company. This is because companies are not

FINANCIAL STATEMENT ANALYSIS CASE 2

(a) The depressed market values (less than book value) suggest that

market participants are not very optimistic about the future prospects

(b) Because the market (fair) value of each company is less than its book

value of its net assets, it fails the first step in the goodwill impairment

test; an impairment should be recorded.

A

B

C

D

E

F

G

H

(Columns C–D)

(Columns B–F)

(Columns D–G)

Company

Market

Value

Book Value

(Net Assets)

Carrying

Value of

Goodwill

ROA

Estimated Fair

Value of Net

Assets

Implied GW

(NA-Market

Value)

Goodwill

Impairment

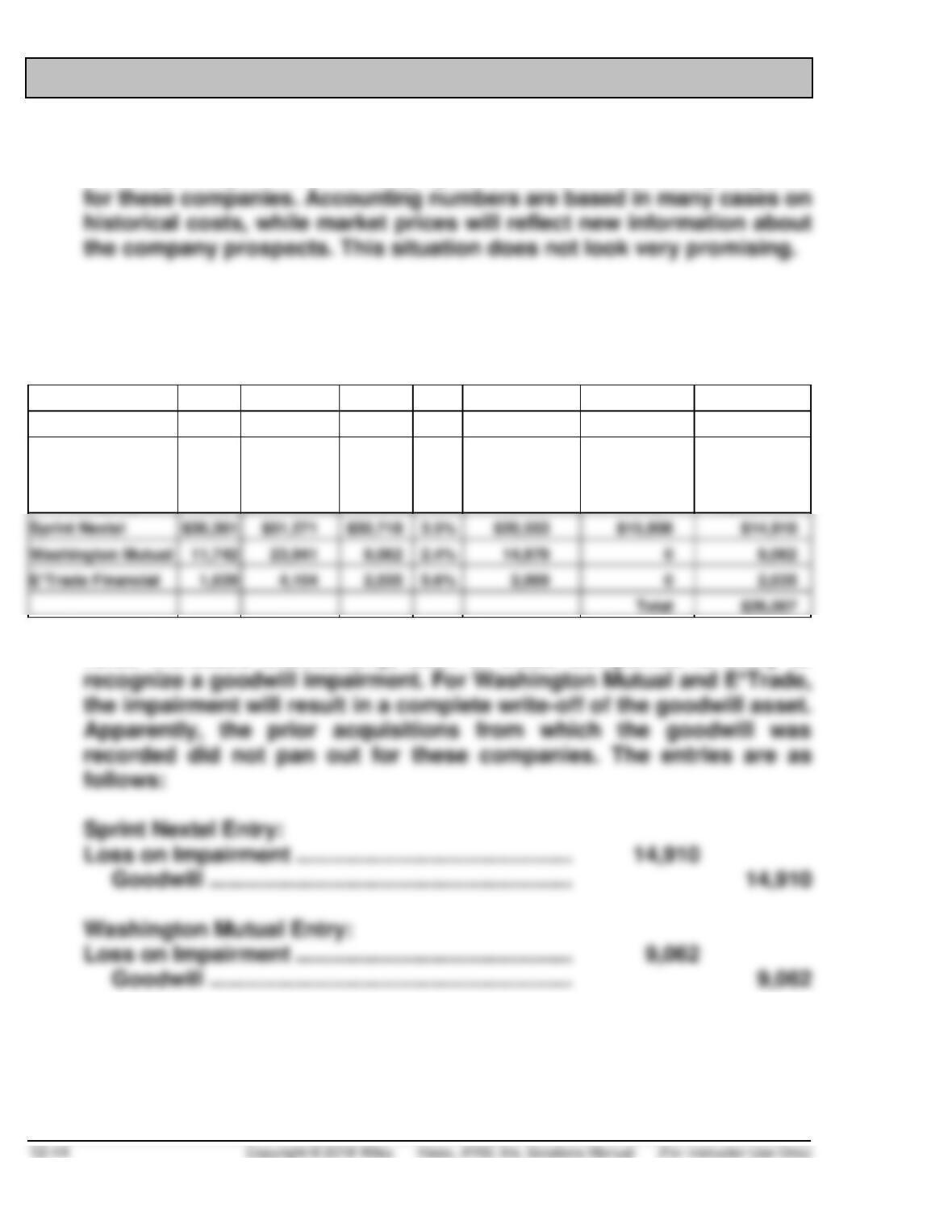

Sprint Nextel

$36,361

E*Trade Financial

4,104

Total

(c) As indicated in the expanded spreadsheet above, unless their market

value increases dramatically, each of these companies is likely to

E*Trade Entry:

Loss on Impairment ……………………………………… 2,035

Goodwill ………………………………………………….. 2,035

(d) Impairment losses are reported in operating income. Thus, the impair–

ments will reduce the numerator in the return on asset ratio. Without

There is a full year of amortization on the copyright. There is no amortization

for the trade name, which is considered an indefinite-life intangible.

The recoverable amount of €16,000 is greater than the carrying value. Thus,

the copyright is not impaired: The trade name is tested for impairment using

a recoverable amount test. Thus, Raconteur writes it down to the

ANALYSIS

Impairment losses are recorded in operating income. Because impairment

losses tend to be nonrecurring items, their recognition can make operating

income more volatile from year to year. This volatility effect can be

ACCOUNTING, ANALYSIS, AND PRINCIPLES (Continued)

PRINCIPLES

The accounting for impairments provides relevant information about intangible

assets by indicating in a timely fashion that intangible assets have declined

RESEARCH CASE

(a) IFRS 3 addresses goodwill, while IAS 38 addresses intangible assets.

(b) IFRS 3 defines goodwill as “an asset representing the future economic

(c) No, goodwill is not amortized. However, it is subject to impairment

testing, as discussed in IAS 36.

(d) Goodwill recognised in a business combination is an asset representing

the future economic benefits arising from other assets acquired in a

business combination that are not individually identified and separately

references also to a group of cash-generating units to which goodwill

is allocated (IAS 36, par. 81).

Applying the requirements in paragraph 80 results in goodwill being

tested for impairment at a level that reflects the way an entity

manages its operations and with which the goodwill would naturally

RESEARCH CASE (Continued)

A cash-generating unit to which goodwill is allocated for the purpose

of impairment testing may not coincide with the level at which

goodwill is allocated in accordance with IAS 21 The Effects of

If the initial allocation of goodwill acquired in a business combination

In accordance with IFRS 3 Business Combinations, if the initial

accounting for a business combination can be determined only

provisionally by the end of the period in which the combination is

effected, the acquirer:

a. accounts for the combination using those provisional values; and

b. recognises any adjustments to those provisional values as a

PROFESSIONAL SIMULATION (Continued)

GAAP PRACTICE

GAAP 12.1. Similarities include (1) in U.S. GAAP and IFRS, the costs associated with research and

development are segregated into the two components; (2) IFRS and U.S. GAAP are similar for

Notable differences are: (1) while costs in the research phase are always expensed under both

IFRS and U.S. GAAP, under IFRS costs in the development phase are capitalized once

GAAP 12.2. As shown in the analysis below, under IFRS, Sophia’s ROA is overstated compared to a

U.S. GAAP company.

IFRS

U.S. GAAP

Net Income

€ 1,125

€ 920*

Average Assets

12,500

12,295**

ROA (Income ÷ Assets)

GAAP 12.3. The IASB has identified a project relating to the accounting for research and develop–

ment that could result in expanded recognition of internally generated intangible assets. IFRS

GAAP PRACTICE (Continued)

GAAP 12.4

(a) ROE = Net Income ÷ Shareholders’ Equity

(b) If some companies capitalize development expenses, this will result

in higher reported assets and income (because R&D expense will be