Archives

Appendix A 1 Profit maximizing Markup Variable Cost

App A-3 Appendix A Pricing Products and Services Answer Key True / False Questions 1. Assume that the price elasticity of demand is less than -1 (for example, -1.5). As the absolute value of the price elasticity of demand increases, […]

Appendix A 2 New Product Automated Crepe Maker Being

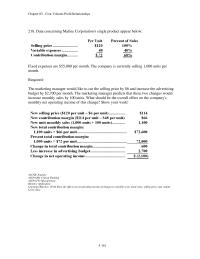

31. A new product, an automated crepe maker, is being introduced at Laguna Corporation. At a selling price of $52 per unit, management projects sales of 90,000 units. Launching the crepe maker as a new product would require an investment […]

Appendix A 3 The Desired Profit According The Target

App A-41 52. The desired profit according to the target costing calculations is: AACSB: Analytic AICPA BB: Critical Thinking AICPA FN: Measurement Bloom’s: Application Learning Objective: AppA-03 Compute the target cost for a new product or service Level: Easy 53. […]

Appendix A Homework If the company has idle capacity and sales to the retail

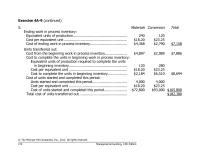

Problem A-5 (continued) c. The income statement is: Sales (15,000 jackets × $90 per jacket) .. $1,350,000 Cost of goods sold (15,000 jackets × $40 per jacket) …….. 600,000 Gross margin ………………………………….. 750,000 Selling and administrative expenses: Shipping ……………………………………… $ […]

Appendix A Homework The First Step The Absorption Costing Approach

318 1. Demand for a product is said to be inelastic if a change in price has little effect on the number of units sold. For example: a. The demand for designer perfumes sold at cosmetic counters in department stores […]

Appendix A Homework The profit-maximizing price should depend only on the variable

Appendix A Pricing Products and Services Solutions to Questions A-1 In cost-plus pricing, prices are set by adding a markup to a product’s cost. The markup is usually a percentage. A-2 The price elasticity of demand measures the degree to […]

Appendix B 1 Amount Of the Constrained Resource Required One Unit

Appendix B – Profitability Analysis App B-1 Appendix B Profitability Analysis Answer Key True / False Questions 1. Relative profitability should be measured by dividing the segment’s market share by the amount of the constrained resource it requires. 2. When […]

Appendix B 2 How Many Units Product L33y Should

Appendix B – Profitability Analysis 29. How many units of product L33Y should be produced each month? A. 0 B. 2,868 C. 712 D. 1,500 Therefore, production of product L33Y would be 3,560 minutes 5 minutes per unit of […]

Appendix B 3 How Many Units Product K36l Should

Appendix B – Profitability Analysis Gorey Products Inc. makes two products—K36L and W81H. Product K36L’s selling price is $345.00 and its unit variable cost is $310.50. Product W81H’s selling price is $256.00 and its unit variable cost is $230.40. The […]

Appendix B 4 Appendix Profitability Analysis Rank The Projects The

Appendix B – Profitability Analysis App B-58 a. Rank the projects on the basis of the profitability index: Project 4, Project 6, Project 5, and Project 2 should be accepted. b. AACSB: Analytic AICPA BB: Critical Thinking AICPA FN: Measurement […]

Appendix B Homework The Optimal Profit 32930 Would Computed Shown

products, customers, and other business segments. Accordingly, this appendix provides a coherent framework for measuring profitability. It distinguishes between absolute profitability and relative profitability. 1 1. If Coca Cola were considering closing down its operations in the African country of […]

Chapter 1 Homework The Theory Constraints Toc Constraint Also Called

iii. Relevance of data 1. Financial accounting data should be objective and verifiable. Managerial accountants focus on providing relevant Chapter 1 Lecture Notes Chapter theme: This chapter explains why managerial accounting is important to the future careers of all business […]

Chapter 1 Homework This Answer Based Nike Which Has Suppliers

© The McGraw-Hill Companies, Inc., 2012. All rights reserved. Solutions Manual, Chapter 1 1 sportscasters, (3) planning how many new television shows to introduce to the market, (4) planning each television show’s designated broadcast time slot, and (5) planning the […]

Chapter 10 1 The materials price variance is computed by multiplying

Chapter 10 Standard Costs and Variances 10-5 Chapter 10 Standard Costs and Variances Answer Key True / False Questions 1. The materials price variance is computed by multiplying the difference between the actual price and the standard price by the […]

Chapter 10 2 Borden Enterprises Uses Standard Costing For

Chapter 10 Standard Costs and Variances 34. Borden Enterprises uses standard costing. For the month of April, the company reported the following data: • Standard direct labor rate: $10 per hour • Standard hours allowed for actual production: 8,000 hours […]

Chapter 10 3 The Labor Efficiency Variance For June

Chapter 10 Standard Costs and Variances 59. The labor efficiency variance for June is: A. $995 U B. $950 U C. $995 F D. $950 F SH = 6,500 units 0.7 hours per unit = 4,550 hours Labor efficiency […]

Chapter 10 4 The Materials Quantity Variance For November

Chapter 10 Standard Costs and Variances 93. The materials quantity variance for November is: A. $420 U B. $434 F C. $420 F D. $434 U SQ = 3,000 units 9.2 grams per unit = 27,600 grams Materials quantity […]

Chapter 10 5 the standard variable overhead rate per machine setup is

Chapter 10 Standard Costs and Variances Cuda Corporation makes a product that uses a material with the following standards: The company budgeted for production of 3,500 units in November, but actual production was 3,300 units. The company used 23,050 pounds […]

Chapter 10 6 The Variable Overhead Efficiency Variance For

Chapter 10 Standard Costs and Variances Jardell Corporation makes a product with the following standards for labor and variable overhead: The company budgeted for production of 6,400 units in June, but actual production was 6,400 units. The company used 3,180 […]

Chapter 10 7 Leerar Corporation Makes Product With The

Chapter 10 Standard Costs and Variances 10-123 166. Leerar Corporation makes a product with the following standard costs: In December the company produced 4,200 units using 34,870 ounces of the direct material and 1,900 direct labor-hours. During the month, the […]

Chapter 10 Homework Predetermined Overhead Rates The Predetermined Overhead Rate

196 processing time required per unit, thereby causing an unfavorable labor efficiency variance. Quick Check – direct labor variance calculations VII. Using standard costs—variable manufacturing overhead variances Learning Objective 3: Compute the variable manufacturing overhead efficiency and rate variances and […]

Chapter 10 Homework The Buying And Using Activities Occur Different

185 Chapter 10 Lecture Notes Chapter theme: This chapter extends our study of management control by explaining how standard costs I. Standard costs – setting the stage A. Basic definitions/concepts i. A standard is a benchmark or “norm” for measuring […]

Chapter 10 Homework The number of units produced can be computed by using

Problem 10-16 (continued) 3. The computations to follow will require the standard quantities allowed for the actual output for direct labor in each department. Standard Hours Allowed Sintering: Production of Alpha8 (0.20 hours per unit × 1,500 units) .. 300 […]

Chapter 10 Homework When Used With The Formula Unfavorable Variances

Problem 10-10 (continued) Note that all of the price variance is due to the hospital’s 4% quantity discount. Also note that the $8,000 quantity variance for the month is equal to nearly 30% of the standard cost allowed for plates. […]

Chapter 10 Homework The materials price variance can be computed either when materials

Chapter 10 Standard Costs and Variances Solutions to Questions 10-1 A quantity standard indicates how much of an input should be used to make a unit of output. A price standard indicates how much the input should cost. indicate that […]

Chapter 10 Homework This variance includes both price and quantity elements

Problem 10A-10 (continued) Fixed overhead variances: Fixed Overhead Applied to Work in Process Budgeted Fixed Overhead Actual Fixed Overhead 16,000 MHs × £4 per MH = £64,000 £72,000 £70,000 Volume variance = £8,000 U Budget variance = £2,000 F Alternative […]

Chapter 10 Homework When variable manufacturing overhead is applied on the basis

Exercise 10B-2 (continued) b. The journal entry would be: Work in Process (600 hours × $10.00 per hour) …… 6,000 Labor Rate Variance (725 hours × $1.20 U per hour) …………………….. 870 Labor Efficiency Variance (125 U hours × $10.00 […]

Chapter 10a 1 Actual Fixed Overhead Budgeted Fixed Overhead Cost

Chapter 10 Appendix A Predetermined Overhead Rates and Overhead Analysis in a Standard Costing System 10A-4 Chapter 10 Appendix A Predetermined Overhead Rates and Overhead Analysis in a Standard Costing System Answer Key True / False Questions 1. In a […]

Chapter 10a 2 Behring Corporation Applies Manufacturing Overhead Products

Chapter 10 Appendix A Predetermined Overhead Rates and Overhead Analysis in a Standard Costing System 34. Behring Corporation applies manufacturing overhead to products on the basis of standard machine-hours. Budgeted and actual fixed manufacturing overhead costs for the most recent […]

Chapter 10a 3 The Fixed Component The Predetermined Overhead

Chapter 10 Appendix A Predetermined Overhead Rates and Overhead Analysis in a Standard Costing System The Malcolm Company uses a standard cost system in which manufacturing overhead costs are applied to products on the basis of standard direct labor-hours (DLHs). […]

Chapter 10a 4 The Denominator Level Activity 6900 Machine hours

Chapter 10 Appendix A Predetermined Overhead Rates and Overhead Analysis in a Standard Costing System 10A–59 88. If the denominator level of activity is 6,900 machine-hours, the fixed element in the predetermined overhead rate would be: AACSB: Analytic AICPA BB: […]

Chapter 10b 1 When The Actual Amount Raw Material Used

Chapter 10 Appendix B Journal Entries to Record Variances Chapter 10 Appendix B Journal Entries to Record Variances Key True / False Questions 1. Although formal entry of standard costs and variances into the accounting records is not required, some […]

Chapter 10b 2 The Debits The Raw Materials Account

Chapter 10 Appendix B Journal Entries to Record Variances Bordes Corporation has provided the following data concerning its most important raw material, compound R85F: The raw material was purchased on account. 30. The debits to the Raw Materials account for […]

Chapter 10b 3 The Lahn Company Produces And Sells

Chapter 10 Appendix B Journal Entries to Record Variances 10B–34 44. The Lahn Company produces and sells a single product. Standards have been established for the product as follows: Direct materials: 5 pounds @ $3.50 per pound = $17.50 Direct […]

Chapter 11 1 Residual Income Better Measure For Performance

Chapter 11 Performance Measurement in Decentralized Organizations Chapter 11 Performance Measurement in Decentralized Organizations Answer Key True / False Questions 1. Residual income is superior to return on investment as a means of measuring performance because it encourages managers to […]

Chapter 11 2 average operating assets we need to determine the sales

Chapter 11 Performance Measurement in Decentralized Organizations 39. The margin in Year 2 was: A. 48% B. 32% C. 20% D. 10% ROI in Year 1: ROI = Margin Turnover = 16% 2.5 = 40% By assumption, the […]

Chapter 11 3 The Divisions Margin Closest To

Chapter 11 Performance Measurement in Decentralized Organizations 69. The division’s margin is closest to: A. 26.2% B. 23.5% C. 2.7% D. 11.5% Margin = Net operating income Sales = $575,100 $21,300,000 = 2.7% AACSB: Analytic AICPA BB: Critical […]

Chapter 11 Homework Cost based Transfer Prices Not Provide Incentives Control

vi. Incentive compensation for employees probably should be linked to balanced scorecard performance measures. 1. However, this should only be done after the organization has been successfully managed those being evaluated with them. B. The balanced scorecard – an example […]

Chapter 11 Homework Division Would Unwilling Pay More Than 47

Problem 11-21 (continued) Each of these hypotheses is questionable to some degree. For example, in the case of Applied Pharmaceuticals, R&D yield is not the sole driver of the customers’ perception of first–to–market capability. More specifically, if Applied Pharmaceuticals experimented […]

Chapter 11 Homework Exercise 1111 Continued Each Offices Individual Performance

Exercise 11-11 (continued) 4. Each office’s individual performance should be based on the scorecard measures only if the measures are controllable by those employed at the branch offices. In other words, it would not make sense to attempt to hold […]

Chapter 11 Homework Exercise 116 15 Minutes Margin Turnover Net

Chapter 11 Performance Measurement in Decentralized Organizations Solutions to Questions 11-1 In a decentralized organization, decision-making authority isn’t confined to a few top executives; instead, decision-making authority is spread throughout the organization. 11-2 The benefits of decentralization include: (1) by […]

Chapter 11 Homework This May Make Difficult Assess This Manager

Chapter 11 Lecture Notes Chapter theme: Managers in large organizations have to delegate some decisions to those who are at lower levels in I. Decentralization in organizations A. A decentralized organization does not confine decision-making authority to a few top […]

Chapter 11 Homework Variable Costs The Clock Division Excluding The

Problem 11A-5 (continued) b. The loss in potential profits to the company as a whole will be: Division B’s outside purchase price ………………………… $39 Division A’s variable cost on the internal transfer ……… 36 Potential added contribution margin lost to […]

Chapter 11a 1 When a division is operating at full capacity

FALSE AACSB: Reflective Thinking AICPA BB: Critical Thinking AICPA FN: Measurement Bloom’s: Comprehension Learning Objective: 11A-05 Determine the range; if any; within which a negotiated transfer price should fall Level: Hard TRUE AACSB: Reflective Thinking AICPA BB: Critical Thinking AICPA […]

Chapter 11b 1 For performance evaluation purposes, budgeted service department

Chapter 11 Appendix B Service Department Charges 11B-1 Chapter 11 Appendix B Service Department Charges Answer Key True / False Questions 1. For performance evaluation purposes, budgeted service department costs, instead of actual service department costs, should be charged to […]

Chapter 11b 2 How Much Housekeeping Department Cost Should

Chapter 11 Appendix B Service Department Charges Gunnison Foods has two operating departments, Processing and Packaging. It also has a Housekeeping Department that serves the two operating departments. The costs of the Housekeeping Department are all variable and are allocated […]

Chapter 12 1 X70 Longer Used The Company Any Its

Chapter 12 – Differential Analysis: The Key to Decision Making 12-1 Chapter 12 Differential Analysis: The Key to Decision Making Answer Key True / False Questions 1. Future costs that do not differ among the alternatives are not relevant in […]

Chapter 12 2 Product R19n Has Been Considered Drag

Chapter 12 – Differential Analysis: The Key to Decision Making 35. Product R19N has been considered a drag on profits at Buzzeo Corporation for some time and management is considering discontinuing the product altogether. Data from the company’s accounting system […]

Chapter 12 3 Two Products And Ri Emerge From

Chapter 12 – Differential Analysis: The Key to Decision Making 52. Two products, IF and RI, emerge from a joint process. Product IF has been allocated $25,300 of the total joint costs of $46,000. A total of 2,000 units of […]

Chapter 12 4 Cosmo Considering Promotional Campaign The Town

Chapter 12 – Differential Analysis: The Key to Decision Making 12–61 74. Cosmo is considering a promotional campaign at the Town Store that would not affect the Mall Store. Increasing annual promotional expenses at the Town Store by $60,000 in […]

Chapter 12 5 Suppose The Company Already Operating Capacity

Chapter 12 – Differential Analysis: The Key to Decision Making 91. Suppose the company is already operating at capacity when the special order is received from the overseas customer. What would be the opportunity cost of each unit delivered to […]

Chapter 12 6 How Much Should The Company Willing

Chapter 12 – Differential Analysis: The Key to Decision Making 109. Up to how much should the company be willing to pay for one additional minute of milling machine time if the company has made the best use of the […]

Chapter 12 7 Nutall Corporation Considering Dropping Product N28x

Chapter 12 – Differential Analysis: The Key to Decision Making 130. Nutall Corporation is considering dropping product N28X. Data from the company’s accounting system appear below: All fixed expenses of the company are fully allocated to products in the company’s […]

Chapter 12 8 Jumonville Company Produces Single Product The

Chapter 12 – Differential Analysis: The Key to Decision Making 143. Humes Corporation makes a range of products. The company’s predetermined overhead rate is $16 per direct labor-hour, which was calculated using the following budgeted data: Management is considering a […]

Chapter 12 Homework Essex Makes Buys Part 4a Hence Also

eliminated in whole or in part by choosing one alternative over another. Avoidable costs are relevant costs. Unavoidable costs are irrelevant costs. ii. Two broad categories of costs are never relevant in any decision: 1. A sunk cost is a […]

Chapter 12 Homework fixed costs will be spread over a larger number of units

Problem 12-25 (continued) 2. a. Note that unit costs for both supervision and equipment rental will change if the company needs 50,000 subassemblies each year. These fixed costs will be spread over a larger number of units, thereby decreasing the […]

Chapter 12 Homework The case strongly suggests that direct labor is fixed

Case 12-29 (continued) Solution assuming direct labor is a variable cost (a) (b) (c) (a) × (c) (a) × (b) Quantity Unit Contri- bution Margin Welding Time per Unit Total Welding Time Balance of Welding Time Total Contri- bution Total […]

Chapter 12 Homework Total Incremental Revenue Incremental Costs Variable

Exercise 12–16 (15 minutes) Relevant Costs Item Make Buy Direct materials (60,000 @ $4.00) …………. $240,000 Direct labor (60,000 @ $2.75) ………………. 165,000 (60,000 @ $0.50) …………………………….. 30,000 Fixed manufacturing overhead, traceable (1/3 of $180,000) …………………………….. 60,000 Cost of purchasing […]

Chapter 12 Homework A relevant cost is a cost that differs in total between

Chapter 12 Differential Analysis: The Key to Decision Making Solutions to Questions 12-1 A relevant cost is a cost that differs in total between the alternatives in a decision. 12-2 An incremental cost (or benefit) is the change in cost […]

Chapter 13 1 Objective 1305 Determine The Payback Period For

Chapter 13 Capital Budgeting Decisions 13-6 Chapter 13 Capital Budgeting Decisions Answer Key True / False Questions 1. If the internal rate of return exceeds the required rate of return for a project, then the net present value of that […]

Chapter 13 2 Ignore Income Taxes This Problem Mcclam

Chapter 13 Capital Budgeting Decisions 40. (Ignore income taxes in this problem.) Mcclam, Inc., is considering the purchase of a machine that would cost $100,000 and would last for 9 years. At the end of 9 years, the machine would […]

Chapter 13 3 the equipment would cost $115,000 and have a 5 year life

Chapter 13 Capital Budgeting Decisions 66. (Ignore income taxes in this problem.) The management of Rusell Corporation is considering a project that would require an investment of $282,000 and would last for 6 years. The annual net operating income from […]

Chapter 13 4 The Payback Period This Investment Closest

Chapter 13 Capital Budgeting Decisions 13–66 92. The payback period of this investment is closest to: (Ignore income taxes in this problem.) The management of Melchiori Corporation is considering the purchase of a machine that would cost $310,000, would last […]

Chapter 13 5 Ignore Income Taxes This Problem Tranter

Chapter 13 Capital Budgeting Decisions 13–86 119. (Ignore income taxes in this problem.) Tranter, Inc., is considering a project that would have a ten-year life and would require a $1,200,000 investment in equipment. At the end of ten years, the […]

Chapter 13 6 an investment in automated equipment with a useful life of

Chapter 13 Capital Budgeting Decisions 134. (Ignore income taxes in this problem.) Rosenholm Corporation uses a discount rate of 18% in its capital budgeting. Partial analysis of an investment in automated equipment with a useful life of 5 years has […]

Chapter 13 Homework Compound Interest The Example Continued What

273 B. Internal rate of return method i. When using the internal rate of return method to rank competing investment projects, the preference rule is: the higher the internal rate of return, the more desirable the project. C. Net present […]

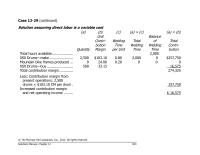

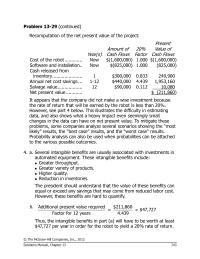

Chapter 13 Homework It appears that the company did not make a wise investment

Problem 13-29 (continued) Recomputation of the net present value of the project: Year(s) Amount of Cash Flows 20% Factor Present Value of Cash Flows Cost of the robot …………. Now $(1,600,000) 1.000 $(1,600,000) Software and installation.. Now $(825,000) 1.000 (825,000) […]

Chapter 13 Homework Net Operating Income Add Noncash Deduction

Chapter 13 Capital Budgeting Decisions Solutions to Questions 13-1 A capital budgeting screening decision is concerned with whether a proposed investment project passes a preset hurdle, such as a 15% rate of return. A capital budgeting preference decision is concerned […]

Chapter 13 Homework Project Investment Working Capital Annual Net

Case 13-35 (45 minutes) 1. Perhaps the clearest approach to a solution is as follows: Item Year(s) Amount of Cash Flows 12% Factor Present Value of Cash Flows Purchase of facilities: Initial payment ………. Now $(6,000,000) 1.000 $ (6,000,000) Annual […]

Chapter 13 Homework This Technique Works Very Well Projects Cash

Chapter 13 Lecture Notes Chapter theme: The term capital budgeting is used to describe how managers plan significant cash outlays on projects that have long-term implications such as the purchase of new equipment and the introduction of new products. This […]

Chapter 13 Homework Which ranking is best depends on Yancey Company’s opportunities

Problem 13-18 (30 minutes) 1. The formula for the project profitability index is: Net present value Project profitability index = Investment required The project profitability index for each project is: Project A: $221,615 ÷ $800,000 = 0.28 Project B: $210,000 […]

Chapter 13a 1 The Guaranteed Interest Rate Closest Toa 13b

FALSE AACSB: Reflective Thinking AICPA BB: Critical Thinking AICPA FN: Measurement Bloom’s: Comprehension Learning Objective: 13A-07 Understand present value concepts and the use of present value tables Level: Medium Chapter 13 – Appendix A The Concept of Present Value 13A-1 […]

Chapter 13c 1 Equipment Selection Capital Budgeting Decision Which The

Chapter 13 – Appendix C Income Taxes in Capital Budgeting Decisions Chapter 13 Appendix C Income Taxes in Capital Budgeting Decisions Answer Key True / False Questions 1. The reduction in taxes made possible by the annual depreciation deductions equals […]

Chapter 13c 2 The Net Present Value The Project

Chapter 13 – Appendix C Income Taxes in Capital Budgeting Decisions 24. The net present value of the project is closest to: A. $250,815 B. $84,495 C. $109,800 D. $276,120 13–14 AACSB: Analytic AICPA BB: Critical Thinking AICPA FN: Measurement […]

Chapter 14 1 Under the indirect method of determining the net cash

Chapter 14 – Statement of Cash Flows 14-1 Chapter 14 Statement of Cash Flows Answer Key True / False Questions 1. Cash payments to retire bonds payable are reported as a cash outflow in the financing activities section of the […]

Chapter 14 2 Waldrop Corporations Comparative Balance Sheet Appears

Chapter 14 – Statement of Cash Flows 41. Waldrop Corporation’s comparative balance sheet appears below: The company did not dispose of any property, plant, and equipment during the year. Its net income for the year was $4,000. The net cash […]

Chapter 14 3 Frizz Hair Salon Had Net Income

Chapter 14 – Statement of Cash Flows 55. Frizz Hair Salon had net income of $93,000 for the year just ended. Frizz collected the following additional information to prepare its statement of cash flows for the year: Frizz uses the […]

Chapter 14 4 The Net Cash Provided Used In

Chapter 14 – Statement of Cash Flows 74. The net cash provided by (used in) investing activities last year was: A. $(95,000) B. $95,000 C. $(125,000) D. $125,000 Investing activities: AACSB: Analytic AICPA BB: Critical Thinking AICPA FN: Measurement Bloom’s: […]

Chapter 14 5 Which The Following Correct Regarding The

Chapter 14 – Statement of Cash Flows 96. Which of the following is correct regarding the operating activities section of the statement of cash flows? A. The change in Accounts Receivable will be subtracted from net income; The change in […]

Chapter 14 6 Smigel Corporation’s balance sheet and income statement appear

Chapter 14 – Statement of Cash Flows 14–92 103. Smigel Corporation’s balance sheet and income statement appear below: Chapter 14 – Statement of Cash Flows Cash dividends were $1. The company sold equipment for $15 that was originally purchased for […]

Chapter 14 Homework The Accrued Liabilities Balance Increased 3 This

4. Will we have to borrow money to make needed investments? 5. Why is there a difference between net income and net cash flow? iii. The statement of cash flows is based on the principle that properly analyzing the changes […]

Chapter 14 Homework The relatively small amount of net cash provided by operating

Problem 14-9 (continued) The net cash provided by operating activities is computed as follows: Net income ………………………………………………….. $63,000 Adjustments to convert net income to cash basis: Depreciation ………………………………………………. $ 45,000 Increase in accounts receivable ……………………… (70,000) Increase in inventory …………………………..………. […]

Chapter 14 Homework although the company is generating substantial cash flow

Problem 14-13 (continued) 2. The company has had a huge buildup of inventory. In an effort to overcome the cash flow impact of this build up, it has delayed payments to suppliers. The corresponding $300,000 increase in accounts payable largely […]

Chapter 14 Homework The company’s specific circumstances should be considered

Chapter 14 Statement of Cash Flows Solutions to Questions 14-1 The statement of cash flows highlights the major activities that impact cash flows and hence affect the overall cash balance. borrowing of $500,000 must both be shown “gross” on the […]

Chapter 14a 1 Tax Expense 27000 The Beginning Last Year

Chapter 14 Appendix A The Direct Method of Determining the Net Cash Provided by Operating Activities 14A-1 Chapter 14 Appendix A The Direct Method of Determining the Net Cash Provided by Operating Activities Answer Key True / False Questions 1. […]

Chapter 14a 2 Under The Direct Method The Sales

Chapter 14 Appendix A The Direct Method of Determining the Net Cash Provided by Operating Activities 22. Under the direct method, the sales adjusted to a cash basis would be: A. $252,000 B. $244,000 C. $260,000 D. $250,000 AACSB: Analytic […]

Chapter 14a 3 The Net Cash Provided Used In

Chapter 14 Appendix A The Direct Method of Determining the Net Cash Provided by Operating Activities 14A–38 40. The net cash provided by (used in) investing activities for the year was: AACSB: Analytic AICPA BB: Critical Thinking AICPA FN: Measurement […]

Chapter 15 1 Horizontal analysis involves comparing two or more l

Chapter 15 – Financial Statement Analysis 15-1 Chapter 15 Financial Statement Analysis Answer Key True / False Questions 1. Horizontal analysis involves comparing two or more years’ financial data for a single company. 2. The gross margin percentage is computed […]

Chapter 15 10 Excerpts From Stepney Corporations Most Recent

Chapter 15 – Financial Statement Analysis 15-173 200. Excerpts from Stepney Corporation’s most recent balance sheet (in thousands of dollars) appear below: Sales on account during the year totaled $1,440 thousand. Cost of goods sold was $890 thousand. Required: Compute […]

Chapter 15 2 Million The Beginning The Year And

Chapter 15 – Financial Statement Analysis 42. Last year the return on total assets in Jeffrey Company was 8.5%. The total assets were 2.9 million at the beginning of the year and 3.1 million at the end of the year. […]

Chapter 15 3 Kaelker Corporation Has Provided The Following

Chapter 15 – Financial Statement Analysis 66. Kaelker Corporation has provided the following data: The inventory turnover for this year is closest to: A. 3.36 B. 0.87 C. 1.15 D. 3.15 Average inventory balance = ($213,000 + $186,000) 2 […]

Chapter 15 4 The Dividend Payout Ratio For Year

Chapter 15 – Financial Statement Analysis 93. The dividend payout ratio for Year 2 is closest to: A. 72.7% B. 54.5% C. 46.2% D. 1818.2% Number of common shares outstanding = Common stock Par value = $200 $1 […]

Chapter 15 5 Larned Company’s Dividend Yield Ratio December

Chapter 15 – Financial Statement Analysis 120. Larned Company’s dividend yield ratio on December 31, Year 2 was closest to: A. 8.7% B. 9.1% C. 8.3% D. 5.5% Number of common shares outstanding = Common stock Par value = […]

Chapter 15 6 Bragg Company’s Inventory Turnover Ratio For

Chapter 15 – Financial Statement Analysis Selected financial data for Bragg Company appear below: 147. Bragg Company’s inventory turnover ratio for Year 2 was closest to: A. 2.00 B. 2.67 C. 4.80 D. 4.00 Inventory turnover = Cost of goods […]

Chapter 15 7 The Times Interest Earned For Year

Chapter 15 – Financial Statement Analysis 175. The times interest earned for Year 2 is closest to: A. 2.73 B. 4.91 C. 7.01 D. 3.91 Times interest earned = Earnings before interest expense and income taxes Interest expense = […]

Chapter 15 8 Financial Statement Analysis The Company Paid

Chapter 15 – Financial Statement Analysis The company paid total dividends of $100,000 during the year. At the end of Year 2, the company’s common stock was selling for $38 per share. Required: On the basis of the information given […]

Chapter 15 9 Financial Statement Analysis Number Common Shares

Chapter 15 – Financial Statement Analysis a. Number of common shares outstanding = Common stock Par value = $200 $1 per share = 200 shares Earnings per share = (Net Income – Preferred Dividends) Average number of […]

Chapter 15 Homework Cost Goods Sold A Average Inventory

Problem 15-12 (continued) c. Financial leverage is positive in both years because the return on common equity is greater than the return on total assets. This positive financial leverage is due to three factors: the preferred stock, which has a […]

Chapter 15 Homework an analyst hopes to get some idea of whether a situation

Chapter 15 Financial Statement Analysis Solutions to Questions 15-1 Horizontal analysis examines how a particular item on a financial statement such as sales or cost of goods sold behaves over time. Vertical analysis involves analysis of items on an income […]

Chapter 15 Homework Reinforce the limitations of relying on financial statements

331 1. If one company values its inventory using the LIFO method and another uses the average cost method, then direct comparisons of financial data such as inventory valuations and cost of goods sold may be misleading. a. Even with […]

Chapter 2 1 Medium34 Which The Following Should Not Included

Chapter 02 – Managerial Accounting and Cost Concepts 2-1 Chapter 02 Managerial Accounting and Cost Concepts Answer Key True / False Questions 1. Direct material costs are generally variable costs. 2. Property taxes and insurance premiums paid on a factory […]

Chapter 2 2 September Direct Labor Was 40 Conversion

Chapter 02 – Managerial Accounting and Cost Concepts 58. In September direct labor was 40% of conversion cost. If the manufacturing overhead for the month was $66,000 and the direct materials cost was $20,000, the direct labor cost was: A. […]

Chapter 2 3 Managerial Accounting And Cost Concepts 79

Chapter 02 – Managerial Accounting and Cost Concepts 79. Given the cost formula Y = $15,000 + $5X, total cost at an activity level of 8,000 units would be: A. $23,000 B. $15,000 C. $55,000 D. $40,000 Y = $15,000 […]

Chapter 2 4 The Best Estimate The Total Contribution

Chapter 02 – Managerial Accounting and Cost Concepts 2-61 103. The best estimate of the total contribution margin when 6,300 units are sold is: AACSB: Analytic AICPA BB: Critical Thinking AICPA FN: Measurement Bloom’s: Application Learning Objective: 02-03 Understand cost […]

Chapter 2 5 Using The High low Method The Estimate

Chapter 02 – Managerial Accounting and Cost Concepts 2-81 129. Using the high-low method, the estimate of the fixed component of electrical cost per month is closest to: AACSB: Analytic AICPA BB: Critical Thinking AICPA FN: Measurement Bloom’s: Application Learning […]

Chapter 2 6 Lett man Corporation Has Provided The Following

Chapter 02 – Managerial Accounting and Cost Concepts 2-100 154. Laco Company acquired its factory building about 20 years ago. For a number of years the company has rented out a small, unused part of the building. The renter’s lease […]

Chapter 2 Homework Administrative Expenses 1 Per Unit 10000 Units

Chapter 2 Managerial Accounting and Cost Concepts Solutions to Questions 2-1 The three major elements of product costs in a manufacturing company are direct materials, direct labor, and manufacturing overhead. 2-2 a. Direct materials are an integral part of a […]

Chapter 2 Homework Internal And External Failure Costs Are Incurred

Problem 2A-4 (continued) 2. a. Quarter DLHs (X) Utilities Cost (Y) Year 1: 1st 5,000 $50,000 2nd 3,000 $45,000 3rd 4,000 $60,000 4th 6,000 $75,000 Year 2: 1st 10,000 $100,000 2nd 9,000 $105,000 3rd 8,000 $85,000 4th 11,000 $120,000 The […]

Chapter 2 Homework Least squares Regression Computations Exercise 20 Minutes

Case 2-25 (30 minutes) 1. The scattergraph of janitorial labor cost versus the number of units produced is presented below: © The McGraw-Hill Companies, Inc., 2012. All rights reserved. Solutions Manual, Chapter 2 45 Case 2-25 (continued) 2. The scattergraph […]

Chapter 2 Homework Prevention Costs Are Incurred Support Activities

Helpful Hint: The income statement from the annual report of a well-known local manufacturing firm can be used to illustrate the functional income statement. Ask if the various expense categories on the income statement III. Cost classifications for assigning costs […]

Chapter 2 Homework The Total Mixed Cost The Total Fixed

Chapter 2 Lecture Notes Chapter theme: This chapter explains how managers need to rely on different cost classifications for different purposes. The four main purposes emphasized in this I. General cost classifications We’ll begin by looking at manufacturing companies because […]

Chapter 2 Homework than the estimate provided by least-squares regression

Exercise 2-13 (continued) 4. The high-low estimate of fixed costs is $1,470.59 higher than the estimate provided by least-squares regression. The high-low estimate of the variable cost per unit is $0.29 lower than the estimate provided by least-squares regression. A […]

Chapter 2a 1 Medium16 Using The Least squares Regression Method The

TRUE AACSB: Reflective Thinking AICPA BB: Critical Thinking AICPA FN: Measurement Bloom’s: Knowledge Learning Objective: 02A-08 Analyze a mixed cost using a scattergraph plot and the least-squares regression method Level: Easy FALSE AACSB: Reflective Thinking AICPA BB: Critical Thinking AICPA […]

Chapter 2b 1 An increase in appraisal costs will usually result in an increase

Chapter 02 – Appendix B Cost of Quality 2B-1 Chapter 02 Appendix B Cost of Quality Answer Key True / False Questions 1. An increase in appraisal costs will usually result in an increase in internal failure costs. 2. Prevention […]

Chapter 2b 2 What Would The Total Internal Failure

Chapter 02 – Appendix B Cost of Quality 2B–12 29. What would be the total internal failure cost appearing on the quality cost report? AACSB: Analytic AICPA BB: Critical Thinking AICPA FN: Measurement Bloom’s: Application Learning Objective: 02B-09 Identify the […]

Chapter 3 1 The use of predetermined overhead rates in a job-order

Chapter 03 – Job-Order Costing 3-1 Chapter 03 Job-Order Costing Answer Key True / False Questions 1. The use of predetermined overhead rates in a job-order cost system makes it possible to estimate the total cost of a given job […]

Chapter 3 2 Capalbo Corporation Bases Its Predetermined Overhead

Chapter 03 – Job-Order Costing 38. Capalbo Corporation bases its predetermined overhead rate on the estimated labor-hours for the upcoming year. At the beginning of the most recently completed year, the company estimated the labor-hours for the upcoming year at […]

Chapter 3 3 Dowan Company Uses Predetermined Overhead Rate

Chapter 03 – Job-Order Costing 64. Dowan Company uses a predetermined overhead rate based on direct labor-hours to apply manufacturing overhead to jobs. Last year Dowan Company incurred $156,600 in actual manufacturing overhead cost. The Manufacturing Overhead account showed that […]

Chapter 3 4 The Overhead For The Year Was

Chapter 03 – Job-Order Costing 3-61 86. The overhead for the year was: AACSB: Analytic AICPA BB: Critical Thinking AICPA FN: Measurement Bloom’s: Application Learning Objective: 03-07 Compute underapplied or overapplied overhead cost and prepare the journal entry to close […]

Chapter 3 5 The Manufacturing Overhead Applied Is 28000

Chapter 03 – Job-Order Costing 111. The manufacturing overhead applied is: A. $28,000 B. $29,000 C. $30,000 D. $38,000 Transaction (6) represents manufacturing overhead applied at $29,000. 3-81 AACSB: Analytic AICPA BB: Critical Thinking AICPA FN: Measurement Bloom’s: Application Learning […]

Chapter 3 6 The Finished Goods Inventory The End

Chapter 03 – Job-Order Costing 135. The finished goods inventory at the end of November after allocation of any underapplied or overapplied manufacturing overhead for the month is closest to: A. $50,840 B. $50,848 C. $52,632 D. $52,640 Allocating underapplied […]

Chapter 3 7 1The Following Cost Data Relate The

Chapter 03 – Job-Order Costing 148. During August, Allee Corporation incurred $64,000 of actual Manufacturing Overhead costs. During the same period, the Manufacturing Overhead applied to Work in Process was $66,000. Required: Prepare journal entries to record the incurrence of […]

Chapter 3 Homework Additional Output Required Attain Target Net Operating

Exercise 3A-2 (continued) Consequently, the income statement would appear as follows: Income Statement Sales ……………………………………………. $43,740 Cost of goods sold (see above) ………….. 26,510 Gross margin …………………………………. 17,230 Underapplied manufacturing overhead … $1,920 Selling and administrative expenses ……. 8,180 10,100 […]

Chapter 3 Homework Cost Goods Sold The Underapplied Overhead Allocated

Exercise 3-17 (30 minutes) 1. The predetermined overhead rate is computed as follows: Y = $106,250 + $0.75 per MH × 85,000 MHs Estimated fixed manufacturing overhead ……………… $106,250 Estimated variable manufacturing overhead $0.75 per MH × 85,000 MHs …………………………… […]

Chapter 3 Homework Deduct Ending Work Process Inventory Cost

Chapter 3 Job-Order Costing Solutions to Questions 3-1 By definition, manufacturing overhead consists of costs that cannot be practically traced to jobs. Therefore, if these costs are to be assigned to jobs, they must be allocated rather than traced. be […]

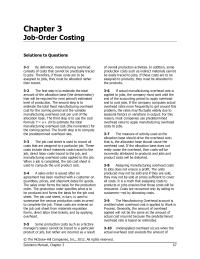

Chapter 3 Homework Direct Materials Direct Labor Manufacturing

Problem 3-26 (continued) 2. Preparation Department overhead applied: 350 machine-hours × $5.20 per machine-hour ….. $1,820 Fabrication Department overhead applied: 130 direct labor-hours × $14.40 per labor-hour …. 1,872 Total overhead cost ……………………………………….. $3,692 3. Total cost of Job 127: […]

Chapter 3 Homework T account Form Close Out Pearcos 30000 Overapplied

vi. Transferring completed units from work in process to finished goods 1. In T-account form: a. The sum of all amounts transferred from work in process to finished 2. In journal entry form: a. Debit Finished Goods and credit Work […]

Chapter 3 Homework Managers need to assign costs to products to facilitate external

Chapter 3 Lecture Notes Chapter theme: Managers need to assign costs to products to facilitate external financial reporting and internal decision making. This chapter illustrates an absorption costing approach to calculating product costs known as job-order costing. I. Job-order costing: […]

Chapter 3a 1 If predetermined overhead rates are based on budgeted activity

Chapter 03 – Appendix A The Predetermined Overhead Rate and Capacity 3A-1 Chapter 03 Appendix A The Predetermined Overhead Rate and Capacity Answer Key True / False Questions 1. If predetermined overhead rates are based on budgeted activity and overhead […]

Chapter 3a 2 The Company Bases Its Predetermined Overhead

Chapter 03 – Appendix A The Predetermined Overhead Rate and Capacity 19. If the company bases its predetermined overhead rate on capacity, the predetermined overhead rate is closest to: A. $41.92 B. $31.32 C. $39.44 D. $40.11 Predetermined overhead rate […]

Chapter 3b 1 The overtime premium paid to factory workers is usually

TRUE AACSB: Reflective Thinking AICPA BB: Critical Thinking AICPA FN: Measurement Bloom’s: Knowledge Learning Objective: 03B-09 Properly account for labor costs associated with idle time; overtime; and fringe benefits. Level: Easy Chapter 03 – Appendix B Further Classification of Labor […]

Chapter 4 1 An additional 90000 Units Were Started Into Production

Chapter 04 – Process Costing 4-1 Chapter 04 Process Costing Answer Key True / False Questions 1. The following journal entry would be made in a processing costing system when units that have been completed with respect to the work […]

Chapter 4 2 The Gasson Company Uses The Weighted average

Chapter 04 – Process Costing 34. The Gasson Company uses the weighted-average method in its process costing system. The company’s ending work in process inventory consists of 10,000 units, 100% complete with respect to materials and 70% complete with respect […]

Chapter 4 3 The Cost Per Equivalent Unit For

Chapter 04 – Process Costing 54. The cost per equivalent unit for materials for the month in the first processing department is closest to: A. $16.32 B. $17.17 C. $15.91 D. $16.73 4-41 AACSB: Analytic AICPA BB: Critical Thinking AICPA […]

Chapter 4 4 The Total Cost Transferred From The

Chapter 04 – Process Costing 4-61 Kramer Corporation uses the weighted-average method in its process costing system. Data concerning the first processing department for the most recent month are listed below: Note: Your answers may differ from those offered below […]

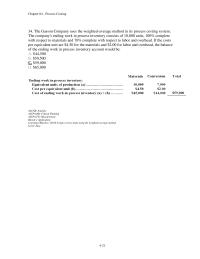

Chapter 4 5 Production And Cost Data For The

Chapter 04 – Process Costing Essay Questions 94. Larney Corporation uses process costing. A number of transactions that occurred in June are listed below. (1) Raw materials that cost $38,200 are withdrawn from the storeroom for use in the Mixing […]

Chapter 4 Homework Examples Service Departments Include Cafeteria Internal Auditing

76 2. The first step is to determine the equivalent units needed to complete beginning work in 3. The second step is to add the units started and completed during the period (5,100 units for materials and conversion). 4. The […]

Chapter 4 Homework For Example Managers Could Paid Bonus Profits

Problem 4-16 (continued) 2. Accounts Receivable Raw Materials (g) 1,400,000 Bal. 198,600 (a) 192,600 Bal. 6,000 Work in Process Blending Department Work in Process Bottling Department Bal. 32,800 (e) 722,000 Bal. 49,000 (f) 920,000 (a) 147,600 (a) 45,000 (b) 73,200 […]

Chapter 4 Homework Learning Objective Compute The Equivalent Units Production

63 Chapter 4 Lecture Notes Chapter theme: Managers need to assign costs to products to facilitate external financial reporting and internal I. Comparison of job-order and process costing A. Similarities between job-order and process costing i. Both systems assign material, […]

Chapter 4 Homework Materials Ending Work Process Inventory Equivalent Units

Chapter 4 Process Costing Solutions to Questions 4-1 A process costing system should be used in situations where a homogeneous product is produced on a continuous basis. 4-2 Job-order and processing costing are similar in the following ways: 1. Job-order […]

Chapter 4 Homework Cost from the beginning work in process inventory

Exercise 4A-9 (continued) 5. Materials Conversion Total Ending work in process inventory: Equivalent units of production …………………………………………… 240 120 Cost per equivalent unit …………………………………………………… $18.20 $23.25 Cost of ending work in process inventory …………………………….. $4,368 $2,790 $7,158 Units transferred out: […]

Chapter 4a 1 Units Completed During The Period Units In beginning

Chapter 04 – Appendix A FIFO Method 4A-1 Chapter 04 Appendix A FIFO Method Answer Key True / False Questions 1. The equivalent units in the ending work in process inventory will be the same under both the FIFO and […]

Chapter 4a 2 Ozogus Company Uses The FIFO Method

Chapter 04 – Appendix A FIFO Method 28. Ozogus Company uses the FIFO method in its process costing system. Operating data for the Brazing Department for the month of November appear below: What were the equivalent units for conversion costs […]

Chapter 4a 3 What Are The Equivalent Units For

Chapter 04 – Appendix A FIFO Method 46. What are the equivalent units for materials for the month in the first processing department? A. 9,000 B. 375 C. 8,300 D. 8,715 FIFO method Units started and completed during the period […]

Chapter 4a 4 The Equivalent Units For Labor And

Chapter 04 – Appendix A FIFO Method 63. The equivalent units for labor and overhead for the month of August are: A. 85,000 units B. 95,000 units C. 87,500 units D. 82,500 units FIFO method Units started and completed during […]

Chapter 4a 5 The company uses the FIFO method in its process costing

Chapter 04 – Appendix A FIFO Method 4A-72 71. Deluz Corporation uses the FIFO method in its process costing. The following data pertain to its Assembly Department for August. Required: Compute the equivalent units of production for both materials and […]

Chapter 4b 1 The step-down method allocates more total cost to operating

Chapter 04 – Appendix B Service Department Allocations 4B-1 Chapter 04 Appendix B Service Department Allocations Answer Key True / False Questions 1. The step-down method allocates more total cost to operating departments than does the direct method. 2. The […]

Chapter 4b 2 The Total Amount Administrative Department Cost

Chapter 04 – Appendix B Service Department Allocations 25. The total amount of Administrative Department cost allocated to the Adult Medicine Department is closest to: A. $28,368 B. $31,096 C. $43,235 D. $32,340 Allocation base for Administrative costs = 33,000 […]

Chapter 4b 3 The Total Corporate Law Department Cost

Chapter 04 – Appendix B Service Department Allocations 38. The total Corporate Law Department cost after allocations is closest to: A. $417,451 B. $417,540 C. $410,562 D. $394,660 Allocation base for Personnel costs = 24 + 111 + 176 = […]

Chapter 5 1 Reynold Enterprises sells a single product for $25

Chapter 05 – Cost-Volume-Profit Relationships 5-1 Chapter 05 Cost-Volume-Profit Relationships Answer Key True / False Questions 1. Reynold Enterprises sells a single product for $25. The variable expense per unit is $15 and the fixed expense per unit is $5 […]

Chapter 5 10 Churchwell Corporation Produces And Sells Single

Chapter 05 – Cost-Volume-Profit Relationships 218. Data concerning Maline Corporation’s single product appear below: Fixed expenses are $55,000 per month. The company is currently selling 1,000 units per month. Required: The marketing manager would like to cut the selling price […]

Chapter 5 11 Mitzel Corporation Has Provided Its Contribution

Chapter 05 – Cost-Volume-Profit Relationships 229. Madlem, Inc., produces and sells a single product whose selling price is $240.00 per unit and whose variable expense is $86.40 per unit. The company’s fixed expense is $720,384 per month. Required: Determine the […]

Chapter 5 2 Sensabaugh Inc Company That Produces And

Chapter 05 – Cost-Volume-Profit Relationships 40. Sensabaugh Inc., a company that produces and sells a single product, has provided its contribution format income statement for January. If the company sells 1,600 units, its total contribution margin should be closest to: […]

Chapter 5 3 Data Concerning Moscowitz Corporations Single Product

Chapter 05 – Cost-Volume-Profit Relationships 62. Data concerning Moscowitz Corporation’s single product appear below: Fixed expenses are $375,000 per month. The company is currently selling 8,000 units per month. The marketing manager would like to cut the selling price by […]

Chapter 5 4 Shiraki Corporation Produces And Sells Single

Chapter 05 – Cost-Volume-Profit Relationships 85. Shiraki Corporation produces and sells a single product. Data concerning that product appear below: The break-even in monthly dollar sales is closest to: A. $650,000 B. $687,722 C. $396,500 D. $1,016,667 CM ratio = […]

Chapter 5 5 What The Company’s Unit Contribution Margin

Chapter 05 – Cost-Volume-Profit Relationships 110. What is the company’s unit contribution margin? A. $4.70 B. $0.42 C. $2.15 D. $2.55 Unit contribution margin = Selling price per unit – Variable expenses per unit = ($1,128,000 240,000 units) – […]

Chapter 5 6 The Operating Leverage Is 033 Degree

Chapter 05 – Cost-Volume-Profit Relationships 137. The operating leverage is: A. 3 B. 8 C. 0.33 D. 5 Degree of operating leverage = Contribution margin Net operating income = $150,000 $50,000 = 3.0 5-101 AACSB: Analytic AICPA BB: […]

Chapter 5 7 Sales Decrease 500 Units Next Month

Chapter 05 – Cost-Volume-Profit Relationships 158. If sales decrease by 500 units by next month, by how much would fixed expenses have to be reduced to maintain the current net operating income? A. $7,500 B. $6,000 C. $2,000 D. $3,000 […]

Chapter 5 8 Assume The Company’s Monthly Target Profit

Chapter 05 – Cost-Volume-Profit Relationships 5-141 180. Assume the company’s monthly target profit is $31,000. The dollar sales to attain that target profit are closest to: AACSB: Analytic AICPA BB: Critical Thinking AICPA FN: Measurement Bloom’s: Application Learning Objective: 05-05 […]

Chapter 5 9 The Following Monthly Data Contribution Format

Chapter 05 – Cost-Volume-Profit Relationships 5-161 202. The following monthly data in contribution format are available for the MN Company and its only product, Product SD: The company produced and sold 300 units during the month and had no beginning […]

Chapter 5 Homework All Rights Reserved Solutions Manual

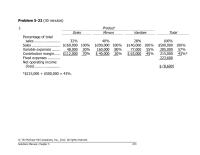

Problem 5-22 (30 minutes) 1. Product Sinks Mirrors Vanities Total Percentage of total sales ……………………. 32% 40% 28% 100% Sales ……………………… $160,000 100 % $200,000 100 % $140,000 100 % $500,000 100 % Variable expenses …….. 48,000 30 % 160,000 […]

Chapter 5 Homework Alternative Solution Sales 19000 Shirts 40 Per

Exercise 5-13 (30 minutes) 1. The contribution margin per person would be: Price per ticket ………………………………………….. $30 Variable expenses: Dinner …………………………………………………… $7 Favors and program …………………………………. 3 10 Contribution margin per person …………………….. $20 The fixed expenses of the Extravaganza […]

Chapter 5 Homework Fixed Cost Goods Sold Fixed Advertising

Problem 5-28 (continued) 4. Incremental contribution margin: $20,000 increased sales × 60% CM ratio ……….. $12,000 Less incremental fixed salary cost …………………… 8,000 Increased net operating income ……………………… $ 4,000 Yes, the position should be converted to a full-time basis. […]

Chapter 5 Homework Present Total Contribution Margin 3000 Units 30

Chapter 5 Cost-Volume-Profit Relationships Solutions to Questions 5-1 The contribution margin (CM) ratio is the ratio of the total contribution margin to total sales revenue. It is used in target profit and break-even analysis and can be used to quickly […]

Chapter 5 Homework The Equation Method Summarized This Slide Our

i. The emphasis is on cost behavior. Variable costs are separate from fixed costs. ii. The contribution margin is defined as the amount remaining from sales revenue after variable expenses have been deducted. iii. Contribution margin is used first to […]

Chapter 6 1 Segment Reporting Tools For Management27 Portion The

Chapter 06 – Variable Costing and Segment Reporting: Tools for Management 6-1 Chapter 06 Variable Costing and Segment Reporting: Tools for Management Answer Key True / False Questions 1. Under variable costing, all variable costs are treated as product costs. […]

Chapter 6 10 Variable Costing And Segment Reporting Tools

Chapter 06 – Variable Costing and Segment Reporting: Tools for Management 6-177 a. Unit product cost under absorption costing: b. Unit product cost under variable costing: c. Chapter 06 – Variable Costing and Segment Reporting: Tools for Management 6-178 AACSB: […]

Chapter 6 2 Swiatek Corporation Produces Single Product And

Chapter 06 – Variable Costing and Segment Reporting: Tools for Management 44. Swiatek Corporation produces a single product and has the following cost structure: The variable costing unit product cost is: A. $161 B. $225 C. $153 D. $158 6-21 […]

Chapter 6 3 Hansen Company Produces Single Product During

Chapter 06 – Variable Costing and Segment Reporting: Tools for Management 62. Hansen Company produces a single product. During the last year, Hansen had net operating income under absorption costing that was $5,500 lower than its income under variable costing. […]

Chapter 6 4 The Contribution Margin Per Unit Would

Chapter 06 – Variable Costing and Segment Reporting: Tools for Management 77. The contribution margin per unit would be: A. $12.10 B. $22.10 C. $17.70 D. $16.60 Variable expenses per unit: Selling price per unit = $850,000 20,000 units […]

Chapter 6 5 What The Net Operating Income For

Chapter 06 – Variable Costing and Segment Reporting: Tools for Management 100. What is the net operating income for the month under variable costing? A. $11,600 B. $2,900 C. $8,700 D. $0 6-81 AACSB: Analytic AICPA BB: Critical Thinking AICPA […]

Chapter 6 6 The Unit Product Cost Under Absorption

Chapter 06 – Variable Costing and Segment Reporting: Tools for Management Mennig Corporation produces a single product and has the following cost structure: 122. The unit product cost under absorption costing is: A. $92 B. $228 C. $182 D. $85 […]

Chapter 6 7 What Was The Absorption Costing Net

Chapter 06 – Variable Costing and Segment Reporting: Tools for Management 6-121 143. What was the absorption costing net operating income this year? AACSB: Analytic AICPA BB: Critical Thinking AICPA FN: Measurement Bloom’s: Application Learning Objective: 06-03 Reconcile variable costing […]

Chapter 6 8 Properly Constructed Segmented Income Statement Contribution

Chapter 06 – Variable Costing and Segment Reporting: Tools for Management 6-141 168. A properly constructed segmented income statement in a contribution format would show that the net operating income of the company as a whole is: AACSB: Analytic AICPA […]

Chapter 6 9 Variable Costing And Segment Reporting Tools

Chapter 06 – Variable Costing and Segment Reporting: Tools for Management 6-161 a. & b. Unit product costs c. & d. Income statements e. Reconciliation Chapter 06 – Variable Costing and Segment Reporting: Tools for Management 6-162 AACSB: Analytic AICPA […]

Chapter 6 Homework Key Concepts definitions Segment Part Activity Organization About

A. Variable costing treats only those costs of production that vary with output as product costs. This approach dovetails with the contribution approach income statement and supports CVP analysis because of its emphasis on separating variable and fixed costs. Helpful […]

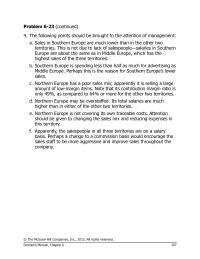

Chapter 6 Homework Northern Europe has a poor sales mix; apparently it is selling

Problem 6-23 (continued) 4. The following points should be brought to the attention of management: a. Sales in Southern Europe are much lower than in the other two territories. This is not due to lack of salespeople—salaries in Southern Europe […]

Chapter 6 Homework Notice The Situation Above That The Company

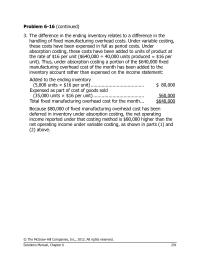

Problem 6-16 (continued) 3. The difference in the ending inventory relates to a difference in the handling of fixed manufacturing overhead costs. Under variable costing, these costs have been expensed in full as period costs. Under absorption costing, these costs […]

Chapter 6 Homework The Unit Product Cost Under Variable Costing

Chapter 6 Variable Costing and Segment Reporting: Tools for Management Solutions to Questions 6-1 Absorption and variable costing differ in how they handle fixed manufacturing overhead. Under absorption costing, fixed manufacturing overhead is treated as a product cost and hence […]

Chapter 7 1 Personnel Administration Example An Unit level Activity

Chapter 07 – Activity-Based Costing: A Tool to Aid Decision Making Chapter 07 Activity-Based Costing: A Tool to Aid Decision Making Answer Key True / False Questions 1. Unit-level activities are performed each time a unit is produced. TRUE AACSB: […]

Chapter 7 2 Spend love Corporation Has Provided The Following

Chapter 07 – Activity-Based Costing: A Tool to Aid Decision Making 34. Spendlove Corporation has provided the following data from its activity-based costing system: The company makes 430 units of product S78N a year, requiring a total of 1,120 machine- […]

Chapter 7 3 What Would The Total Overhead Cost

Chapter 07 – Activity-Based Costing: A Tool to Aid Decision Making 52. What would be the total overhead cost per bouquet according to the activity based costing system? In other words, what would be the overall activity rate for the […]

Chapter 7 4 How Much Overhead Cost Allocated The

Chapter 07 – Activity-Based Costing: A Tool to Aid Decision Making 7-61 Encarnacion Corporation has an activity-based costing system with three activity cost pools- Processing, Supervising, and Other. In the first stage allocations, costs in the two overhead accounts, equipment […]

Chapter 7 5 what is the overhead cost assigned to product

Chapter 07 – Activity-Based Costing: A Tool to Aid Decision Making 7-81 Ballweg Corporation has an activity-based costing system with three activity cost pools- Machining, Order Filling, and Other. In the first stage allocations, costs in the two overhead accounts, […]

Chapter 7 6 Cosgrove Company Manufactures Two Products Product

Chapter 07 – Activity-Based Costing: A Tool to Aid Decision Making 7-101 121. Cosgrove Company manufactures two products, Product K-7 and Product L-15. Product L-15 is of fairly recent origin, having been developed as an attempt to enter a market […]

Chapter 7 7 Activity based Costing Tool Aid Decision Making

Chapter 07 – Activity-Based Costing: A Tool to Aid Decision Making 7-117 a. Assign overhead costs to activity cost pools by applying the percentages in the Distribution of Resource Consumption Across Activity Cost Pools table to the respective costs. For […]

Chapter 7 Homework Most Organizations Use ABC Supplement Rather Than

141 B. The differences between ABC and traditional product costs i. The changes in product margins caused by switching from the traditional cost system to the activity-based costing system are as shown. Notice: 1. The traditional cost system overcosts the […]

Chapter 7 Homework Processing Other Customer 57000 Transactions B

Chapter 7 Activity-Based Costing: A Tool to Aid Decision Making Solutions to Questions 7-1 Activity-based costing differs from traditional costing systems in a number of ways. In activity-based costing, nonmanufacturing as well as manufacturing costs may be assigned to products. […]

Chapter 7 Homework The activity rates are computed by dividing the costs

Exercise 7A-3 (30 minutes) Supporting Direct Labor Batch Processing Order Processing Customer Service Total Total activity for the order ………………….. 1,920 4 1 1 direct labor- hours* batches order customer Manufacturing overhead: Indirect labor ………………………………… $ 3,456 $288 $ 18 […]

Chapter 7 Homework The average cost per diner differs from party to party under

Exercise 7-15 (30 minutes) 1. The first step is to determine the activity rates: Activity Cost Pools (a) Total Cost (b) Total Activity (a) ÷ (b) Activity Rate Serving parties ……. $12,000 5,000 parties $2.40 per party Serving diners …….. […]

Chapter 7 Homework The Lengthy List Activities That Emerges From

128 Chapter 7 Lecture Notes Chapter theme: This chapter introduces students to activity-based costing (ABC) which is a tool that has been embraced by a wide variety of service, manufacturing, and non-profit organizations. I. Activity-based costing: key definition II. How […]

Chapter 7 Homework The unit product cost of the high-volume product

Exercise 7B-2 (continued) The unit product costs combine direct materials, direct labor, and manufacturing overhead costs: Mercon Wurcon Direct materials ……………………………………… $10.00 $ 8.00 Direct labor …………………………………………… 3.00 3.75 Manufacturing overhead ($112,000 ÷ 10,000 units; $224,000 ÷ 40,000 units) ……………… […]

Chapter 7a 1 how they might adjust to changes in activity than

A. “Green” costs adjust automatically to changes in activity. B. “Yellow” costs could be adjusted to changes in activity, but such adjustments require management action; the adjustment is not automatic. C. “Red” costs cannot be adjusted to changes in activity. […]

Chapter 7b 1 Product W21k Is over head Applied Unit Product W21k

Chapter 07 – Appendix B Using a Modified Form of Activity-Based Costing to Determine Product Costs for External Reports 7B-1 Chapter 07 Appendix B Using a Modified Form of Activity-Based Costing to Determine Product Costs for External Reports Answer Key […]

Chapter 7b 2 The Unit Product Cost Product V47q

Chapter 07 – Appendix B Using a Modified Form of Activity-Based Costing to Determine Product Costs for External Reports 11. The unit product cost of product V47Q under the company’s traditional costing system is closest to: A. $53.30 B. $70.32 […]

Chapter 8 1 Assuming there Are Bad Debts The Expected Cash

8-5 Chapter 08 Profit Planning Answer Key True / False Questions 1. The production budget is typically prepared prior to the sales budget. 2. One benefit of budgeting is that it coordinates the activities of the entire organization. TRUE AACSB: […]

Chapter 8 2 The Selling And Administrative Expense Budget

34. The selling and administrative expense budget of Breckinridge Corporation is based on budgeted unit sales, which are 5,500 units for June. The variable selling and administrative expense is $1.00 per unit. The budgeted fixed selling and administrative expense is […]

Chapter 8 3 The Budgeted Cash Receipts For July

The Kafusi Company has the following budgeted sales: The regular pattern of collection of credit sales is 30% in the month of sale, 60% in the month following the month of sale, and the remainder in the second month following […]

Chapter 8 4 The May Cash Disbursements For Manufacturing

8-65 78. The May cash disbursements for manufacturing overhead on the manufacturing overhead budget should be: AACSB: Analytic AICPA BB: Critical Thinking AICPA FN: Measurement Bloom’s: Application Learning Objective: 08-06 Prepare a manufacturing overhead budget Level: Easy Salge Inc. bases […]

Chapter 8 5 Randall Company Merchandising Company That Sells

8-81 96. Randall Company is a merchandising company that sells a single product. The company’s inventories, production, and sales in units for the next three months have been forecasted as follows: Units are sold for $12 each. One fourth of […]

Chapter 8 Homework Budgeted Balance Sheet June Assets Cash

Problem 8-16 (30 minutes) 1. September cash sales ………………………………………. $ 7,400 September collections on account: July sales: $20,000 × 18% ……………………………… 3,600 August sales: $30,000 × 70% …………………………. 21,000 September sales: $40,000 × 10% ……………………. 4,000 Total cash collections ……………………………………….. […]

Chapter 8 Homework Quarter Cash Balance Beginning 50000 30000

Chapter 8 Profit Planning Solutions to Questions 8-1 A budget is a detailed quantitative plan for the acquisition and use of financial and other resources over a given time period. Budgetary control involves using budgets to increase the likelihood that […]

Chapter 8 Homework The First Step Preparing This Budget Multiply

164 ii. Assume the information as shown regarding Royal’s expected cash disbursements for materials. 1. The first step in calculating Royal’s cash disbursements is to insert the beginning accounts payable balance ($12,000) into the April column of the cash disbursements […]

Chapter 8 Homework The Production Budget Turn Directly Influences The

153 Chapter 8 Lecture Notes Chapter theme: This chapter focuses on the steps taken by businesses to achieve their planned levels of profits – a I. The basic framework of budgeting Learning Objective 1: Understand why organizations budget and the […]

Chapter 8 Homework Total Financing Cash Balance Ending May June

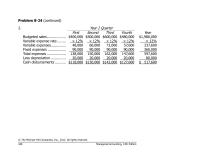

Problem 8-24 (continued) 2. Year 2 Quarter First Second Third Fourth Year Budgeted sales ……………… $400,000 $500,000 $600,000 $480,000 $1,980,000 Variable expense rate …….. × 12% × 12% × 12% × 12% × 12% Variable expenses ………….. 48,000 60,000 72,000 […]

Chapter 9 1 The Purpose Flexible Budget To Remove

Chapter 09 Flexible Budgets and Performance Analysis Chapter 09 Flexible Budgets and Performance Analysis Key True / False Questions 1. Fixed costs should not be included in a performance report because fixed costs are not controllable. FALSE AACSB: Reflective Thinking […]

Chapter 9 10 April Label Each Variance Favorable F Unfavorable

Chapter 09 Flexible Budgets and Performance Analysis 237. Zindell Corporation bases its budgets on the activity measure customers served. During December, the company planned to serve 21,000 customers, but actually served 19,000 customers. The company uses the following revenue and […]

Chapter 9 11 November required prepare The Clinics Flexible Budget Performance Report

Chapter 09 Flexible Budgets and Performance Analysis 9-207 251. Stailey Clinic uses patient-visits as its measure of activity. During September, the clinic budgeted for 3,200 patient-visits, but its actual level of activity was 2,800 patient-visits. The clinic uses the following […]

Chapter 9 12 Revenue 280per Customer Served Wages And Salaries

Chapter 09 Flexible Budgets and Performance Analysis 9-227 AACSB: Analytic AICPA BB: Critical Thinking AICPA FN: Measurement Bloom’s: Application Learning Objective: 09-01 Prepare a flexible budget Learning Objective: 09-04 Prepare a performance report that combines activity variances and revenue and […]

Chapter 9 13 The School Uses The Following Data Inits

Chapter 09 Flexible Budgets and Performance Analysis 278. During October, Keliihoomalu Clinic budgeted for 2,700 patient-visits, but its actual level of activity was 2,200 patient-visits. Revenue should be $27.30 per patient-visit. Personnel expenses should be $21,100 per month plus $6.80 […]

Chapter 9 14 The Clinic Has Provided The following Report required prepare The

Chapter 09 Flexible Budgets and Performance Analysis 9-260 AACSB: Analytic AICPA BB: Critical Thinking AICPA FN: Measurement Bloom’s: Application Learning Objective: 09-03 Prepare a report showing revenue and spending variances Learning Objective: 09-05 Prepare a flexible budget with more than […]

Chapter 9 2 Schlick Framings Cost Formula For Its

Chapter 09 Flexible Budgets and Performance Analysis 37. Schlick Framing’s cost formula for its supplies cost is $1,770 per month plus $12 per frame. For the month of August, the company planned for activity of 628 frames, but the actual […]

Chapter 9 3 The Activity Variance For Cleaning Equipment

Chapter 09 Flexible Budgets and Performance Analysis 65. The activity variance for cleaning equipment and supplies in June would be closest to: A. $800 F B. $730 F C. $730 U D. $800 U Because the flexible budget is greater […]

Chapter 9 4 The Revenue Variance For September Would

Chapter 09 Flexible Budgets and Performance Analysis 9-67 Roye Kennel uses tenant-days as its measure of activity; an animal housed in the kennel for one day is counted as one tenant-day. During September, the kennel budgeted for 3,300 tenant-days, but […]

Chapter 9 5 The Occupancy Expenses The Flexible Budget

Chapter 09 Flexible Budgets and Performance Analysis 108. The occupancy expenses in the flexible budget for May would be closest to: A. $17,718 B. $18,611 C. $18,086 D. $18,530 Cost = Fixed cost per unit + Variable cost per unit […]

Chapter 9 6 The Spending Variance For Expendables May

Chapter 09 Flexible Budgets and Performance Analysis 135. The spending variance for expendables in May would be closest to: A. $784 U B. $1,120 F C. $784 F D. $1,120 U Because the actual expense is greater than the flexible […]

Chapter 9 7 The Total Cost The Activity Level

Chapter 09 Flexible Budgets and Performance Analysis 9-127 159. The total cost at the activity level of 9,200 patient-visits per month should be: Yewston Hotel bases its budgets on guest-days. The hotel’s static budget for April appears below: A. $364,900 […]

Chapter 9 8 The Wages And Salaries The Planning

Chapter 09 Flexible Budgets and Performance Analysis 184. The wages and salaries in the planning budget for July would be closest to: A. $18,070 B. $17,239 C. $17,700 D. $17,670 Cost = Fixed cost per unit + Variable cost per […]

Chapter 9 9 The Net Operating Income The Flexible

Chapter 09 Flexible Budgets and Performance Analysis 9-167 208. The net operating income in the flexible budget for March would be closest to: AACSB: Analytic AICPA BB: Critical Thinking AICPA FN: Measurement Bloom’s: Application Learning Objective: 09-01 Prepare a flexible […]

Chapter 9 Homework Larry’s Lawn Service Computing Revenue And Spending

174 1. If the actual level of activity differs from what was planned, it would be misleading to evaluate performance by comparing actual costs to the static, unchanged planning budget. 3 1. May be prepared for any activity level in […]

Chapter 9 Homework This Procedure Provides Valid Benchmarks For Revenues

Chapter 9 Flexible Budgets and Performance Analysis Solutions to Questions 9-1 The planning budget is prepared for the planned level of activity. It is static because it is not adjusted even if the level of activity subsequently changes. cost has […]

Chapter 9 Homework This Would Require Great Deal Personal Courage

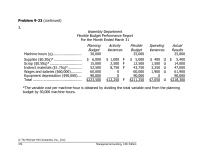

Problem 9-23 (continued) 3. Assembly Department Flexible Budget Performance Report For the Month Ended March 31 Planning Budget Activity Variances Flexible Budget Spending Variances Actual Results Machine-hours (q) ……………………… 30,000 25,000 25,000 Supplies ($0.20q)* …………………….. $ 6,000 $ 1,000 F […]

Chapter 9 Homework the production department is a cost center that does not have

Exercise 9-17 (20 minutes) Gelato Supremo Revenue and Spending Variances For the Month Ended July 31 Flexible Budget Actual Results Revenue and Spending Variances Liters (q) ………………………………. 4,900 4,900 Revenue ($13.50q) …………………. $66,150 $69,420 $3,270 F Expenses: Raw materials ($5.10q) […]