Archives

Accounting Chapter 1 Exchanges Capital Stock And Bonds That Occur

A. secondary markets B. primary markets C. stock exchanges D. tertiary markets A. extending credit B. maintaining a credit relationship C. not extending credit D. investing in credit instruments A. company treasurer B. stockholder in the company C. bank lending […]

Accounting Chapter 1 Interest Calculated The Original Principal Regardless The

Time Value of Money Module Key 1. The method of converting a future dollar amount into its present dollar value by removing the time value of money is called 2. Interest calculated on the original principal regardless of the number […]

Accounting Chapter 10 Alternative Terms For Property Plant And Equipment

Chapter 10—Property, Plant, and Equipment: Acquisition and Disposal Key 1. Alternative terms for property, plant, and equipment include all of the following except 2. All of the following would be classified as property, plant, and equipment except A. office buildings […]

Accounting Chapter 10 ralph company exchanged a machine for some land

Required: For each of the costs identified below, indicate the type of account in which the cost should be recorded by placing the appropriate letter in the space provided. ____ 1. The legal fees associated with the acquisition of land. […]

Accounting Chapter 11 A review of the parameters used in measuring depreciation

77. Which of the following is true regarding IFRS versus U.S. GAAP depreciation requirements? 78. IFRS require a review of the parameters used in measuring depreciation A. at least every year B. at least every quarter C. when events and […]

Accounting Chapter 11 The Service Life Asset May Measured All

Chapter 11—Depreciation and Depletion Key 1. Which one of the following statements is not true? 2. The service life of an asset may be measured by all of the following except A. units of output B. units of activity C. […]

Accounting Chapter 12 Salaries of personnel involved in searching for applications

67. The following costs were incurred by Mark Corporation during 2010: · Legal fees paid to attorneys in connection with a patent application related to a new invention developed by the company’s laboratory personnel: $40,000. · Salaries of personnel involved […]

Accounting Chapter 12 Which The Following Characteristics Not Common Both

Chapter 12—Intangibles Key 1. Which of the following characteristics is not common to both tangible and intangible assets? 2. Which of the following is not a characteristic of an intangible asset which distinguishes it from a tangible asset? A. generally […]

Accounting Chapter 13 All The Following Are Examples Legal Liabilities

Chapter 13—Current Liabilities and Contingencies Key 1. All of the following are examples of legal liabilities except 2. Under current standards of the FASB, liabilities include A. only legal obligations B. both legal and illegal obligations C. both legal and […]

Accounting Chapter 13 Gain Contingency That Reasonably Possible And

70. A gain contingency that is reasonably possible and for which the amount can be reasonably estimated should be 71. Short-term debt expected to be refinanced A. may be classified as long term if both the intent to refinance and […]

Accounting Chapter 14 the customer agreed to purchase an equal amount

135. On January 1, 2010, the Ryder Company issued $600,000 of eight-year bonds at 102. The stated annual interest rate is 8%, and interest is paid on June 30 and December 31. The bonds are callable at 105 plus accrued […]

Accounting Chapter 14 When Longterm Noninterest bearing Note Exchanged Solely

92. When a long-term non-interest-bearing note is exchanged solely for cash, the difference between the cash received and the face value of the note is recorded as 93. If a company sells its 20-year bonds at a premium, the premium […]

Accounting Chapter 14 Which The Following Not Reason For The

Chapter 14—Long-Term Liabilities and Receivables Key 1. Which of the following is not a reason for the issuance of long-term liabilities? 2. Which of the following is the best reason for the issuance of long-term liabilities? A. Debt financing offers […]

Accounting Chapter 15 Investments Debt And Equity Securities That Are

Chapter 15—Investments Key 1. Investments in debt and equity securities that are held for current resale by banks and stockbrokerage firms are termed 2. Investments that are typically held for short periods of time and sold by the company in […]

Accounting Chapter 15 prepare an investment premium amortization schedule

90. At December 31, 2010, Wilkerson had the following portfolio of equity securities available for sale: Cost Market Value Bark Co. stock $30 $32 Howl Co. stock 90 84 Required: a. Assuming any gain or loss is considered to be […]

Accounting Chapter 15 will be held at least 3 years and is classified

105. On December 31, 2010, the England Company held 8%, $200,000 bonds of Marshall Corporation that were purchased at an amount to yield 7%. The bonds were classified as held to maturity and had a carrying value of $208,640 on […]

Accounting Chapter 16 Enables the company to buy back more shares

123. On January 1, 2010, Microtech Company awarded a fixed compensation stock option plan to 40 executives. The plan allows each executive to buy 2,000 shares of the company’s $10 par common stock for $25 a share after a four-year […]

Accounting Chapter 16 one-fourth of these shares were converted into

83. When recording the conversion of preferred stock into common stock, if the total contributed capital eliminated in regard to the preferred stock is less than the common stock par value, the difference is debited to 84. The preference to […]

Accounting Chapter 16 The Corporate Form Organization Important The Us

Chapter 16—Contributed Capital Key 1. The corporate form of organization is important to the U.S. economy because 2. Universities, hospitals, and churches are examples of which type of corporation? A. stock companies B. privately held companies C. nonstock companies D. […]

Accounting Chapter 17 how the net amount for construction in progress

71. Monster, Inc. determined the following information concerning its common stock during 2010: January 1 10,500 shares outstanding March 1 Issued a 2-for-1 stock split July 1 Issued 1,000 additional shares October 1 Reacquired 2,000 shares Required: What should Monster, […]

Accounting Chapter 17 Which One The Following Indicators Intended Show

Chapter 17—Earnings Per Share and Retained Earnings Key 1. Which one of the following indicators is intended to show the potential impacts of possible future events on a corporation’s performance? 2. Which one of the following indicators is a company […]

Accounting Chapter 18 initial direct costs: defer and recognize over

Required: a. Assuming Brooksville uses the percentage-of-completi on method of revenue recognition, determine: (1) The balance of Construction in Progress at the end of 2010. (2) How the net amount for construction in progress inventory should be reported on the […]

Accounting Chapter 18 Revenue Recognition Issues Are Studied Because There

Chapter 18—Income Recognition and Measurement of Net Assets Key 1. Net assets increase from cost to selling price when revenue is recognized During At Time At Time of Production of Sale Cash Receipt I. Yes Yes Yes II. Yes Yes […]

Accounting Chapter 19 Differences Between Pretax Financial Income And Taxable

Chapter 19—Accounting for Income Taxes Key 1. Which statement regarding the objectives of financial accounting and the Internal Revenue Code is true? 2. Differences between pretax financial income and taxable income in an accounting period that will not reverse in […]

Accounting Chapter 19 Intra period Tax Allocation Would Appropriate For

55. The Brownwood Company reports the following for both pretax financial and taxable income: Enacted Year Income (Loss) Tax Rates 2010 $ 40,000 30% 2011 60,000 35% 2012 80,000 30% 2013 (200,000) 30% Brownwood uses the carryback provision for net […]

Accounting Chapter 2 How Many Statements Financial Accounting Concepts Have

Chapter 2—Financial Reporting: Its Conceptual Framework Student: ___________________________________________________________________________ 1. Which of the following statements is not true with regard to the benefits derived from the FASB’s conceptual framework of accounting? 2. How many Statements of Financial Accounting Concepts have been […]

Accounting Chapter 2 how much do you have to invest today to have

56. Using the compound interest tables, solve the following questions. Required: a. What amount of interest will be earned on an investment of $7,500 left on deposit by Mary for three years at 7% compounded annually? b. Taylor deposited $10,000 […]

Accounting Chapter 2 Which The Following Sets Includes Only

50. Which of the following sets includes only accounting assumptions and conventions? 51. The use of the historical cost principle is justified because the resulting information has the primary quality ingredients of A. neutrality and predictive value B. representational faithfulness […]

Accounting Chapter 20 company began a defined benefit pension plan

57. Matilda, Inc. amended its defined benefit pension plan as of January 1, 2010. Matilda received a report from its actuary stating that at the beginning of 2010 unrecognized prior service cost resulting from the amendment amounted to $144,000. The […]

Accounting Chapter 20 Internal Revenue Code Rule That Impacts The

Chapter 20–Accounting for Postemployment Benefits Key 1. An Internal Revenue Code rule that impacts the design of pension plans is 2. A pension plan provides for future retirement income based on the employee’s income and length of service with the […]

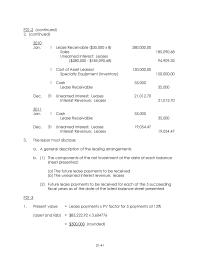

Accounting Chapter 21 January Lessee Company Incorrectly Recorded Capital Lease

Chapter 21—Accounting for Leases Key 1. On January 1, Lessee Company incorrectly recorded a capital lease as an operating lease. The ratio of debt to stockholders’ equity would be 2. On January 1, Lessee Company incorrectly recorded a 10-year operating […]

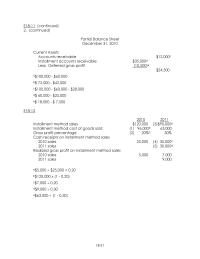

Accounting Chapter 21 the lease agreement calls for five equal annual

80. Exhibit 21-4 On January 1, 2010, General Leasing Company entered into a direct financing lease with a lessee, Lee Company. The lease agreement calls for five equal annual payments of $60,000 at the beginning of each year with the […]

Accounting Chapter 21 what would be the charge to cost of goods sold

115. Tempe Corp. leased some equipment to Glendale, Inc. on January 1, 2010. The lease required six annual payments, with the first payment due on December 31, 2010. The cost, and also fair value, of the equipment was $140,000, and […]

Accounting Chapter 22 which statement best defines a company’s operating

Chapter 22—The Statement of Cash Flows Key 1. In a statement of cash flows, increases or decreases in noncurrent assets are most closely associated with 2. What is the primary purpose of a company’s statement of cash flows? A. to […]

Accounting Chapter 22 Your Friend Business And Wants Your

59. Accounting information from the records of the Singleton Corporation at the end of 2010 is shown below: Net income $100,000 Proceeds from sale of long-term investment in marketable securities 20,000 Proceeds from sale of building 80,000 Gain on sale […]

Accounting Chapter 23 its financial statements for the years ended

68. Exhibit 23-6 Nora Company has a fiscal year ending on December 31. Its financial statements for the years ended December 31, 2010 and 2011, contained the following errors: 2010 2011 Ending inventory $9,000 understated $15,000 overstated Bad debt expense […]

Accounting Chapter 23 The Accounting Changes Identified Current GAAP Include

Chapter 23—Accounting for Changes and Errors Key 1. The accounting changes identified by current GAAP include all of the following except 2. Generally accepted methods of accounting for a change in accounting principle include A. restating prior years’ financial statements […]

Accounting Chapter 3 Countywide Inc Reports The Following Information

Required: Prepare a partial income statement through gross profit on sales. 78. Countywide, Inc., reports the following information at the end of the year 2010: Dividends Distributed $ 560 Inventory, December 31, 2010 620 Income Taxes Payable 408 Accumulated Depreciation-Equipment […]

Accounting Chapter 3 Selected Adjusting Entries Follow Insurance Expense

87. Selected adjusting entries follow: a. Insurance Expense 2,000 Prepaid Insurance 2,000 b. Rent Revenue 1,200 Unearned Rent 1,200 c. Salaries Expense 1,900 Salaries Payable 1,900 d. Interest Expense 300 Interest Payable 300 e. Interest Receivable 800 Interest Revenue 800 […]

Accounting Chapter 3 Which The Following Contra Account Unearned Rental

Chapter 3—Review of a Company’s Accounting System Key 1. Which of the following is a contra account? 2. Which T-account is incorrect? A. B. C. D. 3. Which accounts are increased with debits? A. Cost of Goods Sold, Capital Stock, […]

Accounting Chapter 4 All The Following Items Would Appear The

Chapter 4—The Balance Sheet and the Statement of Changes in Stockholders’ Equity Key 1. If the owners’ equity at the end of the accounting period is greater than the owners’ equity at the beginning of the accounting period, the firm’s […]

Accounting Chapter 4 The Balance Sheet Contains The Major

Required: Match each measurement alternative to its balance sheet element by placing the appropriate letter in the space provided. 66. The following data were taken from the Otay, Inc. balance sheet: Accounts payable $ 150 Inventory 250 Retained earnings 40 […]

Accounting Chapter 5 For Income Reporting Purposes Items Can

____ 1. Merchandise inventory (beginning) ____ 2. Cash dividends declared on common stock ____ 3. Flood loss (infrequent and unusual) ____ 4. Expenses incurred as a result of a strike ____ 5. Discount on bonds payable ____ 6. Correction of […]

Accounting Chapter 5 The Following Income Statement Information For

89. The following income statement information for 2010 and 2011 was obtained from the accounting records of the Upperton Company. 2010 2011 Sales $200,000 $150,000 Beginning inventory (a) ________ (e) ________ Purchases (net) 40,000 50,000 Ending inventory 25,000 5,000 Cost […]

Accounting Chapter 5 Which The Following Best Describes The Characteristics

Chapter 5—The Income Statement and the Statement of Cash Flows Key 1. Which of the following best describes the characteristics that relate to the income statement? 2. The income statement is an important financial statement for all of the following […]

Accounting Chapter 6 Auditor Issues Audit Report That Expresses Three

Chapter 6—Additional Aspects of Financial Reporting and Financial Analysis Key 1. Which one of the following statements regarding market efficiency is false? 2. An auditor issues an audit report that expresses three opinions. Which of the following is not one […]

Accounting Chapter 6 The Following Information Was Obtained From

Included in Latin’s operating expenses are general corporate expenses of $16,000. Required: Based on the provisions of current GAAP, prepare a schedule that reflects required disclosures about operating segments from the above information for Latin Company exclusive of any footnotes. […]

Accounting Chapter 7 Record Sales Return Dec Gross Price Net

d. To record sales return on Dec. 8: Gross Price Net Price Allowance Method Method Method Cash ________ ________ ________ Accounts Receivable ________ ________ ________ Sales ________ ________ ________ Sales Discounts ________ ________ ________ Allowance for Sales Discounts ________ ________ […]

Accounting Chapter 7 Required Prepare The Necessary Journal Entries Record

Required: Prepare the necessary journal entries to record the transactions on Stewart Ski Company’s books. 104. Markham Corp. sold goods for $36,000 on July 17, 2010, and accepted a 12%, 90-day note. On August 1, the note was discounted at […]

Accounting Chapter 7 Which The Following Would Included Cash And

Chapter 7—Cash and Receivables Key 1. Which of the following would be included in cash and cash equivalents on the balance sheet? 2. Which of the following would not be considered a cash equivalent? A. certificates of deposit B. commercial […]

Accounting Chapter 8 1 Manufacturing Company Typically Has How Many Inventory

Chapter 8—Inventories: Cost Measurement and Flow Assumptions Key 1. A manufacturing company typically has how many inventory accounts? 2. A manufacturing firm would not normally have an account titled A. Goods in Process Inventory B. Raw Materials Inventory C. Merchandise […]

Accounting Chapter 8 what is total ending inventory in dollars

69. On January 15, Watson, Inc. purchased merchandise inventory at an invoice price of $300,000, with terms of 3/15, n/30. Required: a. Assuming that the full, appropriate payment was made on January 28, prepare journal entries to record the purchase […]

Accounting Chapter 9 Companies May Express Their Gross Profit

104. England Inc. incurred a fire loss. Certain information follows: Gross profit on cost 25% Purchase returns $ 1,000 Sales 43,200 Beginning inventory 14,500 Cost of goods not burned 6,250 Accounts receivable 5,000 Purchases 41,500 Purchase discounts 500 Required: Using […]

Accounting Chapter 9 Madeline Sports Uses The Dollar value Lifo

74. Madeline Sports uses the dollar-value LIFO retail method. The price index on January 1, 2010, was 100, and on that date the inventory was $20,000 (retail) and $14,000 (cost). Additional information follows: 2010 2011 Purchases, retail $160,000 $204,000 Purchases, […]

Accounting Chapter 9 The Most Common Approach Implementing The Lower

Chapter 9—Inventories: Special Valuation Issues Key 1. The most common approach to implementing the lower of cost or market rule for inventory valuation is to apply it 2. Which application of the lower of cost or market rule will generally […]

Chapter 1 Converted Factor For Present Value Deferred Annuity

TVM-1 TIME VALUE OF MONEY MODULE CONTENT ANALYSIS OF EXERCISES AND PROBLEMS Number Content Time Range (minutes) EM-1 Future Value. (Easy) Single investment, compound interest. 5-10 EM-2 Future Value. (Easy) Single investment, compound interest. 5-10 EM-6 Amount of Each Cash […]

Chapter 1 Issues Exposure Draft The Proposed Statement

1-1 CHAPTER 1 THE ENVIRONMENT OF FINANCIAL REPORTING CONTENT ANALYSIS OF CASES Number Content Time Range (minutes) C1-1 Pronouncements. Matching a list of descriptive statements with a list of pronouncements establishing or related to generally accepted accounting principles. 5-10 C1-2 […]

Chapter 10 Thus Includes The Expected Cash Inflow From

10-38 P10-11 (continued) Feb. 14 Repair Expense 700 Cash (Accounts Payable, etc.) 700 Repairs to machine. 2. Under IFRS, the cost of reorganizing PP&E is expensed. Therefore, the journal entry on March 27 would be: Mar. 27 Office Expenses 1,200 […]

Chapter 10 Compute total acquisition costs of machine and prepare journal

10-1 CHAPTER 10 PROPERTY, PLANT, AND EQUIPMENT: ACQUISITION AND DISPOSAL CONTENT ANALYSIS OF EXERCISES AND PROBLEMS Number Content Time Range (minutes) E10-1 Determination of Cost. (Moderate) Analysis of numerous items to determine whether or not to include in property, plant, […]

Chapter 10 Loss Due to Modifications to Building Land and Buildings

P10-1 (continued) 8. Building 1,000 Land and Buildings 1,000 Cost of insurance during construction (alternatively, could be recorded as Insurance Expense). 9. Profit (Gain) on Construction 12,000 Land and Buildings 12,000 Reversing of profit improperly recognized. 10. Loss Due to […]

Chapter 11 Changing The Beginning The Sixth Year Produces

11-21 E11-12 (continued) Difference in 2010: E11-13 Note to Instructor: This exercise assumes simple knowledge of material in Chapter 5 and Chapter 23. 1. Change in estimate–accounted for prospectively: Straight-line depreciation = 10 $10,000$210,000 − = $20,000 per year Book […]

Chapter 11 Continued Pell Corporation Depreciation Expense For

P11-21 (continued) 2. PELL CORPORATION Depreciation Expense For the Year Ended December 31, 2010 Land improvements: Cost $ 180,000 Straight-line rate [100% ÷ 15] x 6 2/3% Total depreciation on land improvements $ 12,000 Building: Carrying amount 12/31/09 ($1,500,000 – […]

Chapter 11 Error accounted for as a prior period adjustment

P11-12 (continued) 1. (continued) 2010: Sold 50,000 tons Depletion deducted from income = 50,000 tons x $1.25 = $62,500 Depletion included in inventory = 30,000 tons x $1.25 = $37,500 2011: Sold 120,000 tons Depletion deducted from income = 120,000 […]

Chapter 11 which the benefits are recognized as revenues

11-1 CHAPTER 11 DEPRECIATION AND DEPLETION CONTENT ANALYSIS OF EXERCISES AND PROBLEMS Number Content Time Range (minutes) E11-1 Depreciation Methods. (Easy) Straight-line, hours worked, units of output. 5-10 E11-5 Rate of Return. (Moderate) Determination under straight-line and double-declining balance methods. […]

Chapter 12 The Impairment Loss The Difference Between The

12-1 CHAPTER 12 INTANGIBLES CONTENT ANALYSIS OF EXERCISES AND PROBLEMS Number Content Time Range (minutes) E12-1 Patent. (Easy) Amount to be capitalized. Determination of economic life. 5-10 E12-6 (AICPA adapted). Research and Development Costs. (Easy) Determination of amount charged to […]

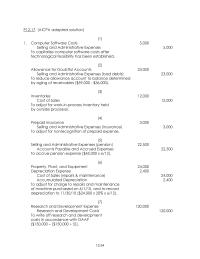

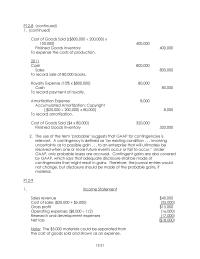

Chapter 12 The Penalty Extraordinary Item Rather Than Part

12-34 P12-17 (AICPA adapted solution) (1) 1. Computer Software Costs 5,000 (2) Allowance for Doubtful Accounts 23,000 Selling and Administrative Expenses (bad debts) 23,000 To reduce allowance account to balance determined by aging of receivables ($59,000 – $36,000). (3) Inventories […]

Chapter 12 when one or more future events occur or fail to occur

P12-8 (continued) 1. (continued) Cost of Goods Sold [($800,000 ÷ 200,000) x 100,000] 400,000 Finished Goods Inventory 400,000 To expense the costs of production. 2011 Cash 800,000 Sales 800,000 To record sale of 80,000 books. Royalty Expense (10% x $800,000) […]

Chapter 13 a provision that has a 51% chance of occurring is accrued

13-1 CHAPTER 13 CURRENT LIABILITIES AND CONTINGENCIES CONTENT ANALYSIS OF EXERCISES AND PROBLEMS Number Content Time Range (minutes) E13-1 Cash Discounts. (Easy) Accounts payable, perpetual inventory system. Net-of-cash discount approach. Journal entries. 5-10 E13-5 Compensated Absences. (Moderate) No sick leave […]

Chapter 13 Current Liabilities Estimated Premium Claims Outstanding

SOLUTIONS TO PROBLEMS P13-1 1. 2010 Dec. 24 Equipment: Computer [($60,000 – ($60,000 x 0.02)] 58,800 Accounts Payable: Computers International 58,800 29 Cash 60,000 Notes Payable: First Local Bank 60,000 30 Retained Earnings 20,000 Dividends Payable (10,000 x $2.00) 20,000 […]

Chapter 13 However Adequate Disclosure Should Made Gain Contingencies

P13-17 (continued) Jan. 26 Accounts Payable 29,400 Purchases Discounts Lost 600 Cash 30,000 Mar. 31 Vans 19,950 Cash 9,950 Notes Payable 10,000 May 1 Cash [$50,000 – ($50,000 x 0.12)] 44,000 Discount on Notes Payable 6,000 Notes Payable 50,000 Nov. […]

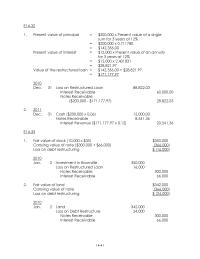

Chapter 14 Cash Credita Interest Expense Debit b Unamortized Premium

14-41 E14-32 1. Present value of principal = $200,000 x Present value of a single sum for 3 years at 12% 2. 2011 Dec. 31 Cash ($200,000 x 0.06) 12,000.00 Notes Receivable 8,541.36 Interest Revenue ($171,177.97 x 0.12) 20,541.36 E14-33 […]

Chapter 14 Determination Interest Rate Present Value Note Annual

E14-9 (con tin ued) 2. (continued) Dec. 31 Interest Expense 1,616.67 Premium on Bonds Payable [($3,000 ÷ 120 months) x 2 months] 50.00 Interest Payable ($100,000 x 0.10 x 2/12) 1,666.67 3. 2012 Feb. 1 Interest Expense* 485 Premium on […]

Chapter 14 Gain or loss recognized in the period of extinguishment

14-92 C14-4 (continued) 1. (continued) c. Gain or loss recognized in the period of extinguishment. Proponents of this method state that the early extinguishment of debt refunded actually does not differ from other types of extinguishment of debt where the […]

Chapter 14 That Is Different Interest Cost Would Incurred

14-1 CHAPTER 14 LONG-TERM LIABILITIES CONTENT ANALYSIS OF EXERCISES AND PROBLEMS Number Content Time Range (minutes) E14-1 Bond Issue at Par. (Easy) Plus accrued interest. Semiannual interest payments. Journal entries. 5-10 E14-6 Proceeds from Bond Issues. (Easy) Determination if sold […]

Chapter 14 The Effective Yield Rate The Interest Rate

P14-18 (continued) 2. (continued) 2013 Dec. 31 Cash 2,222,000.00 Notes Receivable 2,019,998.65 Interest Revenue 202,001.35 3. Transfer of stock: Fair value of stock (160,000 x $14.50) $2,320,000.00 Carrying value of note (2,434,031.82) Loss on debt restructuring $ ( 114,031.82) 2010 […]

Chapter 14 Total interest income for year ended

P14-8 (continued) 3. (continued) After conversion: Market value method Debt to equity ratio = Total liabilities ÷ Total stockholders’ equity = $3,000,000 ÷ ($3,500,000 + $210,000) + $109,200) = 0.79 4. Cash 1,620,000 Bonds Payable 1,560,000a Additional Paid-in Capital: Conversion […]

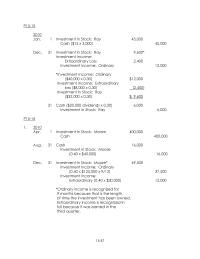

Chapter 15 Earnings Under The Equity Method Are Recognized

P15-15 2010 Jan. 1 Investment in Stock: Ray 45,000 Cash ($15 x 3,000) 45,000 Dec. 31 Investment in Stock: Ray 9,600* Investment Income: Extraordinary Loss 2,400 Investment Income: Ordinary 12,000 *Investment Income: Ordinary ($40,000 x 0.30) $12,000 Investment Income: Extraordinary […]

Chapter 15 However Previously Recorded Income Remains Part The

15-1 CHAPTER 15 INVESTMENTS CONTENT ANALYSIS OF EXERCISES AND PROBLEMS Number Content Time Range (minutes) E15-1 Trading Securities. (Easy) Journal entries. Unrealized holding gain. Balance sheet disclosure. 10-15 E15-5 Available-for-Sale Securities. (Easy) Journal entries. Balance sheet disclosure. 15-20 E15-6 Held-to-Maturity […]

Chapter 15 The company would make the same journal entries

E15-12 2010 Dec. 31 Cash ($100,000 x 0.08) 8,000 Interest Revenue ($107,023.56 x 0.07) 7,491.65 Investment in Held-to-Maturity Debt Securities ($8,000 – $7,491.65) 508.35 31 Investment in Available-for-Sale Securities 106,515.21 Investment in Held-to-Maturity Debt Securities ($107,023.56 – $508.35) 106,515.21 31 […]

Chapter 15 Bond Investment Interest Revenue and Discount Amortization

P15-6 (continued) For Semiannual 2. Period Ended 6/30/10 12/31/10 Interest revenue $3,435a $4,597b Loss on sale of securities – (254) Gain on sale of securities – 441 a$1,455 + $1,980 b$1,150 + $1,468 + $1,979 3. Balance Sheet As of […]

Chapter 16 Mar Memorandum Entry Extend The

E16-17 1. (1) Treasury Stock: Preferred ($53 x 250) 13,250 Cash 13,250 (2) Treasury Stock: Common ($20 x 500) 10,000 Cash 10,000 (3) Cash ($27 x 200) 5,400 Treasury Stock: Common ($20 x 200) 4,000 Additional Paid-in Capital from Treasury […]

Chapter 16 The Two Segments Corporations Contributed Capital

16-1 CHAPTER 16 CONTRIBUTED CAPITAL CONTENT ANALYSIS OF EXERCISES AND PROBLEMS Number Content Time Range (minutes) E16-1 Common Stock Issuance. (Easy) Par-value, no-par (with and without a stated value). Record sale. 5-10 E16-5 Stock Subscription. (Easy) Journal entries to record […]

Chapter 16 This Right Often Not Important Except The

P16-11 (continued) 2. Contributed Capital Preferred stock (6%, $50 par, 8,000 shares authorized, 4,950 shares issued and outstanding) $247,500 Common stock ($4 stated value, 60,000 shares authorized, 30,200 shares issued and outstanding) 120,800 Common stock option warrants 27,000 Additional paid-in […]

Chapter 16 Under The Par Value Method Treasury Stock

C16-6 (AICPA adapted solution) 1. There are four basic rights inherent in ownership of common stock. The first right is that common shareholders may participate in the actual management of the corporation through participation and voting at the corporate stockholders […]

Chapter 17 Assessments Stockholders Forfeitures Stock Subscriptions

17-57 DANA COMPANY Statement of Changes in Stockholders’ Equity For Year Ended December 31, 2010 Compre- Preferred Stock Common Stock Additional Paid-In Capital Accumulated Other Explanation hensive Income Shares Issued Par Value Shares Issued Par Value Preferred Stock Common Stock […]

Chapter 17 Corporation May Restrict Its Retained Earnings

17-1 CHAPTER 17 EARNINGS PER SHARE AND RETAINED EARNINGS CONTENT ANALYSIS OF EXERCISES AND PROBLEMS Number Content Time Range (minutes) E17-1 Weighted Average Shares. (Moderate) Stock dividend, stock split, reacquisition. 10-20 E17-2 Comparative EPS. (Easy) Weighted average shares, stock split, […]

Chapter 17 Retained earnings are reduced more by a small stock

17-21 E17-13 (continued) 1. (continued) (5) Retained Earnings (10,000 x $0.70) 7,000 2. (1) (2) (3) (4) (5) Current assets Investment in M bonds Fixed assets (net) Current assets Fixed assets (net) Current assets Investment in M bonds Fixed assets […]

Chapter 17 Retained Earnings Previously Reported January 2010 Add

P17-10 (continued) Schedule 1: Distribution of Remaining Retained Earnings Common stock 8% Preferred stock Total Dividends on common stock at preferred rate ($500,000 x 8%) Distribution of remaining retained earnings of $406,000* based on the ratio of par values: Common […]

Chapter 18 The Notes Receivable Are Properly Recorded Their

18-56 C18-5 (continued) 3. Classifying “deferred gross profit” as a deferred credit is the traditional treatment, but its support is diminishing with the decline in the use of the deferred credit caption and with the growing view that the credit […]

Chapter 18 The Seller Has Transferred The Buyer The

18-1 CHAPTER 18 INCOME RECOGNITION AND MEASUREMENT OF NET ASSETS CONTENT ANALYSIS OF EXERCISES AND PROBLEMS Number Content Time Range (minutes) E18-1 Revenue Recognition Alternatives. (Moderate) Computation of revenue, expense, and gross profit over 3 year period for various recognition […]

Chapter 18 The Three Necessary Conditions Are Not Often

18-41 P18-9 (continued) Deferred Gross Profit, 2009 11,800a Gross Profit Realized on Installment Sales 11,800 a$16,000 – $700 – $3,500 Cash 87,500c Installment Accounts Receivable, 2010 87,500 c$17,500 ÷ 0.20, or $200,000 – $112,500 Gross Profit Realized on Installment Sales […]

Chapter 18 the account titles are the same as that used in the chapter

E18-11 (continued) 2. (continued) Partial Balance Sheet December 31, 2010 Current Assets Accounts receivable $12,000c Installment accounts receivable $35,000d Less: Deferred gross profit (10,500)e $24,500 a$100,000 – $60,000 b$ 72,000 – $42,000 c$100,000 – $60,000 – $28,000 d$ 60,000 – […]

Chapter 19 A valuation allowance is not needed because the company

E19-14 (continued) 2. LESTER CORPORATION Statement of Retained Earnings For Year Ended December 31, 2010 Retained earnings, January 1, 2010 $191,000 Less: Prior period adjustment, understatement of 2006 bad debt expense (net of $3,500 income tax credit) (10,500) Adjusted retained […]

Chapter 19 For Operating Loss Carryforward The Tax Effect

19-36 P19-13 (continued) 5. Current Liabilities P19-14 1. 2010 Dec. 31 Income Tax Expense 35,500c Gain on Disposal of Division F ($23,000 x 0.30) 6,900 Retained Earnings ($15,000 x 0.30) 4,500 Deferred Tax Liability 2,000b Extraordinary Loss ($18,000 x 0.30) […]

Chapter 19 The Income Tax Laws Rates Are

19-1 CHAPTER 19 ACCOUNTING FOR INCOME TAXES CONTENT ANALYSIS OF EXERCISES AND PROBLEMS Number Content Time Range (minutes) E19-1 Future Taxable Amount. (Easy) Deferred tax liability. Higher future tax rate. Scheduling. Preparation of income tax journal entry. 10-15 E19-5 Valuation […]

Chapter 2 Financial Information Needed Help Establish Expectations About

2-1 CHAPTER 2 FINANCIAL REPORTING: ITS CONCEPTUAL FRAMEWORK CONTENT ANALYSIS OF CASES Number Content Time Range (minutes) C2-1 Qualitative Characteristics. Matching of definitions to the qualities of useful accounting information. 10-20 C2-5 (AICPA adapted). Cost and Expense Recognition. Rationale for […]

Chapter 2 Looking Down The 12 Column The Table

TVM-21 PM-6 1. o P = ) in, o C(P 3. deferred P = )] ik, o (P) ik,n o C[(P − + deferred P = )] 5.5%i5,k o (P) 5.5%i13,kn o C[(P == − ==+ deferred P = $8,000 […]

Chapter 2 The Amount The Contract Price Recognized Should

2-12 C2-9 Accounting information is relevant if it can make a difference in a decision by helping users predict the outcomes of past, present, and future events or confirm or correct prior expectations. To be relevant, accounting information must be […]

Chapter 20 Continued Service Cost Interest Cost Projected

20-32 P20-10 (continued) 3. Service cost $183,000 Interest cost on projected benefit obligation 4. 2010 Jan. 01 Other Comprehensive Income: Prior Service Cost 88,000 Accrued/Prepaid Pension Cost 88,000 Dec. 31 Pension Expense 197,490 Accrued/Prepaid Pension Cost 2,510 Cash 200,000 31 […]

Chapter 20 GAAP Requires That The Net Gain Loss

20-1 CHAPTER 20 ACCOUNTING FOR POSTEMPLOYMENT BENEFITS CONTENT ANALYSIS OF EXERCISES AND PROBLEMS Number Content Time Range (minutes) E20-1 Pension Expense. (Easy) Computation of pension expense, journal entry. 5-10 E20-5 Pension Expense Different than Funding. (Moderate) Computation of pension expense, […]

Chapter 20 Total Expected Years Future Service 2010 Amortization

SOLUTIONS TO PROBLEMS P20-1 1. 2010 2011 Service cost $211,000 $217,000 Interest cost on projected benefit obligation 42,000 45,000 Expected return on plan assets (27,000) (28,000) Amortization of prior service cost 7,000 6,000 Amortization of net (gain) loss (3,000) 4,000 […]

Chapter 21 Circuit Village Isn’t Aware The 14 Rate

21-72 P21-15 1. Application of Criteria for Determination of Lease Classification Column A Criteria Met Remarks 1. Transfer of ownership at end of lease No Column B Criteria Met 1. Collectibility assured Yes 2. No uncertainties Yes Since one or […]

Chapter 21 Column Criteria Collectibility Assured Yes Uncertainties Yes

21-21 E21-6 (con tin ued) 2. (continued) Dec. 31 Depreciation Expense: Leased Equipment 6,000 E21-7 1. Selling price (fair value and the net investment) = PV 12%)i4,n ($50,000 == = $50,000 x 3.037349 = $151,867.45 2. Summary of lease receipts […]

Chapter 21 Dec Initial Direct Sales type Lease Expense Cash

21-61 P21-9 (continued) 2. (c) Summary of Lease and Interest Payments (1) Murrell Builders Benjamin Company Date (2) Lease Payment Required Lease Payment Received (3) Interest Expense Interest Revenue (4) Balance of Lease Obligation Net Investmenta January 1, 2010 $50,000.00 […]

Chapter 21 Heavy Equipment Less Accumulated Amortization The Following

P21-2 (continued) 2. (continued) 2010 Jan. 1 Lease Receivable ($35,000 x 8) 280,000.00 Sales 185,090.68 Unearned Interest: Leases ($280,000 – $185,090.68) 94,909.32 1 Cost of Asset Leased 150,000.00 Specialty Equipment (Inventory) 150,000.00 1 Cash 35,000 Lease Receivable 35,000 Dec. 31 […]

Chapter 21 Including Any Profit Thereon 2 The Unguaranteed

21-1 CHAPTER 21 ACCOUNTING FOR LEASES CONTENT ANALYSIS OF EXERCISES AND PROBLEMS Number Content Time Range (minutes) E21-1 Operating Lease. (Easy) Annual rental payments, no renewable option clause, executory costs. Lessee’s journal entries to record agreement, payments, expenses. 5-10 E21-4 […]

Chapter 22 Continued Fazzi Company Balance Sheet December

22-21 E22-9 (continued) FAZZI COMPANY Balance Sheet December 31, 2010 Assets Liabilities and Stockholders’ Equity Cash $ 1,500 Current liabilities $ 1,700 E22-10 ANDELL COMPANY Statement of Cash Flows For Year Ended December 31, 2010 Net Cash Flow From Operating […]

Chapter 22 Financing activities during an accounting period

22-1 CHAPTER 22 THE STATEMENT OF CASH FLOWS CONTENT ANALYSIS OF EXERCISES AND PROBLEMS Number Content Time Range (minutes) E22-1 Classification of Cash Flows. (Easy) Determination of the proper section and of the direction of cash flow for various items. […]

Chapter 22 Less Gain Sale Carrying Value Sold Add

P22-7 (continued) 1. (continued) Worksheet Entries Debit Credit Net Cash Flow From Operating Activities Net income Add: Depreciation expense Decrease in accounts receivable Decrease in inventories Increase in accounts payable Increase in income taxes payable Increase in interest payable Loss […]

Chapter 22 Review Each Noncurrent Account And Determine The

22-61 Note to Instructor: There are no interest and dividends collected and no other operating receipts. Since salaries expense information is not given, no breakdown of payments to employees is possible. The selling and administrative expenses are used to determine […]

Chapter 23 One example of an error that is counterbalanced

23-1 CHAPTER 23 ACCOUNTING FOR CHANGES AND ERRORS CONTENT ANALYSIS OF EXERCISES AND PROBLEMS Number Content Time Range (minutes) E23-1 Identification of Changes and Errors. (Easy) Indicate how to report various items, whether increases or decreases are to be expected. […]

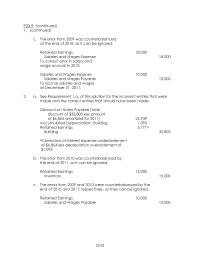

Chapter 23 this solution for the incorrect entries that were made

P23-9 (continued) 1. (continued) c. The error from 2009 was counterbalanced at the end of 2010, so it can be ignored. Retained Earnings 18,000 Salaries and Wages Expense 18,000 To correct error in salary and wage accrual in 2010. Salaries […]

Chapter 23 Adjustment for the cumulative effect on prior year

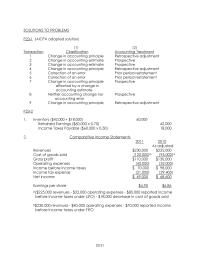

SOLUTIONS TO PROBLEMS P23-1 (AICPA adapted solution) (1) (2) Transaction Classification Accounting Treatment 1 Change in accounting principle Retrospective adjustment 2 Change in accounting estimate Prospective 3 Change in accounting estimate Prospective 4 Change in accounting principle Retrospective adjustment 5 […]

Chapter 3 Cash And Credit Sales Revenue Failed Record

P3-3 1. NEALY COMPANY Income Statement For Year Ended December 31, 2010 Sales revenue (net of $4,900 sales returns) $ 54,900 Cost of goods sold (27,400) Gross profit on sales $ 27,500 Operating expenses Administrative expenses $ 6,500 Selling expenses […]

Chapter 3 Liabilities Current Liabilities Accounts Payable Note Payable

3-21 E3-7 2010 Dec. 31 Bad Debts Expense 500 Allowance for Doubtful Accounts 500 To provide for possible bad debt losses ($25,000 x 2%). 31 Interest Receivable 500 Interest Revenue 500 To record interest earned but not collected. 31 Unearned […]

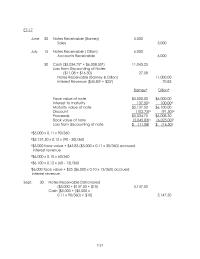

Chapter 3 Making reversing entries enables the company to

P3-12 (continued) 2. (continued) LANGER COMPANY Balance Sheet December 31, 2010 Assets Current Assets Cash $ 1,000 Accounts receivable $ 2,700 Less: Allowance for doubtful accounts (100) 2,600 Note receivable (due 5/1/11) 1,200 Rent receivable 50 Interest receivable 80 Inventory […]

Chapter 3 Plan Purchase The Equipment The Present Value

PM-17 Plan 1: PV = $600,000 Plan 2: Down Payment $200,000.00 12 payments P o of $65,000 for 12 years at 12%: $65,000 x 6.194374 402,634.31 Total PV $602,634.31 Plan 3: Down payment $200,000.00 First 3 payments: Po of $25,000 […]

Chapter 3 The Retained Earnings Balance Also Updated And

3-1 CHAPTER 3 REVIEW OF A COMPANY’S ACCOUNTING SYSTEM CONTENT ANALYSIS OF EXERCISES AND PROBLEMS Number Content Time Range (minutes) E3-1 Financial Statement Interrelationship. (Easy) Diagram. 5-10 E3-2 Journal Entries. (Easy) Sales, purchases, accounts payable. 5-10 E3-7 Adjusting Entries. (Moderate) […]

Chapter 4 Stockholders Equity Contributed Capital Preferred Stock 50

4-21 E4-10 STEVENS COMPANY Balance Sheet December 31, 2010 Assets Current Assets Cash $ 2,300 Temporary investments in marketable Long-Term Investments Investment in held-to-maturity bonds 10,000 Plant and Equipment Land $ 8,100 Buildings and equipment $35,600 Less: Accumulated depreciation (9,200) […]

Chapter 4 Subsequent Events That Provide Evidence Concerning Conditions

4-1 CHAPTER 4 THE BALANCE SHEET AND STATEMENT OF CHANGES IN STOCKHOLDERS’ EQUITY CONTENT ANALYSIS OF EXERCISES AND PROBLEMS Number Content Time Range (minutes) E4-1 Current Assets. (Easy) Partial balance sheet preparation from listed accounts. 5-10 E4-5 Balance Sheet. (Moderate) […]

Chapter 4 The more difficult explanations are explained in footnotes

4-41 P4-8 (continued) Stockholders’ Equity Contributed Capital Preferred stock, $100 par $12,000 Common stock, $5 par 25,000 P4-9 BRANDT COMPANY Balance Sheet December 31, 2010 Assets Current Assets Cash $ 3,800 Temporary investments in available-for-sale securities 4,600 Accounts receivable $18,500 […]

Chapter 5 as a current asset on the balance sheet and as a

5-61 P5-12 (continued) 2. Net income, 2007: $5,981 million; Basic net income (earnings) per common share for 2007: $2.59 (p. 66). 7. Cash dividends on common stock paid per share and in total in 2007: $1.36 per share; $3,149 million […]

Chapter 5 Cash dividends on common stock paid per share and in total

5-21 E5-4 1. Income statement; in the Other Items section 2. Income statement; as part of General and Administrative Expenses 6. Income statement; in the Other Items section 7. Income statement; in the Other Items section 8. Income statement; Depreciation […]

Chapter 5 Schedule Selling Expenses Sales Commissions And Salaries

SOLUTIONS TO PROBLEMS P5-1 1. MACK COMPANY Income Statement For Year Ended December 31, 2010 Sales $XXXX Less: Sales discounts taken $ XX Sales returns and allowances XX (XXX) Net sales $XXXX Cost of goods sold Merchandise inventory, 1/1/2010 $XXX […]

Chapter 5 Second Extraordinary Item Shown Net Applicable Income

5-74 P5-22 GIBB COMPANY Balance Sheet December 31, 2010 Assets Current Assets Cash $ 3,300a Liabilities Current Liabilities Accounts payable $ 3,000g Salaries payable 1,500h Total current liabilities $ 4,500 Long-Term Liabilities Bonds payable $ 6,000 Less: Discount on bonds […]

Chapter 5 Preparation of results from discontinued operations

5-1 CHAPTER 5 THE INCOME STATEMENT AND THE STATEMENT OF CASH FLOWS CONTENT ANALYSIS OF EXERCISES AND PROBLEMS Number Content Time Range (minutes) E5-1 Simple Income Statement. (Easy) Periodic inventory system. Multiple-step and single-step format preparation from selected account balances. […]

Chapter 6 Period Costs Costs Not Directly Associated With

P6-11 (continued) 1. (continued) PEREZ COMPANY Comparative Balance Sheets (Horizontal Analysis) December 31, 2009, 2010, and 2011 Base-Year-to-Date Increase (Decrease) December 31 2009 to 2010 2009 to 2011 2011 2010 2009 Amount % Amount % Cash Receivables (net) Inventories Noncurrent […]

Chapter 6 Return Stockholders Equity Net Income Average Stockholders

6-1 CHAPTER 6 ADDITIONAL ASPECTS OF FINANCIAL REPORTING AND FINANCIAL ANALYSIS CONTENT ANALYSIS OF EXERCISES AND PROBLEMS Number Content Time Range (minutes) E6-1 Segment Reporting. (Easy) Schedule showing segment revenues, profit, and assets. 10-15 E6-5 Interim Reporting. (Moderate) First quarter […]

Chapter 6 The large percentage changes in dividend revenue and interest

6-21 SLUSHER COMPANY Comparative Income Statements (Horizontal Analysis) (1) Year-to-Year Increase (Decrease) (2) Base-Year-to- Date Increase (Decrease) For Years Ended December 31, 2010 to 2011 2009 to 2010 2009 to 2011 2011 2010 2009 Amount % Amount % Amount % […]

Chapter 6 Weighted average Price Per Share For Options Exercised

6-41 P6-5 (continued) 2. (continued) The major weakness in the first quarter report is that it is misleading because the company is expecting a profit for the year, not a loss as normally would be 3. (1) The treatment of […]

Chapter 7 Accounts Receivable Sales Discounts Not Taken Sales

7-21 E7-17 June 30 Notes Receivable (Barney) 5,000 Sales 5,000 July 15 Notes Receivable ( Dillon) 6,000 Accounts Receivable 6,000 a$5,000 x 0.11 x 90/360 b$5,137.50 x 0.12 x (90 – 30)/360 c$5,000 face value + $45.83 ($5,000 x 0.11 […]

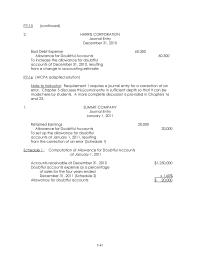

Chapter 7 Doubtful accounts expense as a percentage of sales

7-41 P7-15 (continued) 2. HARRIS CORPORATION Journal Entry December 31, 2010 Bad Debt Expense 60,300 from a change in accounting estimate. P7-16 (AICPA adapted solution) Note to Instructor: Requirement 1 requires a journal entry for a correction of an error. […]

Chapter 7 They Are Negotiable Instruments Which Means That

7-1 CHAPTER 7 CASH AND RECEIVABLES CONTENT ANALYSIS OF EXERCISES AND PROBLEMS Number Content Time Range (minutes) E7-1 Cash. (Easy) Determination of items to be included as cash on the balance sheet. 5-10 E7-6 Returns and Allowances. (Moderate) Record as […]

Chapter 8 It is typically preferable to use a FIFO measure

8-41 P8-6 (continued) 4. Inventory turnover = Cost of goods sold ÷ Ending inventory P8-7 1. a. FIFO: 2009 2010 2011 2012 Sales Cost of Goods Sold: Beginning inventory Production Goods available for sale Ending inventory* Cost of goods sold […]

Chapter 8 Lifo Finally Strict Application The Lifo Method

8-1 CHAPTER 8 INVENTORIES: COST MEASUREMENT AND FLOW ASSUMPTIONS CONTENT ANALYSIS OF EXERCISES AND PROBLEMS Number Content Time Range (minutes) E8-1 Inventory. (Easy) Manufacturing company. Computation of ending account balances. 10-15 E8-5 Discounts. (Easy) Gross price and net price methods. […]

Chapter 8 Note that the difference is seldom recognized formally

8-21 Date Ending Inventory At Current Costs x Base Year Cost Index Current Cost Index = Inventory At Base-Year Costs Increase (Decrease) at Base-Year Costs x Relevant Cost Index Base-Year Cost Index = Increase (Decrease) at Relevant Current Costs Ending […]

Chapter 8 The Differences From One Yearend Another Are

P8-14 (continued) 2. (continued) In 2011, the company experienced an unexpected increase in demand for our products that caused a decline in the physical size of the inventory. The resulting liquidation of LIFO layers caused a LIFO liquidation profit that […]

Chapter 9 Computation Cost Goods Sold During June 2010

P9-12 (AICPA adapted solution) RED DEPARTMENT STORE Computation of Estimated Inventory Using Retail Inventory Method December 31, 2010 Cost Retail Inventory at January 1, 2010 $ 32,000 $ 80,000 Purchases 270,000 590,000 Freight in 7,600 Net markups ($60,000 – $10,000) […]

Chapter 9 Continued Income Statement Beginning Inventory Purchases

E9-14 (continued) Ending inventory at cost: $120,000 x 0.625 = $ 75,000 $ 8,000 x 0.659 = 5,272 $ 80,272 E9-15 (AICPA adapted solution) Ending inventory converted to base-year prices = $660,000 x 110 100 = $600,000 There is a […]

Chapter 9 Retail Inventory and Dollar-Value Methods

9-1 CHAPTER 9 INVENTORIES: SPECIAL VALUATION PROBLEMS CONTENT ANALYSIS OF EXERCISES AND PROBLEMS Number Content Time Range (minutes) E9-1 Lower of Cost or Market. (Easy) Determination of inventory value. 5-10 E9-5 Purchase Commitment. (Moderate) Loss. Journal entries to record transactions. […]