PROBLEM 20.3

(a) Pension expense for 2019 comprises the following:

Service cost ………………………………………………….. £52,000

Interest on defined benefit obligation

(10% X £380,000) ………………………………………… 38,000

(c) 2019 Increase/Decrease in Gains/Losses

(1) 12/31/19 new actuarially computed

DBO £490,000

Less: Defined benefit obligation

PROBLEM 20.3 (Continued)

(2) 12/31/19 fair value of plan assets £276,000

Less: Expected fair value

1/1/19 fair value of plan

assets £200,000

(d) Financial Statements—2019

Income Statement

Pension expense ……………………………………… £ 70,000

Comprehensive Income Statement

Net Income …………………………………………………….. £ XXXX

20–43 Copyright © 2018 Wiley Kieso, IFRS, 3/e, Solutions Manual (For Instructor Use Only)

PROBLEM 20.3 (Continued)

PROBLEM 20.4

(a) Computation of pension expense:

2019

2020

Service cost ………………………………………………

($60,000

$90,000

Interest revenue ($560,000* X .09) and

Pension expense ……………………………………….

Interest expense ($700,000 X .09)

(b)

2019

Pension Asset/Liability ……………………………….

(39,000

Pension Expense ……………………………………….

72,600

Other Comprehensive Income (G/L) …………….

Cash …………………………………………………….

120,000

General Journal Entries

Memo Record

Annual

Pension

OCI—

Pension

Defined

Benefit

Plan

PROBLEM 20.4 (Continued)

PROBLEM 20.5

(a) Pension expense for 2019 consisted only of the service cost component

amounting to €60,000. There was no net gain or loss, plan assets, or

defined benefit obligation as of January 1, 2019.

Pension expense for 2020 comprised the following:

Pension expense for 2021 comprised the following:

PROBLEM 20.5 (Continued)

(b) Journal Entries—2019

Pension Expense …………………………………………….. 60,000

Cash ………………………………………………………… 50,000

Pension Asset /Liability ……………………………… 10,000

Journal Entries—2020

Service cost

119,000 Dr.

119,000 Cr.

Interest expense

16,000 Dr.

16,000 Cr.

Interest revenue

6,800 Cr.

6,800 Dr.

Contributions

105,000 Cr.

105,000 Dr.

Benefits

18,500 Dr.

18,500 Cr.

Asset gain

1,700 Cr.

1,700 Dr.

Liability loss*

7,500 Dr.

7,500 Cr.

Journal entry for 2021

128,200 Dr.

105,000 Cr.

5,800 Dr.

29,000 Cr.

Accumulated OCI, Dec. 31, 2020

78,900 Dr.

Balance, Dec. 31, 2021

84,700 Dr.

144,000 Cr.

324,000 Cr.

180,000 Dr.

*€324,000 – (€200,000 + €119,000 + €16,000 – €18,500).

LO: 4, Bloom: AP, Difficulty: Complex, Time: 45-55, AACSB: Analytic, AICPA BB: Critical Thinking, AICPA FC: Reporting, AICPA PC: Problem Solving

Expense

Gain/Loss

Asset/Liability

Service cost

60,000 Dr.

60,000 Cr.

Interest expense

Interest revenue

Contributions

50,000 Dr.

Journal entry for 2019

50,000 Cr.

Accumulated OCI, Dec. 31, 2018

Balance, Dec. 31, 2019

60,000 Cr.

50,000 Dr.

Service cost

85,000 Dr.

85,000 Cr.

Interest expense

6,600 Dr.

6,600 Cr.

Interest revenue

5,500 Cr.

5,500 Dr.

Contributions

60,000 Cr.

60,000 Dr.

Asset loss

Liability loss

78,400 Dr.

78,400 Cr.

Benefits

30,000 Dr.

30,000 Cr.

Journal entry for 2020

60,000 Cr.

78,900 Dr.

Accumulated OCI, Dec. 31, 2019

0

Balance, Dec. 31, 2020

78,900 Dr.

200,000 Cr.

85,000 Dr.

PROBLEM 20.6

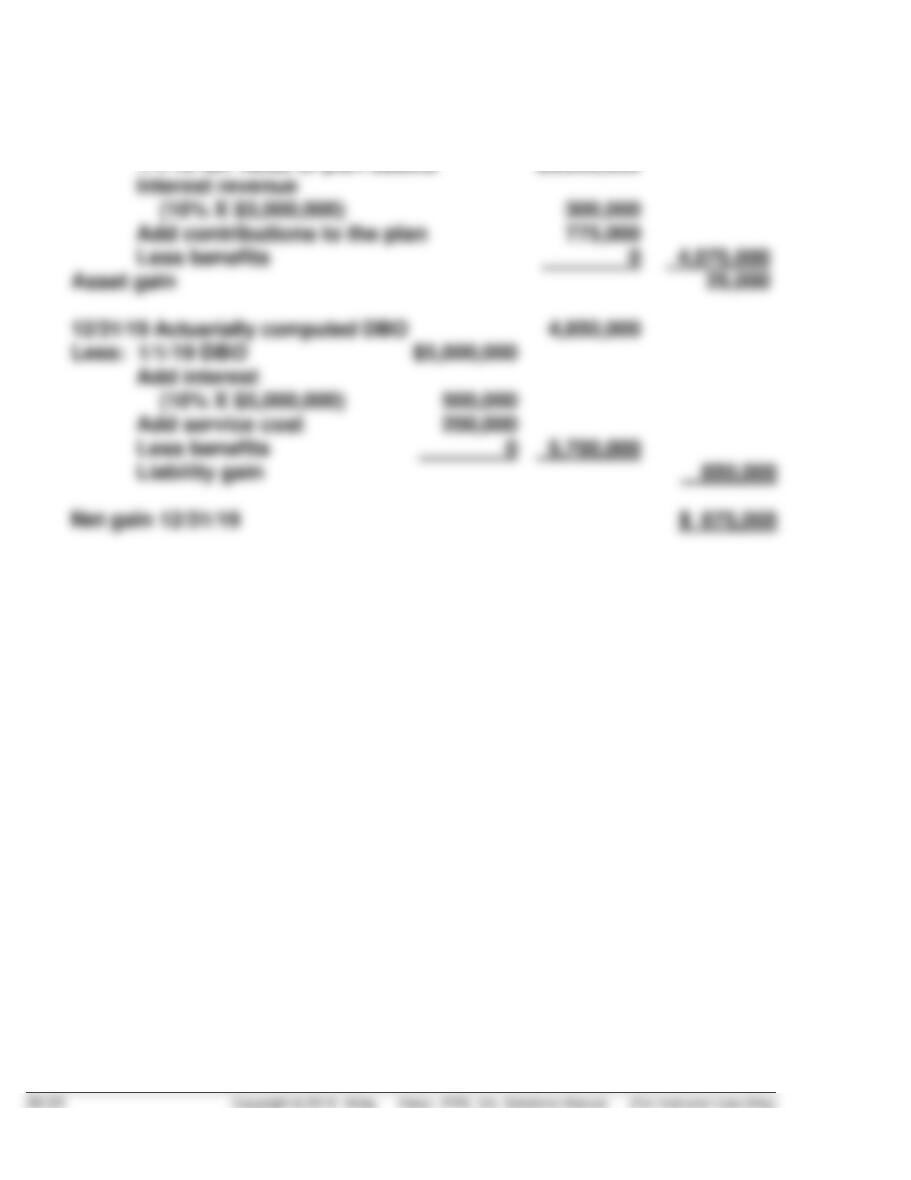

(a) Pension expense for 2019 comprised the following:

Service cost …………………………………………………………….. $200,000

(b) Pension liability, beginning of year ……………………………. $2,000,000

Less: Pension liability, end of year ……………………………. 750,000*

Decrease in liability …………………………………………… $1,250,000

PROBLEM 20.6 (Continued)

(c) 12/31/19 Fair value of plan assets $4,100,000

Less: Expected fair value of assets

1/1/19 fair value of plan assets $3,000,000

20–51 Copyright © 2018 Wiley Kieso, IFRS, 3/e, Solutions Manual (For Instructor Use Only)

PROBLEM 20.6 (Continued)

General Journal Entries

Memo Record

Annual

Defined

20–52 Copyright © 2018 Wiley Kieso, IFRS, 3/e, Solutions Manual (For Instructor Use Only)

Annual

Defined

HANSON LTD.

Service cost

108,000 Cr.

Interest expense*

Benefits

Asset loss**

Accumulated OCI, Dec. 31, 2011

Balance, Dec. 31, 2012

786,000 Cr.

20–53 Copyright © 2018 Wiley Kieso, IFRS, 3/e, Solutions Manual (For Instructor Use Only)

PROBLEM 20.8

LEMKE SA

Pension Worksheet—2019 and 2020

General Journal Entries

Memo Record

Items

Annual

Pension

Expense

Cash

OCI—

Gain/Loss

Pension

Asset/

Liability

Defined

Benefit

Obligation

Plan Assets

Balance, Jan. 1, 2019

190,000 Cr.

600,000 Cr.

410,000 Dr.

Service cost

40,000 Dr.

40,000 Cr.

60,000 Dr.

60,000 Cr.

41,000 Cr.

Contributions

Benefits

31,500 Dr.

Liability loss

87,000 Cr.

Journal entry for 2019

59,000 Dr.

Accumulated OCI, Dec. 31, 2018

Balance, Dec. 31, 2019

92,000 Dr.

244,000 Cr.

755,500 Cr.

Service cost

59,000 Dr.

59,000 Cr.

75,550 Dr.

75,550 Cr.

51,150 Cr.

Contributions

Benefits

54,000 Dr.

Balance, Dec. 31, 2020

82,150 Dr.

236,550 Cr.

836,050 Cr.

PROBLEM 20.8 (Continued)

Worksheet computations:

(a)R60,000 = R600,000 X 10%.

(b) 2019

Pension Expense ……………………………………………… 59,000

Other Comprehensive Income (G/L) …………………… 92,000

Cash …………………………………………………………. 97,000

PROBLEM 20.8 (Continued)

(c) Financial Statements—2020

Income Statement

Pension expense …………………………………….. R 83,400

Comprehensive Income Statement

PROBLEM 20.9

(a) See worksheet on next page.

(b) December 31, 2019

Other Comprehensive Income (G/L) ………………… 208,000

(c) See worksheet on next page. The entry is below.

December 31, 2020

Other Comprehensive Income (G/L) ………………… 133,200

(d) Financial Statements—2020

Income Statement

20-57 Copyright © 2018 Wiley Kieso, IFRS, 3/e, Solutions Manual (For Instructor Use Only)

PROBLEM 20.9 (Continued)

(a) HOBBS AG

Pension Worksheet—2019 and 2020

General Journal Entries Memo Record

Items

Annual

Pension

Expense

Cash

OCI—

Gain/Loss

Pension

Asset/Liability

Defined

Benefit

Obligation

Plan

Assets

Balance, Jan. 1, 2019

4,600,000 Cr.

4,600,000 Dr.

Service cost

150,000 Dr.

150,000 Cr.

Interest expense(a)

460,000 Dr.

460,000 Cr.

Interest revenue(b)

460,000 Cr.

460,000 Dr.

Contributions

200,000 Cr.

200,000 Dr.

Benefits

220,000 Dr.

220,000 Cr.

Asset loss(c)

208,000 Cr.

Journal entry for 2019

150,000 Dr.

200,000 Cr.

Accumulated OCI Dec. 31, 2018

Balance, Dec. 31, 2019

4,832,000 Dr.

Additional PSC, 1/1/2020

600,000 Dr.

Balance, Jan. 1, 2020

Service cost

170,000 Dr.

170,000 Cr.

Interest expense(d)

559,000 Dr.

559,000 Cr.

Interest revenue(e)

483,200 Cr.

483,200 Dr.

Contributions

184,658 Cr.

184,658 Dr.

Benefits

280,000 Dr.

280,000 Cr.

Asset loss(f)

133,200 Cr.

Journal entry for 2020

845,800 Dr.

Accumulated OCI, Dec. 31, 2019

Balance, Dec. 31, 2020

5,086,658 Dr.

(c) 1. Discount Rate: $26,000 ÷ $325,000 = 8% based on interest expense or $16,400 ÷ $205,000 = 8%, based on

interest revenue.

LO: 2,4, Bloom: AP, Difficulty: Moderate, Time: 25–30, AACSB: Analytic, AICPA BB: Critical Thinking, AICPA FC: Reporting, AICPA PC: Problem Solving

20–59 Copyright © 2018 Wiley Kieso, IFRS, 3/e, Solutions Manual (For Instructor Use Only)

PROBLEM 20.11

KRAMER COMPANY

(a) Completed Worksheet—2020

Interest expense

Interest revenue

Benefits

Asset gain

Accumulated OCI, Dec. 31, 2019

Balance, Dec. 31, 2020

PROBLEM 20.11 (Continued)

Worksheet computations:

Asset gain: $12,080 = $32,000 – $19,920.

(b) 2020

Pension Expense ……………………………………………….. 71,040

(c) Financial Statements—2020

Income Statement

Pension expense ………………………………………….. $71,040