Time and Purpose of Problems (Continued)

Problem 19.8 (Time 40–50 minutes)

Purpose—to test a student’s understanding of the relationships that exist in the subject area of

accounting for income taxes. The student is required to compute and classify deferred income taxes for

Problem 19.9 (Time 40–50 minutes)

Purpose—to test a student’s ability to compute and classify deferred taxes for three temporary differences

SOLUTIONS TO PROBLEMS

PROBLEM 19.1

(a) X(.40) = $320,000 taxes due for 2019

X = $320,000 ÷ .40

X = $800,000 taxable income for 2019

2020

Income Tax Expense

($343,000 + $7,000 – $10,500) ………………………… 339,500

Deferred Tax Liability [($120,000 ÷ 4) X .35] ……….. 10,500

Income Taxes Payable ($980,000 X .35) ………. 343,000

Deferred Tax Asset [($40,000 ÷ 2) X .35] ……… 7,000

PROBLEM 19.2

(a) Before deferred taxes can be computed, the amount of temporary dif-

ference originating (reversing) each period and the resulting cumulative

temporary difference at each year-end must be computed:

2018

2019

2020

2021

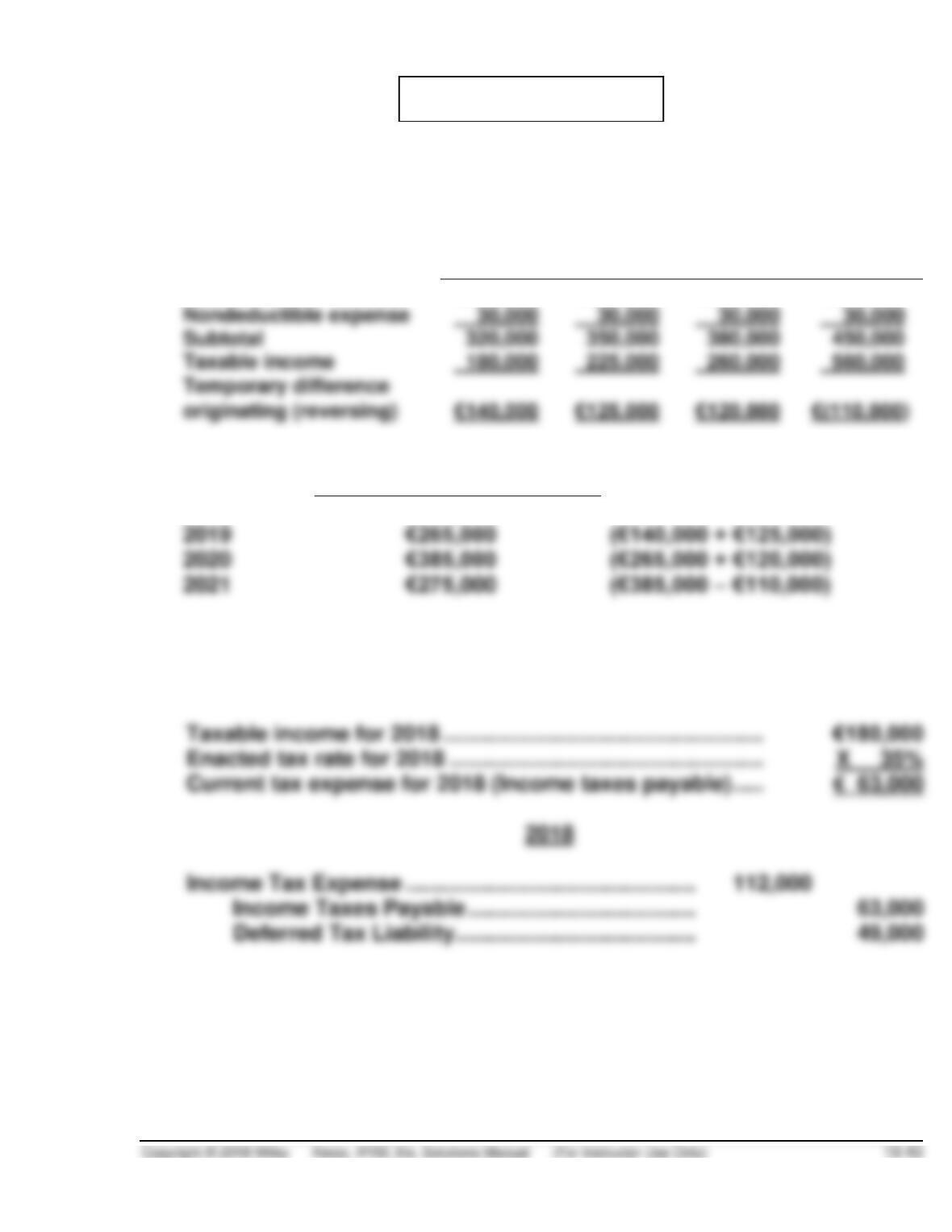

Pretax financial income

€290,000

€320,000

€350,000

(€420,000

Cumulative Temporary

Difference At End of Year

2018

€140,000

2019

€265,000

2020

€385,000

2021

Because the temporary difference causes pretax financial income to

exceed taxable income in the period it originates, the temporary differ–

ence will cause future taxable amounts.

PROBLEM 19.2 (Continued)

The deferred taxes at the end of 2018 would be computed as follows:

Temporary

Difference

Future Taxable

(Deductible) Amounts

Tax

Rate

Deferred Tax

(Asset)

Liability

Depreciation

€140,000

35%

€49,000

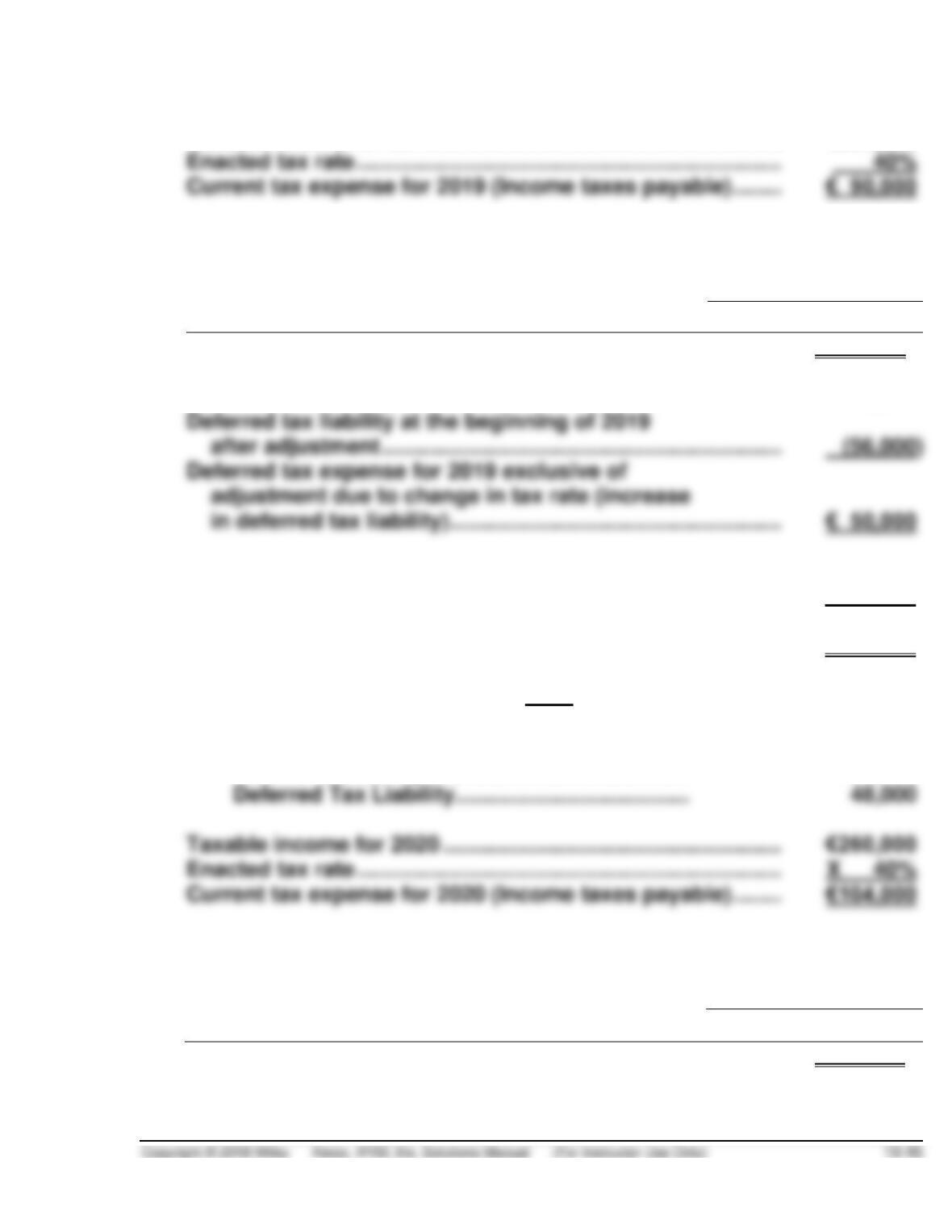

Deferred tax liability at the end of 2018 ………………………… € 49,000

Deferred tax liability at the beginning of 2018 ………………. 0

2019

Income Tax Expense ……………………………………….. 7,000*

Deferred Tax Liability ………………………………… 7,000

*The adjustment due to the change in the tax rate is computed as

follows:

Cumulative temporary difference at the end

of 2018 ……………………………………………………………………. €140,000

Newly enacted tax rate for future years ………………………… X 40%

PROBLEM 19.2 (Continued)

Taxable income for 2019 ………………………………………………. €225,000

The deferred taxes at December 31, 2019, are computed as follows:

Temporary

Difference

Future Taxable

(Deductible) Amounts

Tax

Rate

Deferred Tax

(Asset)

Liability

Depreciation

€265,000

40%

€106,000

Deferred tax liability at the end of 2019 ………………………….. €106,000

Deferred tax expense for 2019 ………………………………………. € 50,000

Current tax expense for 2019 (Income taxes payable) …….. 90,000

Income tax expense (total) for 2019, exclusive

of adjustment due to change in tax rate …………………….. €140,000

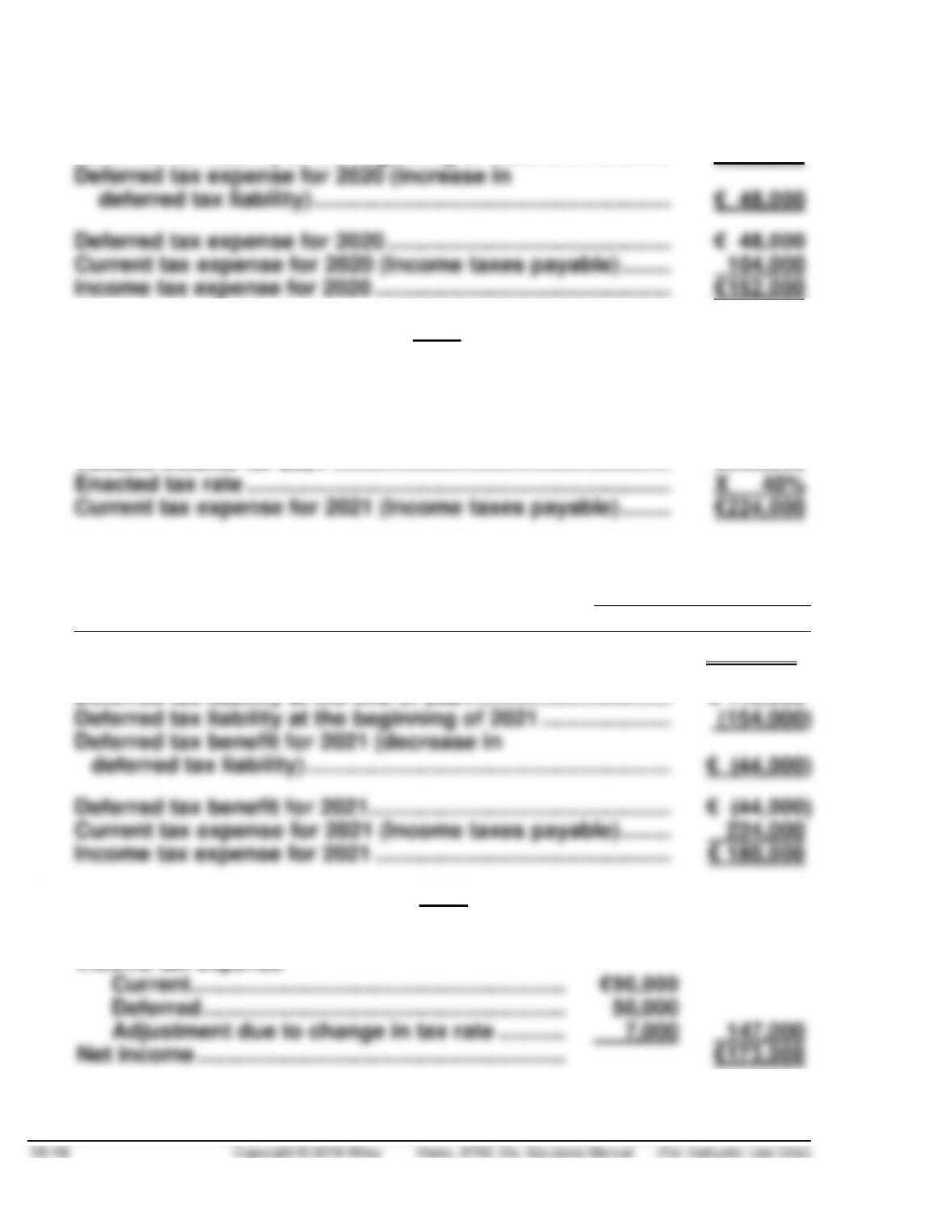

2020

Income Tax Expense ………………………………………. 152,000

Income Taxes Payable ……………………………… 104,000

The deferred taxes at December 31, 2020, are computed as follows:

Temporary

Difference

Future Taxable

(Deductible) Amounts

Tax

Rate

Deferred Tax

(Asset)

Liability

Depreciation

€385,000

40%

€154,000

PROBLEM 19.2 (Continued)

Deferred tax liability at the end of 2020 ………………………….. €154,000

Deferred tax liability at the beginning of 2020 ………………… 106,000

2021

Income Tax Expense …………………………………….. 180,000

Deferred Tax Liability ……………………………………. 44,000

Income Taxes Payable ……………………………. 224,000

Taxable income for 2021 ………………………………………………. €560,000

The deferred taxes at December 31, 2021, are computed as follows:

Temporary

Difference

Future Taxable

(Deductible) Amounts

Tax

Rate

Deferred Tax

(Asset)

Liability

Depreciation

€275,000

40%

€110,000

(b) 2019

Income before income taxes …………………………. €320,000

LO: 1,2, Bloom: AP, Difficulty: Complex, Time: 50-60, AACSB: Analytic, AICPA BB: Critical Thinking, AICPA FC: Reporting, AICPA PC: Problem Solving

PROBLEM 19.3

Book Depreciation

Tax Depreciation

Difference

2018

€ 150,000

€ 120,000*

(€ 30,000

2019

150,000

240,000

(90,000)

2020

150,000

240,000

(90,000)

2021

150,000

240,000

(90,000)

2023

150,000

120,000*

30,000

2024

150,000

2025

€1,200,000

(€ 0

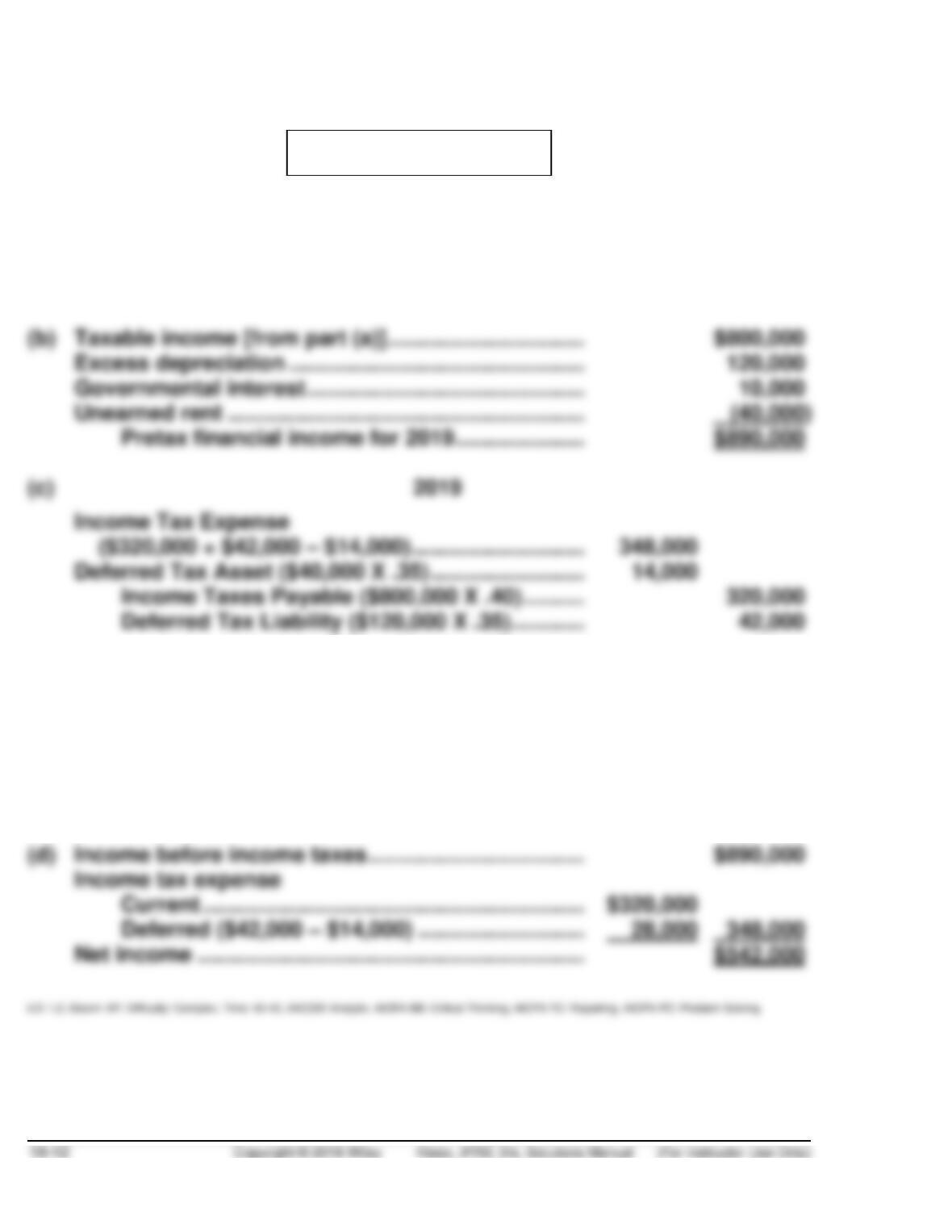

(a) Pretax financial income for 2019 ………………………………… €1,400,000

Nontaxable interest …………………………………………………… (60,000)

Income taxes payable for 2019 …………………………………… € 437,500

(b) Income Tax Expense …………………………………….. 469,000

PROBLEM 19.3 (Continued)

Scheduling—End of 2019

Future Years

2020

2021

2022

Future taxable (deductible)

amounts

€(90,000)

€(90,000)

€(90,000)

Enacted tax rate

Deferred tax (asset) liability

Future Years

2023

2024

2025

Total

Future taxable (deductible)

amounts

€30,000

€150,000

€150,000

€60,000

Enacted tax rate

Deferred tax (asset) liability

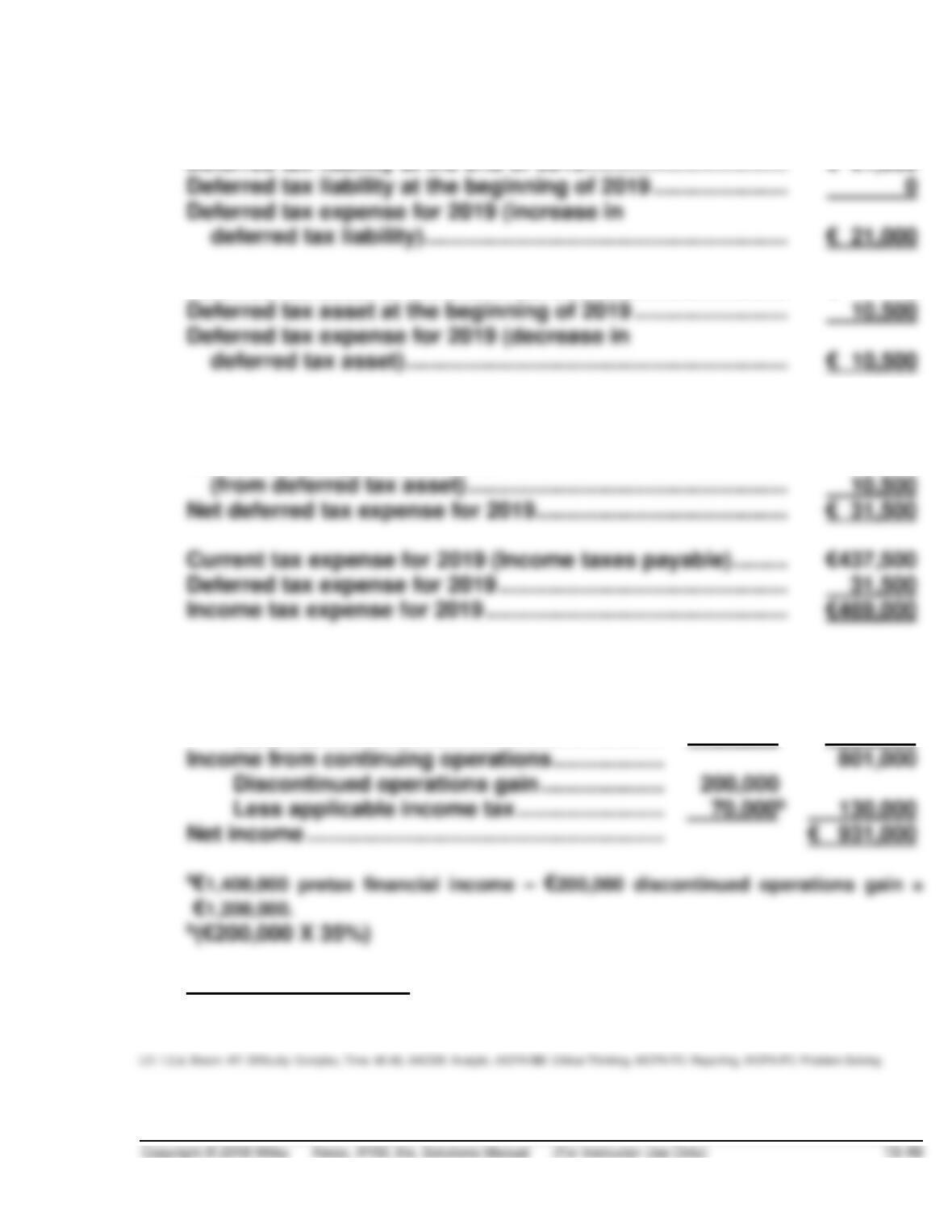

The net deferred tax liability at December 31, 2019, is €21,000.

Scheduling—End of 2018

Future Years

2019

2020

2021

2022

Enacted tax rate

Deferred tax (asset) liability

Future taxable (deductible)

Future Years

2023

2024

2025

Total

Enacted tax rate

Deferred tax (asset) liability

Future taxable (deductible)

PROBLEM 19.3 (Continued)

The net deferred tax asset at December 31, 2018, is €10,500.

Deferred tax asset at the end of 2019 ……………………………… € 0

Deferred tax expense for 2019

(from deferred tax liability) …………………………………………. € 21,000

Deferred tax expense for 2019

(c) Income before income taxes ………………………… €1,200,000a

Income tax expense

Current (€437,500 – €70,000b) ………………… €367,500

Deferred ………………………………………………. 31,500 399,000

(d) Non-current liabilities

Deferred tax liability ……………………………………. €21,000

PROBLEM 19.4

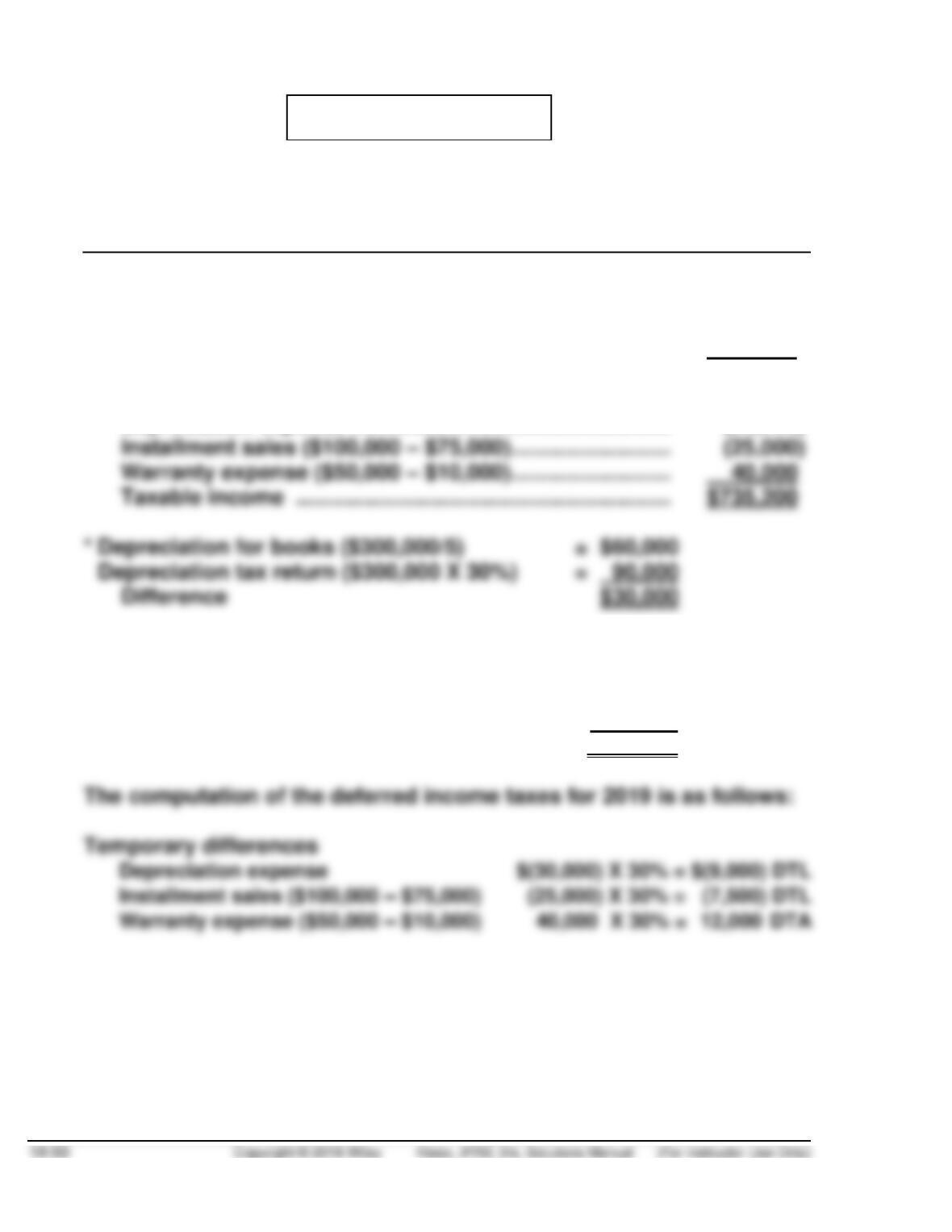

(a) Schedule of Pretax Financial Income

and Taxable Income for 2019

Pretax financial income …………………………..………………….. $750,000

Permanent differences

Bond interest revenue……………………………………………. (4,000)

Pollution fines ………………………………………………………. 4,200

750,200

Temporary differences

Depreciation expense ……………………………………………. (30,000)*

The income taxes payable for 2019 is as follows:

Taxable income …………………………..……. $735,200

Tax rate ……………………………………………. X 30%

Income taxes payable ……………………….. $220,560

PROBLEM 19.4 (Continued)

(b) The journal entry to record income taxes payable, income tax expense

and deferred income taxes is as follows:

Income Tax Expense ……………………………………… 225,060*

*Deferred tax expense for 2019

(from deferred tax liability) ($9,000 + $7,500) …. $ 16,500

Deferred tax benefit for 2019

PROBLEM 19.5

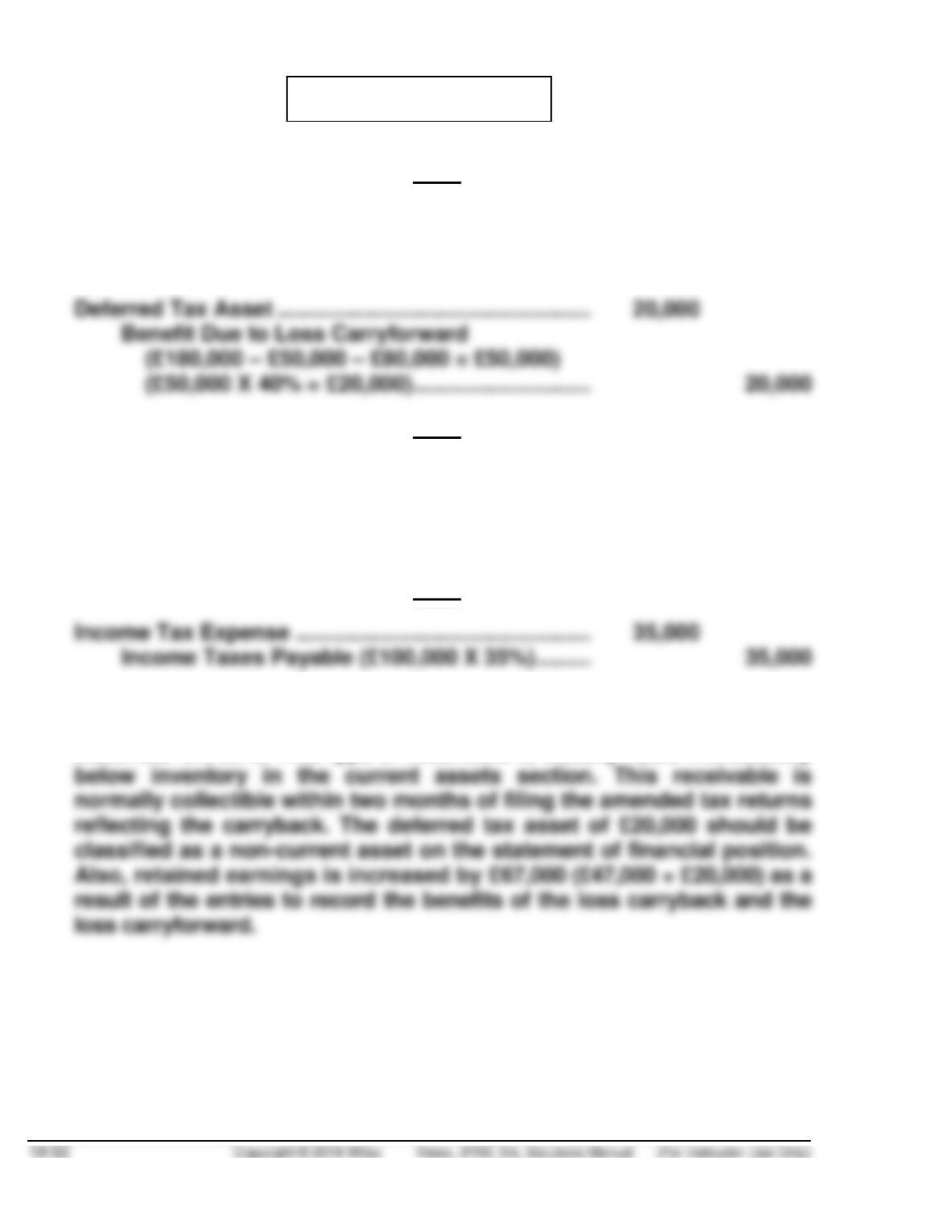

(a) 2018

Income Tax Refund Receivable

[(£50,000 X 30%) + (£80,000 X 40%)] ……………….. 47,000

Benefit Due to Loss Carryback …………………… 47,000

2019

Income Tax Expense ………………………………………… 28,000

Deferred Tax Asset …………………………………….. 20,000

Income Taxes Payable

[(£70,000 – £50,000) X 40%] …………………….. 8,000

2020

(b) The income tax refund receivable account totaling £47,000 will be

reported under current assets on the statement of financial position at

December 31, 2018. This type of receivable is usually listed immediately

PROBLEM 19.5 (Continued)

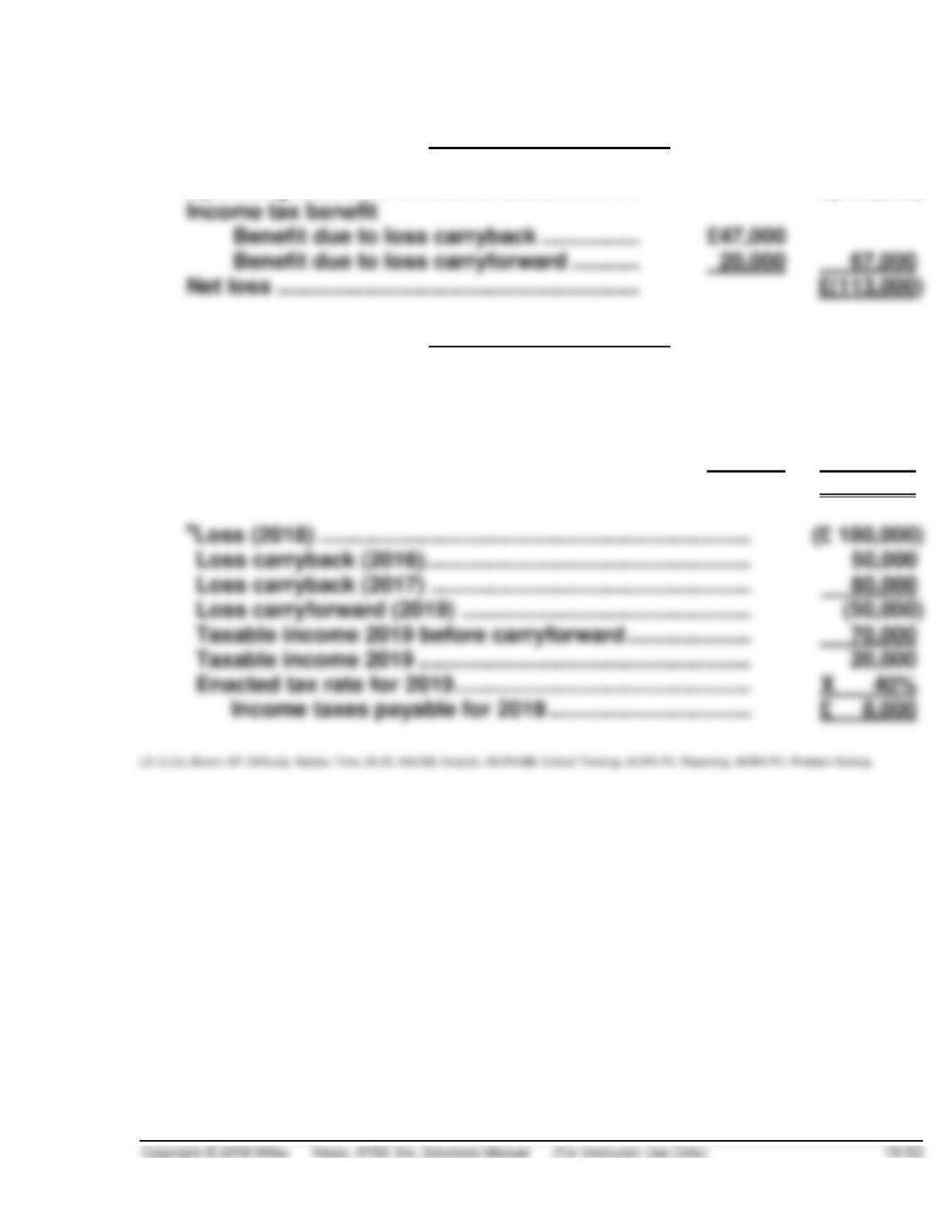

(c) 2018 Income Statement

Operating loss before income taxes …………. £(180,000)

(d) 2019 Income Statement

Income before income taxes …………………….. £ 70,000

Income tax expense

Current …………………………………………….. £ 8,000a

Deferred …………………………………………… 20,000 28,000

Net income ……………………………………………… £ 42,000

PROBLEM 19.6

1.

Temporary

Difference

Future Taxable

(Deductible) Amounts

Tax

Rate

Deferred Tax

(Asset)

Liability

2019

$ 300

30%a

$ 90

2020

300

30%b

90

2021

300

30%c

90

2022

35%d

2023

300

35%e

aTax rate for 2019. dTax rate for 2022

bTax rate for 2020. eTax rate for 2023.

cTax rate for 2021.

MOONEY CO.

Statement of Financial Position

December 31, 2018

2.

Temporary

Difference

Future Taxable

(Deductible) Amounts

Tax

Rate

Deferred Tax

(Asset)

Liability

2019

$ 300

30%a

$ 90

2020

300

30%b

90

2021

300

30%c

90

2021

30%c

2022

300

35%d

PROBLEM 19.6 (Continued)

ROESCH CO.

Statement of Financial Position

December 31, 2018

Other assets (non-current)

PROBLEM 19.7

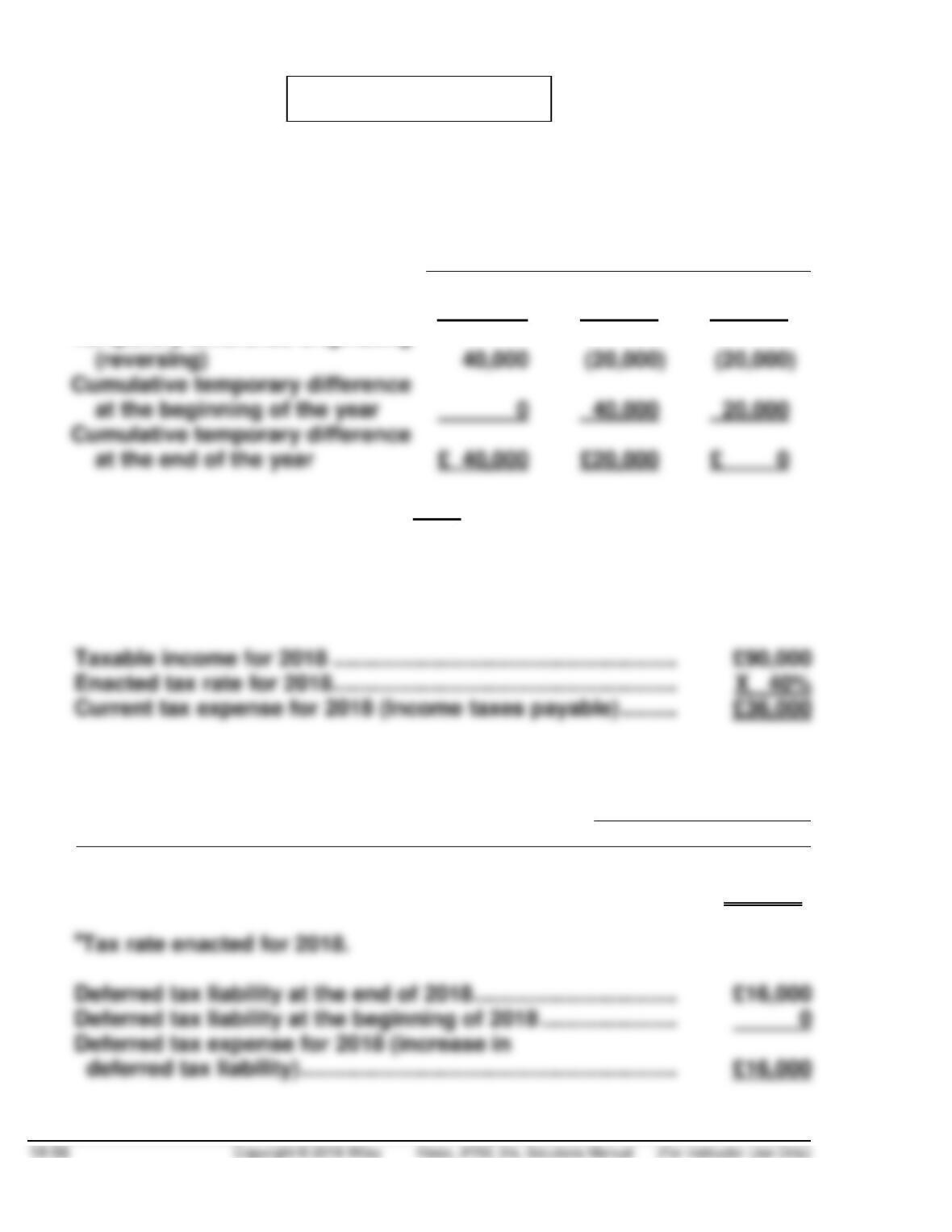

(a) Before deferred taxes can be computed, the amount of cumulative tem-

porary difference existing at the end of each year must be computed:

2018

2019

2020

Pretax financial income

£130,000

(£70,000

(£70,000

Taxable income

90,000

( 90,000

( 90,000

Cumulative temporary difference

Temporary difference originating

(

2018

Income Tax Expense ……………………………………….. 52,000

Income Taxes Payable ………………………………. 36,000

Deferred Tax Liability ………………………………… 16,000

Temporary

Difference

Future Taxable

(Deductible)

Amounts

Tax

Rate

December 31, 2018

Deferred Tax

(Asset)

Liability

Installment Accounts

Receivable

(

£ 40,000

40%a

£16,000

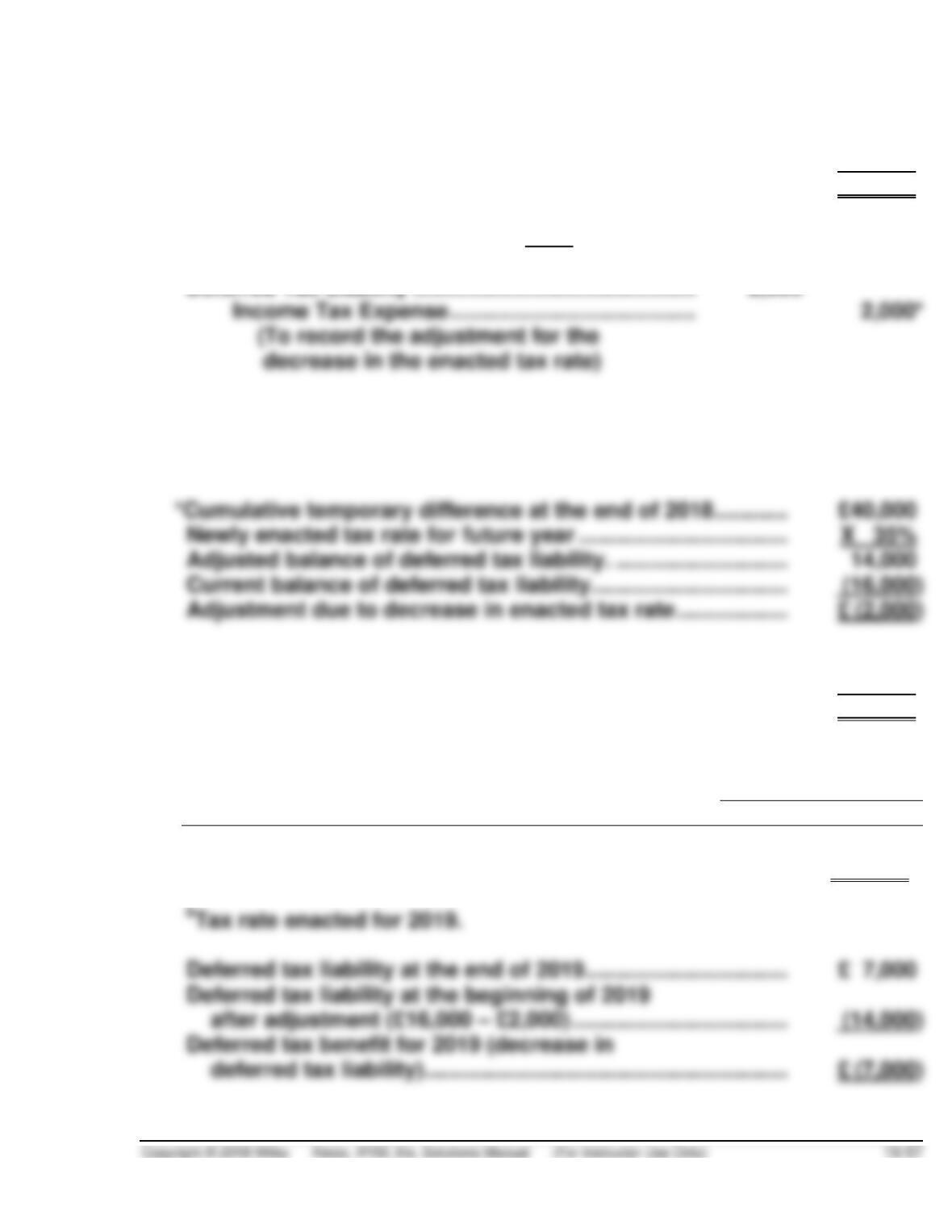

PROBLEM 19.7 (Continued)

Deferred tax expense for 2018 ……………………………………….. £16,000

Current tax expense for 2018 (Income taxes payable) ……… 36,000

Income tax expense for 2018 …………………………………………. £52,000

2019

Income Tax Expense ……………………………………….. 24,500

Deferred Tax Liability ………………………………………. 7,000

Income Taxes Payable ………………………………. 31,500

Taxable income for 2019 ……………………………………………….. £90,000

Enacted tax rate for 2019 ………………………………………………. X 35%

Current tax expense for 2019 (Income taxes payable) ……… £31,500

Temporary

Difference

Future Taxable

(Deductible) Amounts

Tax

Rate

December 31, 2019

Deferred Tax

(Asset)

Liability

Installment Accounts

Receivable

£20,000

35%b

£ 7,000

PROBLEM 19.7 (Continued)

Deferred tax benefit for 2019 ………………………………………….. £ (7,000)

2020

Income Tax Expense ……………………………………….. 24,500

Temporary

Difference

Future Taxable

(Deductible)

Amounts

Tax

Rate

December 31, 2020

Deferred Tax

(Asset)

Liability

Installment Accounts

Receivable

(

£—0—

30%

£—0—

Deferred tax liability at the end of 2020 …………………………... £ 0

Deferred tax liability at the beginning of 2020 …………………. 7,000

Income tax expense for 2020 …………………………………………. £24,500

(b) December 31, 2018

Non-current liabilities

Deferred tax liability ……………………………………………….. £16,000

December 31, 2019

Non-current liabilities

Deferred tax liability ……………………………………………….. £ 7,000

December 31, 2020

PROBLEM 19.7 (Continued)

(c) 2018

Income before income taxes ………………………………… £130,000

Income tax expense

2019

Income before income taxes ………………………………… £70,000

Income tax expense

2020

Income before income taxes ………………………………… £70,000

Income tax expense

PROBLEM 19.8

(a)

Temporary

Difference

Future Taxable

(Deductible)

Amounts

Tax

Rate

Deferred Tax

(Asset)

Liability

Depreciation

¥120,000,000*

40%

¥48,000,000

(b) Income Tax Expense ……………………………… 178,000,000

Deferred Tax Liability ………………………. 48,000,000

Income Taxes Payable …………………….. 130,000,000

¥130,000,000 taxes due for 2018 ÷ 40% 2018

tax rate = ¥325,000,000 taxable income for 2018.

Taxable income for 2018 ………………………………………… ¥325,000,000

Tax rate …………………………………………………………………. X 40%

(c) Income before income taxes …………… ¥445,000,000a

Income tax expense

Current …………………………………… ¥130,000,000

Deferred …………………………………. 48,000,000 178,000,000