EXERCISE 17.9 (20–25 minutes)

(a) STEFFI GRAF, SA

Statement of Comprehensive Income

For the Year Ended December 31, 2019

_____________________________________________________________

Net income €120,000

(b) STEFFI GRAF, SA

Statement of Comprehensive Income

For the Year Ended December 31, 2020

_____________________________________________________________

Net income €140,000

Other comprehensive income

Holding gains €40,000

40,000

EXERCISE 17.10 (10–15 minutes)

(a) Fair Value Adjustment (£68,000 – £65,000) …………… 3,000

Unrealized Holding Gain or Loss—Income ……. 3,000

EXERCISE 17.11 (10–15 minutes)

(a) December 31, 2019

Unrealized Holding Gain or Loss—Income ………….. 1,400

Fair Value Adjustment ………………………………… 1,400

(b) During 2020

(c) December 31, 2020

Investments

Cost

Fair Value

Unrealized

Gain (Loss)

Stargate Corp. shares

€20,000

€19,300

(€ (700)

Vectorman Co. shares

EXERCISE 17.12 (5–10 minutes)

The unrealized gains and losses resulting from changes in the fair value of

equity investments [classified as non-trading] are recorded in an unrealized

EXERCISE 17.13 (10–15 minutes)

(a) The portfolio should be reported at the fair value of $54,500. Since the

cost of the portfolio is $53,000, the unrealized holding gain is $1,500, of

(b) The unrealized holding gain of $1,300 should be reported as other

income and expense on the income statement and the Fair Value

Adjustment account balance of $1,500 should be added to the cost of

the investment account.

WENGER, INC.

Statement of Financial Position

As of December 31, 2019

____________________________________________________________

(d) Equity Investment ……………………………………………… 1,300

Unrealized Holding Gain or Loss—Equity …….. 1,300

EXERCISE 17.14 (20–25 minutes)

(a) The total purchase price of these investments is:

The purchase entries will be:

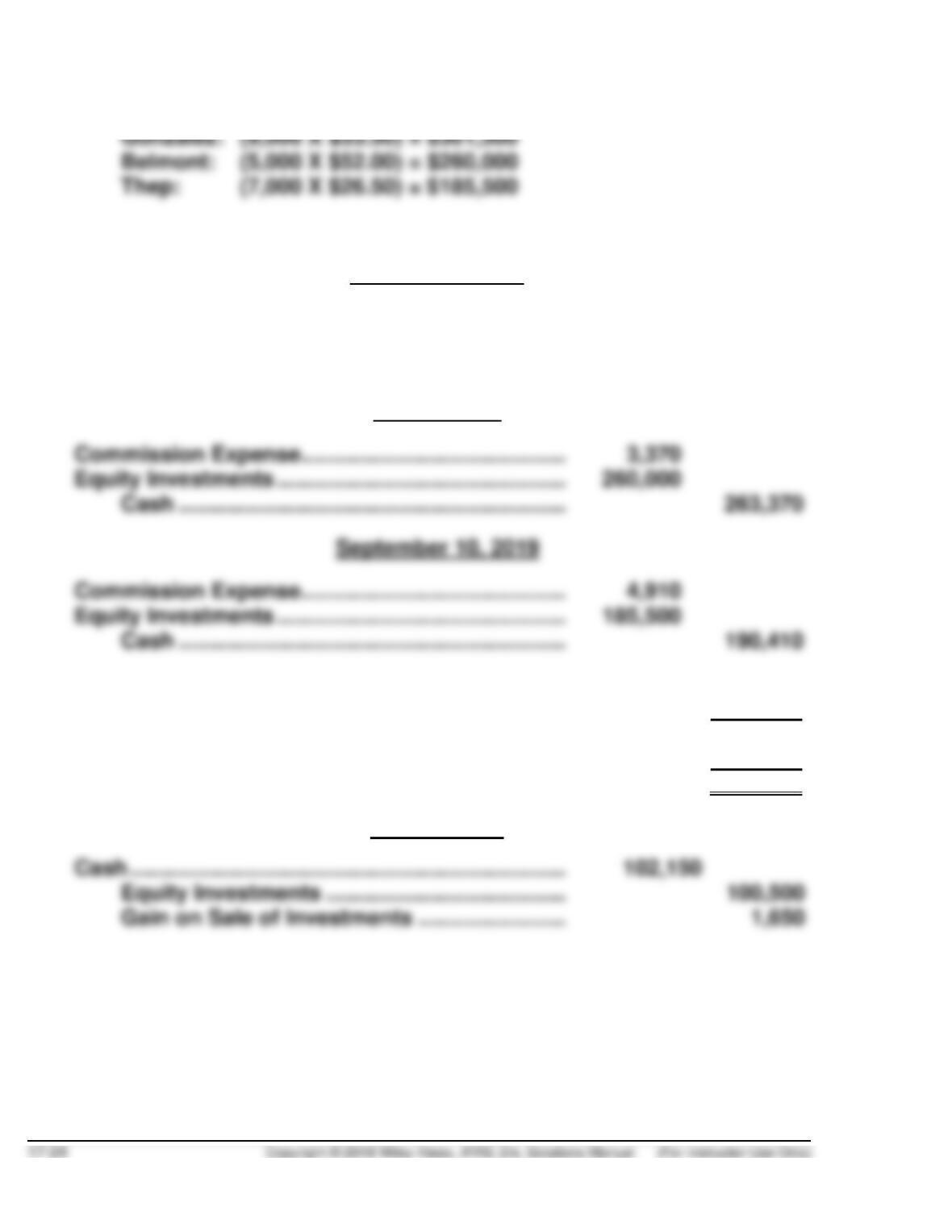

January 15, 2019

Commission Expense ……………………………………. 1,980

Equity Investments ……………………………………….. 301,500

Cash ……………………………………………………… 303,480

April 1, 2019

(b) Gross selling price of 3,000 shares at $35 ………. $105,000

Less: Commissions, taxes, and fees ……………… (2,850)

Net proceeds from sale …………………………………. 102,150

Cost of 3,000 shares ($301,500 X 3/9) ……………… (100,500)

Gain on sale of shares …………………………………… $ 1,650

May 20, 2019

EXERCISE 17.14 (Continued)

(c)

Investments

Cost

Fair Value

Unrealized

Gain (Loss)

Gonzalez Co.

$201,000*

$180,000(1)

$(21,000)

Belmont Co.

260,000

275,000(2)

(15,000

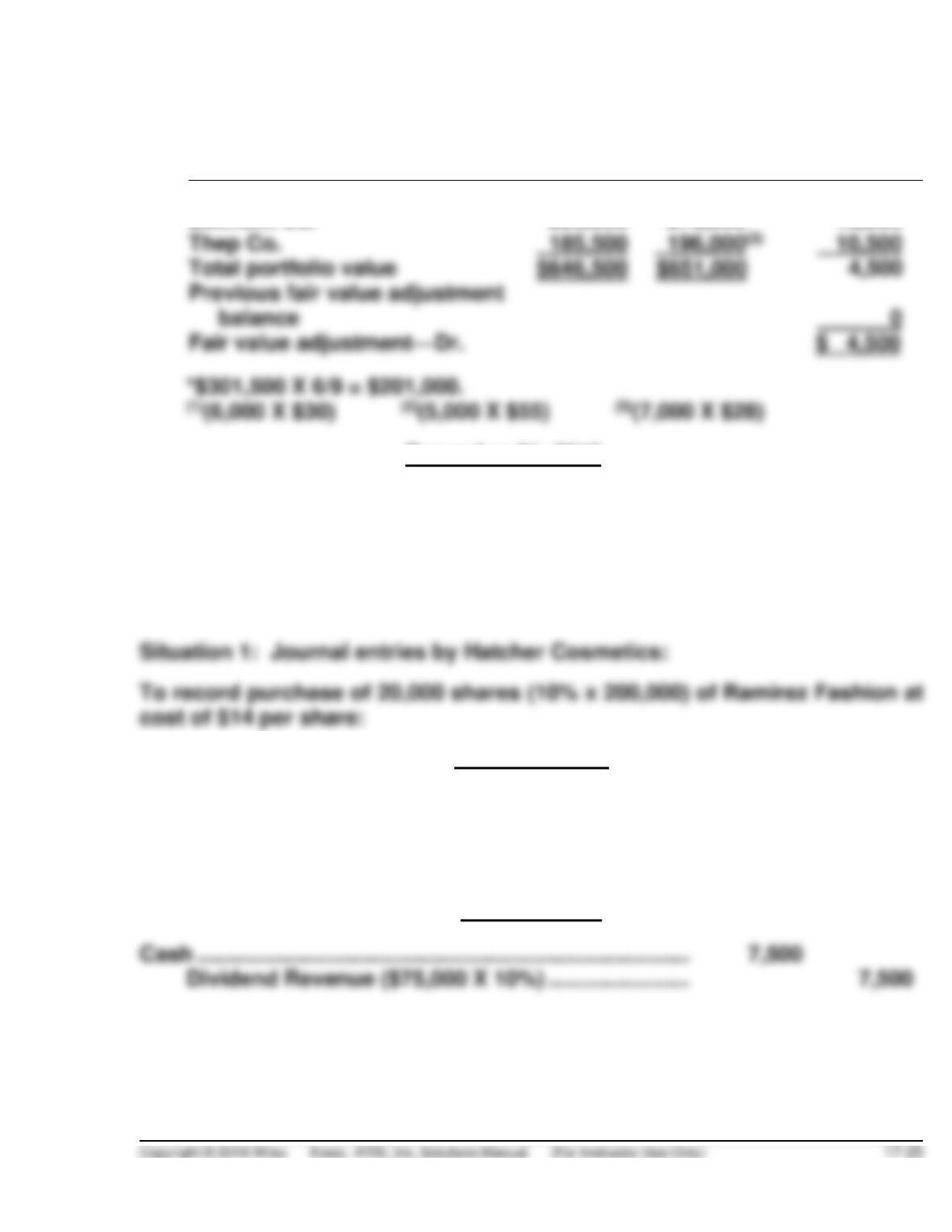

Thep Co.

Total portfolio value

$646,500

December 31, 2019

Fair Value Adjustment …………………………………….. 4,500

Unrealized Holding Gain or Loss—Income … 4,500

LO: 2, Bloom: AN, Difficulty: Moderate, Time: 20-25, AACSB: Analytic, AICPA BB: Critical Thinking, AICPA FC: Reporting, AICPA PC: Problem Solving

EXERCISE 17.15 (15–20 minutes)

March 18, 2019

Equity Investments (20,000 X $14) ………………………….. 280,000

Cash ………………………………………………………………. 280,000

To record the dividend revenue from Ramirez Fashion:

June 30, 2019

EXERCISE 17.15 (Continued)

To record the investment at fair value:

December 31, 2019

Fair Value Adjustment …………………………..…………………. 20,000

Unrealized Holding Gain or Loss—Income …………. 20,000*

January 1, 2019

Equity Investments ………………………………………………….. 67,500

Cash [(30,000 X 25%) X $9] ………………………………… 67,500

June 15, 2019

Cash ($36,000 X 25%) ………………………………………………. 9,000

Equity Investments …………………………………………… 9,000

EXERCISE 17.16 (10–15 minutes)

(a) £130,000, the increase to the Investment account.

(b) If the dividend payout ratio is 40%, then 40% of the net income is their

EXERCISE 17.17 (10–15 minutes)

1. Equity Investments (300 shares X £40) …………….. 12,000

Cash ……………………………………………………. 12,000

EXERCISE 17.18 (15–20 minutes)

(a) Unrealized Holding Gain or Loss—Income …………. 5,900

Fair Value Adjustment (£311,500 – £305,600) .. 5,900

EXERCISE 17.18 (Continued)

(d)

Investments

Cost

Fair Value

Unrealized

Holding Gain

(Loss)

Beilman Corp., Ordinary

£180,000

£175,000

£(5,000)

McDowell Corp., Ordinary

52,500

50,400

(2,100)

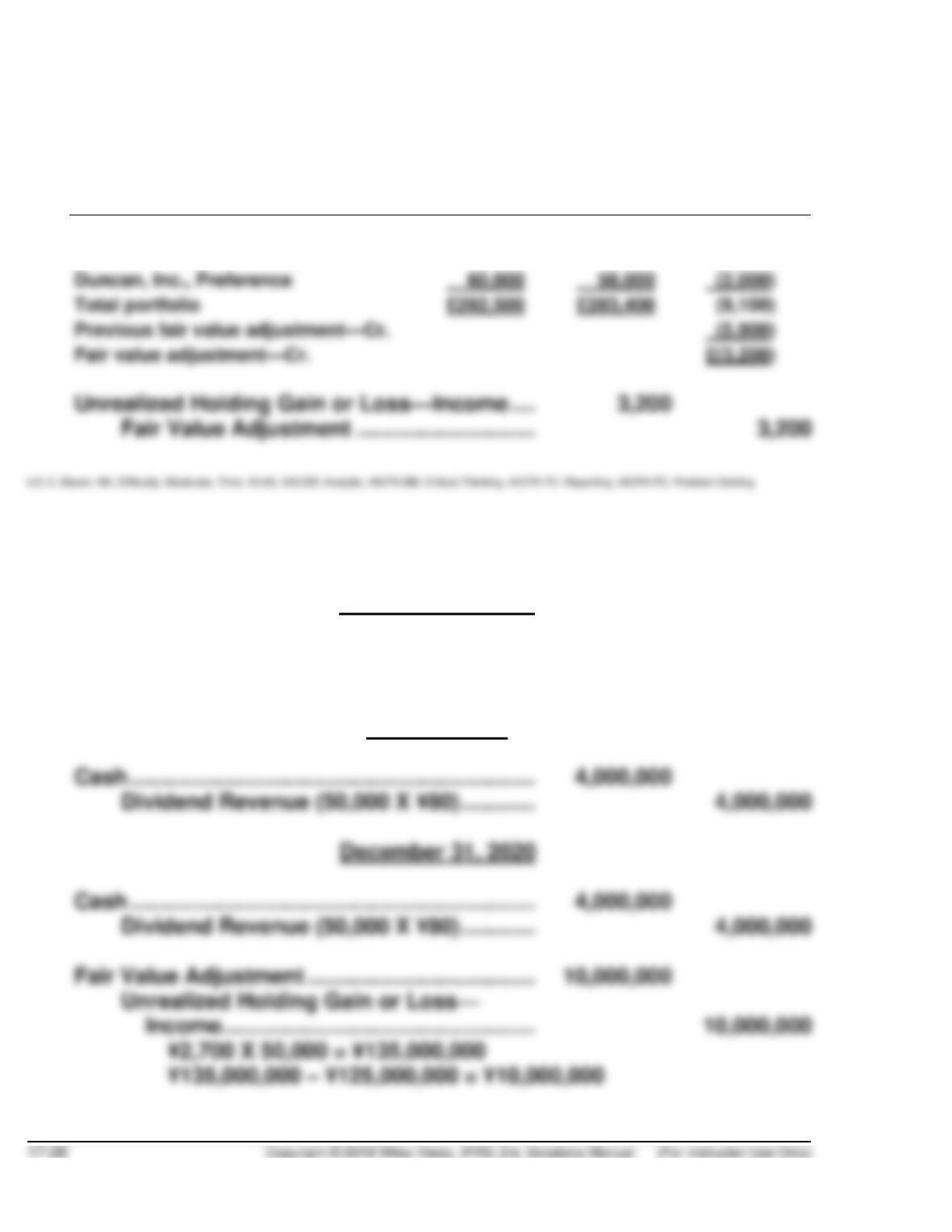

Duncan, Inc., Preference

Total portfolio

(9,100)

Previous fair value adjustment—Cr.

Fair value adjustment—Cr.

£(3,200)

EXERCISE 17.19 (15–20 minutes)

(a) December 31, 2019

Equity Investments …………………………………… 125,000,000

Cash …………………………………………………. 125,000,000

June 30, 2020

EXERCISE 17.19 (Continued)

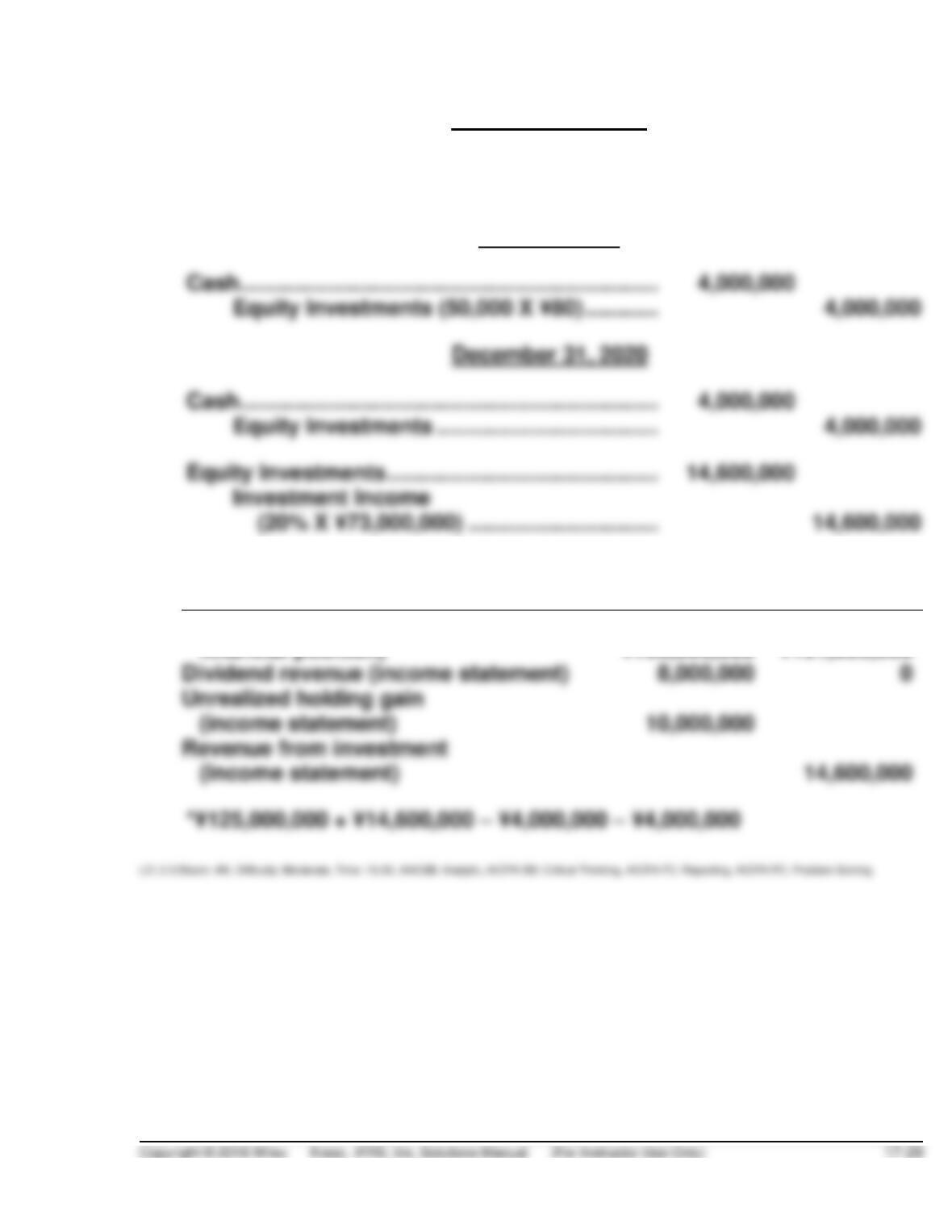

(b) December 31, 2019

Equity Investments …………………………………….. 125,000,000

Cash …………………………………………………… 125,000,000

June 30, 2020

(c)

Fair Value

Method

Equity Method

Investment amount (statement of

financial position)

¥135,000,000

*¥131,600,000*

Dividend revenue (income statement)

EXERCISE 17.20 (10–15 minutes)

Equity Investments ………………………………………….. 200,000

Cash ………………………………………………………… 200,000

EXERCISE 17.21 (15–20 minutes)

(a) The entry to record the impairment is as follows:

December 31, 2019

Loss on Impairment ($800,000 – $740,000) ………. 60,000

Allowance for Impaired Debt Investments … 60,000

EXERCISE 17.22 (10–15 minutes)

(a) Contractual cash flow

[(€400,000 X .10 X 3) + €400,000]……………………. €520,000

(b) Loss on Impairment ………………………………………… 49,998

Allowance for Impaired Debt Investment …… 49,998

(c) Since Komissarov will now receive the contractual cash flow (€520,000)

EXERCISE 17.23 (20–25 minutes)

(a) December 31, 2020

(b) December 31, 2021

Allowance for Impaired Debt Investments

($2,950,000 − $2,500,000) ……………… 450,000

Reversal of Impairment Loss ……………………. 450,000

(d)

Loss on Impairment …………………………………………. 250,000

Unrealized Holding Gain or Loss − Equity ………… 550,000

*EXERCISE 17.24 (15–20 minutes)

(a) January 2, 2019

Call Option ……………………………………………………. 300

Cash ………………………………………………………….. 300

*EXERCISE 17.25 (20–25 minutes)

(a)

6/30/19

(b)

12/31/19

Fixed-rate debt

€100,000

€100,000

Fixed rate (6% ÷ 2)

X3%

X3%

Semiannual debt payment

€ 3,000

€ 3,000

Swap fixed receipt

(3,000)

(3,000)

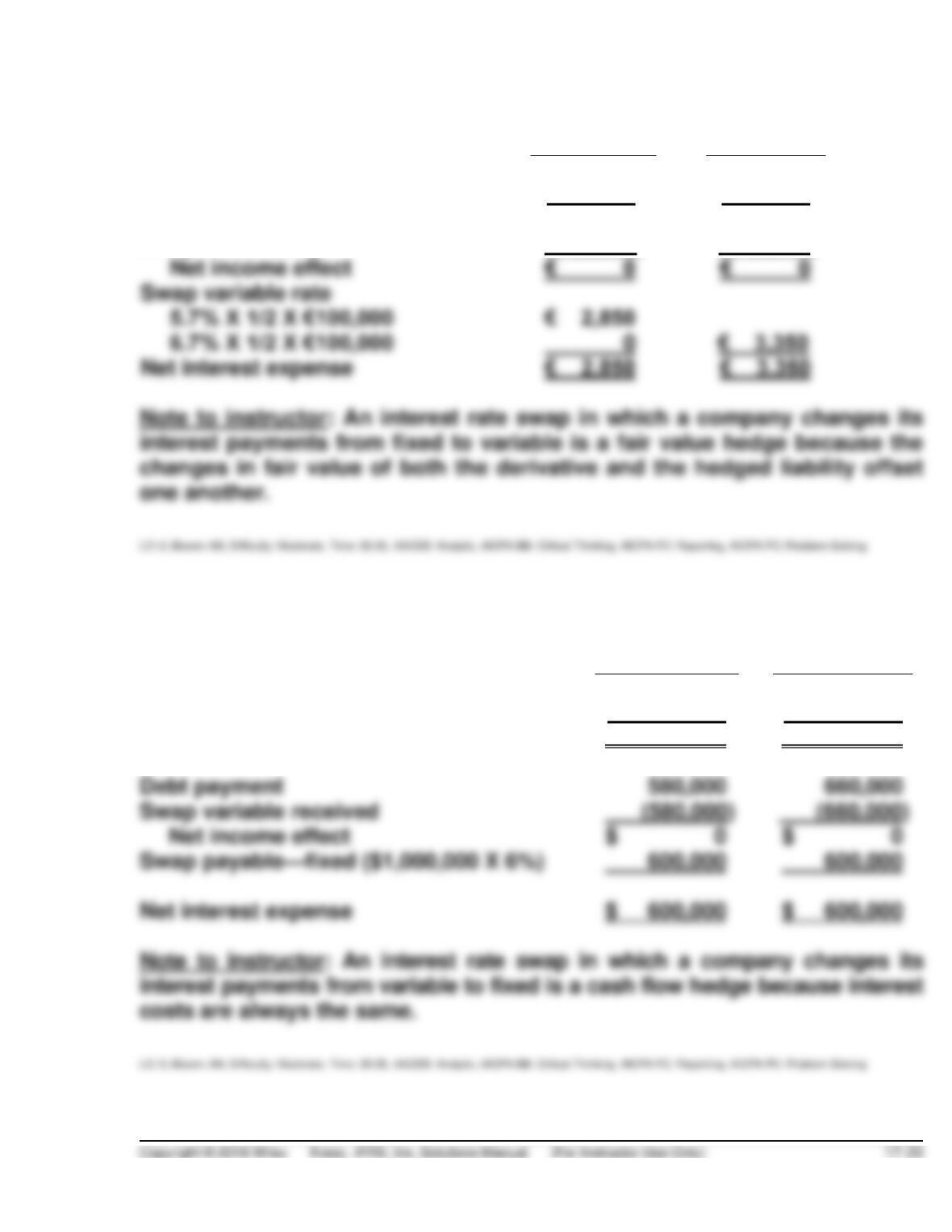

Net income effect

Swap variable rate

Net interest expense

€ 2,850

€ 3,350

*EXERCISE 17.26 (20–25 minutes)

(a)

12/31/19

(b)

12/31/20

Variable-rate debt

$10,000,000

$10,000,000

Variable rate

X5.8%

X6.6%

Debt payment

$ 580,000

$ 660,000

Debt payment

580,000

660,000

Swap variable received

(580,000)

(660,000)

Net income effect

$ 0

$ 0

600,000

600,000

Net interest expense

$ 600,000

$ 600,000

*EXERCISE 17.27 (15–20 minutes)

(a) Interest Expense ……………………………………………… 75,000

Cash (7.5% X £1,000,000) …………………………... 75,000

*EXERCISE 17.28 (20–25 minutes)

(a) August 15, 2019

Call Option ……………………………………………………… 360

Cash ………………………………………………………… 360

(c) December 31, 2019

Unrealized Holding Gain or Loss—Income ………… 800

Call Option ($2 X 400) ……………………………….. 800

Unrealized Holding Gain or Loss—Income ………… 115

Call Option ($180 – $65) …………………………….. 115

(d) January 15, 2020

Call Option ($1 X 400) ………………………………………. 400

*Value of Call Option at settlement:

Call Option

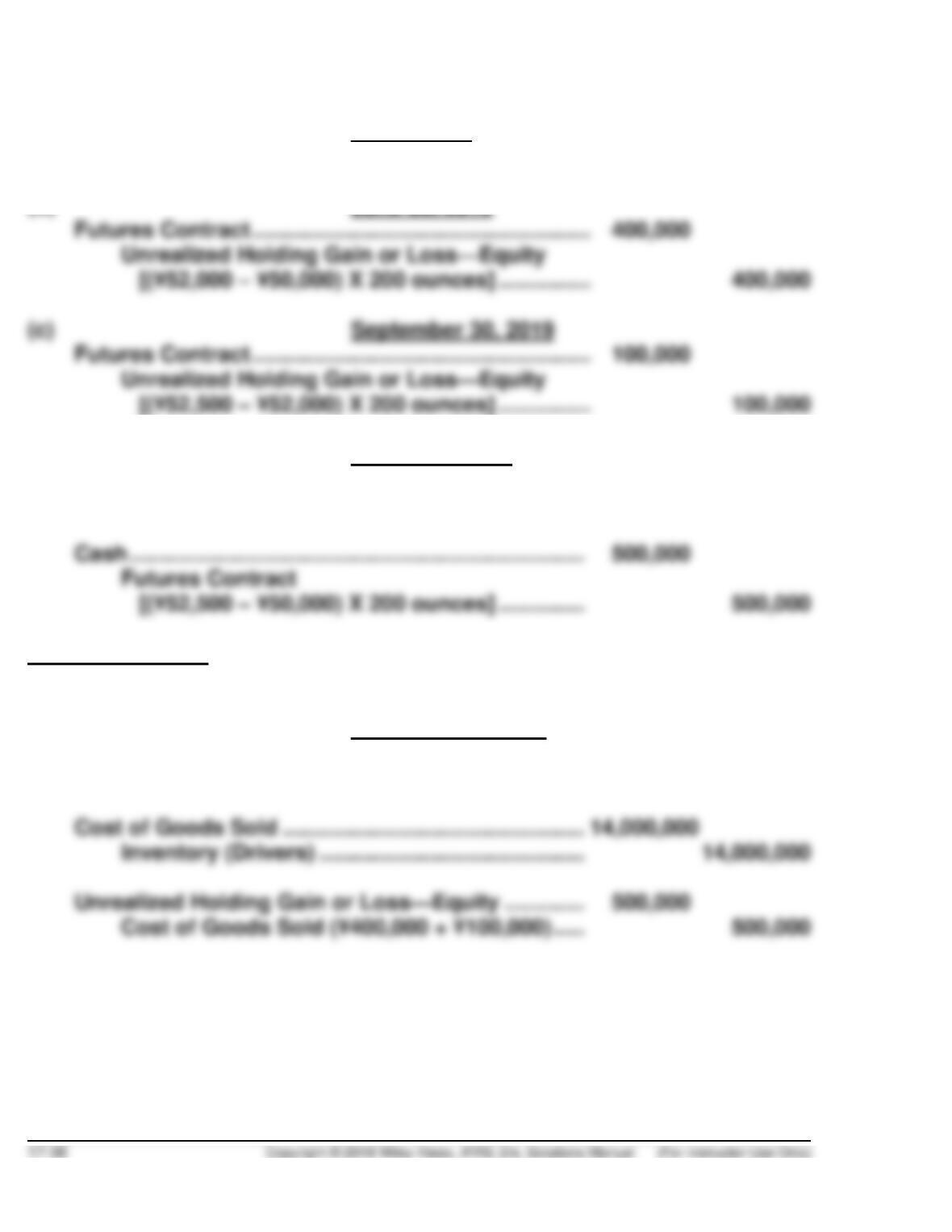

*EXERCISE 17.29 (25–30 minutes)

(a) May 1, 2019

Memorandum entry to indicate entering into the futures contract.

(b) June 30, 2019

(d) October 5, 2019

Titanium Inventory …………………………………………… 10,500,000

Cash (¥52,500 X 200 ounces) …………………….. 10,500,000

Note to instructor: In practice, futures contracts are settled on a daily basis;

for our purposes, we show only one settlement for the entire amount.

(e) December 15, 2019

Cash ……………………………………………………………….. 25,000,000

Sales Revenue ………………………………………….. 25,000,000

*EXERCISE 17.29 (Continued)

(f) CHOI GOLF.

Partial Income Statement

For the Quarter Ended December 31, 2019

Sales revenue …………………………………………………. ¥25,000,000

TIME AND PURPOSE OF PROBLEMS

Problem 17.1 (Time 20–30 minutes)

Purpose—the student is required to prepare journal entries and adjusting entries covering a three-year

Problem 17.2 (Time 30–40 minutes)

Purpose—The student is required to prepare journal entries and adjusting entries for debt investments,

along with an amortization schedule. The fair value option is addressed.

Problem 17.3 (Time 25–30 minutes)

Purpose—to provide the student with an understanding of the differentiation in accounting treatments

Problem 17.4 (Time 25–35 minutes)

Purpose—the student is required to distinguish between the existence of a bond premium or discount.

Problem 17.5 (Time 25–35 minutes)

Purpose—the student is required to prepare journal entries for the sale and purchase of equity

Problem 17.6 (Time 25–35 minutes)

Problem 17.7 (Time 25–35 minutes)

Problem 17.8 (Time 20–30 minutes)

Purpose—to provide the student with an understanding of the accounting for equity investments. The

Problem 17.9 (Time 20–30 minutes)

Purpose—to provide the student with an understanding of the proper accounting treatment with respect

Problem 17.10 (Time 30–40 minutes)

Purpose—to provide the student with an understanding of the reporting problems associated with non–

Problem 17.11 (Time 20–30 minutes)

Purpose—to provide the student with an understanding of the reporting problems associated with

Time and Purpose of Problems (Continued)

*Problem 17.12 (Time 20–25 minutes)

Purpose—the student is required to prepare the entries at purchase, throughout the life, and at expiration

for a stand alone derivative (call option).

*Problem 17.15 (Time 30–40 minutes)

Purpose—the student is provided with an opportunity to prepare the entries for a fair value hedge in the

context of an interest rate swap, including how the effects of the swap will be reported in the financial

statements.

SOLUTIONS TO PROBLEMS

PROBLEM 17.1

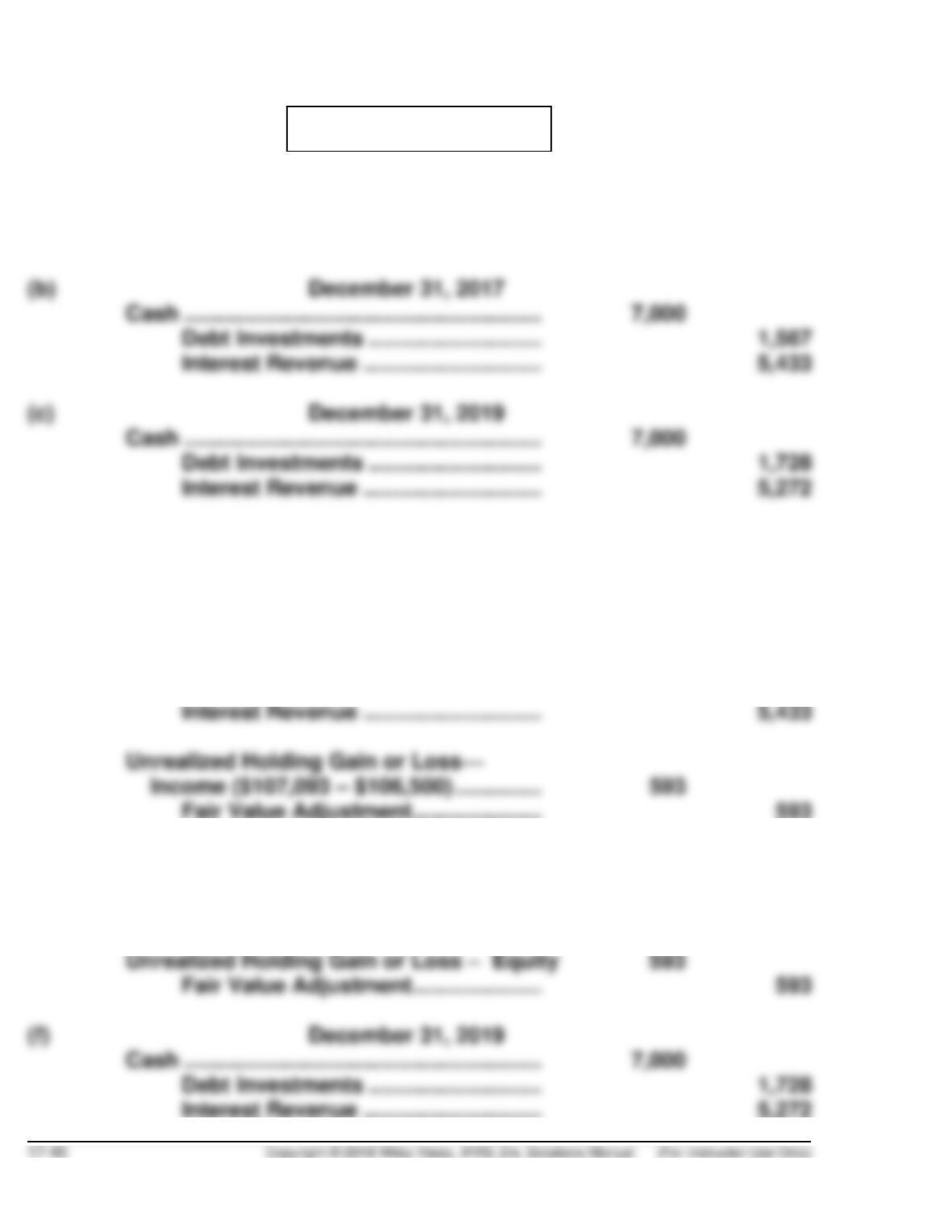

(a) December 31, 2016

Debt Investments ……………………………….. 108,660

Cash …………………………………………. 108,660

(d) December 31, 2016

Debt Investments ……………………………….. 108,660

Cash …………………………………………. 108,660

(e) December 31, 2017

1. Cash …………………………………………………. 7,000

Debt Investments ………………………. 1,567

2. Cash …………………………………………………. 7,000

Debt Investments ………………………. 1,567

Interest Revenue ……………………….. 5,433