EXERCISE 18.27 (15–20 minutes)

(a) October 1, 2019

To record sales revenue, warranties, and related cost of goods sold

Cash (or Accounts Receivable) ………………………….. 3,600

(b) Celic recognizes warranty expenses associated with the assurance-

type warranty as actual warranty costs are incurred during the first 90

EXERCISE 18.28 (10–15 minutes)

(a) No entry – neither party has performed on the contract on January 1,

2019.

(b) The entries to record the sale and related cost of goods sold of the

wiring base is as follows.

February 5, 2019

EXERCISE 18.28 (continued)

(c) The entries to record the sale and related cost of goods sold of the

shelving unit is as follows.

February 25, 2019

Cash …………………………..……………………………………. 3,000

EXERCISE 18.29 (20–25 minutes)

(a) Cash …………………………..………………………….. 9,000

Sales Revenue (90 X $100) ……………….. 9,000

(b) Cash …………………………..………………………….. 1,000

Sales Revenue (10 X $100) ……………….. 1,000

(c) In this case, because the new price does not reflect a stand-alone

EXERCISE 18.29 (continued)

Under the prospective approach, Gaertner determines the transaction

price for subsequent sales ($97.86) as follows.

Consideration for products not yet delivered

under original contract ($100 X 60) $ 6,000

EXERCISE 18.30 (20–25 minutes)

(a) January 1, 2019

Cash ……………………………………………………….. 10,000

EXERCISE 18.30 (continued)

January 1, 2020

Cash …………………………..………………………….. 10,000

(b) January 1, 2021

Cash ($8,000 + $20,000) …………………………... 28,000

In this case, the modification of the contract does not result in a new

performance obligation. As a result, the remaining service revenue is

recognized evenly over the remaining four years.

(c) Given the change in services in the extended contract period, the

EXERCISE 18.30 (continued)

December 31, 2021

Unearned Service Revenue ………………………. 8,000

EXERCISE 18.31 (10–15 minutes)

(a) The €2,000 commission costs related to obtaining the contract are

recognized as an asset. The design services (€3,000), controllers

(b) Companies only capitalize costs that are direct, incremental, and

recoverable (assuming that the contract period is more than one year.

EXERCISE 18.32 (20–25 minutes)

(a) If the contract is for 1 year or less, Rex can use the practical expedient

and recognize the incremental costs of obtaining a contract as an

expense when incurred.

(b) The collectibility of the contract payments will not affect the amount of

revenue recognized. That is, the amount recognized is not adjusted for

customer credit risk. Rather, Rex should report the revenue gross and

*EXERCISE 18.33 (20–25 minutes)

(a) Gross profit recognized in:

2019

2020

2021

Contract price

$1,600,000

$1,600,000

$1,600,000

Costs:

Costs to date

$400,000

$825,000

$1,070,000

Estimated costs to

complete

600,000

1,000,000

275,000

1,100,000

0

1,070,000

Total estimated profit

500,000

530,000

to date

X 75%**

X 100%

recognized

375,000

530,000

years

*EXERCISE 18.33 (continued)

(b)

2020

Construction in Process ($825,000 – $400,000) …. 425,000

Materials, Cash, Payables ………………………… 425,000

Construction Expenses …………………………………… 425,000

Construction in Process …………………………………. 135,000

(c) Gross profit recognized in:

*EXERCISE 18.34 (10–15 minutes)

(a) Contract billings to date ………………………………….. €61,500

Less: Accounts receivable 12/31/19 ………………… 18,000

Portion of contract billings collected ……………….. €43,500

*EXERCISE 18.35 (10–15 minutes)

DOUGHERTY INC.

Computation of Gross Profit to be

Recognized on Uncompleted Contract

Year Ended December 31, 2019

Total contract price

Estimated contract cost at completion

LO: 5, Bloom: AP, Difficulty: Moderate, Time: 10–15, AACSB: Analytic, AICPA BB: None, AICPA FC: Reporting, AICPA PC: Problem Solving

*EXERCISE 18.36 (15–20 minutes)

(a)

2019:

$640,000

X $2,200,000 = $880,000

$1,600,000

(b) The amount of revenue recognized in 2020 is $1,560,000 ($2,200,000 –

$640,000).

(c) Using the percentage–of-completion method, the following entries

would be made:

*EXERCISE 18.36 (continued)

Revenue from Long-Term Contracts

*EXERCISE 18.37 (15–25 minutes)

(a) (1) No gross profit to be recognized in 2019 under cost-recovery

method

(b) (1) Contract price ………………………………… $6,000,000

Costs to date ………………………………………… $1,185,800

Estimated costs to complete …………………. 4,204,200

Total ……………………………………………… $5,390,000

(2) Billings (25% X $6,000,000) …………….. $1,500,000

*EXERCISE 18.38 (20–25 minutes)

(a) May 1, 2019

Cash …………………………..……………………………………. 28,000

(b) May 1, 2019

Cash …………………………..……………………………………. 28,000

Notes Receivable ……………………………………………… 42,000

Discount on Notes Receivable

* [$42,000 – (2.48685* X $14,000)]

**Present value factor for 10%, 3-year ordinary annuity.

***($62,816 ÷ 3) X 8/12

(c) May 1, 2019

Cash …………………………..……………………………………. 28,000

Notes Receivable ……………………………………………… 34,816

*EXERCISE 18.38 (continued)

July 1, 2019

Unearned Service Revenue (Training) ………………… 1,200***

Unearned Franchise Revenue ……………………………. 60,416

September 1, 2019

Unearned Service Revenue (Training) ………………… 1,200*

LO: 8, Bloom: AP, Difficulty: Moderate, Time: 20–25, AACSB: Analytic, AICPA BB: None, AICPA FC: Reporting, AICPA PC: Problem Solving

*EXERCISE 18.39 (15–20 minutes)

(a) January 1, 2019

Cash …………………………………………………………………. 10,000

Notes Receivable ………………………………………………. 29,567

April 1, 2019

Unearned Franchise Revenue ……………………………. 39,567

Franchise Revenue …………………………………….. 39,567

*EXERCISE 18.39 (continued)

December 31, 2019

Discount on Notes Receivable …………………………... 3,252*

Interest Revenue ……………………………………….. 3,252

*($40,000 – $10,433) X 11%

(b) January 1, 2019

Cash …………………………..……………………………………. 10,000

Notes Receivable ……………………………………………… 40,000

December 31, 2019

Unearned Service Revenue (Training)………………… 2,700

(c) January 1, 2019

Cash …………………………..……………………………………. 10,000

Notes Receivable ……………………………………………… 40,000

Discount on Notes Receivable ……………………. 10,433

*EXERCISE 18.39 (continued)

December 31, 2019

Unearned Franchise Revenue ……………………………. 7,913**

Franchise Revenue …………………………………….. 7,913

TIME AND PURPOSE OF PROBLEMS

Problem 18.1 (Time 30–35 minutes)

Purpose—to provide the student with an opportunity to determine transaction price, allocate the

transaction price to performance obligations, and account for upfront fees.

Problem 18.2 (Time 20–25 minutes)

Purpose—to provide the student with an opportunity to determine transaction price, allocate the

Problem 18.3 (Time 30–35 minutes)

Purpose—to provide the student with an opportunity to determine transaction price, allocate the

Problem 18.4 (Time 35–40 minutes)

Purpose—to provide the student with an opportunity to determine transaction price, allocate the

Problem 18.5 (Time 35–40 minutes)

Purpose—to provide the student with an opportunity to determine transaction price, allocate the

Problem 18.6 (Time 25–30 minutes)

Problem 18.7 (Time 30–35 minutes)

Purpose—to provide the student with an understanding of the criteria and applications utilized in the

Problem 18.8 (Time 30–35 minutes)

Purpose—to provide the student with an understanding of and an opportunity to determine transaction

price, allocate the transaction price to performance obligations, and account for time value, gift cards,

and discounts.

*Problem 18.9 (Time 30–40 minutes)

*Problem 18.10 (Time 20–25 minutes)

*Problem 18.11 (Time 40–50 minutes)

Purpose—to provide the student with a long-term construction contract problem that requires the

*Problem 18.12 (Time 35–45 minutes)

SOLUTIONS TO PROBLEMS

PROBLEM 18.1

(a) The total revenue of €50,000 (100 contracts X €500) should be allocated

to the two performance obligations based on their relative standalone

selling prices. In this case, the standalone selling price of each tablet

is €250 and the standalone selling price of the internet service is €300.

The total standalone selling price to consider is €550 (€250 + €300) for

each contract. The allocation for each contract is as follows.

January 2, 2019

Cash (€500 X 100) …………………………………………….. 50,000

December 31, 2019

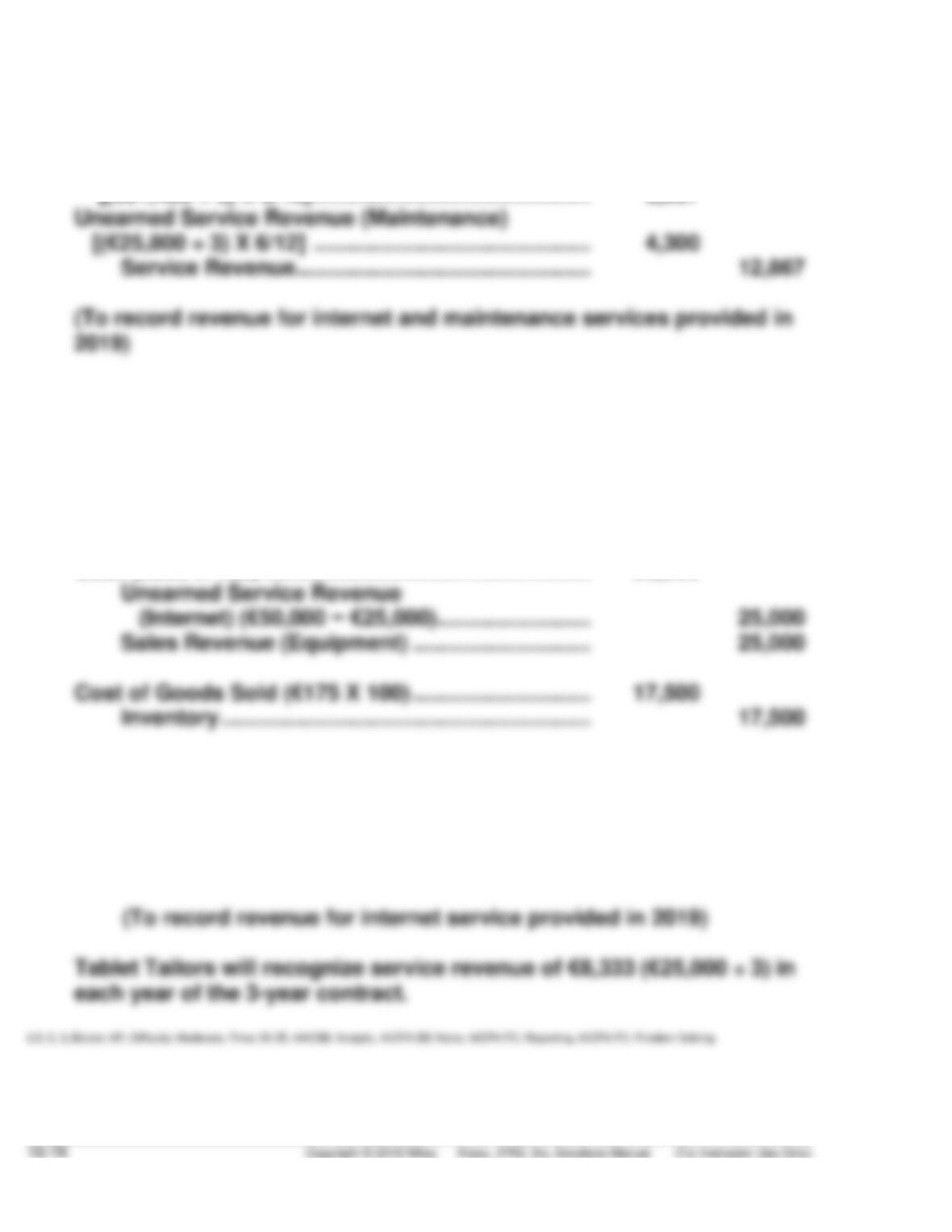

Unearned Service Revenue (€27,300 ÷ 3) ……………. 9,100

Service Revenue………………………………………… 9,100

PROBLEM 18.1 (Continued)

The total revenue of €120,000 (200 contracts X $600) should be allocated to

the three performance obligations based on their relative standalone

selling prices:

Tablet €250

The allocation for a single contract is as follows.

Tablet €214 (€250 / €700) X €600

Tablet Tailors makes the following entries for 200 Tablet Bundle B.

July 1, 2019

Cash (€600 X 200) ……………………………………………… 120,000

Unearned Service Revenue (Internet) …………… 51,400*

The sale of the tablets (and gross profit) should be recognized once the

tablets are delivered on July 1, 2019.

PROBLEM 18.1 (Continued)

December 31, 2019

Unearned Service Revenue (Internet)

[(€51,400 ÷ 3) X 6/12] ……………………………………… 8,567

(c) Without reliable data with which to estimate the standalone selling

price of the internet service Tablet Tailors allocates €250 for each

contract to revenue on the tablets, with the residual amount allocated

to the Internet service. Tablet Tailors makes the following entries.

January 2, 2019

Cash (€500 X 100) …………………………………………….. 50,000

December 31, 2019

Unearned Service Revenue (€25,000 ÷ 3) ……………. 8,333

Service Revenue………………………………………… 8,333

PROBLEM 18.2

Since the services in the extended period are the same as those provided

in the original contract period, the services are not distinct; the

modification should be considered as part of the original contract.

(a)

January 2, 2021

(b)

December 31, 2021

Unearned Service Revenue ………………………………… 2,413

Service Revenue (€7,240* ÷ 3) ……………………… 2,413

PROBLEM 18.3

(a) The total revenue of $8,000 ($800 X 10) should be allocated to the two

performance obligations based on their relative standalone selling

prices. In this case, the standalone selling price of the grills is

Grill Masters makes the following entries.

April 20, 2019

Cash …………………………..……………………………………. 8,000

Unearned Service Revenue (Installation) …….. 1,412

Cost of Goods Sold ………………………………………….. 4,250

Inventory ($425 X 10) …………………………………. 4,250

(b) April 17, 2019

Cash …………………………..……………………………………. 56,000

Unearned Sales Revenue …………………………... 3,360