PROBLEM 11.2

Depreciation Expense

2019

2020

(a)

Straight-line:

(€89,000 – €5,000) ÷ 7 = €12,000/yr.

2019: €12,000 X 7/12

€7,000

2020: €12,000

€12,000

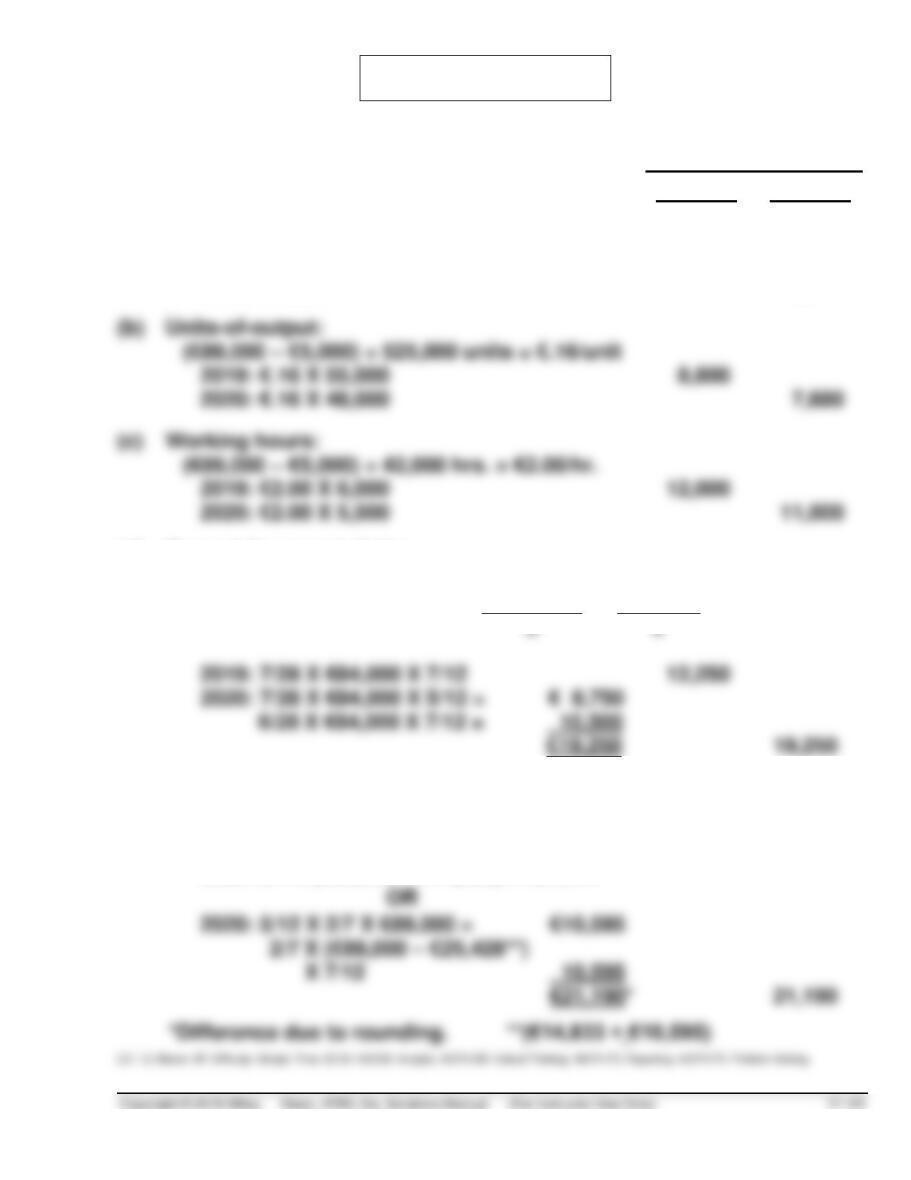

(b)

(€89,000 – €5,000) ÷ 525,000 units = €.16/unit

2019: €.16 X 55,000

2020: €.16 X 48,000

(c)

Working hours:

(€89,000 – €5,000) ÷ 42,000 hrs. = €2.00/hr.

2019: €2.00 X 6,000

2020: €2.00 X 5,500

(d)

Sum-of-the-years’-digits:

1 + 2 + 3 + 4 + 5 + 6 + 7 = 28 or

n(n + 1)

=

7 x 8

= 28

2019: 7/28 X €84,000 X 7/12

2020: 7/28 X €84,000 X 5/12 = € 8,750

6/28 X €84,000 X 7/12 = 10,500

19,250

(e)

Declining-balance:

Rate = 2/7 or (100% ÷ 7) x 2

2019: 7/12 X 2/7 X €89,000

14,833

2020: 2/7 X (€89,000 – €14,833) = €21,191

2020: 5/12 X 2/7 X €89,000 = €10,595

€21,190*

21,190

PROBLEM 11.3

(a)

Depreciation Expense ……………………………………………..

3,900

Accumulated Depreciation—Asset A

(5/55* X [£46,000 – £3,100]) …………………………..

3,900

*[10 x (10 + 1)] ÷ 2

Accumulated Depreciation—Asset A ……………………….

Asset A (£46,000 – £13,000) …………………………..

Gain on Disposal of Plant Assets** ………………….

2,100

**($46,000 – $35,900) – $13,000

(b)

Depreciation Expense ……………………………………………..

6,720

Accumulated Depreciation—Asset B

([£51,000 – £3,000] ÷ [15,000 X 2,100]) ……………

6,720

(c)

Depreciation Expense ……………………………………………..

6,000

Accumulated Depreciation—Asset C

([£80,000 – £15,000 – £5,000] ÷ 10) …………………

6,000

(d)

Asset E …………………………..………………………………………

Retained Earnings …………………………………………..

Depreciation Expense ……………………………………………..

Accumulated Depreciation—Asset E ……………….

5,600

Note: No correcting entry is needed for asset D. In 2019, Eshkol

records depreciation expense of £80,000 X [(100% ÷ 10) X 2] =

£16,000.

Depreciation Expense ……………………………………………..

16,000

Copyright © 2018 Wiley Kieso, IFRS, 3/e, Solutions Manual (For Instructor Use Only) 11–43

7

16,400

(46,200)

104,000

_______

30,400

(98,750)

(30,400)

________

Balances

Depreciation

Balances

Income effect

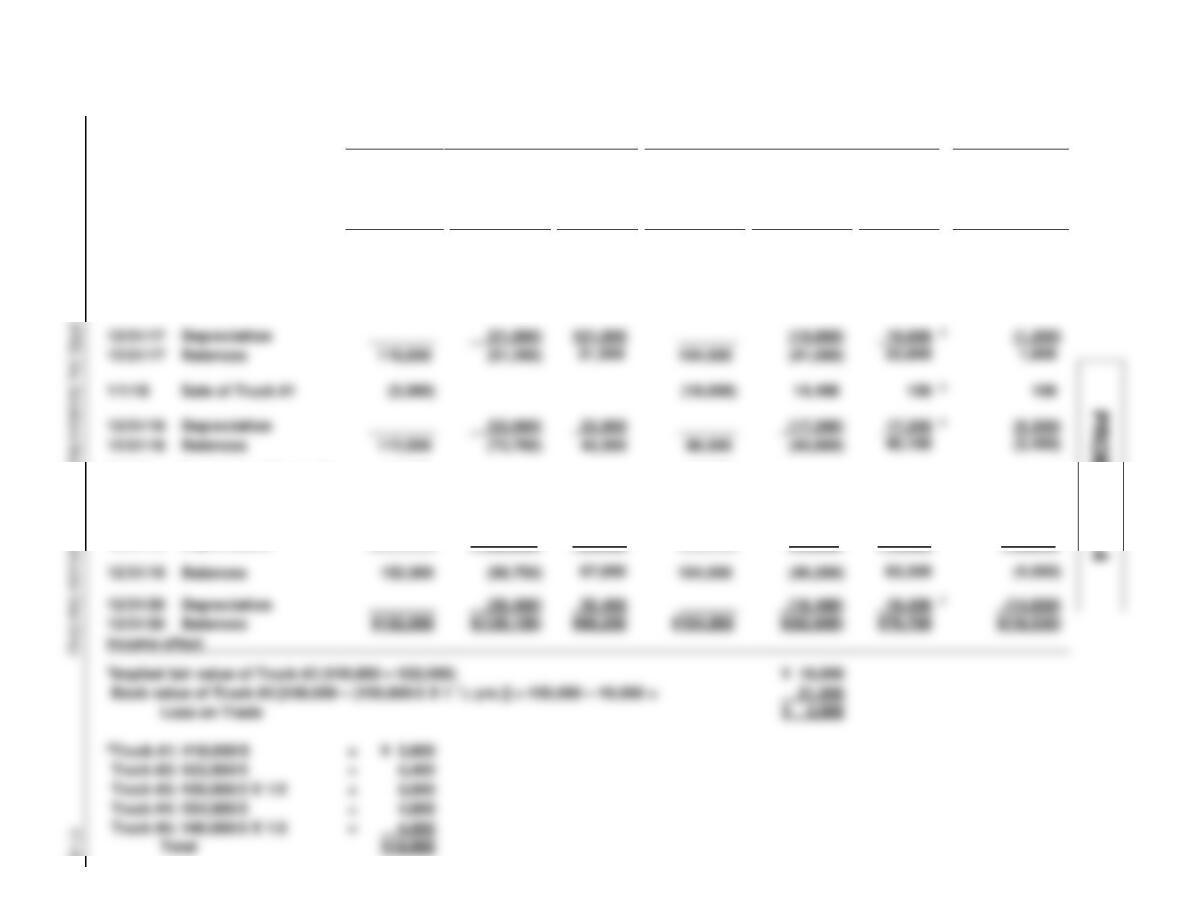

Loss on Trade

Truck #2: ¥22,000/5

Truck #5: ¥40,000/5 X 1/2

Total

12/31/19

Net

Income

Overstated

(Understated)

¥ 3,000

7,100

(8,250)

1

5

6

As Adjusted

Retained

Earnings

dr. (cr.)

¥ 3,000

6,400

16,800

Acc. Dep.,

Semitrucks

dr. (cr.)

¥(30,200)

9,000

14,400

(16,800)

Trucks

dr. (cr.)

¥94,000

40,000

(30,000)

42,000

(24,000)

_______

Per Company Books

Retained

Earnings

dr. (cr.)

(700)

25,050

Acc. Dep.

Semitrucks

dr. (cr.)

¥(30,200)

(25,050)

Trucks

dr. (cr.)

¥ 94,000

22,000

42,000

(2,500)

________

Balance

Purchase Truck #5

Trade Truck #3

Purchase of Truck #6

Disposal of Truck #4

Depreciation

(a)

1/1/17

7/1/17

7/1/19

7/1/19

12/31/19

2

3

4

19,800

(19,800)

(41,000)

14,400

_______

(18,000)

_______

¥21,000

22,500

(21,000)

(51,200)

________

Depreciation

Balances

Sale of Truck #1

Depreciation

12/31/17

12/31/17

12/31/18

PROBLEM 11.4 (Continued)

3Book value of Truck #1 [¥18,000 – (¥18,000/5 X 4 yrs.)] =

¥18,000 – ¥14,400 …………………………………………………….

= ¥3,600

Cash received on sale ……………………………………………………..

= (3,500)

¥22,000/5

=

¥24,000/5

=

¥40,000/5

=

5Book value of Truck #4 ¥24,000 – [(¥24,000/5 X 3 yrs.)] …….

= ¥9,600

Cash received (¥700 + ¥2,500) ………………………………………….

= (3,200)

Loss on disposal …………………………………………………….

¥6,400

6Truck #2:

¥22,000/5 X 1/2

=

¥ 2,200

¥24,000/5 X 1/2

=

¥42,000/5 X 1/2

=

4,200

7Truck #2:

(fully dep.)

=

¥40,000/5

=

¥42,000/5

=

(b)

Compound journal entry December 31, 2020:

Accumulated Depreciation—Trucks …………………..

66,550

Trucks ……………………………………………………..

48,000

Retained Earnings …………………………………….

Depreciation Expense 2020 ……………………….

14,000

PROBLEM 11.4 (Continued)

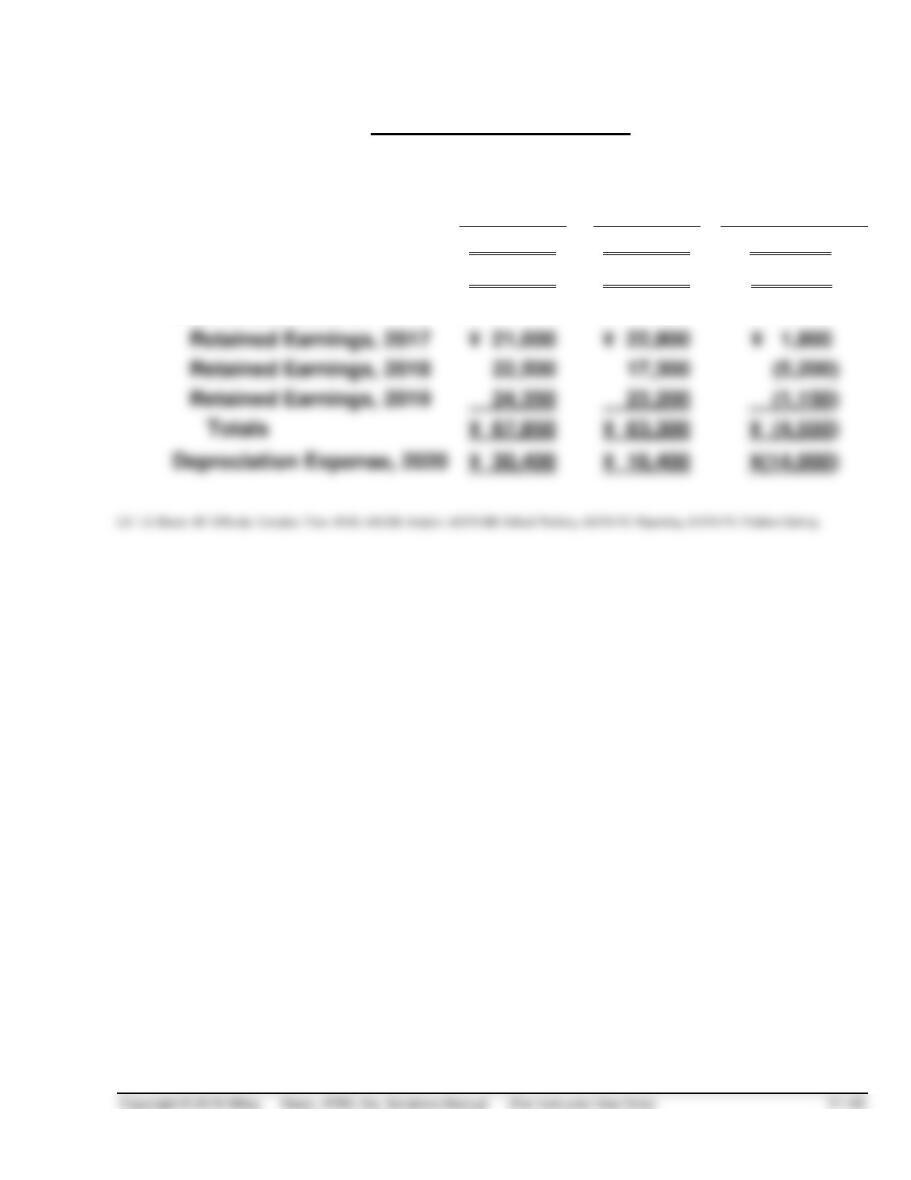

Summary of Adjustments:

Per

Books

As

Adjusted

Adjustment

Dr. or (Cr.)

Trucks

¥152,000

¥104,000

¥(48,000)

Accumulated Depreciation

¥129,150

¥ 62,600

¥ 66,550

Prior Years’ Income

¥ 21,000

¥ 22,800

22,500

17,300

24,350

23,200

Totals

¥ 67,850

¥ 63,300

¥ (4,550)

PROBLEM 11.5

(a) The amounts to be recorded on the books of Darby Sporting Goods

Plc. as of December 31, 2019, for each of the properties acquired from

Quay Athletic Equipment are calculated as follows:

Cost Allocations to Acquired Properties

Appraisal

Value

Remaining

Purchase

Price

Allocations

Renovations

Capitalized

Interest

Total

(1) Land

£290,000

£290,000

(2) Building

(3) Machinery

Supporting Calculations

1Balance of purchase price to be allocated.

Total purchase price …………………………………………………..

£400,000

Less: Land appraisal ………………………………………………….

Building

X £110,000

PROBLEM 11.5 (Continued)

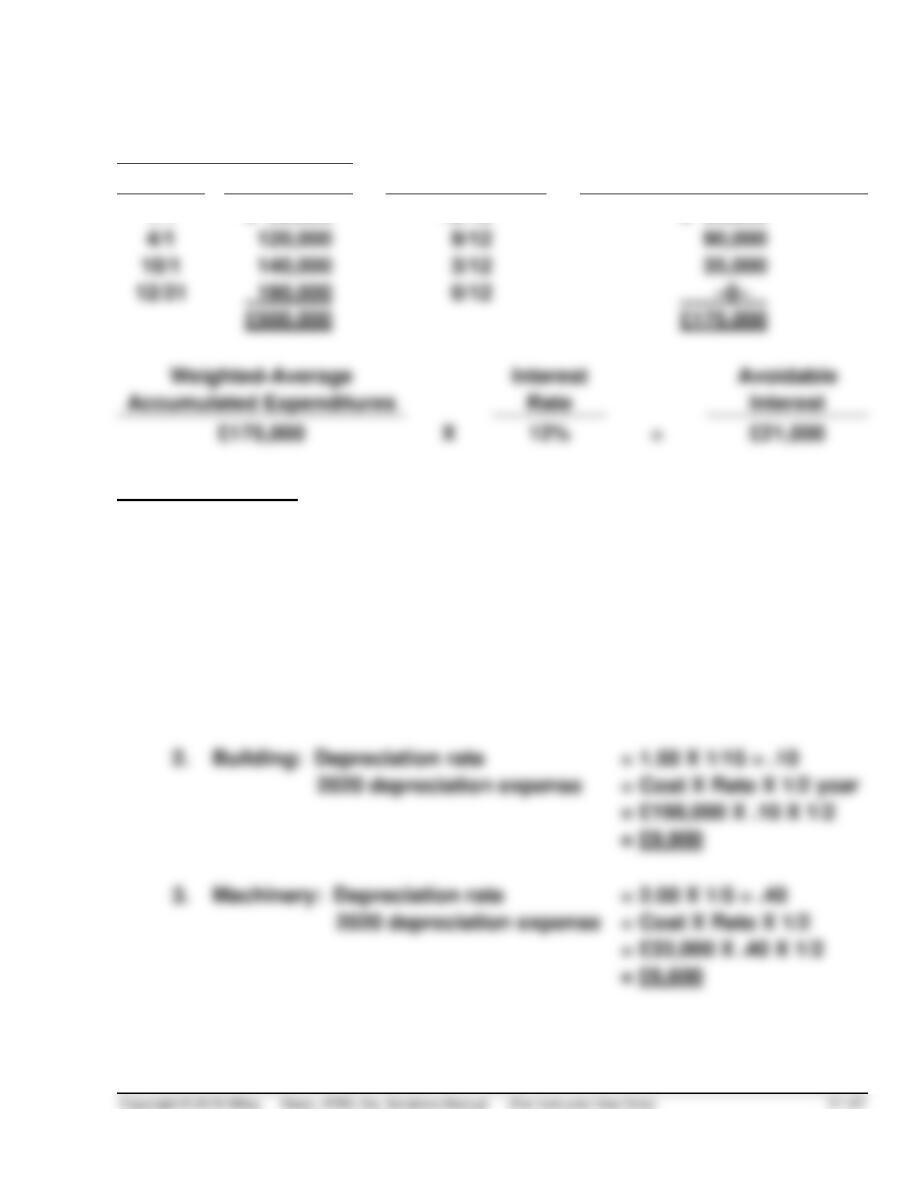

2Capitalizable interest.

Expenditures

Capitalization

Period

Weighted-Average

Accumulated Expenditures

Date

Amount

1/1

£ 50,000

12/12

£ 50,000

4/1

90,000

35,000

£175,000

Note to instructor: If the interest is allocated between the building and the

machinery, £14,700 (£21,000 X 105/150) would be allocated to the building

and £6,300 (£21,000 X 45/150) would be allocated to the machinery.

(b) Darby Sporting Goods Inc.’s 2020 depreciation expense, for book

purposes, for each of the properties acquired from Quay Athletic

Equipment Company is as follows:

1.

Land: No depreciation.

2.

Building: Depreciation rate

= Cost X Rate X 1/2 year

= £198,000 X .10 X 1/2

3.

Machinery: Depreciation rate

= 2.00 X 1/5 = .40

= Cost X Rate X 1/2

= £33,000 X .40 X 1/2

PROBLEM 11.5 (Continued)

(c) Arguments for the capitalization of interest costs include the following.

1. Diversity of practices among companies and industries called for

Arguments against the capitalization of interest include the following:

1. Interest capitalized in a period would tend to be offset by amorti-

(d) If Darby decides to use revaluation accounting for this building, then

revaluation applies to all assets in that class of assets. Darby cannot

selectively apply revaluation accounting to certain buildings but keep

PROBLEM 11.6

(1)

$80,000

Allocated in proportion to appraised values

(*1/10 X $800,000). *[$90,000 ÷ ($810,000 + $90,000)

(2)

$720,000

Allocated in proportion to appraised values

(3)

Fifty years

Cost less residual ($720,000 – $40,000) divided by

annual depreciation ($13,600).

(4)

$13,600

Same as prior year since it is straight-line depreciation.

(5)

$91,000

[Number of shares (2,500) times fair value ($30)]

plus demolition cost of existing building ($16,000).

(6)

None

No depreciation before use.

(7)

$40,000

Fair value.

(8)

$6,000

Cost ($40,000) times percentage (1/10 X ***150%).

***[100% ÷ 10) x 150%

(9)

$5,100

equals $34,000. Multiply $34,000 times ***15%.

(10)

$168,000

Total cost ($182,900) less repairs and maintenance

($14,900).

(11)

$36,000

Cost less residual ($168,000 – $6,000) times 8/36****.

PROBLEM 11.6 (Continued)

(13)

$52,000

Annual payment ($6,000) times present value of annuity

due at 8% for 11 years (7.710) plus down payment ($5,740).

This can be found in an annuity due table since the

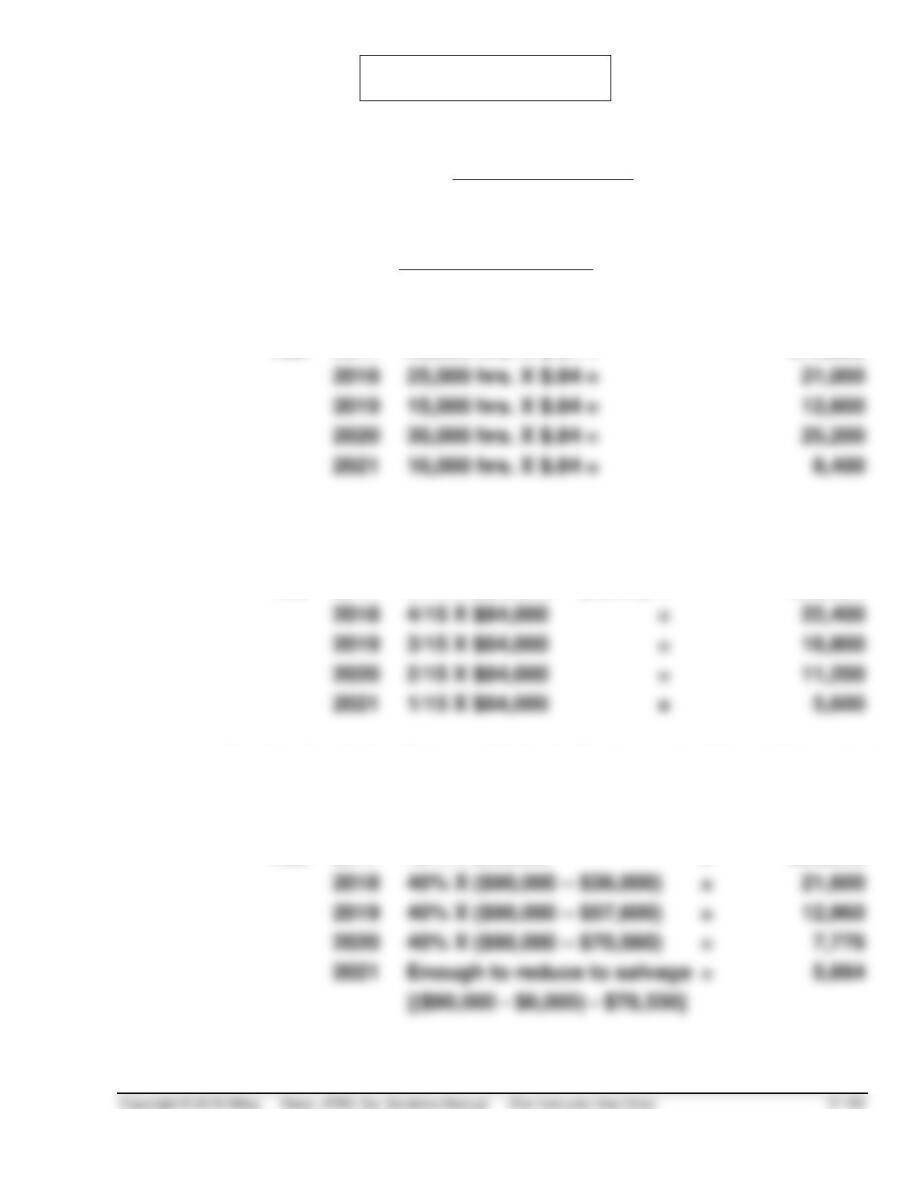

PROBLEM 11.7

(a)

1.

Straight-line Method:

$90,000 – $6,000

= $16,800 a year

5 years

2.

Activity Method:

$90,000 – $6,000

= $.84 per hour

100,000 hours

Year

2017

20,000 hrs. X $.84 =

$16,800

2018

25,000 hrs. X $.84 =

2019

15,000 hrs. X $.84 =

2020

30,000 hrs. X $.84 =

2021

10,000 hrs. X $.84 =

3. Sum-of-the-Years’-Digits: 5 + 4 + 3 + 2 + 1 = 15 or [5 x (5 + 1)] ÷ 2

Year

2017

5/15 X ($90,000 – $6,000) =

$28,000

2018

4/15 X $84,000 =

2019

3/15 X $84,000 =

2020

2/15 X $84,000 =

2021

1/15 X $84,000 =

4. Double-Declining-Balance Method: Each year is 20% (100 % ÷ 5) of

its total life. Double the rate to 40% (20% x 2).

Year

2017

40% X $90,000 =

$36,000

2018

40% X ($90,000 – $36,000) =

2019

40% X ($90,000 – $57,600) =

2020

40% X ($90,000 – $70,560) =

2021

Enough to reduce to salvage =

PROBLEM 11.7 (Continued)

(b) 1. Straight-line Method:

Year

2017

$90,000 – $6,000

X 9/12 =

$12,600

5 years

2018

Full year

16,800

2019

Full year

16,800

2020

Full year

16,800

2021

Full year

16,800

2022

Full year X 3/12 year =

2. Sum-of-the-Years’-Digits:

2017

(5/15 X $84,000) X 9/12 =

$21,000

2018

(5/15 X $84,000) X 3/12 =

(4/15 X $84,000) X 9/12 =

2019

(4/15 X $84,000) X 3/12 =

(3/15 X $84,000) X 9/12 =

2020

(3/15 X $84,000) X 3/12 =

(2/15 X $84,000) X 9/12 =

2021

(2/15 X $84,000) X 3/12 =

(1/15 X $84,000) X 9/12 =

2022

(1/15 X $84,000) X 3/12 =

PROBLEM 11.7 (Continued)

3. Double-Declining-Balance Method:

Year

Cost

Accum.

Depr. at

beg. of

Year

Book

Value at

beg. of

Year

Depr.

Expense

2017

$90,000

—

$90,000

$27,000 (1)

2018

25,200 (2)

2019

15,120 (3)

2020

9,072 (4)

2021

5,443 (5)

2022

8,165

2,165 (6)

(1) $90,000 X 40% X 9/12

(2) ($90,000 – $27,000) X 40%

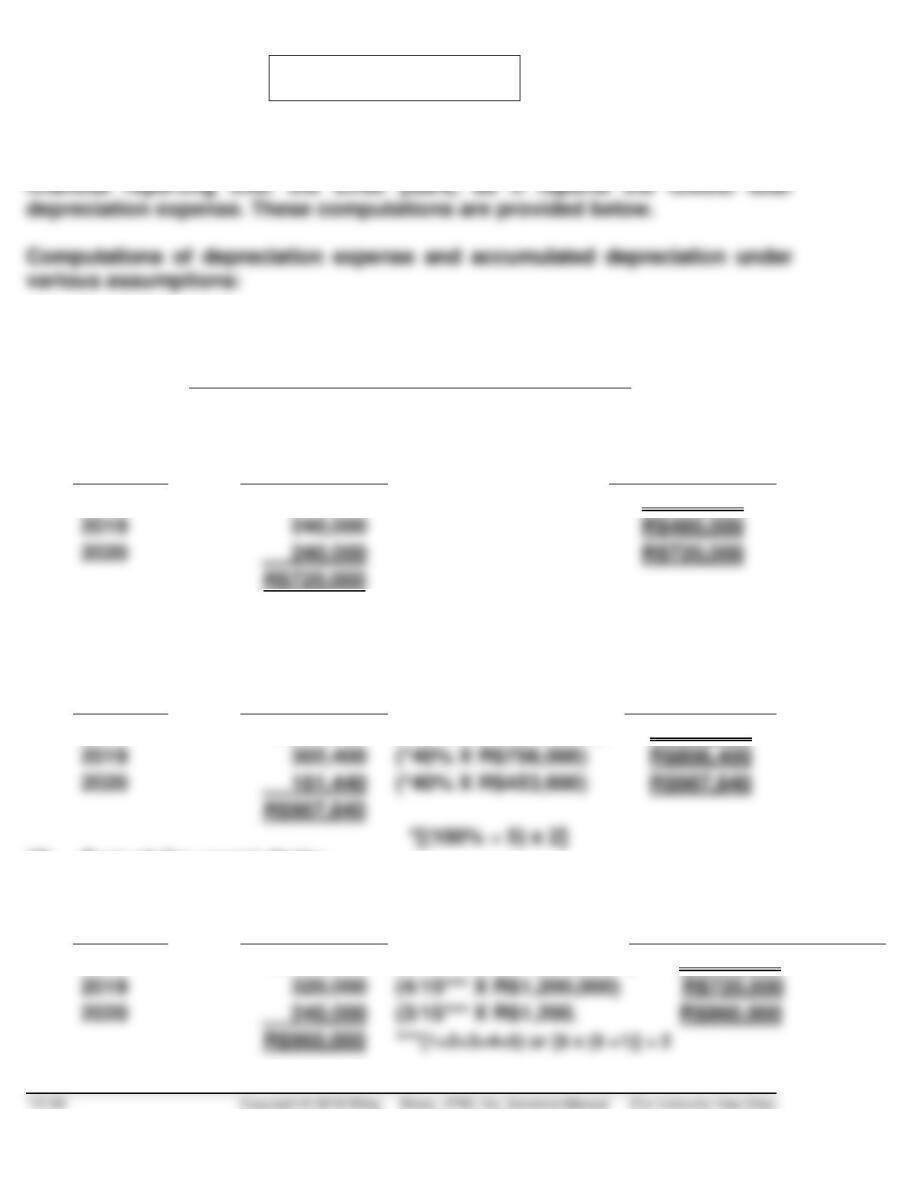

PROBLEM 11.8

The straight-line method would provide the highest total net income for

(1) Straight-line:

R$1,260,000 – R$60,000 = R$1,200,000***

= R$240,000

5 years

Year

Depreciation

Expense

Accumulated

Depreciation

2018

R$240,000

R$240,000

2019

R$480,000

2020

R$720,000

R$720,000

(2) Double-declining-balance:

Year

Depreciation

Expense

Accumulated

Depreciation

2018

R$504,000

(*40% X R$1,260,000)

R$504,000

2019

(*40% X R$756,000)

2020

(*40% X R$453,600)

R$987,840

(3) Sum-of-the-years’-digits:

Year

Depreciation

Expense

Accumulated

Depreciation

2018

R$400,000

(5/15*** X R$1,200,000**)

R$400,000

2019

(4/15*** X R$1,200,000)

R$720,000

2020

(3/15*** X R$1,200,

PROBLEM 11.8 (Continued)

(4) Units-of-output:

Year

Depreciation

Expense

Accumulated

Depreciation

2018

R$288,000

(R$24* X 12,000)

R$288,000

2019

(R$24 X 11,000)

R$552,000

2020

(R$24 X 10,000)

R$792,000

PROBLEM 11.9

(a) Carrying value of asset: €10,000,000 – €2,500,000* = €7,500,000.

*(€10,000,000 ÷ 8) X 2

(b) Depreciation Expense …………………………….. 1,400,000**

Accumulated Depreciation—

Equipment …………………………..……… 1,400,000

(c) No depreciation is recorded on impaired assets to be disposed of.

Recovery of impairment losses are recorded.

December 31, 2019

Loss on Impairment …………………………..…… 1,900,000

Accumulated Depreciation—

PROBLEM 11.10

Part I

(a) Calculation of the machine’s value-in-use at the end of 2019

Year

Future Cash

Flows

Present Value

Factor

Discounted

Cash Flow

2020

¥22,165

0.86957

¥ 19,274

2021

21,450

0.75614

16,219

2023

24,725

0.57175

14,137

2024

25,325

0.49718

12,591

2025

24,825

0.43233

10,733

2026

24,123

0.37594

2027

25,533

0.32690

2028

24,234

0.28426

2029

22,850

0.24719

The calculation of the impairment loss at the end of 2019 is as follows.

Machine

Carrying amount before impairment loss …….. ¥150,000

(b) December 31, 2019

PROBLEM 11.10 (Continued)

Part II

(c) Revised Cash Flows

Year

Future Cash

Flows

Present Value

Factor 15%

Discounted

Cash Flow

2024

¥30,321

.86957

¥ 26,366

2026

.65752

2027

.57175

¥118,816

Calculation of the reversal of the impairment loss at the end of 2023

Carrying amount at the end of 2019 (Part I) ……. ¥116,419

*Original cost …………………………………….. ¥150,000

Accumulated depreciation

based on historical cost (¥15,000 X 4) … (60,000)

Costs to enhance ……………………………… 25,000

¥115,000

PROBLEM 11.11

(a) Cost per barrel: (£1,200,000 + £50,000) ÷ 500,000 = £2.5/barrel

(b) Sales (36,000 X £65) …………………………………. £2,340,000

Expenses:

(c) Phelps has a choice on how to account for its exploration and evaluation

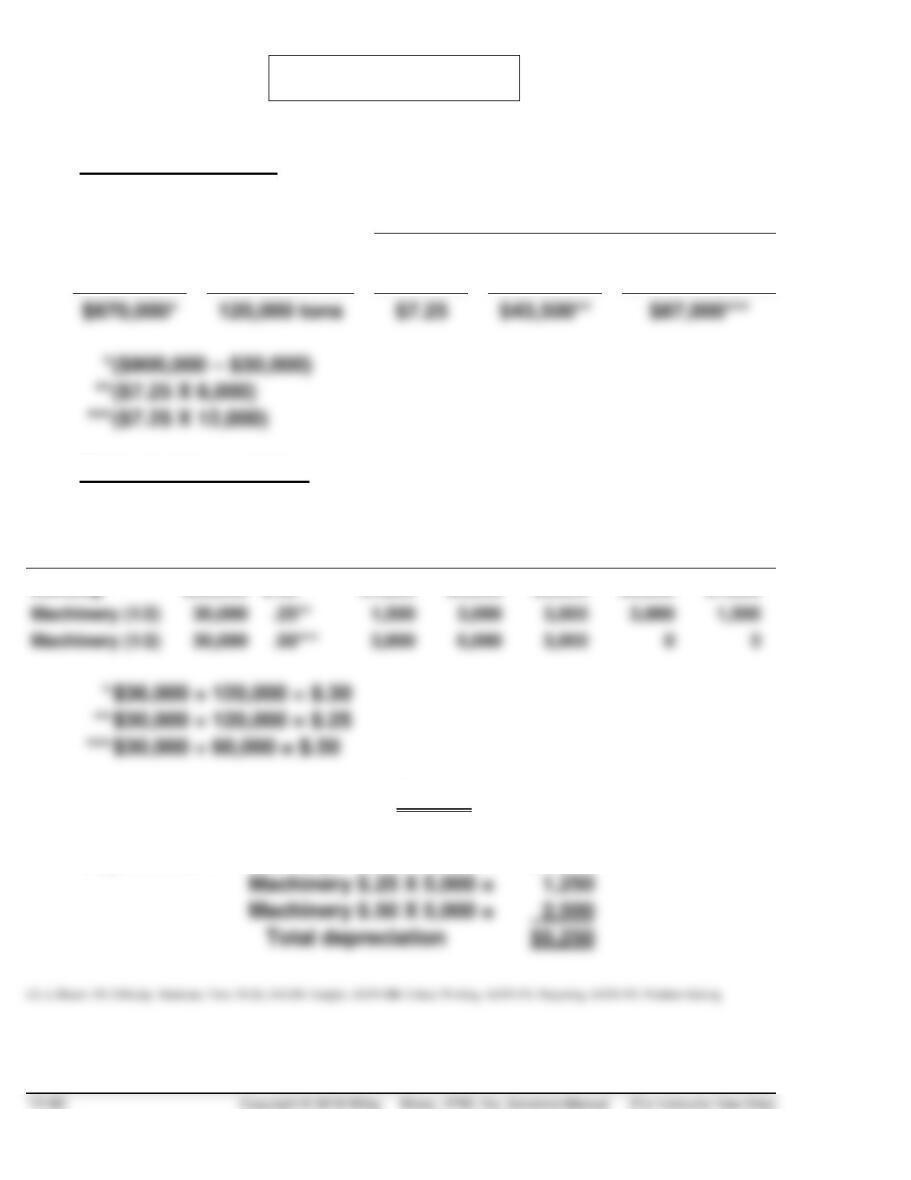

PROBLEM 11.12

(a) Estimated depletion:

Estimated Depletion

Depletion

Base

Estimated

Yield

Per

Ton

1ST & 11th

Yrs.

Each of Yrs.

2-10 Incl.

Estimated depreciation:

Asset

Cost

Per ton

Mined

1st

Yr.

Yrs.

2–5

6th

Yr.

Yrs.

7–10

11th

Yr.

Building

$36,000

$.30*

$1,800

$3,600

$3,600

$3,600

$1,800

Machinery (1/2)

Machinery (1/2)

0

0

(b) Depletion: $7.25 X 5,000 tons = $36,250

Depreciation:

Building $.30 X 5,000 =

$1,500

Total depreciation