EXERCISE 16.13 (15–25 minutes)

1/1/18 No entry (total compensation cost is HK$450,000)

12/31/18 Compensation Expense …………………………….. 225,000

Share Premium—Share Options

(HK$450,000 X 1/2) ……………………………. 225,000

EXERCISE 16.14 (10–15 minutes)

(a) 1/1/19 Unearned Compensation …………………………... 120,000

Share Capital—Ordinary (4,000 X £5) ……. 20,000

Share Premium—Ordinary …………………… 100,000

EXERCISE 16.15 (10–15 minutes)

(a) 1/1/19 Unearned Compensation …………………………... 500,000

Share Capital—Ordinary (€10 X 10,000) … 100,000

Share Premium—Ordinary …………………… 400,000

EXERCISE 16.15 (Continued)

EXERCISE 16.16 (15–25 minutes)

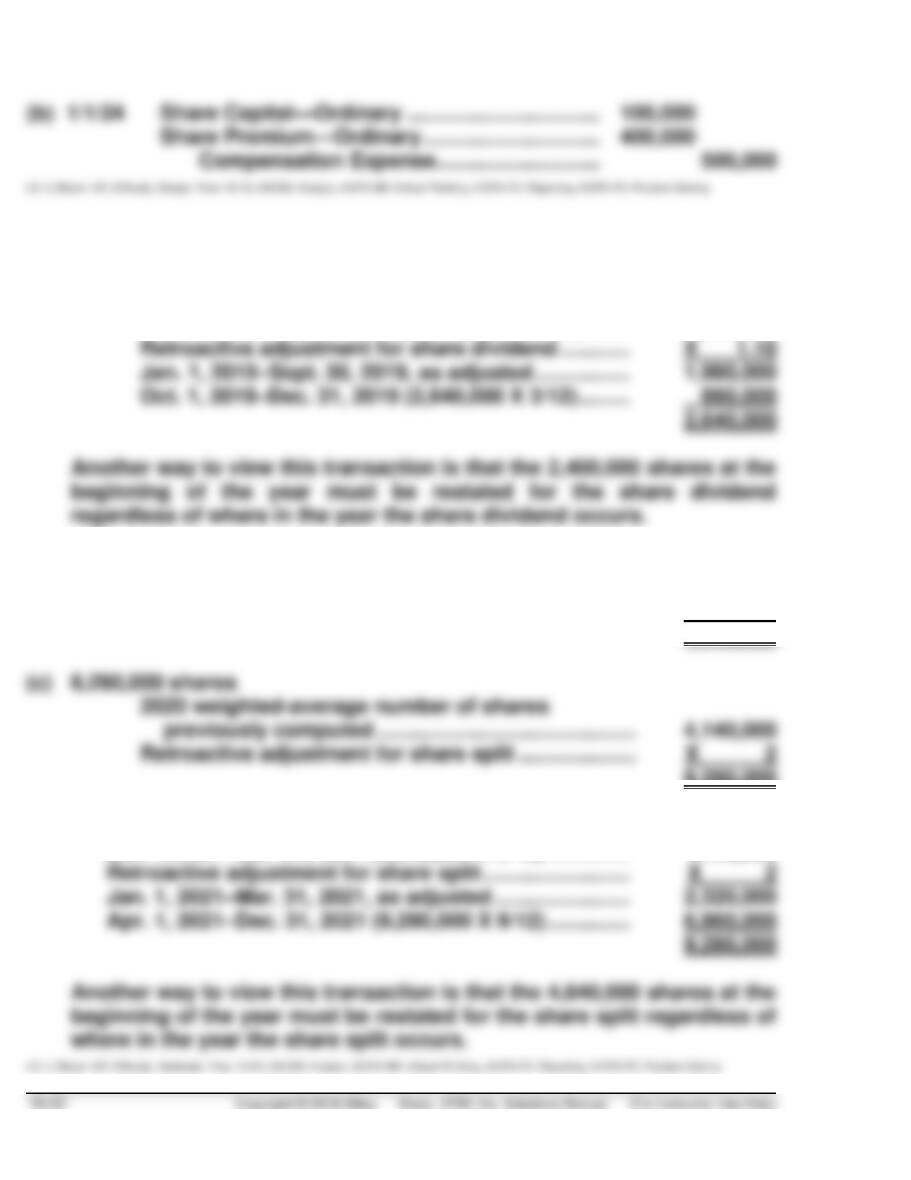

(a) 2,640,000 shares

Jan. 1, 2019–Sept. 30, 2019 (2,400,000 X 9/12) ……. 1,800,000

(b) 4,140,000 shares

Jan. 1, 2020–Mar. 31, 2020 (2,640,000 X 3/12) ………. 660,000

Apr. 1, 2020–Dec. 31, 2020 (4,640,000 X 9/12) ……… 3,480,000

4,140,000

8,280,000

(d) 9,280,000 shares

Jan. 1, 2021–Mar. 31, 2021 (4,640,000 X 3/12) ………….. 1,160,000

EXERCISE 16.17 (10–15 minutes)

(a)

Event

Dates

Outstanding

Shares

Outstanding

Restatement

Fraction

of Year

Weighted

Shares

Beginning balance

Jan. 1–Feb. 1

480,000

1.2 X 3.0

1/12

144,000

Share dividend

720,000

3.0

2/12

360,000

Share split

4/12

620,000

Reissued shares

3/12

(b)

Earnings Per Share =

¥3,256,000,000 (Net Income)

= ¥1,679.22

1,939,000 (Weighted-Average Shares)

(d) Income from continuing operationsa ……………………….. ¥ 1,902.01

Loss from discontinued operationsb ……………………….. 222.80

Net income ……………………………………………………………. ¥ 1,679.21

EXERCISE 16.18 (10–15 minutes)

Event

Dates

Outstanding

Shares

Outstanding

Fraction

of Year

Weighted

Shares

Beginning balance

Jan. 1–May 1

210,000

4/12

70,000

Issued shares

May 1–Oct. 31

218,000

6/12

Reacquired shares

Oct. 31–Dec. 31

204,000

2/12

Weighted-average number of shares outstanding

EXERCISE 16.19 (10–15 minutes)

Event

Dates

Outstanding

Shares

Outstanding

Restatement

Fraction

of Year

Weighted

Shares

Beginning balance

Jan. 1–May 1

600,000

2

4/12

400,000

Reacquired shares

Aug. 1–Dec. 31

750,000

2

5/12

Net income ………………………………………………………………………… ¥2,200,000

Preference dividend (50,000 X ¥100 X 8%) …………………………... (400,000)

¥1,800,000

EXERCISE 16.20 (20–25 minutes)

Earnings per ordinary share:

Income data:

Income from continuing operations ……………………………… $15,000,000

Dates

Outstanding

Shares

Outstanding

Fraction

of Year

Weighted

Shares

January 1–April 1

7,000,000

3/12

1,750,000

April 1–December 31

8,000,000

9/12

6,000,000

Weighted-average number of shares outstanding

7,750,000

EXERCISE 16.21 (10–15 minutes)

Income from continuing operations before taxes …………………. €300,000

Income taxes …………………………………………………………………….. 120,000

EXERCISE 16.21 (Continued)

Dates

Outstanding

Shares

Outstanding

Fraction

of Year

Weighted

Shares

January 1–April 1

200,000

3/12

50,000

April 1–July 1

260,000

3/12

65,000

July 1–Oct. 1

340,000

3/12

85,000

Oct. 1–Dec. 31

370,000

3/12

Weighted-average number of shares outstanding

EXERCISE 16.22 (10–15 minutes)

Event

Dates

Outstanding

Shares

Outstanding

Fraction

of Year

Weighted

Shares

Beginning balance

Jan. 1–April 1

800,000

3/12

200,000

Issued shares

April 1–Oct. 1

1,250,000

6/12

625,000

Reacquired shares

1,140,000

3/12

EXERCISE 16.23 (20–25 minutes)

(a) Revenues ₺17,500

Expenses:

Other than interest ………………………………….. ₺8,400

(b) Revenues………………………………………………………. ₺17,500

Expenses:

Other than interest ………………………………….. ₺8,400

(c) Revenues………………………………………………………. ₺17,500

Expenses:

Other than interest ………………………………….. ₺8,400

Bond interest (75 X ₺950 X .10 X 1/2)….. 3,563

EXERCISE 16.24 (15–20 minutes)

(a) 1. Number of shares for basic earnings per share.

Dates

Outstanding

Shares

Outstanding

Fraction

of Year

Weighted

Shares

Jan. 1–April 1

800,000

3/12

200,000

April 1–Dec. 1

9/12

2. Number of shares for diluted earnings per share:

Dates

Outstanding

Shares

Outstanding

Fraction

of Year

Weighted

Shares

Jan. 1–April 1

800,000

3/12

200,000

(b) 1. Earnings for basic earnings per share:

After-tax net income ……………………………… €1,540,000

2. Earnings for diluted earnings per share:

After-tax net income ……………………………… €1,540,000

Add back interest on convertible

EXERCISE 16.25 (20–25 minutes)

(a) Net income for year …………………………………………………… $7,500,000

Add: Adjustment for interest (net of tax) ……………………. 208,000*

$7,708,000

*Interest expense ……………………………………………………… $ 320,000

(b) If the convertible security were preference shares, basic EPS would be

the same assuming there were no preference dividends declared and the

EXERCISE 16.26 (10–15 minutes)

(a) Net income ……………………………………………………………….. €240,000

Add: Interest savings (net of tax)

EXERCISE 16.26 (Continued)

(b) Shares outstanding ……………………………………………………….. 100,000

Add: Shares assumed to be issued (10,000* X 5) …………….. 50,000

EXERCISE 16.27 (20–25 minutes)

(a) Diluted

Shares assumed issued on exercise ……………………………….. 1,000

(b) Diluted

Shares assumed issued on exercise ……………………………….. 1,000

Proceeds = £8,000

EXERCISE 16.28 (10–15 minutes)

(a) The contingent shares would have to be reflected in diluted earnings

EXERCISE 16.29 (15–20 minutes)

(a) Diluted

The warrants are dilutive because the option price

(€10) is less than the average market price (€15).

(b) Basic EPS = €2.60

(€260,000 ÷ 100,000 shares)

*EXERCISE 16.30 (15–25 Minutes)

(a) Schedule of Compensation Expense Share Appreciation Rights

Cumulative

16–32 Copyright © 2018 Wiley Kieso, IFRS, 3/e, Solutions Manual (For Instructor Use Only)

*EXERCISE 16.31 (15–25 Minutes)

2022

Compensation Expense ………………………………………………….. 400,000

Liability Under Share-Appreciation Plan ……………………. 400,000

LO: 6, Bloom: AP, Difficulty: Moderate, Time: 15-25, AACSB: Analytic, AICPA BB: Critical Thinking, AICPA FC: Reporting, AICPA PC: Problem Solving

Copyright © 2018 Wiley Kieso, IFRS, 3/e, Solutions Manual (For Instructor Use Only) 16–33

TIME AND PURPOSE OF PROBLEMS

Problem 16.1 (Time 35–40 minutes)

Purpose—to provide the student with an opportunity to prepare entries to properly account for a series

of transactions involving the issuance and exercise of ordinary share rights and detachable share

Problem 16.2 (Time 30–35 minutes)

Purpose—to provide the student with an understanding of the entries to properly account for a share-

Problem 16.3 (Time 25–30 minutes)

Purpose—to provide the student with an understanding of the entries to properly account for a share

option and restricted share plan. The student is asked to identify the important features of an employee

share-purchase plan.

Problem 16.4 (Time 30–35 minutes)

Problem 16.5 (Time 30–35 minutes)

Purpose—to provide the student with an understanding of the proper computation of the weighted–

Problem 16.6 (Time 35–45 minutes)

Purpose—to provide the student with an opportunity to calculate the number of shares used to compute

basic and diluted earnings per share which is complicated by a share dividend, a share split, and

Problem 16.7 (Time 25–35 minutes)

Purpose—to provide the student with a problem with multiple dilutive securities which must be analyzed

to compute basic and diluted EPS.

Problem 16.8 (Time 30–40 minutes)

Purpose—to provide the student with an opportunity to calculate the weighted-average number of

SOLUTIONS TO PROBLEMS

PROBLEM 16.1

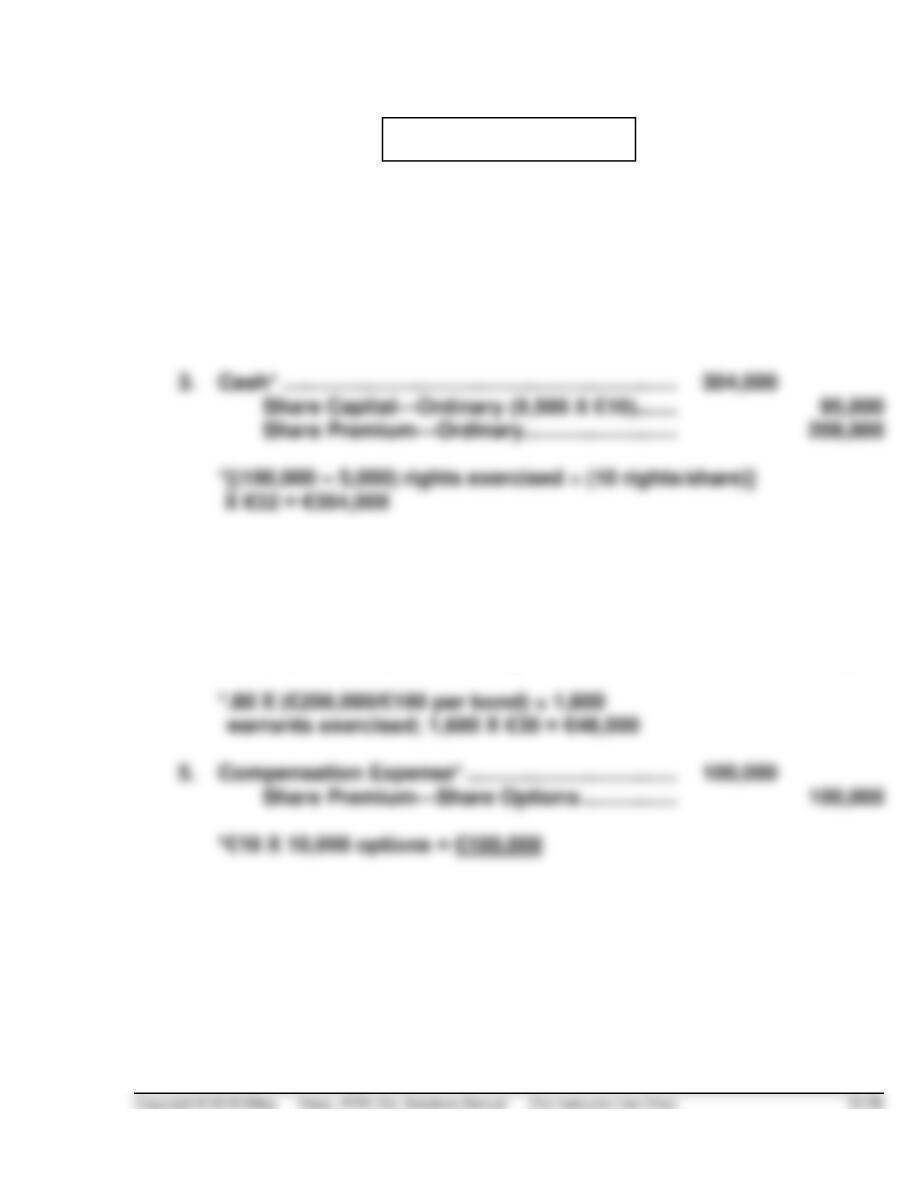

(a) 1. Memorandum entry made to indicate the number of rights issued.

2. Cash …………………………………………………………… 208,000

Bonds Payable …………………………………….. 192,000

Share Premium—Share Warrants ………….. 16,000

4. Share Premium—Share Warrants

(€16,000 X 80%) ………………………………………. 12,800

Cash* …………………………………………………………. 48,000

Share Capital—Ordinary (1,600 X €10)……. 16,000

Share Premium—Ordinary …………………….. 44,800

PROBLEM 16.1 (Continued)

6. For options exercised:

Cash (9,000 X €30)………………………………………. 270,000

Share Premium—Share Options

(90% X €100,000) …………………………………….. 90,000

Share Capital—Ordinary (9,000 X €10) …… 90,000

(b) Equity:

Share Capital—Ordinary €10 par value, authorized

1,000,000 shares, 320,100 shares

issued and outstanding …………………………... €3,201,000

Share Premium—Ordinary …………………………. 1,123,800

PROBLEM 16.2

2018 No journal entry would be recorded at the time the share option

2019 January 2

No entry

December 31

Compensation Expense ……………………………… 88,000

2020 December 31

Compensation Expense ……………………………… 80,000

Share Premium—Share Options …………… 80,000

2021 December 31

Cash (20,000 X $9) ……………………………………… 180,000

Share Premium—Share Options

PROBLEM 16.3

(a) 1/1/19 No entry

12/31/19 Compensation Expense (R$6 X 5,000 ÷ 5) …. 6,000

Share Premium—Share Options ……….. 6,000

(c) No change for part (a), unless the fair value of the options change.

For part (b):

1/1/19 Unearned Compensation (R$45 X 700) …….. 31,500

(d) Employee share-purchase plans generally permit all employees to pur–

chase shares at a discounted price. When employees purchase the

PROBLEM 16.4

The computation of Fitzgerald Pharmaceutical Industries’ basic earnings

per share and the diluted earnings per share for the fiscal year ended

June 30, 2019, are shown below.

(a)

Basic earnings per share

=

Net income – Preference dividends

Average ordinary shares outstanding

=

(b)

Diluted earnings per share

=

Net income – Preference dividends +

Interest (net of tax)

Average ordinary shares + Potentially

dilutive ordinary shares

=

PROBLEM 16.4 (Continued)

4Use treasury-share method to determine incremental

shares outstanding