CHAPTER 6

Accounting and the Time Value of Money

ASSIGNMENT CLASSIFICATION TABLE (BY TOPIC)

Topics

Questions

Brief

Exercises

Exercises

Problems

1.

Present value concepts.

1, 2, 3, 4, 5,

9, 17, 19

2.

Use of tables.

13, 14

8

1

3.

Present and future value

problems:

a. Unknown future amount.

7, 19

1, 5, 13

2, 3, 4, 6

b. Unknown payments.

10, 11, 12

6, 12, 17

8, 16, 17

2, 7

c. Unknown number of

periods.

4, 9

10, 15

2

d. Unknown interest rate.

15, 18

3, 11, 16

9, 10, 11

2, 7

4.

Value of a series of irregular

deposits; changing interest

rates.

3, 5, 8

5.

Valuation of leases,

pensions, bonds; choice

between projects.

6

7, 12, 13,

14, 15

1, 3, 5, 6, 8, 9,

10, 11, 12

6.

Deferred annuity.

ASSIGNMENT CLASSIFICATION TABLE (BY LEARNING OBJECTIVE)

Learning Objectives

Brief

Exercises

Exercises

Problems

1. Describe the fundamental concepts

related to the time value of money.

8

1

4, 7, 8

10, 15

7, 9, 10

15, 16

4. Solve present value of ordinary and

annuity due problems.

10, 11, 12,

14, 16, 17

1, 3, 4, 5, 6,

11, 12, 17,

18, 19

1, 3, 4, 5,

7, 8, 9, 10,

13, 14

expected cash flows.

14, 20, 21,

13, 14, 15

ASSIGNMENT CHARACTERISTICS TABLE

Item

Description

Level of

Difficulty

Time

(minutes)

E6.1

Using interest tables.

Simple

5–10

E6.2

Simple and compound interest computations.

Simple

5–10

E6.3

Computation of future values and present values.

Simple

10–15

E6.4

Computation of future values and present values.

Moderate

15–20

E6.5

Computation of present value.

Simple

10–15

E6.6

Future value and present value problems.

Moderate

15–20

E6.7

Computation of bond prices.

Moderate

12–17

E6.8

Computations for a retirement fund.

Simple

10–15

E6.9

Unknown rate.

Moderate

5–10

E6.10

Unknown periods and unknown interest rate.

Simple

10–15

E6.11

Evaluation of purchase options.

Moderate

10–15

E6.12

Analysis of alternatives.

Simple

10–15

E6.13

Computation of bond liability.

Moderate

15–20

E6.14

Computation of pension liability.

Moderate

15–20

E6.15

Investment decision.

Moderate

15–20

E6.16

Retirement of debt.

Simple

10–15

E6.17

Computation of amount of rentals.

Simple

10–15

E6.18

Least costly payoff.

Simple

10–15

E6.19

Least costly payoff.

Simple

10–15

E6.20

Expected cash flows.

Simple

5–10

E6.21

Expected cash flows and present value.

Moderate

15–20

E6.22

Fair value estimate.

Moderate

15–20

P6.1

Various time value situations.

Moderate

15–20

P6.2

Various time value situations.

Moderate

15–20

P6.3

Analysis of alternatives.

Moderate

20–30

P6.4

Evaluating payment alternatives.

Moderate

20–30

P6.5

Analysis of alternatives.

Moderate

20–25

P6.6

Purchase price of a business.

Moderate

25–30

P6.7

Time value concepts applied to solve business problems.

Complex

30–35

P6.8

Analysis of alternatives.

Moderate

20–30

P6.9

Analysis of business problems.

Complex

30–35

P6.10

Analysis of lease vs. purchase.

Complex

30–35

P6.11

Pension funding.

Complex

25–30

P6.12

Pension funding.

Moderate

20–25

P6.13

Expected cash flows and present value.

Moderate

20–25

P6.14

Expected cash flows and present value.

Moderate

20–25

P6.15

Fair value estimate.

Complex

20–25

ANSWERS TO QUESTIONS

1. Money has value because with it one can acquire assets and services and discharge obligations.

The holding, borrowing or lending of money can result in costs or earnings. And the longer the

time period involved, the greater the costs or the earnings. The cost or earning of money as a

function of time is the time value of money. A dollar received today is worth more than a dollar

promised at some time in the future because of the opportunity to invest today’s dollar and receive

interest on the investment.

2. Some situations in which present value measures are used in accounting include:

(a) Notes receivable and payable—these involve single sums (the face amounts) and may involve

annuities, if there are periodic interest payments.

(b) Leases—involve measurement of assets and obligations, which are based on the present value

of annuities (lease payments) and single sums (if there are residual values to be paid at the

conclusion of the lease).

3. Interest is the payment for the use of money. It may represent a cost or earnings depending upon

whether the money is being borrowed or loaned. The earning or incurring of interest is a function

4. The interest rate generally has three components:

(a) Pure rate of interest—This would be the amount a lender would charge if there were no

possibilities of default and no expectation of inflation.

(b) Expected inflation rate of interest—Lenders recognize that in an inflationary economy, they

Questions Chapter 6 (Continued)

5. (a) Present value of an ordinary annuity at 8% for 10 periods (Table 6-4).

(b) Future value of 1 at 8% for 10 periods (Table 6-1).

6. He should choose quarterly compounding, because the balance in the account on which interest

will be earned will be increased more frequently, thereby resulting in more interest earned on the

investment. This is shown in the following calculation:

Semiannual compounding, assuming the amount is invested for 2 years:

7. $26,897.80 = $20,000 X 1.34489 (future value of 1 at 21/2% (10% ÷ 4) for 12 (3 x 4) periods).

LO: 3, Bloom: AP, Difficulty: Simple, Time: 5-7, AACSB: Analytic, AICPA BB: Critical Thinking, AICPA FC: Reporting, AICPA PC: Problem Solving

8. $44,671.20 = $80,000 X .55839 (present value of 1 at 6% (12% ÷ 2) for 10 (5 x 2) periods).

LO: 1, Bloom: AP, Difficulty: Simple, Time: 5-7, AACSB: Analytic, AICPA BB: Critical Thinking, AICPA FC: Reporting, AICPA PC: Problem Solving

10.

Amount paid each year =

€40,000

(present value of an ordinary annuity at 12% for 4 years).

3.03735

11.

Amount deposited each year =

Questions Chapter 6 (Continued)

12.

Amount deposited each year =

¥20,000,000

[future value of an annuity due at 10% for 4 years

(4.64100 X 1.10)].

5.10510

13. The process for computing the future value of an annuity due using the future value of an ordinary

annuity interest table is to multiply the corresponding future value of the ordinary annuity by one

14. The basis for converting the present value of an ordinary annuity table to the present value of an

15. Present value = present value of an ordinary annuity of $25,000 for 20 periods at ? percent.

$245,000 = present value of an ordinary annuity of $25,000 for 20 periods at ? percent.

LO: 1,4, Bloom: AP, Difficulty: Simple, Time: 5-7, AACSB: Analytic, AICPA BB: Critical Thinking, AICPA FC: Reporting, AICPA PC: Problem Solving

16. 4.96764 Present value of ordinary annuity at 12% for eight periods.

17. (a) Present value of an annuity due.

(b) Present value of 1.

18. R$27,600 = PV of an ordinary annuity of $6,900 for five periods at ? percent.

19. The taxing authority argues that the future reserves should be discounted to present value. The

SOLUTIONS TO BRIEF EXERCISES

BRIEF EXERCISE 6.1

8% annual interest

i = 8%

PV = $15,000 FV = ?

8% annual interest, compounded semiannually

i = 4%

PV = $15,000 FV = ?

BRIEF EXERCISE 6.2

12% annual interest

i = 12%

PV = ? FV = R$25,000

12% annual interest, compounded quarterly

i = 3%

PV = ? FV = R$25,000

BRIEF EXERCISE 6.3

i = ?

PV = €30,000 FV = €150,000

BRIEF EXERCISE 6.4

i = 5%

PV = $10,000 FV = $17,100

BRIEF EXERCISE 6.5

First payment at year-end (Ordinary Annuity)

i = 6%

FV – OA =

?

€8,000 €8,000 €8,000 €8,000 €8,000

First payment today (Annuity Due)

i = 6%

R = FV – AD =

€8,000 €8,000 €8,000 €8,000 €8,000 ?

BRIEF EXERCISE 6.6

i = 5%

FV – OA =

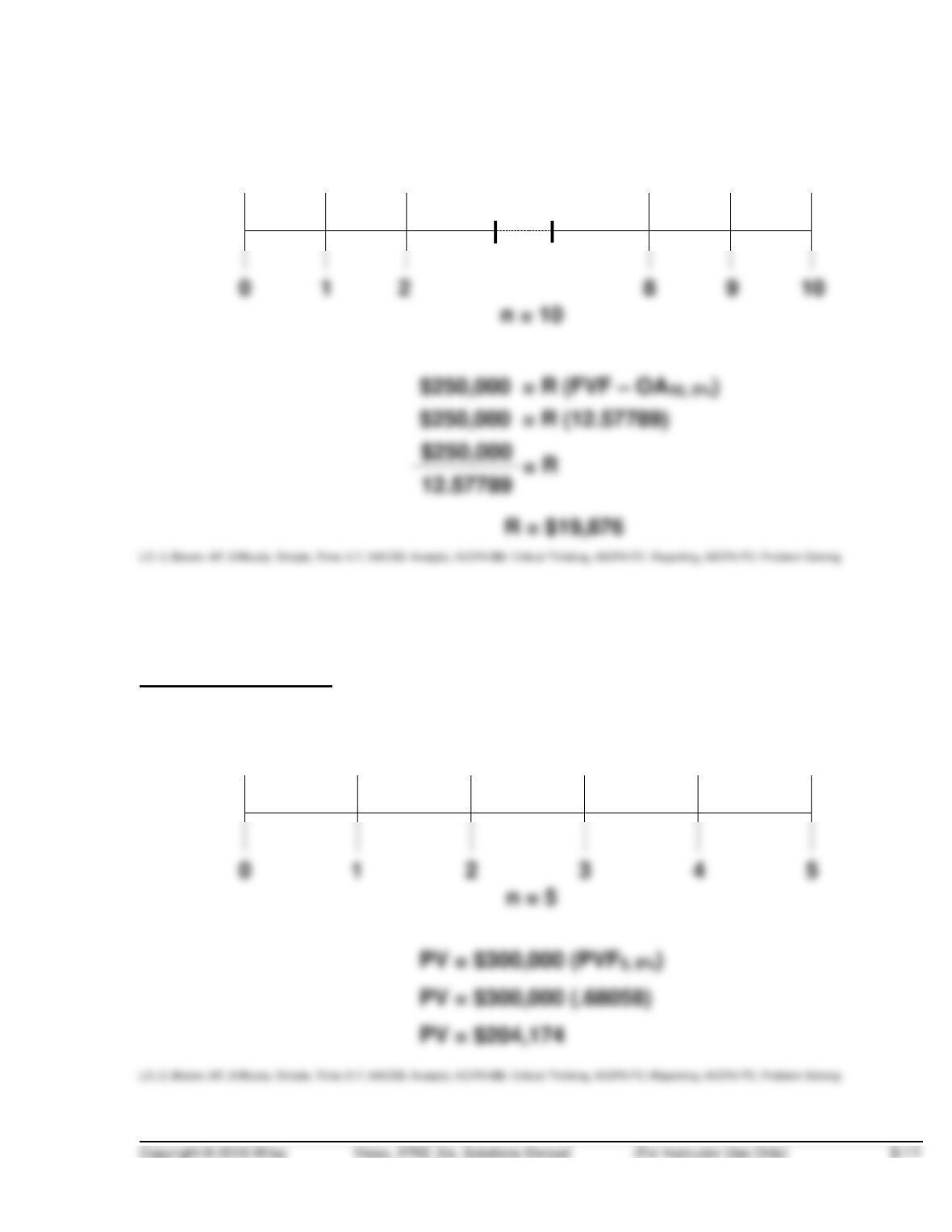

R = ? ? ? ? $250,000

BRIEF EXERCISE 6.7

8% annual interest

i = 8%

PV = ? FV = $300,000

BRIEF EXERCISE 6.8

With quarterly compounding, there will be 20 (5 x 4 ) quarterly compounding

BRIEF EXERCISE 6.9

i = 5%

FV – OA =

R = $100,000

$9,069 $9,069 $9,069

BRIEF EXERCISE 6.10

First withdrawal at year-end

i = 8%

PV – OA = R =

? £30,000 £30,000 £30,000 £30,000 £30,000

0

8

First withdrawal immediately

i = 8%

PV – AD =

?

R =

8

9 10

BRIEF EXERCISE 6.11

i = ?

PV = R =

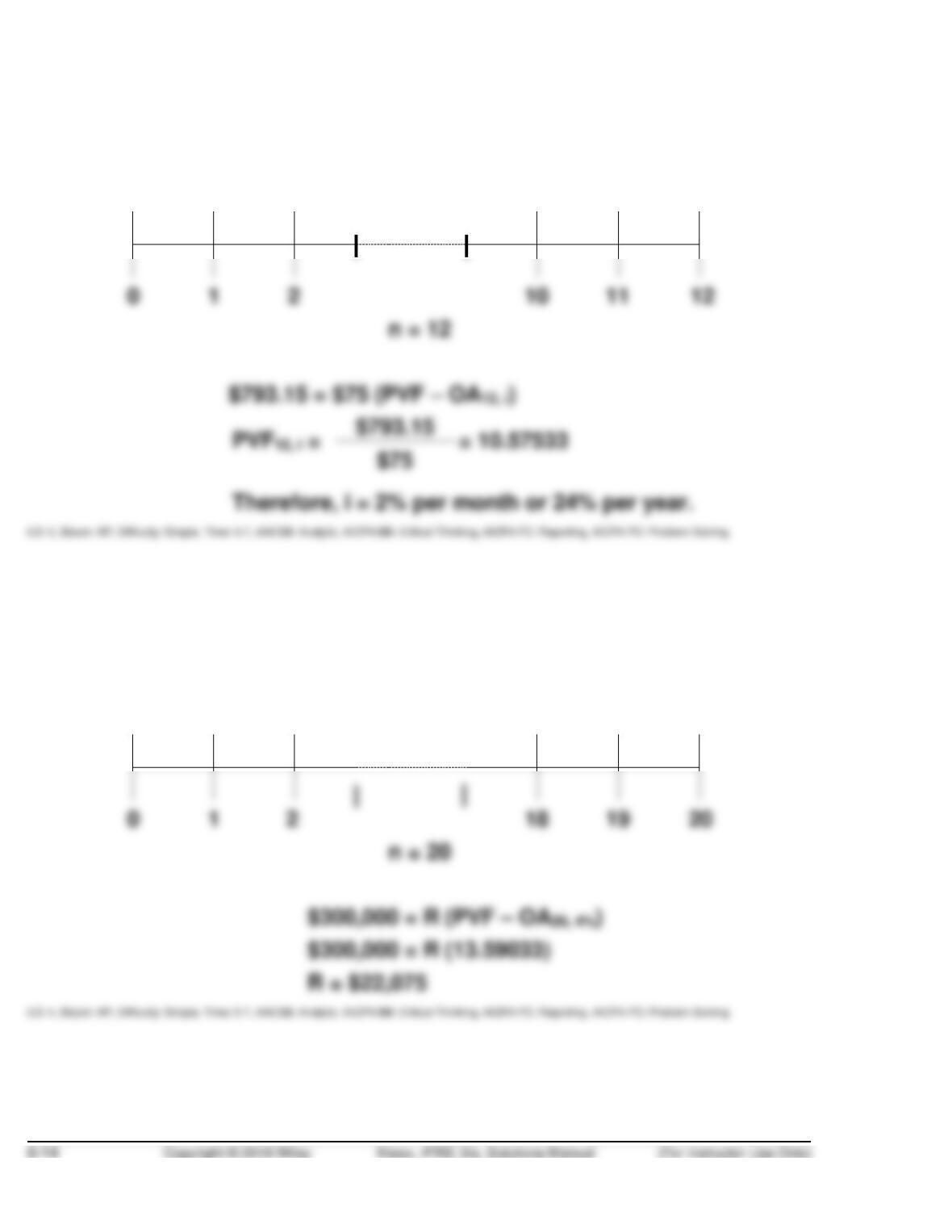

$793.15 $75 $75 $75 $75 $75

11 12

BRIEF EXERCISE 6.12

i = 4%

PV =

$300,000 R = ? ? ? ? ?

2

19 20

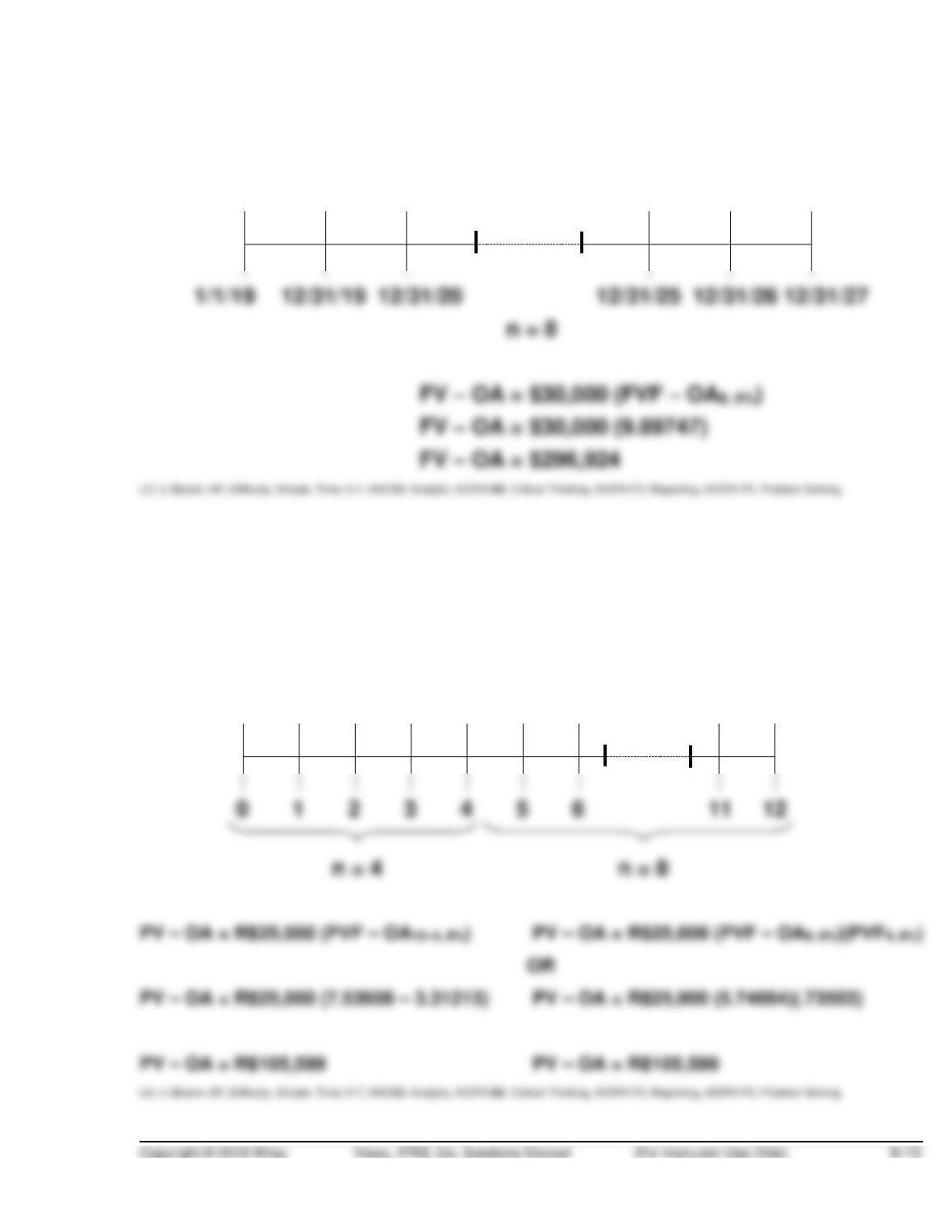

BRIEF EXERCISE 6.13

i = 6%

R =

$30,000 $30,000 $30,000 $30,000 $30,000

1/1/19

12/31/19

12/31/25

BRIEF EXERCISE 6.14

i = 8%

PV – OA = R =

? R$25,000 R$25,000 R$25,000 R$25,000

0

1

2

3

4

5

6

BRIEF EXERCISE 6.15

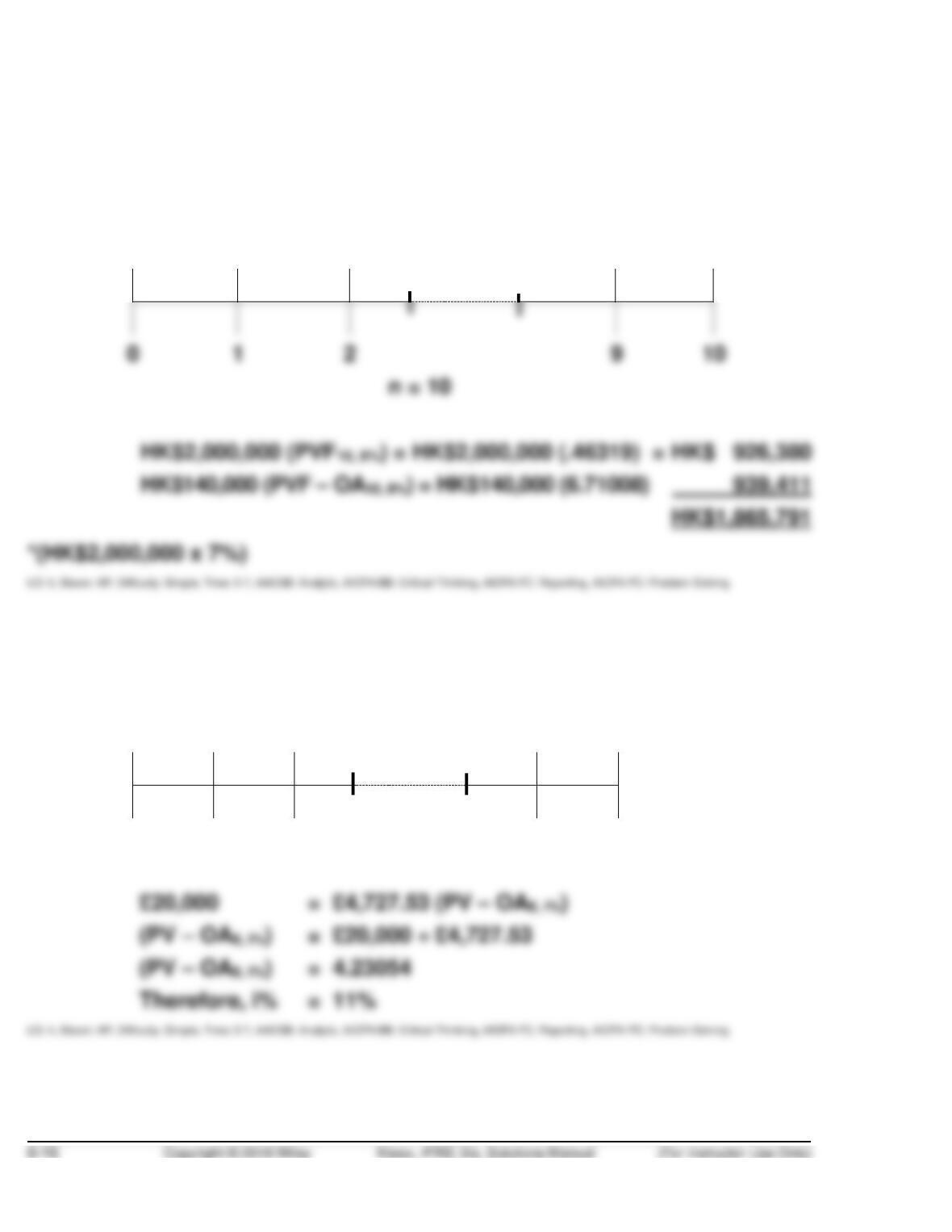

i = 8%

PV = ?

PV – OA = R = HK$2,000,000

? HK$140,000* HK$140,000 HK$140,000 HK$140,000

0

1

2

BRIEF EXERCISE 6.16

PV – OA = £20,000

£4,727.53 £4,727.53 £4,727.53 £4,727.53

0

1

2

5 6

BRIEF EXERCISE 6.17

PV – AD = £20,000

£? £? £? £?

0

1

2

5 6

SOLUTIONS TO EXERCISES

EXERCISE 6.1 (5–10 minutes)

(a)

(b)

Rate of Interest

Number of Periods

1.

a.

9%

9

b.

2% (8% ÷ 4)

20 (5 x 4)

c.

5% (10% ÷ 2)

30 (15 x 2)

2.

a.

9%

25

c.

3% (12% ÷ 4)

EXERCISE 6.2 (5–10 minutes)

(a)

Simple interest of HK$2,400 (HK$30,000 X 8%)

per year X 8 …………………………………………………………

HK$19,200

Principal …………………………………………………………………..

30,000

Total withdrawn ………………………………………………..

HK$49,200

(b)

Interest compounded annually—Future value of

(c)

Interest compounded semiannually—Future

EXERCISE 6.3 (10–15 minutes)

(a)

€9,000 X (FVF5, 8%) 1.46933 = €13,224.

(b)

€9,000 X (PF8, 6%) .62741 = €5,647.

(d)

€9,000 X (PVF–OA30, 5%) 12.46221 = €112,160.

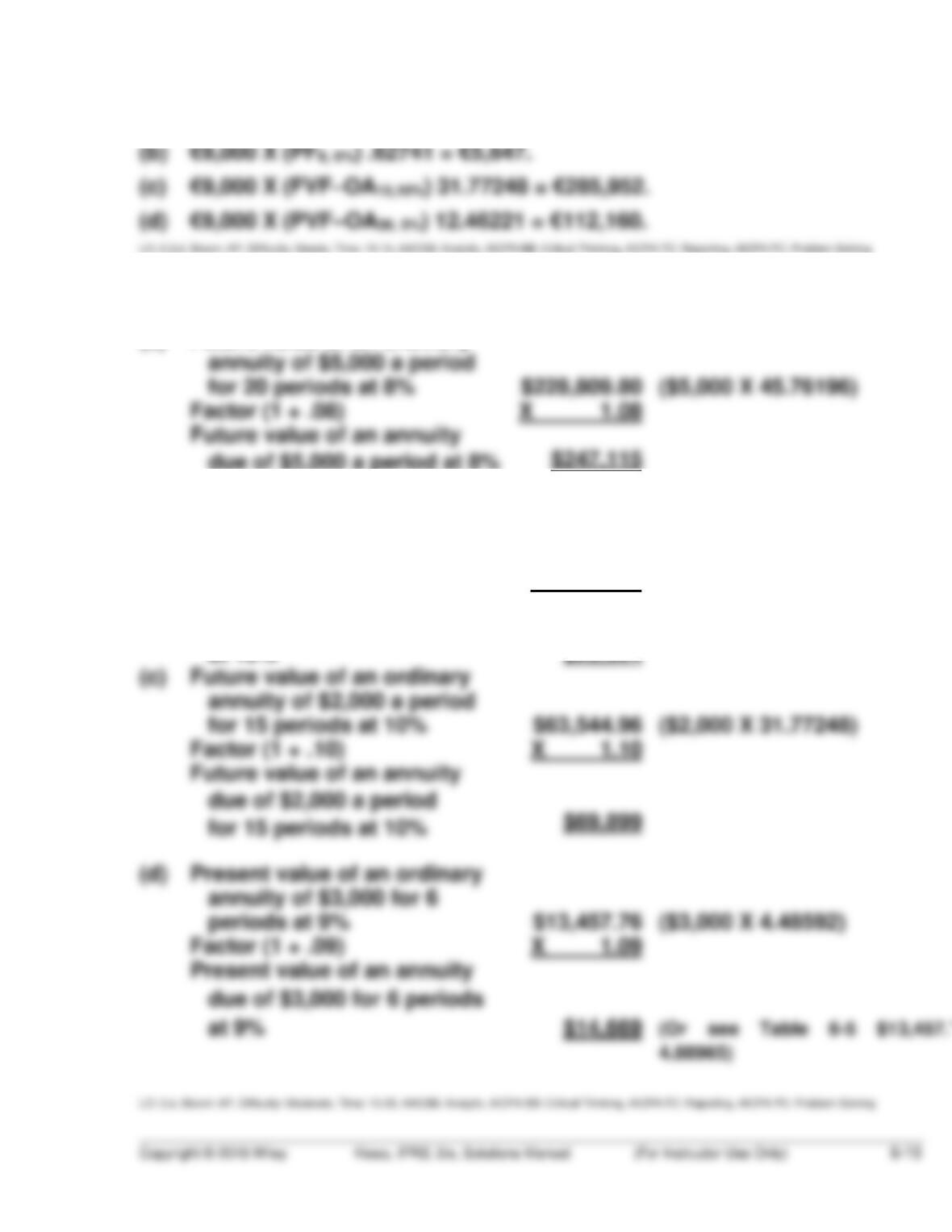

EXERCISE 6.4 (15–20 minutes)

(a)

Factor (1 + .08)

X 1.08

Future value of an ordinary

due of $5,000 a period at 8%

(b)

Present value of an ordinary

annuity of $2,500 for 30

periods at 10%

$23,567.28

($2,500 X 9.42691)

Factor (1 + .10)

X 1.10

Present value of annuity

due of $2,500 for 30 periods

(Or see Table 6-5 $23,567 x 10.369

at 10%

(c)

Future value of an ordinary

Factor (1 + .10)

X 1.10

EXERCISE 6.5 (10–15 minutes)

(a)

£50,000 X (PVF–OA8, 12%) 4.96764 = £248,382.

(c)

£50,000 X (PVF–AD4, 12%) (PVF6, 12%) (3.03735 X .50663) = £76,941.

EXERCISE 6.6 (15–20 minutes)

(a)

Future value of ¥1,200,000 @ 10% for 10 years

(¥1,200,000 X 2.59374) =

¥ 3,112,488

(b)

Future value of an ordinary annuity of W620,000

at 10% for 15 years (W620,000 X 31.77248)

(c)

R$75,000 discounted at 8% for 10 years:

Accept the bonus of R$40,000 now.

EXERCISE 6.7 (12–17 minutes)

(a)

$100,000 X (PVF15,8%) .31524

=

$ 31,524

+ $10,000 X (PVF–OA15,8%) 8.55948

=

85,595

$117,119

(b)

$100,000 X (PVF15,10%) .23939

=

+ $10,000 X (PVF–OA15,10%) 7.60608

=

76,061

(c)

$100,000 X (PVF15,12%).18270

=

+ $10,000 X (PVF–OA15,12%) 6.81086

=