*PROBLEM 14.13 (Continued)

(b)

December 31, 2019

Interest Payable ……………………………………………………..

33,000

Notes Payable (Old) ………………………………………………..

300,000

Gain on Extinguishment of Debt ………………………

Note Payable (New) …………………………………………

Gain on extinguishment of debt

£47,411

December 31, 2020

Interest Expense …………………………………………………….

34,271

Notes Payable ………………………………………………..

Cash ……………………………………………………….

December 31, 2021

Interest Expense …………………………………………………….

34,783

Notes Payable ………………………………………………..

Cash ……………………………………………………….

PROBLEM 14.14

(a)

Langley Co.

Carrying amount of the bonds on 1/1/19 ……………..

$656,992

Effective-interest rate (10%) ……………………………….

(b)

Tweedie Building Co.

Maturities and sinking fund requirements on long-term debt for

the next five year are as follows:

2020

$400,000 ($300,000 + $100,000)

2021

2022

2023

200,000 ($100,000 + $100,000)

2024

(c)

Beckford Inc.

Since the three bonds reported by Beckford Inc. are secured by

either real estate, securities of other corporations, or plant equip-

TIME AND PURPOSE OF CONCEPTS FOR ANALYSIS

CA 14.1 (Time 25–30 minutes)

Purpose—to provide the student with some familiarity with the economic theory which relates to the

accounting for a bond issue. The student is required to discuss the conceptual merits for each of the three

CA 14.2 (Time 10–15 minutes)

Purpose—to provide the student with an understanding of the various accounts which are generated in

a bond issue and their proper classifications on the statement of financial position. Justification must be

provided for the treatment accorded these accounts in relation to the specifics of this case.

CA 14.3 (Time 15–25 minutes)

Purpose—this case includes discussions of the determination of the selling price of bonds, presentation

CA 14.4 (Time 20–25 minutes)

Part I—Purpose—to provide the student with an understanding of the use of the effective-interest

CA 14.5 (Time 20–30 minutes)

Purpose—the student is asked to explain project financing arrangements, take-or-pay contracts, off–

balance-sheet financing, and the conditions for which a contractual obligation is to be disclosed as an

CA 14.6 (Time 20–30 minutes)

Purpose—to provide the student with an opportunity to examine the ethical issues related to the issue

of bonds.

SOLUTIONS TO CONCEPTS FOR ANALYSIS

CA 14.1

(a) 1. This is a common statement of financial position presentation and has the advantage of being

2. This presentation indicates the dual nature of the bond obligations. There is an obligation to

make periodic payments of $55,000 and an obligation to pay the $1,000,000 at maturity. The

3. This presentation shows the total liability which is incurred in a bond issue, but it ignores the

time value of money. This would be a fair presentation of the bond obligations only if the

effective-interest rate were zero.

(b) When an entity issues interest-bearing bonds, it normally accepts two types of obligations: (1) to

pay interest at regular intervals and (2) to pay the principal at maturity. The investors who

purchase Nichols Company bonds expect to receive $55,000 each January 1 and July 1 through

Another way of viewing this is that the $1,085,800 is the amount which, if invested at an annual

interest rate of 10% compounded semiannually, would allow withdrawals of $55,000 every six

months from July 1, 2020 through January 1, 2040 and $1,000,000 on January 1, 2040.

(c) 1. The use of the coupon rate for discounting bond obligations would give the face value of the

bond at January 1, 2020, and at any interest-payment date thereafter. Although the coupon

rate is readily available while the effective rate must be computed, the coupon rate may be set

CA 14.1 (Continued)

2. The effective-interest rate at January 1, 2020 is the market rate to Nichols Company for long-

term borrowing. This rate gives a discounted value for the bond obligations, which is the

amount that could be invested at January 1, 2016 at the market rate of interest. This

(d) Using a current yield rate produces a current value, that is, the amount which could currently be

invested to produce the desired payments. When the current yield rate is lower than the rate at the

issue date (or than at the previous valuation date), the liabilities for principal and interest would

CA 14.2

1. Use of the asset requires a depreciation charge in each year of use thereby reporting this

2. The obligation of a company is to its bondholders, not to the trustee. Until the bondholders have

received payment, the company still has a liability.

CA 14.3

(a) 1. The selling price of the bonds would be the present value of all of the expected net future cash

2. Immediately after the bond issue is sold, the current asset, cash, would be increased by the

CA 14.3 (Continued)

(b) The following item related to the bond issue would be included in Sealy’s 2020 income statement:

Interest expense would be included for ten months (March 1, 2020, to December 31, 2020) at an

effective-interest rate (yield) of 11 percent. This is composed of the nominal interest of

CA 14.4

Part I.

Before the effective-interest method of amortization can be used, the effective yield or interest rate

of the bond must be computed. The effective yield rate is the interest rate that will discount the two

CA 14.4 (Continued)

Part II.

(a) 1. Gain or loss to be amortized over the remaining life of old debt. The basic argument

2. Gain or loss to be amortized over the life of the new debt instrument. This argument states

that the gain or loss from early extinguishment of debt actually affects the cost of obtaining a new

3. Gain or loss recognized in the period of extinguishment. Proponents of this method state

that the early extinguishment of debt to be refunded actually does not differ from other types of

extinguishment of debt where the consensus is that any gain or loss from the transaction

should be recognized in full in current net earnings. The early extinguishment of the debt is

prompted for the same reason that other debt instruments are extinguished, namely, that the

(b) The immediate recognition principle is the only acceptable method of reflecting gains or losses on

the early extinguishment of debt, and these amounts, if material, must be reflected as other

CA 14.5

(a) Such financing arrangements arise when (1) two or more entities form another entity to construct

CA 14.5 (Continued)

(b) In some cases, project financing arrangements become more formalized through the use of take-

or-pay contracts or similar types of contracts. In a simple take-or-pay contract, a purchaser of goods

(c) Ryan should not record the plant as its asset. The plant is to be constructed and operated by ACC.

Although Ryan agrees to purchase all of the cans produced by ACC, Ryan does not have the

property right to the plant, nor the right to use the plant.

Although the discussion does not exclude the possibility of recording assets and liabilities for

purchase commitments, it contains no conclusions or implications about whether they should be

recorded.

(d) Off-balance-sheet financing is an attempt to borrow monies in such a way that the obligations

are not recorded in a company’s statement of financial position. The reasons for off-balance-sheet

financing are many. First, many believe that removing debt or otherwise keeping it from the

statement of financial position enhances the quality of the statement of financial position and

permits credit to be obtained more readily and at less cost. Second, loan covenants often impose

CA 14.6

(a) The stakeholders in the Wichita case are as follows:

Donald Lennon, president, founder, and majority shareholder.

CA 14.6 (Continued)

(b) The ethical issues:

The desires of the majority shareholder (Donald Lennon) versus the desires of the minority

shareholders (Nina Friendly and others).

(c) The rationale provided by the student will be more important than the specific position because

FINANCIAL REPORTING PROBLEM

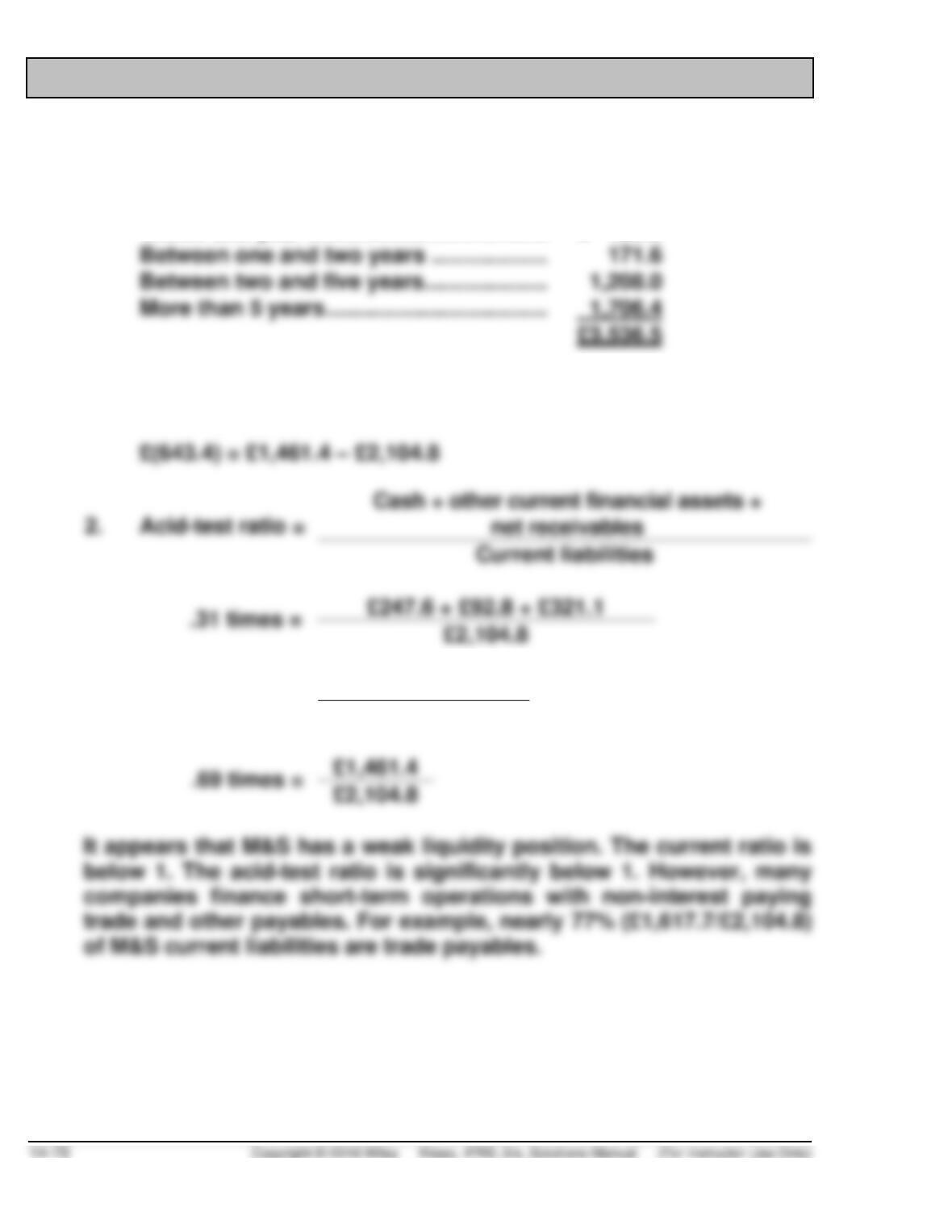

(a) According to the financial instruments note (Note 21), timing of cash

flows are:

Within one year ………………………………… £ 450.5

(b) (Amounts in £ millions)

1. Working capital = Current assets less current liabilities.

3.

Current ratio =

Current assets

Current liabilities

FINANCIAL REPORTING PROBLEM (Continued)

The other ratio analysis below can be used to evaluate M&S’s

financial position in 2016. Turnover ratios could be compared to prior

year levels.

Inventory turnover =

Cost of goods sold

Average inventory

=

£6,427.0

£799.9 + £797.8

2

=

8.05 times

Net cash provided by operating activities

FINANCIAL REPORTING PROBLEM (Continued)

£5,033.0 + £4,997.3

= .59

£8,476.4

Time interest earned =

Income before income taxes and interest expense

Interest expense

=

£404.4 + £113.5 + £99.3

£113.5

=

5.44 times

COMPARATIVE ANALYSIS CASE

(a) Debt to assets ratio:

adidas €7,696/€13,343 = 57.68%

Puma €1,001.0/€2,620.3 = 38.20%

Times interest earned ratio:

(b)

Carrying Value

Fair Value

adidas

€1,830

£1.331

Puma

€14.0

€14.0

(c) adidas has debt issued in foreign countries. These companies may

use foreign debt because

1. Lower interest rates may be available in foreign countries.