BRIEF EXERCISE 21.22 (Continued)

Lease liability: $22,156

Legal fees: 1,000

Right-of–use asset: $23,156

BRIEF EXERCISE 21.23

Answer: $78,998

PV of lease payments: $83,498

Cash incentive received from Badger (lessor): (5,000)

BRIEF EXERCISE 21.24

Answer: €46,551

PV of lease payments: €44,651

Cash incentive received from Highlander (lessor): (2,000)

Internal engineering costs are specifically excluded as initial direct costs, and

would not be included in the calculation of the right-of-use asset.

BRIEF EXERCISE 21.25

Lease Expense ……………………………………………………… 15,000

Cash ……………………………………………………………… 15,000

*BRIEF EXERCISE 21.26

The transaction between Irwin and Peete will qualify as a sale-leaseback, as Irwin

has transferred control of the asset to Peete. That is, the terms of the leaseback

BRIEF EXERCISE 21.26 (Continued)

1/1/19

Cash …………………………………………………………………….. 35,000

Trucks …………………………………………………………… 28,000

Gain on Disposal of Plant Assets ……………………. 7,000

IRWIN ANIMATION

Lease Amortization Schedule

Ordinary-Annuity Basis

Date

Annual

Payment

Interest (6%) on

Liability

Reduction

of Lease

Liability

Lease Liability

1/1/19

€23,245

*Rounded $1

12/31/19

Interest Expense …………………………………………………… 1,395

Lease Liability ……………………………………………….. 1,395

*BRIEF EXERCISE 21.27

With the change of facts, the leaseback meets the lease term and present value

classification tests (5/5 = 100% of asset’s economic life; €8,309 x 4.21236 =

1/1/19

Cash …………………………………………………………………….. 35,000

Notes Payable [€8,309 X 4.21236*] …………………… 35,000

SOLUTIONS TO EXERCISES

EXERCISE 21.1 (15–20 minutes)

Note to Instructor: The lease term is 100% of the asset’s economic life, and the

present value of the rental payments are 100% of the asset’s fair value, as shown

below:

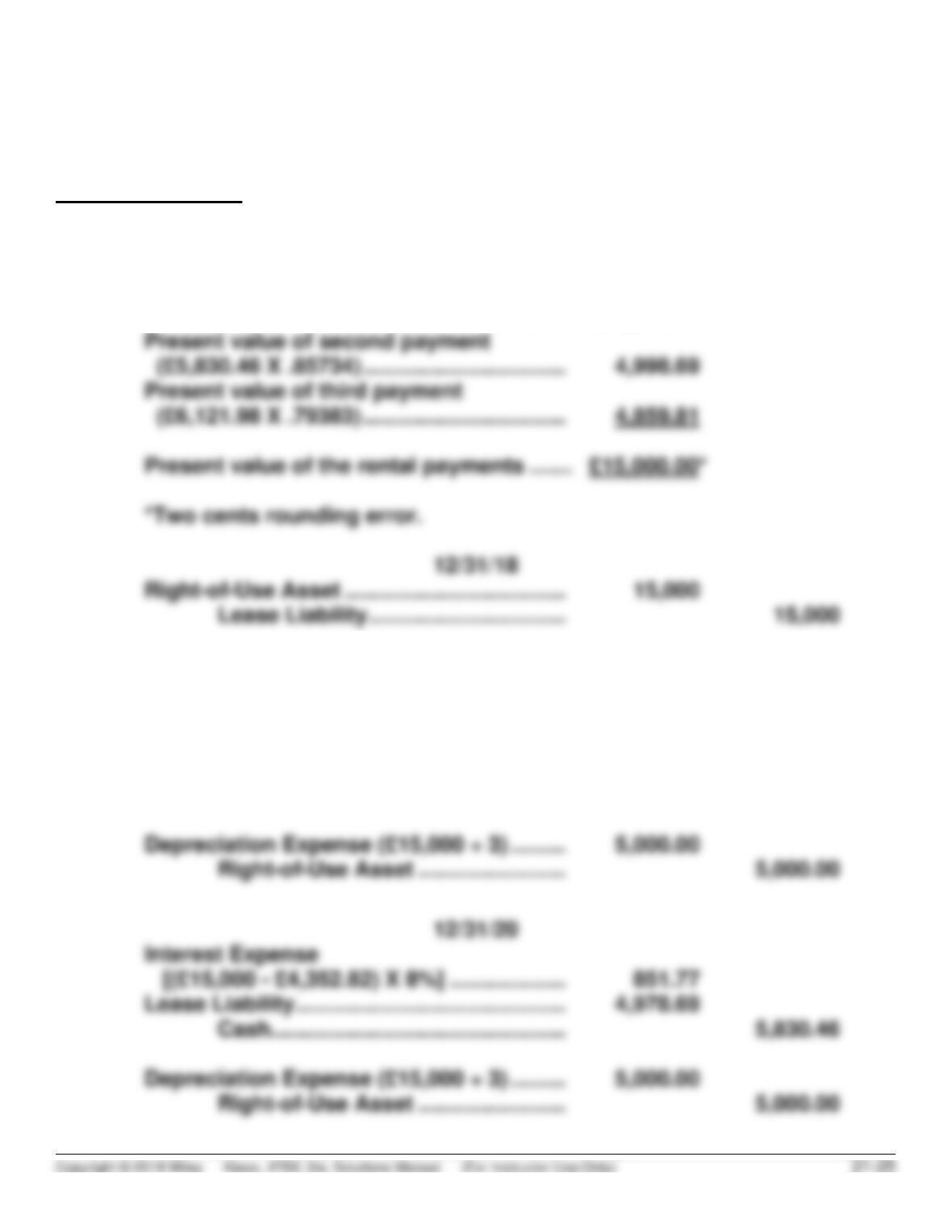

Present value of first payment

(£5,552.82 X .92593) …………………………... £ 5,141.52

12/31/19

Interest Expense (£15,000 X 8%) ………….. 1,200.00

Lease Liability …………………………………….. 4,352.82

Cash………………………………………… 5,552.82

EXERCISE 21.1 (Continued)

(b) The initial valuation of the lease liability and related right-of-use asset should

not include any unknown increases or decreases in lease payments due to

EXERCISE 21.2 (15–20 minutes)

(a) Computation of present value of lease payments:

$8,668 X 4.54595* = $39,404

*Present value of an annuity-due of 1 for 5 periods at 5%.

EXERCISE 21.3 (20–25 minutes)

(a) The present value of lease payments, for purposes of determining the lease

liability for the lessee, should only include the present value of any

guaranteed residual value probable to be owed under the lease agreement

(i.e. the amount of guaranteed residual value over the expected residual

(b) Right-of–Use Asset ……………………………………………. 8,873

Lease Liability …………………………………………….. 8,873

(c) Lease Liability ………………………………………………….. 200

Cash …………………………..……………………………… 200

(f) As explained in part (a), the lessee should include the present value of any

guaranteed residual value probable to be owed under the lease agreement.

Because the expected residual value (€500) is less than the guaranteed residual

value (€1,180), Delaney should include the present value of the difference in the

initial measurement of the lease liability. Thus, the present value of the lease

payments is calculated as follows:

EXERCISE 21.4 (20–30 minutes)

(a) For purposes of calculating the initial lease liability, the present value of the

lease payments will only include the amount of a residual value guarantee

probable to be owed at the end of the lease term. Thus, the initial lease liability

and right-of-use asset to be recorded on the books of Stora Enso is calculated

as follows:

€ 71,830 Annual rental payment

EXERCISE 21.4 (Continued)

12/31/18

Right-of–Use Asset …………………………. 521,934

Lease Liability ……………………… 521,934

Lease Liability ………………………………… 35,822

Interest Expense

(See Schedule 1) …………………………... 36,008

Cash……………………………………. 71,830

12/31/20

EXERCISE 21.4 (Continued)

Schedule 1 Stora Enso

Lease Amortization Schedule (partial)

(Lessee)

Date

Annual Lease

Payment

Interest (8%) on

Liability

Reduction

of Lease

Liability

Lease Liability

12/31/18

€521,934

12/31/19

(b) Initial direct costs and lease incentives do not affect the initial measurement

of the lease liability. Instead, they only affect the measurement of the right–of-use

asset. Initial direct costs incurred by the lessee increase the right-of–use asset,

(c) The annual insurance payments of €5,000 are considered part of the annual

payments to the lessor similar to the rental payments, as they do not transfer a

separate good or service to the lessee, but rather are part of the payment to use

EXERCISE 21.4 (Continued)

€ 3,000 Amount probable to be owed under

residual value guarantee (€10,000 – €7,000)

Note how the inclusion of the executory costs leads to an inflated lease liability

and related right-of–use asset. Additionally, note that had the insurance

payments been variable, they would not have been included at all in the

measurement of the lease liability, which would have led to a very different initial

measurement of the liability and asset.

(d) Because Stora Enso expected the residual value of the asset at the end of the

lease to be €7,000, it expected to owe Sheffield an additional €3,000 in addition to

EXERCISE 21.5 (15–25 minutes)

(a) Fair value of leased asset to lessor £245,000

Less: Present value of unguaranteed

residual value £24,335 X .63017

EXERCISE 21.5 (Continued)

(b) MORGAN LEASING GROUP (Lessor)

Lease Amortization Schedule

Date

Annual

Lease

Payment

Plus URV

Interest (8%) on

Lease

Receivable

Recovery

of Lease

Receivable

Lease

Receivable

1/1/19

£245,000

1/1/19

£ 46,000

£ –0–

£ 46,000

199,000

1/1/20

46,000

15,920

30,080

168,920

1/1/22

46,000

46,000

40,923

12/31/24

*Rounded by £2.

1/1/19

(c) Lease Receivable …………………………... 245,000*

Cost of Goods Sold 229,665**

Sales Revenue ………………………… 229,665***

Inventory ………………………………… 245,000

*The lease receivable will include both the present value of the

rental payments (£46,000 X 4.99271) plus the present value of the

EXERCISE 21.5 (Continued)

1/1/19

Cash ……………………………………………………….. 46,000

Lease Receivable …………………………….. 46,000

12/31/19

EXERCISE 21.6 (20–25 minutes)

Computation of annual payments

Fair value of leased asset to lessor $160,000

Less: Present value of residual value

($16,000 X .90703*) 14,512

Amount to be recovered through lease payments $145,488

EXERCISE 21.6 (Continued)

CASTLE LEASING COMPANY (Lessor)

Lease Amortization Schedule

Date

Annual Lease

Payment

Interest (5%)

on Lease

Receivable

Recovery

of Lease

Receivable

Lease

Receivable

1/1/19

$160,000

12/31/19

1/1/19

(a) Lease Receivable ………………… 160,000*

12/31/19

Cash…………………………………… 78,244

Lease Receivable ………….. 70,244

Interest Revenue …………… 8,000

(b) Cash…………………………………… 16,000

Lease Receivable ………….. 16,000

EXERCISE 21.7 (15–20 minutes)

(a) The lessee accounts for all leases using the finance lease method and

records the right-of–use asset and lease liability at the present value of the

lease payments using the incremental borrowing rate if it is impracticable to

determine the interest rate implicit in the lease. The lessee’s amortization

The lessor should account for the lease as a sales-type lease. Because title

to the asset passes to the lessee, the lease term is longer than 75% of the

economic life of the asset (3/3 = 100%), and the present value of the lease

payments is more than 90% of the fair value of the asset (€95,000/€95,000 =

100%), it is a finance (sales-type) lease by the lessor. Assuming collectibility

of the rents is probable, the lease is accounted for as a sales-type lease to

the lessor.

Fair value of leased asset

(Amount to be recovered by lessor through lease

payments) …………………………..…………………………………….. €95,000

EXERCISE 21.7 (Continued)

(b) Amortization Schedule

Rent Receipt/

Payment

Interest (8%)

Revenue/

Expense

Reduction of

Principal

Receivable/

Liability

1/1/19

—

—

—

€95,000

12/31/19

€36,863

€7,600*

€29,263

65,737

(c) 1/1/19

Lease Receivable ……………………………. 95,000

(d) 1/1/19

Right-of–Use Asset …………………………. 95,000

Lease Liability ……………………… 95,000

(e) 1/1/19

EXERCISE 21.8 (15–20 minutes)

(b) Because the lease term test is met (8/10 = 80% > 75%), the lease is classified

as a sales-type lease.

1/1/19

Lease Receivable …………………………. 230,410

(c) If the collectibility of lease payments is not probable for the lessor, the

lessor does not derecognize the asset or recognize selling profit on the lease.

Instead, Crosley would recognize any cash receipts as a deposit liability.

1/1/19

Cash …………………………………………………………………….. 35,004

Deposit Liability ……………………………………………… 35,004

EXERCISE 21.9 (20-25 minutes)

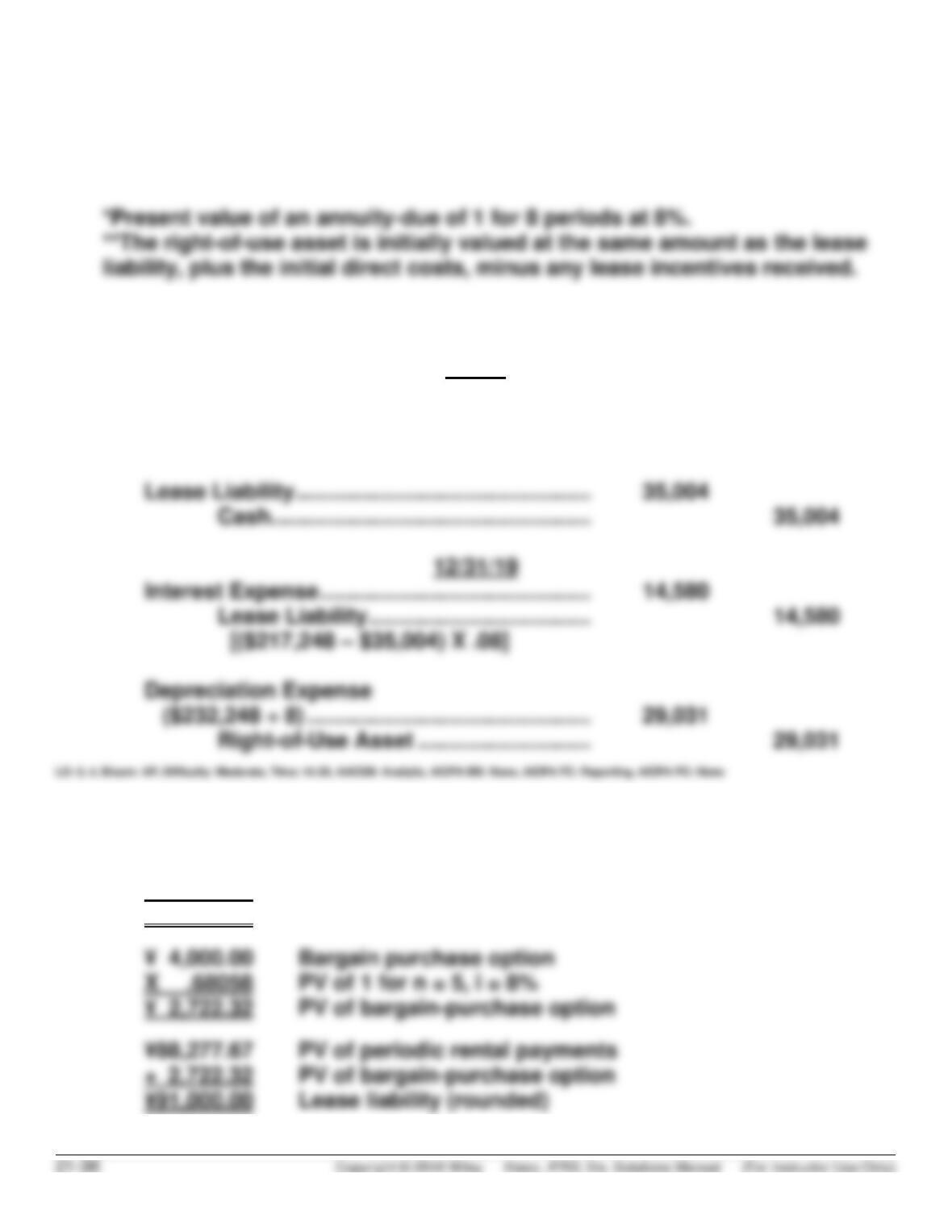

(a) Lease Liability = $35,004 x 6.20637* = $217,248

Right-of–Use Asset = $217,248 + $15,000** = $232,248

(b) The lease is accounted for using the finance lease method.

1/1/19

Right-of–Use Asset …………………………. 232,248

Cash……………………………………. 15,000

Lease Liability ……………………… 217,248

EXERCISE 21.10 (20–30 minutes)

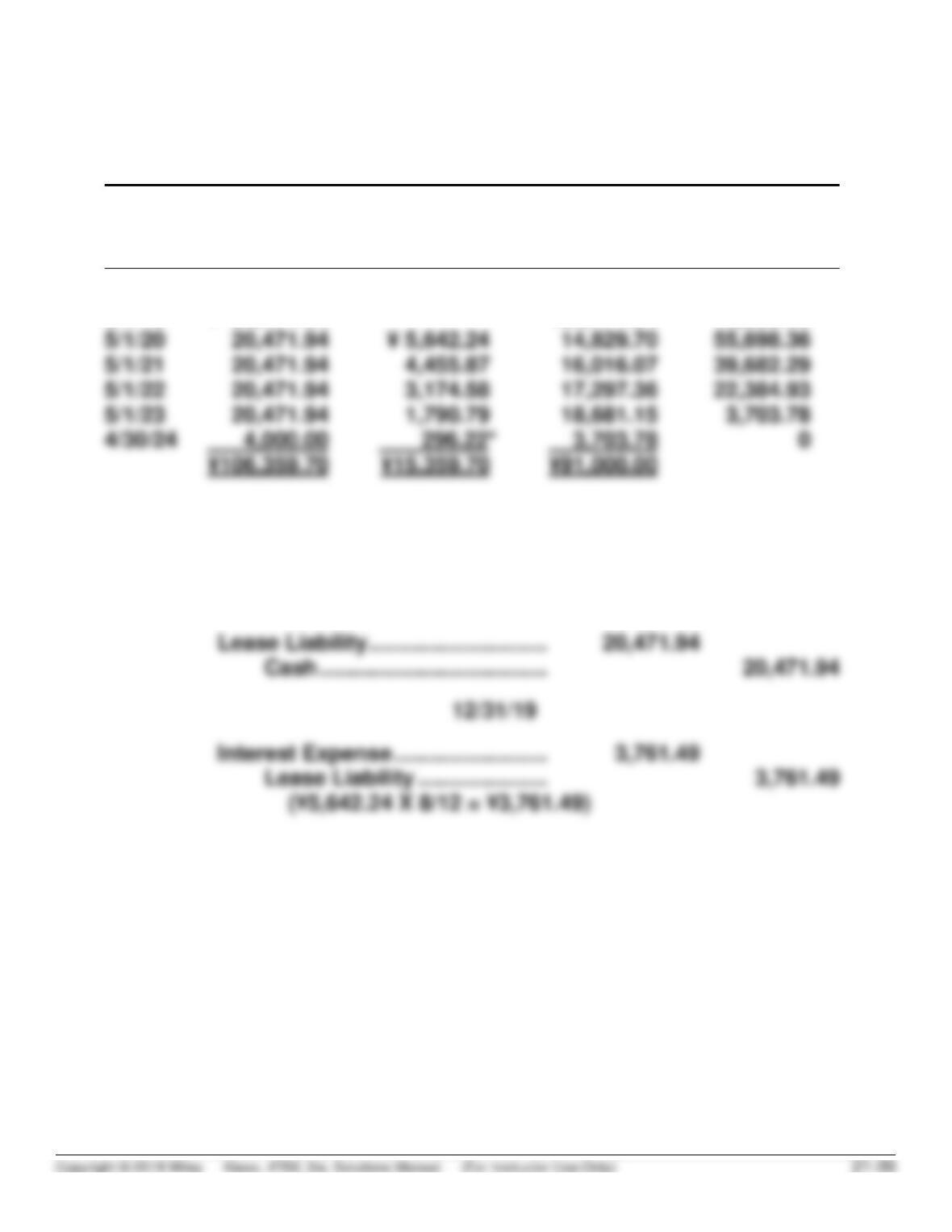

(a) Computation of lease liability:

¥20,471.94 Annual rental payment

X 4.31213 PV of annuity-due of 1 for n = 5, i = 8%

¥88,277.67 PV of periodic rental payments

EXERCISE 21.10 (Continued)

Choi Group (Lessee)

Lease Amortization Schedule

Date

Annual Lease

Payment Plus

BPO

Interest

(8%) on

Liability

Reduction

of Lease

Liability

Lease

Liability

5/1/19

¥91,000.00

5/1/19

¥ 20,471.94

¥20,471.94

70,528.06

5/1/22

5/1/23

4/30/24

3,703.78

¥91,000.00

*Rounding error is 8 Yen.

5/1/19

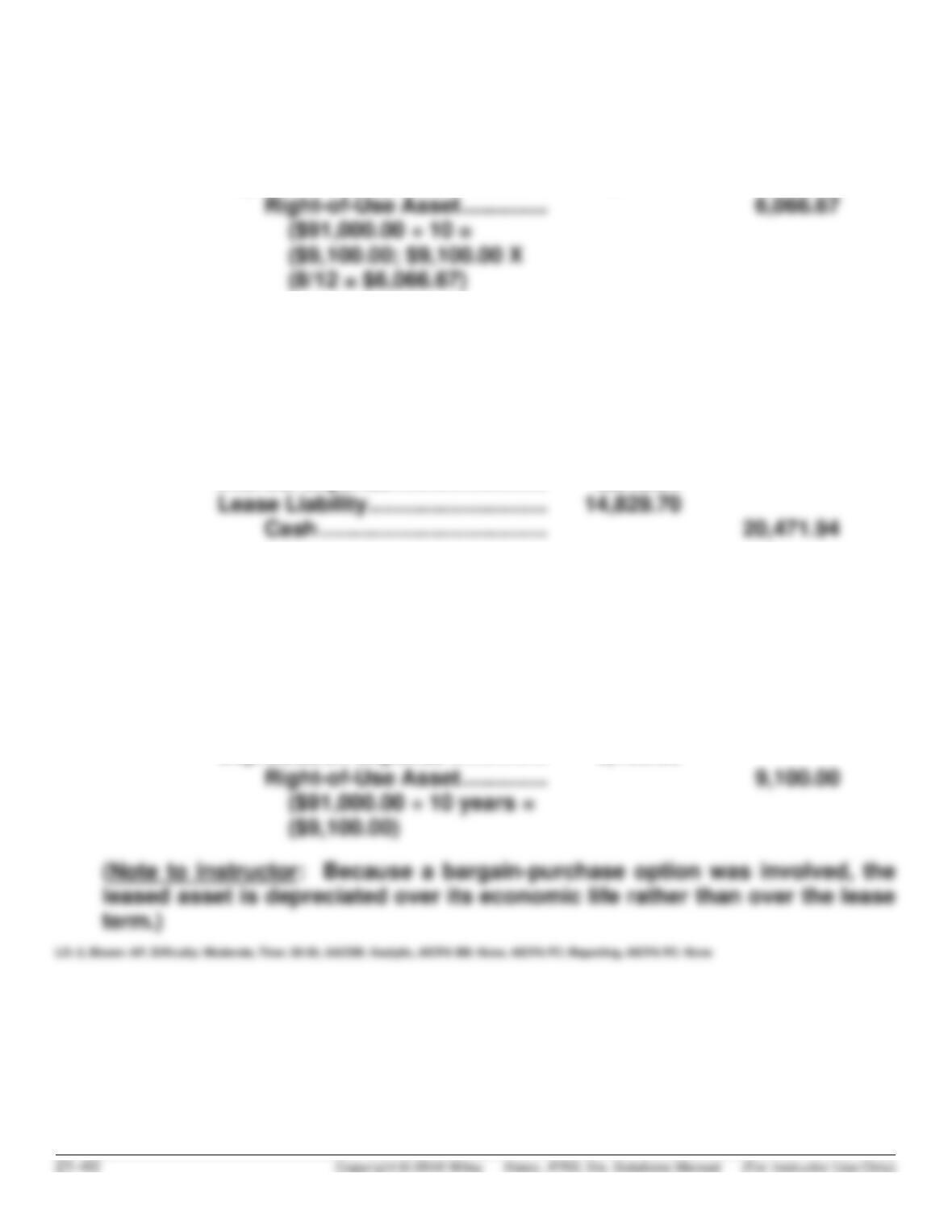

(b) Right-of-Use Asset ………………… 91,000.00

Lease Liability ………………… 91,000.00

EXERCISE 21.10 (Continued)

12/31/19

Depreciation Expense ……………. 6,066.67

1/1/20

Lease Liability ……………………….. 3,761.49

Interest Expense …………….. 3,761.49

5/1/20

Interest Expense ……………………. 5,642.24

12/31/20

Depreciation Expense ……………. 2,970.58

Lease Liability ………………… 2,970.58

($4,455.87 X 8/12)

12/31/20

Depreciation Expense ……………. 9,100.00