CHAPTER 10

Acquisition and Disposition

of Property, Plant, and Equipment

ASSIGNMENT CLASSIFICATION TABLE (BY TOPIC)

Topics

Questions

Brief

Exercises

Exercises

Problems

Concepts

for Analysis

1.

Valuation and classification

of land, buildings, and

equipment.

1, 2, 3,

5, 6, 11,

12, 21

1

1, 2, 3, 4,

5, 13

1, 2, 3, 5

1, 6, 7

2.

Self-constructed assets,

capitalization of overhead.

4, 7, 20, 21

4, 6, 12, 16

2

12, 21

7, 8, 9, 10,

16

assets.

11, 12

17, 18,

10, 11

19, 20

5.

Lump-sum purchases,

issuance of shares,

deferred-payment contracts.

11, 13, 14

5, 6, 7

3, 6, 11, 12,

13, 14,

15, 16

2, 3, 11

Government grants.

21, 22

7.

Costs subsequent to

acquisition.

18, 19

23, 24, 25

1

Disposition of assets.

22, 23

15, 16

26, 27

4

1

ASSIGNMENT CLASSIFICATION TABLE (BY LEARNING OBJECTIVE)

Learning Objectives

Brief

Exercises

Exercises

Problems

Concepts

for

Analysis

1. Understand property, plant, and equipment and

its related costs.

1

1, 2, 3, 4, 5, 6,

12, 13

1, 2, 3, 4,

5, 11

1, 2, 7

2. Describe the accounting problems associated

with interest capitalization.

2, 3, 4

1, 2, 4, 5, 6, 7,

8, 9, 10, 16

1, 5, 6, 7

3, 4, 6, 7

18, 19, 20, 21,

4. Describe the accounting treatment for costs

subsequent to acquisition.

13

23, 24, 25

1

5. Describe the accounting treatment for the

disposal of property, plant, and equipment.

15, 16

26, 27

2, 4, 11

1

ASSIGNMENT CHARACTERISTICS TABLE

Item

Description

Level of

Difficulty

Time

(minutes)

E10.1

Acquisition costs of realty.

Moderate

15–20

E10.2

Acquisition costs of realty.

Simple

10–15

E10.3

Acquisition costs of trucks.

Simple

10–15

E10.4

Purchase and self-constructed cost of assets.

Moderate

20–25

E10.5

Treatment of various costs.

Moderate

20–25

E10.6

Correction of improper cost entries.

Moderate

15–20

E10.7

Capitalization of interest.

Moderate

20–25

E10.8

Capitalization of interest.

Moderate

20–25

E10.9

Capitalization of interest.

Moderate

20–25

E10.10

Capitalization of interest.

Moderate

20–25

E10.11

Entries for equipment acquisitions.

Simple

10–15

E10.12

Entries for asset acquisition, including self-construction.

Simple

15–20

E10.13

Entries for acquisition of assets.

Simple

20–25

E10.14

Purchase of equipment with zero-interest-bearing debt.

Moderate

15–20

E10.15

Purchase of computer with zero-interest-bearing debt.

Moderate

15–20

E10.16

Asset acquisition.

Moderate

25–35

E10.17

Non-monetary exchange.

Simple

10–15

E10.18

Non-monetary exchange.

Moderate

20–25

E10.19

Non-monetary exchange.

Moderate

15–20

E10.20

Non-monetary exchange.

Moderate

15–20

E10.21

Government grants.

Simple

15–20

E10.22

Government grants.

Moderate

10–15

E10.23

Analysis of subsequent expenditures.

Moderate

20–25

E10.24

Analysis of subsequent expenditures.

Simple

15–20

E10.25

Analysis of subsequent expenditures.

Simple

10–15

E10.26

Entries for disposition of assets.

Moderate

20–25

E10.27

Disposition of assets.

Simple

15–20

P10.1

Classification of acquisition and other asset costs.

Moderate

35–40

P10.2

Classification of acquisition costs.

Moderate

40–55

P10.3

Classification of land and building costs.

Moderate

35–45

P10.4

Dispositions, including condemnation, demolition, and

trade-in.

Moderate

35–40

P10.5

Classification of costs and interest capitalization.

Moderate

20–30

P10.6

Interest during construction.

Moderate

25–35

P10.7

Capitalization of interest.

Moderate

20–30

P10.8

Non-monetary exchanges.

Moderate

35–45

P10.9

Non-monetary exchanges.

Moderate

30–40

P10.10

Non-monetary exchanges.

Moderate

30–40

P10.11

Purchases by deferred payment, lump-sum, and non-

monetary exchanges.

Moderate

35–45

ASSIGNMENT CHARACTERISTICS TABLE (Continued)

Item

Description

Level of

Difficulty

Time

(minutes)

CA10.1

Acquisition, improvements, and sale of realty.

Moderate

20–25

CA10.2

Accounting for self-constructed assets.

Moderate

20–25

CA10.4

Capitalization of interest.

Moderate

30–40

CA10.5

Non-monetary exchanges.

Moderate

30–40

CA10.6

Costs of acquisition.

20–25

CA10.7

Cost of land vs. building—ethics.

Moderate

20–25

ANSWERS TO QUESTIONS

1. The major characteristics of plant assets are (1) that they are acquired for use in operations and

2. (a) The acquisition costs of land may include the purchase or contract price, the broker’s commis-

sion, title search and recording fees, assumed taxes or other liabilities, and surveying, demolition

(less salvage), and landscaping costs.

(b) Machinery and equipment costs may properly include freight and handling, taxes on purchase,

3. (a) Land.

(b) Land.

(c) Land.

4. (a) The position that no fixed overhead should be capitalized assumes that the construction of

plant (fixed) assets will be timed so as not to interfere with normal operations. If this were not

the case, the savings anticipated by constructing instead of purchasing plant assets would be

nullified by reduced profits on the product that could have been manufactured and sold. Thus,

Questions Chapter 10 (Continued)

5. (a) Disagree. Promotion expenses should be expensed.

(b) Agree. Architect’s fees for plans actually used in construction of the building should be charged

to the building account as part of the cost.

(c) Agree. IFRS requires that avoidable interest or actual interest cost, whichever is lower, be

6. Since the land for the plant site will be used in the operations of the firm, it is classified as property,

7. A common accounting justification is that all costs associated with the construction of an asset,

8. Assets that do not qualify for interest capitalization are (1) assets that are in use or ready for their

9. The avoidable interest is determined by multiplying (an) interest rate(s) by the weighted-average

amount of accumulated expenditures on qualifying assets. For the portion of weighted-average

accumulated expenditures which is less than or equal to any amounts borrowed specifically to

10. The total interest cost incurred during the period should be disclosed, indicating the portion

capitalized and the portion charged to expense.

Questions Chapter 10 (Continued)

11. (a) Assets acquired by issuance of ordinary shares—when property is acquired by issuance of

securities such as ordinary shares, the cost of the property is not measured by par or stated

value of such shares. If the shares are actively traded on the market, then the fair value of the

shares is a fair indication of the cost of the property because the fair value of the shares is a

good measure of the current cash equivalent price. If the fair value of the ordinary shares is

not determinable, then the fair value of the property should be established and used as the

basis for recording the asset and issuance of ordinary shares.

(d) Deferred payments—assets should be recorded at the present value of the consideration

exchanged between contracting parties at the date of the transaction. In a deferred payment

situation, there is an implicit (or explicit) interest cost involved, and the accountant should be

careful not to include this amount in the cost of the asset.

are significantly different.

12. The cost of such assets includes the purchase price, freight and handling charges incurred,

insurance on the equipment while in transit, cost of special foundations if required, assembly and

installation costs, and costs of conducting trial runs. Costs thus include all expenditures incurred in

acquiring the equipment and preparing it for use. When plant assets are purchased subject to cash

discounts for prompt payment, the question of how the discount should be handled arises. The

Questions Chapter 10 (Continued)

13.

Fair value of land

X Cost = Cost allocated to land

Fair value of building and land

15. Ordinarily accounting for the exchange of non-monetary assets should be based on the fair value

of the asset given up or the fair value of the asset received, whichever is more clearly evident.

Thus any gains and losses on the exchange should be recognized immediately. If the fair value of

16. In accordance with IFRS which requires gains and losses to be recognized when an exchange has

commercial substance the entry should be:

Equipment ……………………………………………………………………………… 42,000

Accumulated Depreciation—Equipment ……………………………………… 9,800*

17. IFRS requires that a grant be recognized in income on a systematic basis that matches it with the

related costs that they are intended to compensate. This can be accomplished by either

(1) recording the grant as deferred grant revenue, which is recognized as income over the useful

18. Ordinarily such expenditures include (1) the recurring costs of servicing necessary to keep property

in good operating condition, (2) cost of renewing structural parts of major plant units, and (3) costs

of major overhauling operations which may or may not extend the life beyond original expectation.

Questions Chapter 10 (Continued)

The third class of expenditures, major overhauls, is usually entered through the asset accounts

because replacement of important structural elements is usually involved. Other than maintenance

19. (a) Additions. Additions represent entirely new units or extensions and enlargements of old units.

Expenditures for additions are capitalized by charging either old or new asset accounts

depending on the nature of the addition.

(b) Major Repairs. Expenditures to replace parts or otherwise to restore assets to their previously

efficient operating condition are regarded as repairs. To be considered a major repair, several

periods must benefit from the expenditure. The cost should be recorded as an asset, with the

20. The cost of installing the machinery should be capitalized, but the extra month’s wages paid to the

dismissed employees should not, as this payment did not add any value to the machinery.

21. (a) Overhead of a business that builds its own equipment. Some accountants have maintained

that the equipment account should be charged only with the additional overhead caused by

such construction. However, a more realistic figure for cost of equipment results if the plant

asset account is charged for overhead applied on the same basis and at the same rate as

used for production (see Question 4).

Questions Chapter 10 (Continued)

(d) Profit on self-construction. This is not a proper cost of property, plant and equipment.

(e) Freight on equipment returned before installation, for replacement by other equipment of

greater capacity. If ordering the first equipment was an error, whether due to judgment or

addition to the building and not merely a replacement or repair.

(h) Replastering of a section of the building. This seems more in the nature of a repair than

anything else and as such should be treated as an expense.

22. This approach is not correct since at the very minimum the investor should be aware that certain

assets are used in the business which are not reflected in the main body of the financial statements.

23. Gains or losses on plant asset disposals should be shown in the income statement in the other

SOLUTIONS TO BRIEF EXERCISES

BRIEF EXERCISE 10.1

BRIEF EXERCISE 10.2

Expenditures

Date

Amount

Capitalization

Period

Weighted-Average

Accumulated Expenditures

3/1

HK$1,800,000

10/12

HK$1,500,000

6/1

3,000,000

HK$6,000,000

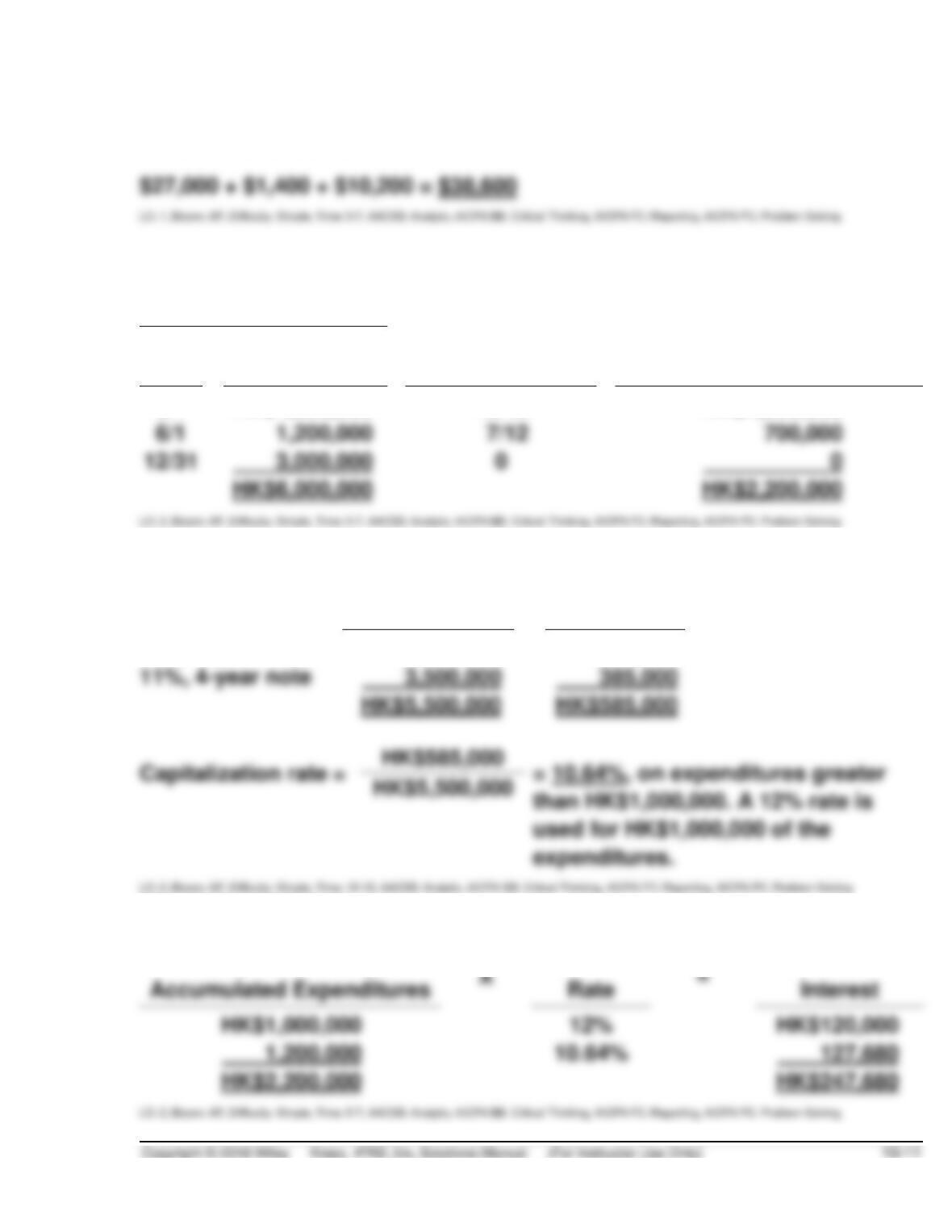

BRIEF EXERCISE 10.3

Principal

Interest

10%, 5-year note

HK$2,000,000

HK$200,000

11%, 4-year note

HK$585,000

BRIEF EXERCISE 10.4

Weighted-Average

Interest

Avoidable

BRIEF EXERCISE 10.5

Truck (£80,000 X .68301) ………………………………………….

54,641

Notes Payable …………………………………………………

BRIEF EXERCISE 10.6

Fair Value

% of Total

Cost

Recorded

Amount

Land

$ 60,000

60/360

X

$315,000

$ 52,500

Building

Equipment

BRIEF EXERCISE 10.7

Land (2,000 X $40) …………………………..………………………

80,000

Share Capital—Ordinary (2,000 X $10) ………………

Share Premium—Ordinary …………………………..

BRIEF EXERCISE 10.8

Equipment ……………………………………………………….

3,300

Accumulated Depreciation—Trucks …………………………

18,000

Trucks ……………………………………………………….

Cash ……………………………………………………….

Gain on Disposal of Trucks …………………………..

BRIEF EXERCISE 10.9

Computer (£3,300 – £800) ………………………………………..

2,500

Accumulated Depreciation ………………………………………

18,000

Truck ……………………………………………………….

Cash ……………………………………………………….

BRIEF EXERCISE 10.10

Equipment……………………………………………………….

5,000

Accumulated Depreciation—Equipment …………………..

Loss on Disposal of Equipment …………………………..

Equipment ……………………………………………………..

Cash ……………………………………………………….

BRIEF EXERCISE 10.11

Trucks ……………………………………………………………………

39,000

Accumulated Depreciation—Trucks …………………………

27,000

Trucks ……………………………………………………….

Cash ……………………………………………………….

BRIEF EXERCISE 10.12

Trucks ……………………………………………………………………

35,000

Accumulated Depreciation—Trucks …………………………

17,000

Loss on Disposal of Truck ……………………………………….

1,000

Trucks ……………………………………………………….

Cash ……………………………………………………….

BRIEF EXERCISE 10.13

BRIEF EXERCISE 10.14

1.

Deferred revenue approach:

Cash ………………………………………………………………………

Deferred Grant Revenue …………………………..

2.

Reduction of asset approach:

Cash ………………………………………………………………………

Equipment ……………………………………………………..

BRIEF EXERCISE 10.15

(a)

Depreciation Expense ($2,400 X 8/12) ………………………

1,600

Accumulated Depreciation—Machinery ……………

1,600

(b)

Cash ………………………………………………………………………

($8,400 + $1,600)—Machinery …………………………..

Machinery ………………………………………………………

Gain on Disposal of Machinery ………………………..

BRIEF EXERCISE 10.16

(a)

Depreciation Expense ($2,400 X 8/12) ………………………

1,600

Accumulated Depreciation—Machinery ……………

1,600

(b)

Cash ………………………………………………………………………

5,200

Loss on Disposal of Machinery …………………………..

4,800

($8,400 + $1,600)—Machinery …………………………..

Machinery ………………………………………………………

SOLUTIONS TO EXERCISES

EXERCISE 10.1 (15–20 minutes)

Item

Land

Land

Improvements

Buildings

Other Accounts

(a)

(€275,000) Notes Payable

(b)

€275,000

(c)

€ 10,000

(d)

7,000

6,000

(g)

25,000

(h)

11,000

(5,000)

13,000

(n)

(p)

3,000

EXERCISE 10.2 (10–15 minutes)

The allocation of costs would be as follows:

Land

Buildings

Land……………………………………………………………………….

$450,000

Razing costs …………………………..…………………………..

42,000

Residual value ……………………………………………………….

(6,300)

Legal fees …………………………..…………………………..

Survey ……………………………………………………….

Plans ………………………………………………………………………

Title insurance ……………………………………………………….

Liability insurance …………………………………………………..

Construction ……………………………………………………….

Interest ……………………………………………………….

EXERCISE 10.3 (10–15 minutes)

1.

Trucks ……………………………………………………………………

13,900

Cash ……………………………………………………….

13,900

2.

Trucks ……………………………………………………………………

Cash ……………………………………………………….

Notes Payable ………………………………………………..

16,364

*PV of $18,000 @ 10% for 1 year =

$18,000 X .90909 = $16,364

$16,364 + $2,000 = $18,364

3.

Trucks ……………………………………………………………………

15,200

Cost of Goods Sold ………………………………………………..

12,000

Inventory ……………………………………………………….

12,000

Sales ……………………………………………………….

15,200

4.

Trucks ……………………………………………………………………

13,000

Share Capital—Ordinary…………………………..

10,000

Share Premium—Ordinary

$13,000 less $10,000 par value) ……………………

EXERCISE 10.4 (20–25 minutes)

Purchase

Cash paid for equipment, including sales tax of €5,000 ……

€105,000

Freight and insurance while in transit …………………………….

2,000

Cost of moving equipment into place at factory ………………

3,100

Wage cost for technicians to test equipment …………………..

6,000

Special plumbing fixtures required for new equipment …….

8,000

Construction

Material and purchased parts (€200,000 X .99) …………………

€198,000

Labor costs …………………………………………………………………..

190,000

Overhead costs ……………………………………………………………..

50,000

Cost of installing equipment …………………………………………..

4,400

Total cost ……………………………………………………………………..

€442,400

EXERCISE 10.5 (20–25 minutes)

Land

Buildings

Equipment

Other

Abstract fees

£ 520

Architect’s fees

£ 3,170

Cash paid for land

and old building

92,000

Removal of old building

($20,000 – $5,500)

14,500

Interest on loans during

construction

7,400

Machinery purchased

£1,300

(Discount Lost)

Freight on machinery

Storage charges caused by

noncompletion of building

New building

Assessment by city

1,600

Hauling charges—machinery

(Loss)

5,400

£114,020

EXERCISE 10.6 (15–20 minutes)

Land ……………………………………………………………………………………

127,500

Buildings ………………………………………………………………………………

297,500

Cash ……………………………………………………………………………

2.

Equipment ……………………………………………………….

25,000

Cash ……………………………………………………….

2,000

Note Payable ………………………………………………….

23,000

Equipment ……………………………………………………….

Accounts Payable ($20,000 X .98) …………………….

19,600

Buildings ……………………………………………………….

Deferred Grant Revenue …………………………..

Buildings ……………………………………………………….

Cash ……………………………………………………….