PROBLEM 6.3

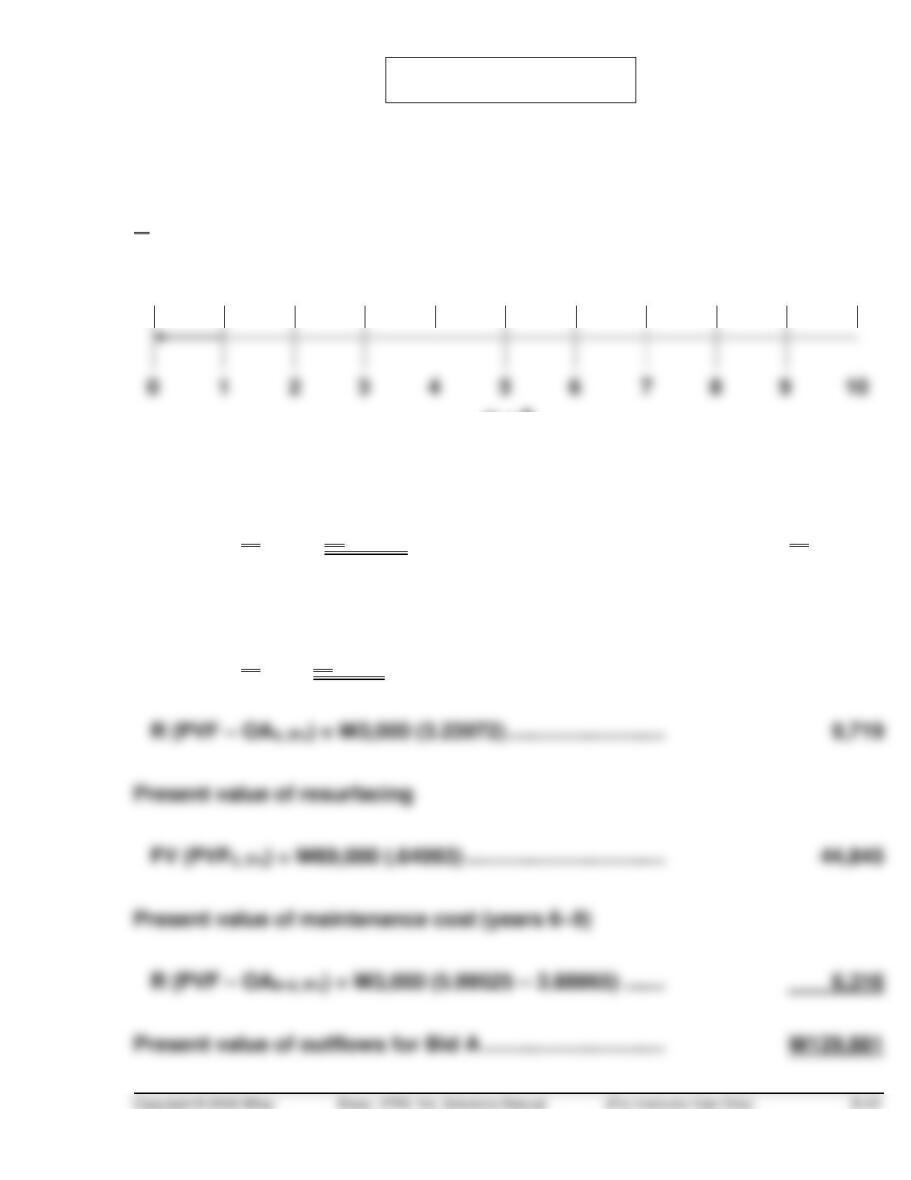

Time diagram (Bid A):

i = 9%

W69,000

PV – OA = R =

? 3,000 3,000 3,000 3,000 69,000 3,000 3,000 3,000 3,000 0

n = 9

Present value of initial cost

12,000 X W5.75 = W69,000 (incurred today) ……………

W 69,000

Present value of maintenance cost (years 1–4)

12,000 X W.25 = W3,000

R (PVF – OA4, 9%) = W3,000 (3.23972) ………………………

Present value of resurfacing

Present value of maintenance cost (years 6–9)

R (PVF – OA9–5, 9%) = W3,000 (5.99525 – 3.88965) …….

PROBLEM 6.3 (Continued)

Time diagram (Bid B):

i = 9%

W126,000

PV – OA = R =

? 1,080 1,080 1,080 1,080 1,080 1,080 1,080 1,080 1,080 0

Present value of initial cost

12,000 X W10.50 = W126,000 (incurred today) …….

W126,000.00

Present value of maintenance cost

12,000 X W.09 = W1,080

R (PV – OA9, 9%) = W1,080 (5.99525) ……………………

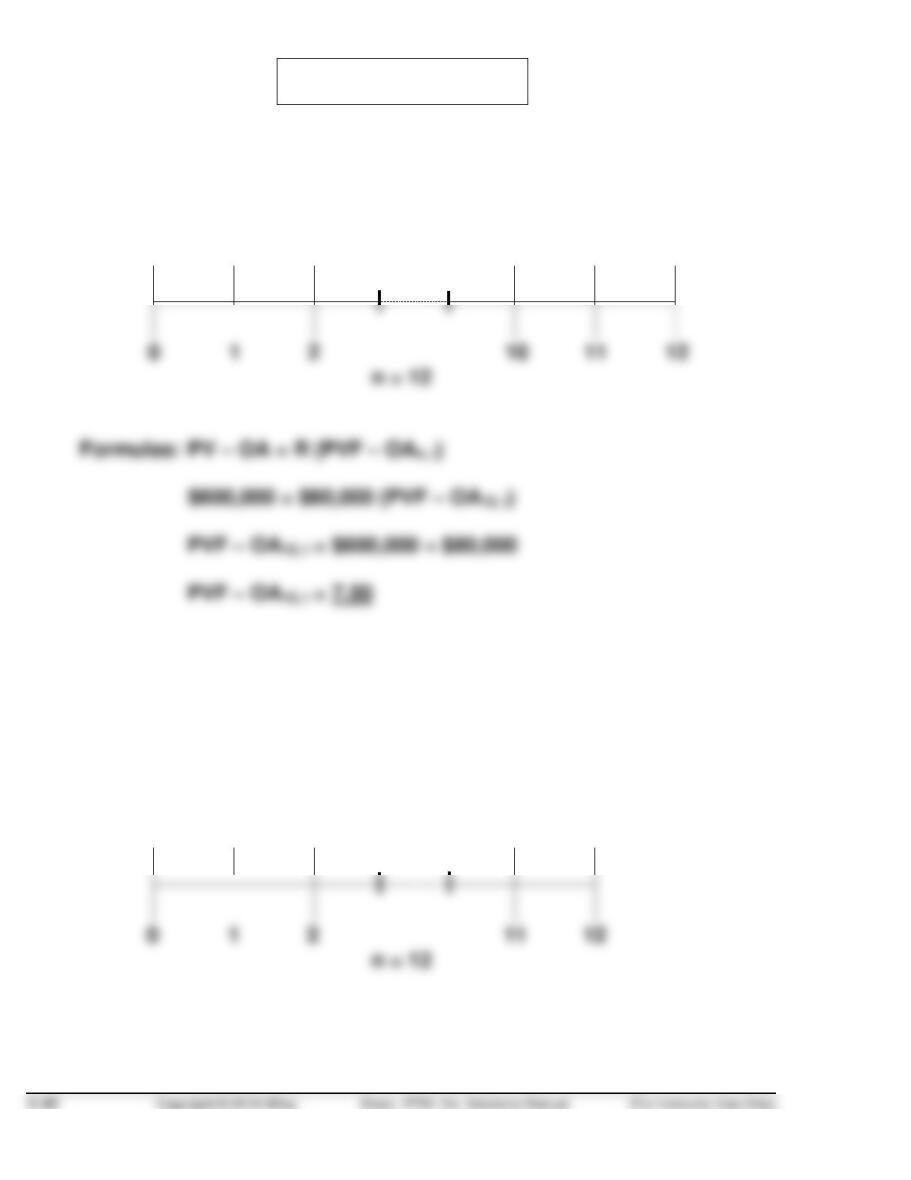

PROBLEM 6.4

Lump sum alternative: Present Value = $500,000 X (1 – .46) = $270,000.

Annuity alternative: Payments = $36,000 X (1 – .25) = $27,000.

PROBLEM 6.5

(a) The present value of €55,000 cash paid today is €55,000.

(b) Time diagram:

i = 21/2% per quarter

PV – OA = €62,357

(c) Time diagram:

i = 21/2% per quarter

€18,000

PV – AD =

PROBLEM 6.5 (Continued)

Formula: PV – AD = R (PVF – ADn, i)

(d) Time diagram:

i = 21/2% per quarter

PV – OA = R =

? €1,500 €1,500 €1,500 €1,500

PV – OA = R =

? €4,000 €4,000 €4,000

0 1 11 12 13 14 36 37

PROBLEM 6.5 (Continued)

Present values:

(a) €55,000.

Time diagram:

i = 12%

PV – OA = ? R =

(€39,000) (€39,000) €18,000 €18,000 €68,000 €68,000 €68,000 €68,000 €38,000 €38,000 €38,000

€12,000)

€12,000)

€12,000)

Formulas:

PV – OA = R (PVF – OAn, i)

PV – OA = R (PVF – OAn, i)

PV – OA = R (PVF – OAn, i)

PV – OA =R (PVF – OAn, i)

PV – OA = (€39,000)(PVF – OA5, 12%)

PV – OA = €18,000 (PVF – OA10–5, 12%)

PV – OA = €68,000 (PVF – OA30–10, 12%)

PV – OA = €38,000 (PVF – OA40–30, 12%)

PV – OA = (€39,000)(3.60478)

PV – OA = €18,000 (5.65022 – 3.60478)

PV – OA = €68,000 (8.05518 – 5.65022)

PV – OA = €38,000 (8.24378 – 8.05518)

PV – OA = (€140,586)

PV – OA = €18,000 (2.04544)

PV – OA = €68,000 (2.40496)

PV – OA = €38,000 (.18860)

PV – OA = €36,818

PV – OA = €163,537

PV – OA = €7,167

Present value of future net cash inflows:

€(140,586)

36,818

Copyright © 2018 Wiley Kieso, IFRS, 3/e, Solutions Manual (For Instructor Use Only) 6-47

PROBLEM 6.7

(a) Time diagram (alternative one):

i = ?

PV – OA =

$600,000 R =

$80,000 $80,000 $80,000 $80,000 $80,000

7.50 is the present value of an annuity factor of $1 for 12 years

discounted at an interest rate of approximately 8%.

Time diagram (alternative two):

i = ?

PV = $600,000 FV = $1,900,000

PROBLEM 6.7 (Continued)

Future value approach

Present value approach

FV = PV (FVFn, i)

PV = FV (PVFn, i)

$1,900,000 = $600,000 (FVF12, i)

$600,000 = $1,900,000 (PVF12, i)

(b) Time diagram:

i = ?

($824,150 – $200,000)

PV – OA = R =

$624,150 $76,952 $76,952 $76,952 $76,952

PROBLEM 6.7 (Continued)

Formulas: PV – OA = R (PVF – OAn, i)

(c) Time diagram:

i = 5% per six months (10% ÷ 5)

PV = ?

PV – OA = R =

? $32,000 $32,000 $32,000 $32,000 $32,000 ($800,000 X 8% X 6/12)

PROBLEM 6.7 (Continued)

(d) Time diagram (future value of $200,000 deposit)

i = 21/2% per quarter (10% ÷ 4)

PV =

$200,000 FV = ?

Amount to which quarterly deposits must grow:

$1,300,000 – $537,012 = $762,988.

Time diagram (future value of quarterly deposits)

PROBLEM 6.7 (Continued)

Formulas: FV – OA = R (FVF – OAn, i)

PROBLEM 6.8

Vendor A:

£18,000

Annual Payment

X 6.14457

(PV of ordinary annuity 10%, 10 periods)

£110,602

+ 55,000

down payment

+ 10,000

maintenance contract

£175,602

total cost from Vendor A

Vendor B:

£9,500

semiannual payment

X 18.01704

(PV of annuity due *5%, **40 periods)

£171,162

*(10 ÷ 2) **(20 periods x 2)

Vendor C:

£1,000

X 3.79079

(PV of ordinary annuity of 5 periods, 10%)

£ 3,791

PV of first 5 years of maintenance

£2,000

[PV of ordinary annuity 15 per., 10% (7.60608) –

X 3.81529

PV of ordinary annuity 5 per., 10% (3.79079)]

£3,000

[(PV of ordinary annuity 20 per., 10% (8.51356) –

X .90748

PV of ordinary annuity 15 per., 10% (7.60608)]

£ 2,722

PV of last 5 years of maintenance

Total cost of press and maintenance Vendor C:

£150,000.00

cash purchase price

3,791

maintenance years 1–5

7,631

maintenance years 6–15

2,722

£164,144

PROBLEM 6.9

(a) Time diagram for the first ten payments:

i = 10%

PV–AD = ?

R =

$800,000 $800,000 $800,000 $800,000 $800,000 $800,000 $800,000

Formula for the first ten payments:

PV – AD = R (PVF – ADn, i)

Formula for the last ten payments:

PV – AD = R (PVF – ADn, i)

Note: The present value of an annuity due is used here, not the

present value of an ordinary annuity, although it may be used.

PROBLEM 6.9 (Continued)

The total cost for leasing the facilities is:

$5,407,216 + $1,042,360 = $6,449,576.

Formulas for the last ten payments:

(i) Present value of the last ten payments:

PV – A = R (PVF – ADn, i)

PROBLEM 6.9 (Continued)

(ii) Present value of the last ten payments at the beginning of current

year:

PV = FV (PVFn, i)

(b) Time diagram:

i = 11%

PV – OA = ?

R =

$15,000 $15,000 $15,000 $15,000 $15,000 $15,000 $15,000

PROBLEM 6.9 (Continued)

Formula: PV – OA = R (PVF – OAn, i)

(c) Time diagram:

Amount paid =

$792,000

If the company decides not to take the cash discount, then the company

can use the $792,000 for an additional 20 days. The implied interest

rate for postponing the payment can be calculated as follows:

(i) Implied interest for the period from the end of discount period to

the due date:

PROBLEM 6.9 (Continued)

(ii) Convert the implied interest rate to annual basis:

Daily interest = 0.010101/20 = 0.000505